The Derivative Disasters of the Crypto Winter: The Tragedy of Silvergate and Abra

The revival of the cryptocurrency banking sector directly depends on the temperature of the macro environment for cryptocurrencies.

The revival of the cryptocurrency banking sector directly depends on the temperature of the macro environment for cryptocurrencies.Original Title: "The Tragedy of Crypto-Friendly Banks: Silvergate's Collapse and Abra's Misfortune"

Source: R3PO

On January 5, according to The Wall Street Journal, crypto-friendly bank Silvergate has processed $8.1 billion in withdrawal requests following the collapse of FTX, with cryptocurrency deposits plunging 68% in Q4. To meet withdrawal demands, Silvergate liquidated the debt it held on its balance sheet and incurred significant markdown losses.

Silvergate's stock price once soared above $200 during the peak of cryptocurrency prices in 2021, but now it stands at just $11, with nearly 95% of its market value evaporated. The fall of Silvergate undoubtedly serves as a wake-up call for Web3 investment institutions, and the development of the crypto banking sector may be negatively impacted.

R3PO will analyze the impact of this incident on the crypto banking sector from three perspectives: the Silvergate event, the crypto banking sector, and the case of competitor Abra.

Silvergate Suffers Huge Withdrawals Due to FTX Incident

Initially, Silvergate (SI) was a community retail bank located in California, primarily providing financial services to local small and micro enterprises. With its transformation into a crypto-friendly bank, providing banking settlement services for Coinbase, Gemini, and the now scandal-ridden FTX trading platform and trading firm Alameda Research, Silvergate achieved a qualitative shift and went public on the NYSE at the end of 2019.

In the past three months, SI's stock price has fallen over 80%, reflecting investors' concerns about two factors: 1) SI may have credit exposure to FTX/Alameda in its Bitcoin collateral loan portfolio (approximately $300 million as of September 30, accounting for about 27% of tangible common equity); 2) Due to the market crash, SI is experiencing significant deposit outflows.

These investor concerns were recently validated by the market.

Digital Currency Deposits Plummet Nearly 70%

By the end of Q4, the total amount of digital currency deposits dropped to $3.8 billion, a 68% decrease quarter-over-quarter, with deposits as low as $3.5 billion during the quarter. Silvergate's clients incurred a $150 million loss related to bankruptcies. According to Silvergate's 8-K disclosure on November 16, its digital currency deposit size was $9.8 billion, down $2.2 billion from the average digital currency deposits of $11.9 billion in Q3 2022.

Source: S&P Global

Selling Assets to Address Withdrawals

To meet withdrawal demands, Silvergate sold $5.2 billion in bonds held on its balance sheet in Q4 2022, incurring significant markdown losses. Since 2013, the bank's losses from selling debt have far exceeded its total profits, resulting in a loss of $718 million. By the end of Q3, the company still had approximately $427 million in HTM securities investment losses not accounted for at book value. From management's statements regarding the end-of-period balance sheet, the fair value of securities at the end of the quarter was about $5.3 billion (with company cash around $4.6 billion).

Layoffs and Business Cuts

Silvergate announced a 40% layoff of about 200 employees, which is expected to result in a cumulative cost of $12 million related to employee severance and benefits. The company also stated it would cut back on business, deciding to shelve its plan to develop a digital currency through the acquisition of Diem for $196 million, as the company is "no longer in a hurry to launch blockchain payment solutions in the current market environment."

R3PO believes that Silvergate Bank will be affected by several factors moving forward: 1) the company may face further potential regulatory fines; 2) a weaker cryptocurrency market ahead, stricter crypto regulations, and lower-than-expected deposit growth; 3) significant uncertainty in the cryptocurrency regulatory environment may lead to continued declines in the company's stock price. SI's business and development may remain sluggish for an extended period.

2023 May Mark the End for Some Unprofitable Crypto Banks

In recent years, although the adoption rate of crypto assets has gradually increased, banking financial services for crypto assets are far from widespread, leading to growing interest in the field. Crypto-friendly banks have attempted to capture deposits flowing into the digital asset ecosystem, with some trying to use cryptocurrencies or crypto mining equipment as collateral for loans.

