First-Class Cabin Public Due Diligence: Programmable Liquidity Layer Native

Native's overall positioning is as a programmable liquidity layer, currently featuring three products: the protocol-oriented liquidity interface Native, the cross-chain trading aggregator NativeX, and the new lending tool Aqua aimed at market makers.

Native's overall positioning is as a programmable liquidity layer, currently featuring three products: the protocol-oriented liquidity interface Native, the cross-chain trading aggregator NativeX, and the new lending tool Aqua aimed at market makers.Native is positioned as the liquidity layer of blockchain, comprising three products: the liquidity interface Native that can be integrated by projects, the trading and cross-chain aggregator NativeX, and the new lending tool Aqua. NativeX integrates multiple decentralized exchanges and cross-chain bridges as sources of liquidity, and based on this, collaborates with some private market makers to provide users with zero slippage and a convenient trading experience. Its core product Aqua allows market makers to borrow funds from deposit users for market making, addressing the liquidity shortage faced by market makers. Since market makers use Aqua liquidity for settlement, the funds remain in the Aqua contract, significantly reducing risks compared to traditional institutional lending. Aqua increases the efficiency and yield of capital while controlling risks.

Project Overview

Native is overall positioned as a programmable liquidity layer, currently offering three products: the protocol-oriented liquidity interface Native, the cross-chain trading aggregator NativeX, and the new lending tool Aqua aimed at market makers. Native can help project parties directly connect to Native's liquidity on their own websites. NativeX is already a leading player in the cross-chain aggregation trading space; although the overall demand in this sector is relatively low, it reflects the team's operational capabilities to some extent. The design of its new lending product Aqua greatly enhances the capital efficiency of market makers while controlling risks, showcasing significant innovation. Native has secured two rounds of funding from Nomad Capital and is in the process of launching its core product Aqua.

Native can assist project parties in launching trading functions on their own websites, providing protocol users with a more convenient interactive experience. Protocols can easily integrate Native's liquidity into their own websites using Native's tools and can modify trading fees themselves.

Although cross-chain trading aggregation products are currently used less frequently, they have certain growth potential. Users have a significant demand for cross-chain bridges and trading aggregation, but often operate them separately, resulting in fewer users directly utilizing cross-chain trading aggregation. While cross-chain trading aggregation can provide a convenient trading experience, it has not been widely adopted due to issues such as liquidity and user habits. NativeX is already at the forefront in the cross-chain aggregation field, having integrated considerable liquidity and accumulated numerous market maker resources, capturing over 70% of DeFi order flow, which is beneficial for the subsequent launch of Aqua. As major L1 and L2 networks continue to emerge, the demand for cross-chain trading is increasing, and cross-chain trading aggregation may gain more user adoption.

Aqua as a new lending tool improves the capital efficiency of market makers while minimizing user capital risk. Institutional credit lending protocols often do not require collateral, allowing institutions to directly lend user funds after being vetted, with minimal disclosure regarding the use and direction of the funds, exposing users to significant institutional default risk. In contrast, all market makers borrowing through Aqua are over-collateralized and do not actually lend out funds; they only use the funds within the Aqua pool for trading settlements, engaging in two-way transactions with users and the Aqua pool before and after settlement. Subsequently, market makers generate corresponding long and short positions in the Aqua pool, allowing them to simultaneously conduct reverse operations on centralized exchanges to profit from price differences. For deposit users, the funds used by market makers as collateral remain in the Aqua pool, minimizing default risk, and users can achieve sustainable low-risk returns. For institutions, they gain liquidity on blockchains without assets and can open more positions, maximizing capital efficiency.

Native, NativeX, and Aqua as joint products can mutually provide pricing, order flow, and liquidity, forming a synergistic competitive advantage.

Overall, Native has accumulated considerable resources in cross-chain trading aggregation, facilitating the further development of its new product Aqua, and creating a synergistic effect among Native, NativeX, and Aqua. As a new product of Native, Aqua has pioneered a new paradigm of cooperation between liquidity providers and market makers. While ensuring the safety of deposit users' funds, it provides market makers with higher capital efficiency and convenience, creating a win-win situation. As a rare innovation in the DeFi space, there are currently no similar products, making Native worthy of attention.

1. Basic Overview

1.1. Project Introduction

Native is positioned as a programmable liquidity layer, currently offering the protocol-oriented liquidity interface Native and the cross-chain trading aggregation product NativeX to provide trading users with a more convenient trading experience. Native has launched a new lending protocol Aqua aimed at users and market makers on the testnet. Aqua enables market makers to obtain borrowing capabilities through collateral and uses the funds from the Aqua pool for user trading settlements, increasing capital efficiency while minimizing the default risk for market makers.

1.2. Basic Information

|------|---------------| | Established | November 2022 | | Sector | DeFi, Trading Aggregation & Lending | | Fundraising Status | Not disclosed |

2. Project Details

2.1. Team

According to LinkedIn data, the team consists of 3-10 members. Core members are introduced as follows:

Meina Zhou, CEO of Native. Holds a Master's degree in Data Science from New York University and has over 8 years of experience leading data science teams, with rich experience in machine learning, data mining, and project management. Meina Zhou is also the founder and host of the CryptoMeina podcast.

Wee Howe Ang, Advisor to Native, holds a Bachelor's degree in Electrical Engineering from the National University of Singapore. Formerly a software development manager (Assistant Vice President) at Deutsche Bank. Chief Technology Officer of cryptocurrency trading company Altonomy and Chief Technology Officer of cryptocurrency trading company Tokka Labs.**

Hung, Technical Lead at Native. Entered the crypto industry in March 2019, a full-stack engineer familiar with EVM-compatible smart contracts.

Native has a small team, but the division of labor is clear, with considerable industry experience in technology, trading, and promotional operations.

2.2. Funding

In April 2023, Nomad led a $2 million seed round. Nomad Capital received investment from Binance in March 2023 and invested in its first project Native the following month. In December 2023, Native received strategic investment from Nomad Capital.

Table 2-1 Funding Status

2.3. Products

2.3.1. Aqua

Early decentralized exchanges primarily used order book and RFQ (Request for Quotation) trading types. However, the cost of conducting order book trading on the Ethereum network is too high, with poor trading depth and matching difficulties. Therefore, the automated market maker mechanism has become the mainstream model for decentralized exchanges. For example, Uniswap uses a constant product market-making model, which achieves price self-discovery but has low capital efficiency, requiring substantial liquidity to reduce price impact, and liquidity providers still face the risk of impermanent loss, often earning less than simply holding tokens.

Native is launching a new paradigm of trading model with Aqua, which is a new lending product for ordinary users and market makers, combining the attributes of decentralized exchanges and lending products. It aims to increase the capital efficiency of market makers and the deposit yield for users while ensuring the safety of user funds. Typically, market makers' funds are stored in centralized exchanges and individual blockchains. If there is a certain market-making demand on a new blockchain, they need to allocate part of their funds and bear the security risks of that blockchain, which may lead market makers to forgo some market-making profits.

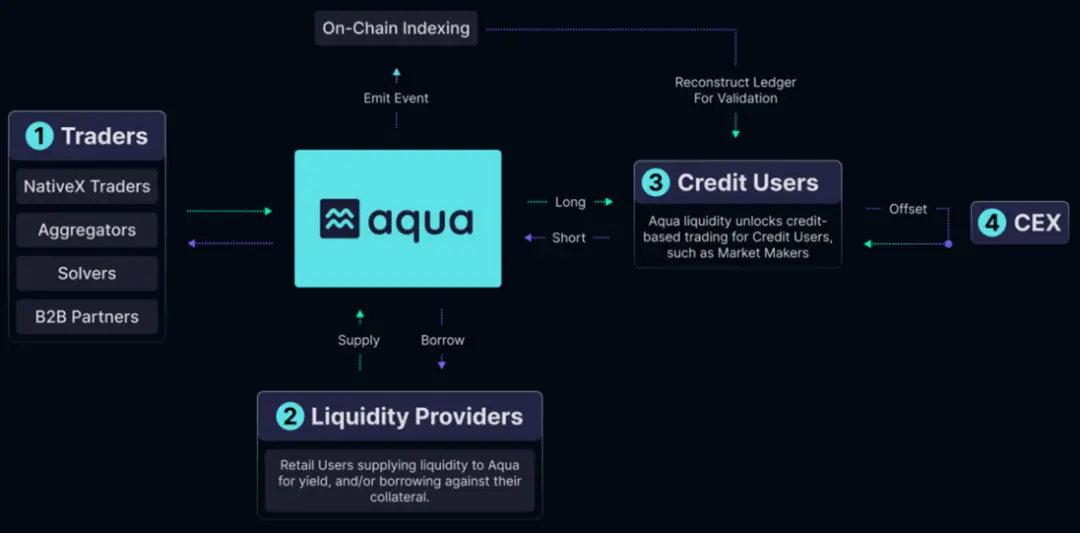

Through Aqua, market makers use asset collateral to borrow for market making on new blockchain networks (collateral can exist on other chains), generally using the RFQ mechanism, which is highly efficient without issues like slippage and MEV. The funds come from deposit users/liquidity providers (deposit users can also obtain some borrowing capacity). For example, if a user sells ETH for USDT, the market maker provides a quote and settles using Aqua's funds (deposited by users), after which the market maker generates a short position in USDT and a long position in ETH (equivalent to the market maker borrowing USDT from the pool and depositing ETH, but the funds remain in the Aqua contract). Within its borrowing limits, the market maker can maintain multiple positions simultaneously, maximizing liquidity and capital efficiency.

Aqua not only improves the capital efficiency of market makers but also addresses the liquidity shortage faced by market makers on certain blockchains. A significant highlight is that the money borrowed by market makers remains within the Aqua contract, manifested as long and short positions, making the asset table of market makers more transparent and preventing the misuse of borrowed assets, with risks significantly lower than traditional institutional lending protocols.

For borrowing users, the returns are augmented by the interest on the funds used by market makers (interest costs for opening positions), and the deposited funds have more borrowing scenarios, yielding higher returns compared to traditional lending protocols, without facing the credit risk of market makers (as funds remain in the Aqua contract). Moreover, market makers have a continuous demand for trading settlements, meaning deposit users' returns are also relatively stable and sustainable.

Figure 2-5 Aqua Operational Logic

Market makers using Aqua are all over-collateralized, and the collateral and settlement funds do not need to exist on the same blockchain. Aqua employs a fixed interest rate lending model, adjusting according to market conditions and capital utilization rates. Interest will be calculated off-chain (determined by the number of blocks passed and position changes), and the calculated interest amount will be periodically sent on-chain. Aqua uses off-chain quotes; when a market maker's borrowing exceeds its borrowing limit, whitelisted liquidators can propose liquidation, Aqua will verify the proposal and return a signature, and the liquidators will then perform the liquidation on-chain.

2.3.2. Native & NativeX

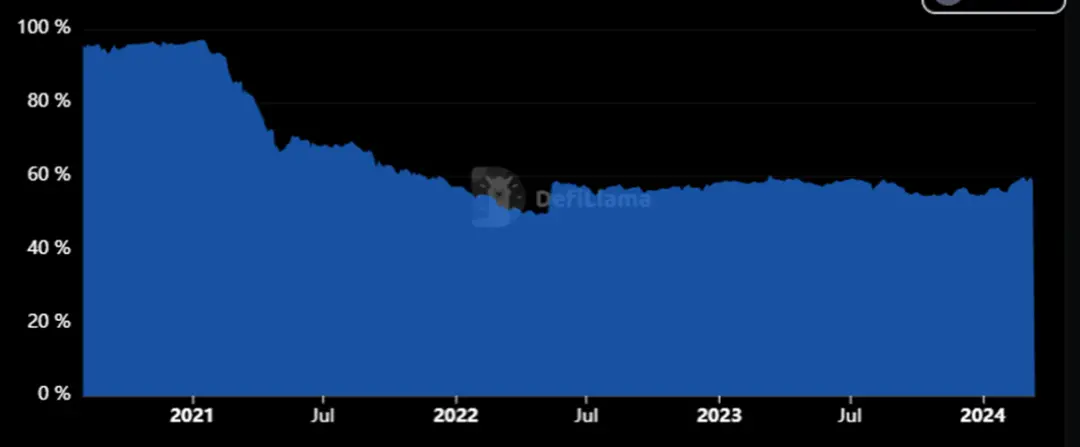

Since the Ethereum GAS issue has been criticized, the crypto market is gradually moving towards multi-chain. From the perspective of TVL, Ethereum's network TVL has maintained around 58% for nearly two years, indicating that other blockchains have certain market competitiveness and maintain a certain level of liquidity. From the narrative of public chains, Ethereum focuses on serving Layer 2 networks, and more funds will migrate to Layer 2 networks in the future. It can be expected that the future crypto market will be multi-chain parallel rather than a single Ethereum monopoly.

Figure 2-1 Ethereum TVL Market Share [1]

With the launch of more blockchains, liquidity has become fragmented. Whether it is Layer 1 blockchains like Solana and Aptos or Layer 2 networks like Ethereum, there is a huge demand for liquidity.

For traders, the current price order book trading model and deep liquidity of centralized exchanges can reduce trading costs, but it also means users need to give up ownership of their assets and cannot trade tokens that are not listed. While decentralized exchanges allow users to retain ownership of their assets, they are limited by on-chain liquidity, forcing traders to bear slippage, price impact, and MEV losses.

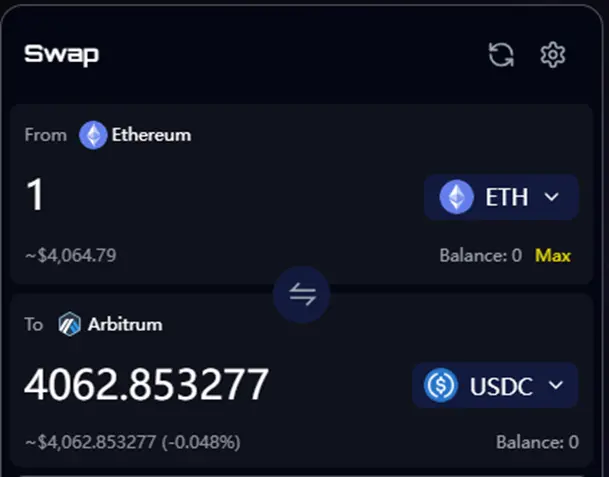

Native is a liquidity solution that integrates multiple sources of cross-chain liquidity. Its product Native can help project parties integrate Native's liquidity and launch trading functions on their own websites. Another product, NativeX, has both cross-chain bridge and trading aggregation functions, supporting users in cross-chain trading. As of March 18, 2024, NativeX supports 10 EVM-compatible chains, including Ethereum, Arbitrum, Polygon, BNB Chain, and Base, and is continuing to add more blockchains.

Figure 2-2 NativeX Swap Interface Display

Based on the aggregation of multiple DEXs (including aggregators) and cross-chain bridge liquidity, NativeX collaborates with several private market makers to provide traders with better quotes. Private market makers differ from traditional automated market makers; they are individual entities providing a Request for Quotation (RFQ) mechanism similar to limit orders on centralized exchanges, and they use their own algorithms and pricing models to provide liquidity to their partners (such as trading aggregators). The RFQ mechanism offers greater flexibility compared to automated market maker mechanisms and significantly improves capital efficiency.

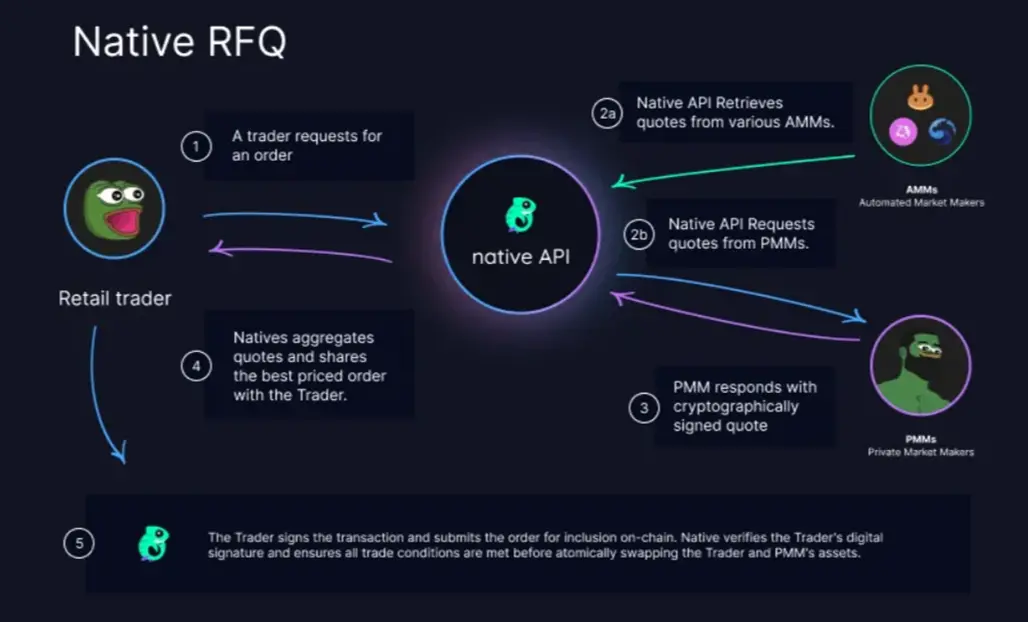

When users place order requests, Native will obtain quotes from multiple decentralized exchanges, and Native will also obtain quotes from private market makers, who respond with encrypted signed quotes (avoiding front-running, price impact, and slippage losses). After aggregating quotes, Native provides traders with the optimal pricing strategy. If a deal is made with a private market maker, Native will verify the trader's digital signature, and when the trading conditions are met, an atomic swap occurs between the trader and the market maker; otherwise, the order will be automatically canceled to ensure the safety of both parties' funds.

Figure 2-3 Native Quote Aggregation Mechanism

There are no trading fees or price impact losses when users transact with private market makers. Thus, Native reduces trading costs for users while retaining ownership of their assets.

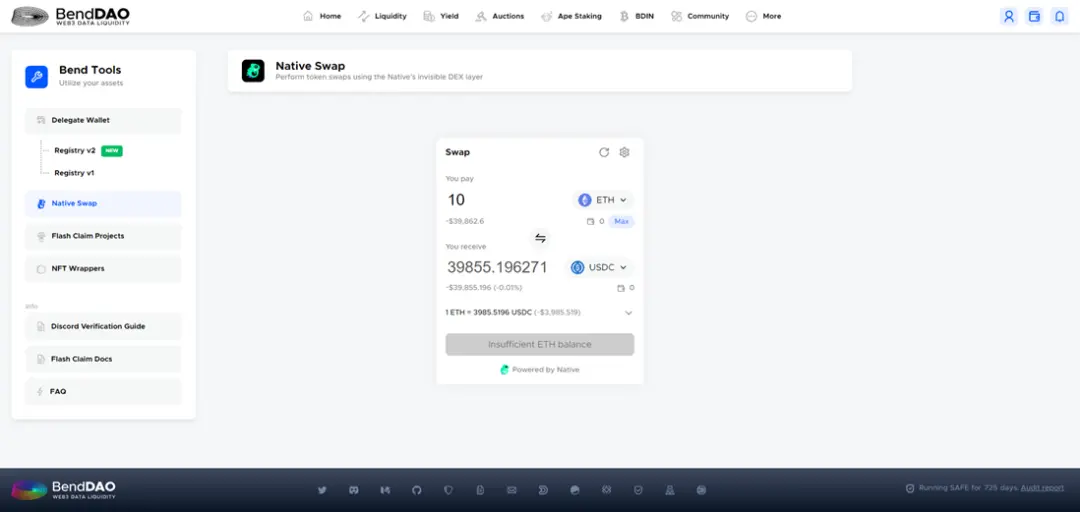

NativeX is aimed at traders, while project parties can connect to Native's liquidity sources through the built-in Native program, allowing them to add trading functions and choose to charge trading fees (default 0%) and provide additional token rewards to liquidity providers. Currently, BendDAO, Aboard, Range Protocol, and Velo have integrated Native for a more convenient trading experience, and ZetaSwap directly uses Native for construction.

Figure 2-4 BendDAO Native Trading Interface [2]

For market makers, accessing Native's liquidity can yield more order flow, and aggregators connecting to Native can obtain more quote sources, facilitating further price optimization.

Summary: The Native team includes executives from two cryptocurrency trading companies with considerable market-making experience. The protocol's products consist of NativeX and Aqua. NativeX serves as an aggregator for cross-chain bridges and trading, helping users conduct more convenient transactions. Aqua, as the team's new product, has pioneered a new paradigm of cooperation between liquidity providers and market makers, addressing the liquidity shortage faced by market makers on certain blockchains while enhancing their capital efficiency. At the same time, deposit users have more demand for their funds, increasing their deposit yields while ensuring the safety of their funds as much as possible.

3. Development

3.1. History

Table 3-1 Major Events of Native

From Native's historical progress, the speed of product delivery and the addition of supported networks are rapid, gaining a certain market demand in a short period.

3.2. Current Status

Since its launch in April 2023, Native has accumulated a trading volume of $2.45 billion and a total of 3 million transactions, with the assets of its partnered private market makers exceeding $100 million.

Figure 3-1 Cumulative Data of Native [3]

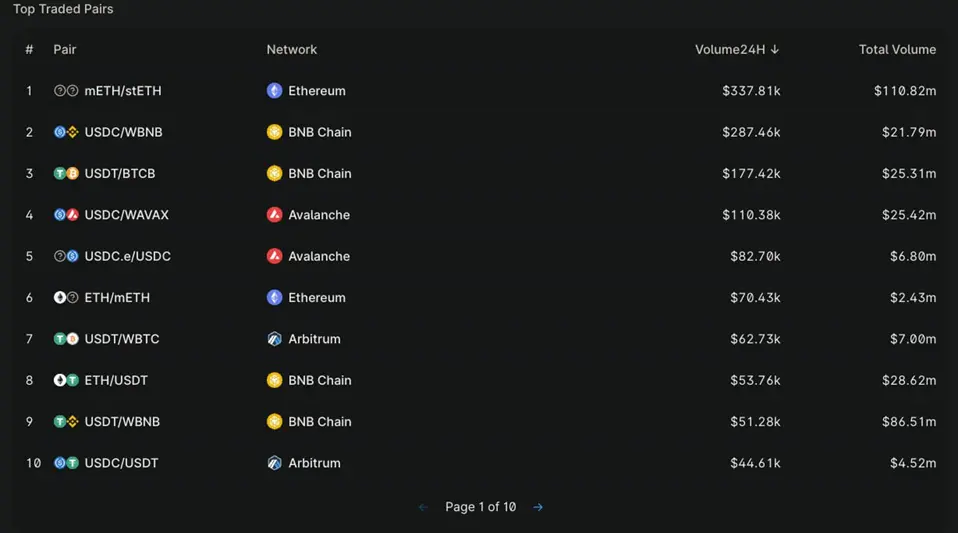

The main sources of trading volume for the protocol come from Ethereum, Avalanche, and BNB Chain, primarily involving WAVAX, USDT, and ETH tokens. Assuming traders consider factors like slippage, Native's main competitive edge lies in the aforementioned trading pairs, with private market makers partnered with Native primarily providing liquidity for mETH, AVAX, and BTC tokens on Ethereum and BNB Chain.

Figure 3-2 Top 10 Trading Pairs of Native

3.3. Future

Native is completing the final testing of Aqua (including auditing of on-chain contracts and off-chain structural execution). Subsequently, Native will deploy Aqua and launch the mainnet, gradually supporting perpetual contract RFQ and on-chain credit mechanisms based on zero-knowledge proofs.

Summary: The Native team has a fast overall product delivery speed and has gained a certain market share. The team is launching its lending product Aqua aimed at market makers and will subsequently integrate it into the perpetual contract field and introduce on-chain credit mechanisms based on zero-knowledge proofs. The performance and data of Aqua after its launch will be crucial for Native.

4. Economic Model

Native has not yet issued a token and has not disclosed its economic model.

5. Competition

5.1. Industry Overview

Native currently has two products: the cross-chain trading aggregator NativeX and the lending protocol Aqua aimed at market makers. Cross-chain trading aggregation has always been a niche sector, while institutional lending protocols often grant KYC institutions the right to unsecured loans, with low transparency regarding the direction and retention of funds, making it difficult to ensure the safety of user funds.

Users have always had significant demand for trading aggregation; for example, as of March 18, 2024, the trading volume achieved through aggregators accounted for 36.7% of the total DEX trading volume. Although trading aggregation has a large user base and demand, the niche sector of cross-chain trading aggregation has struggled to win the market. Among the top ten aggregators by trading volume, only the tenth-ranked Jumper Exchange (a product under LI.FI) is a cross-chain trading aggregator. Overall, cross-chain trading aggregation remains a niche sector, with users more familiar with well-known aggregators like 1inch, Jupiter, and CowSwap.

Figure 5-1 Ranking of Aggregator Trading Volumes

Institutional lending protocols often do not require full collateral, allowing cooperating institutions to lend directly without collateral, with very low transparency regarding the use of funds, and users may not even know the amount borrowed and the lender. Depositors face significant institutional default risks and low fund security. For example, in the RWA sector, Goldfinch experienced two security issues from September to October 2023. Goldfinch is considered a cautious protocol in the sector, yet there are still many instances of insufficient borrowing information and disclosure. This illustrates that institutional lending protocols severely lack transparency and carry significant institutional default risks, resulting in low levels of TVL in the sector.

5.2. Competitive Analysis

5.2.1. Aqua

Native's new product Aqua features strong product logic innovation. Aqua incorporates characteristics of both decentralized exchanges and lending protocols, pioneering a new cooperation paradigm between market makers and liquidity providers. The funds deposited by liquidity providers are stored within Aqua's contract, allowing market makers to use the funds in the Aqua pool for market making after over-collateralization. When a market maker conducts a transaction, they settle using the funds from the Aqua pool. This is equivalent to holding a long position and a short position in the pool (rather than lending funds out for market making), and market makers can simultaneously conduct reverse operations on centralized exchanges to profit from price differences.

Traditional lending protocols like Compound and AAVE primarily focus on users increasing leverage, shorting, and interest rate arbitrage, requiring sufficient market volatility to create borrowing demand, such as increased stablecoin interest rates from market rebounds and higher ETH deposit yields from staking. Compared to Compound, the funds deposited in Aqua have more borrowing demand and higher yields. Additionally, lending protocol interest rates are often affected by market fluctuations, while market maker demand is more stable. Thus, users' returns are relatively more stable and sustainable. Throughout the process, users' funds remain within Aqua's contract, and all market makers are over-collateralized, with transparent positions. Compared to directly transferring funds to market makers or institutions, the security of Aqua's lending model is significantly enhanced.

For market makers, settling through Aqua allows them to open more positions simultaneously, maximizing their capital efficiency compared to directly lending out funds. Moreover, through collateralization, they can access liquidity across multiple blockchains, greatly enriching their market-making scenarios, making it an innovative product in DeFi. Private market makers utilize the liquidity deposited by users and provide quotes through the RFQ mechanism, offering better quotes per unit of liquidity than automated market makers, potentially disrupting the current dominance of automated market maker mechanisms in decentralized exchanges.

5.2.2. Native & NativeX

In the cross-chain trading aggregation sector, NativeX's $3.5 million trading volume over 24 hours ranks it among the top players in this niche (aggregator overall ranking 12), with trading volume second only to Jumper Exchange in this sector. Jumper Exchange is developed by LI.FI, which raised $5.5 million and $17.5 million in funding in July 2022 and March 2023, respectively, with the seed round led by 1kx, making it the strongest player in this sector. As a newly established fund backed by Binance, Nomad also has a good reputation in the DeFi space, placing Native at a first-tier level in terms of funding background.

The product logic of cross-chain trading aggregation is relatively simple; protocols aggregate more liquidity sources from cross-chain bridges and decentralized exchanges and collaborate with certain private market makers to provide additional liquidity sources. Ultimately, cross-chain trading aggregation synthesizes quotes and selects the optimal solution for traders, offering a more convenient and efficient trading experience. Similar to NativeX, LI.FI's promotion strategy mainly involves integration with other protocols' websites, and LI.FI has launched pre-built user interface component tools, allowing project parties to integrate Jumper Exchange's swapping services into their websites, achieving a one-stop cross-chain trading aggregation service.

Since its launch in April 2023, as of March 19, 2024, Native has aggregated 3 million transactions and $2.45 billion in trading volume, while LI.FI has aggregated 5 million transactions and $4 billion in trading volume. Native launched later, with its total trading data approximately 60% of LI.FI's, and its daily trading volume of $3.5 million is about 53% of LI.FI's.

Figure 5-2 LI.FI Aggregation Data

Currently, NativeX supports 10 EVM chains. Although it has fewer in number than LI.FI, NativeX supports most major EVM networks and is rapidly expanding to other networks. From the data perspective, NativeX is at the forefront of cross-chain trading aggregation.

Figure 5-3 LI.FI Multi-Chain Liquidity

Summary: Native's product NativeX is already at the forefront in the cross-chain trading aggregation sector, demonstrating considerable market competitiveness. However, overall, cross-chain trading aggregation remains a niche sector with relatively low demand. Its new product Aqua has many innovations, using a unified pool to manage funds, with market makers settling trades using Aqua pool liquidity. This not only significantly increases the capital efficiency of market makers and helps them access liquidity across more blockchains but also ensures the safety of users' funds as much as possible.

6. Risks

1) Code Risk

Native's code has been audited by Salus, Veridise, and Halborn, and its immunefi bounty program will soon be launched, but code risks still exist.

2) Delayed Liquidation

Liquidation of Aqua is conducted periodically by whitelisted liquidators. If a market maker has significant token exposure and encounters extreme market conditions, there is a possibility of delayed liquidation leading to losses for liquidity providers.