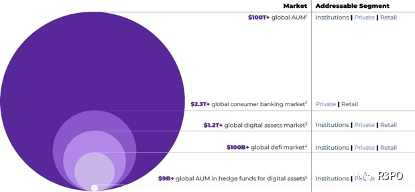

As of October 2022, about 80 financial institutions regulated by the Federal Deposit Insurance Corporation expressed interest in cryptocurrency-related activities, with around 24 actively participating, hoping to tap into the $1.2 trillion global digital asset market. Crypto-friendly banks serve as a bridge between fiat and digital currencies, catering to the broadest range of institutional and retail users.

Source: Abra Company Data

Industry Segmentation

In the broader industry of cryptocurrency storage, there are segmented markets such as custody, banking, and CeFi, with each segment offering a diverse product mix. Compared to Coinbase's trading platform attributes, Signature and Silvergate only provide basic cryptocurrency deposit and withdrawal transfer functions, while CeFi institutions like Celsius and BlockFi offer complex financial products that lack regulatory oversight. The development path of crypto banks is to cover as many product needs and functions as possible on the compliance road to generate revenue.

Source: Abra Company Data

Crypto Asset Bank Business Model

The main sources of income for banks are interest income and non-interest income. Non-interest income, also known as fees, is not the primary source of a bank's income; the core of bank revenue lies in net interest income. When you deposit cash into a bank account, the bank may offer you a 1% interest rate, which is an interest expense for the bank (what they pay you). Then, that cash will be lent to another customer at a 3% interest rate, which is the bank's interest income. Net interest income is the spread between interest income and interest expenses, and in a competitive market, the only way to create this spread is to take on some risk. The two most common risks are: credit risk: the risk that the borrower will not repay; interest rate risk: the risk of changes in market interest rates if you lend for more than one day.

In cryptocurrency, there are two important risks: liquidation risk: loans are over-collateralized, but you expect to liquidate the collateral to avoid any losses; protocol risk: the blockchain is code, and the code may be exploited, leading to losses. The banks we are analyzing today are all full-reserve banks, not taking on these risks.

In the real world, the differences in deposits between banks are quite small due to regulations, such as the Basel III Accord, which uses liquidity coverage ratios (LCR) and high-quality liquid assets (HQLA) to define how much high-level funding banks should retain, creating homogeneity.

As we can see, every bank has a goal: to increase the amount of deposits so they can earn the spread between funding rates and investment rates, as well as other fees.

R3PO believes that crypto banks, like traditional banks, derive their business profits from non-interest income and net interest income generated in the flow of funds through the deposit-loan chain. The business model of crypto asset banks benefits from the following activities:

- Charging transaction fees based on fluctuations in the overall capacity and trading volume of the cryptocurrency market,

- Attracting cryptocurrency deposit accounts to charge account-related fees,

- Charging interest to customers borrowing against cryptocurrency collateral,

- Charging fees for the flow of funds generated from linking DeFi and NFT gateways,

- Charging interest fees to credit card users and receiving rebates from card issuers and merchants,

- Charging management fees and performance fees for proprietary asset management businesses.

R3PO believes that for cryptocurrency banks, how to manage the balance sheet to meet solvency and liquidity constraints while optimizing the spread between funding and investment rates will determine who becomes the king of the sector, with the winner being a trillion-dollar company.

However, as the market capitalization of cryptocurrencies has fallen from nearly $3 trillion in November 2021 to below $1 trillion currently, investment institutions' confidence in the cryptocurrency industry is wavering, and the businesses of participants in the crypto banking sector are also significantly impacted.

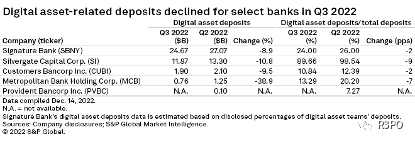

· Provident Bancorp Inc. delayed submitting its Q3 10-Q form due to assessing the actual loss levels of distressed cryptocurrency miners.

· Metropolitan Bank reported a $485.9 million decline in cryptocurrency-related deposits in Q3 2022, with about 70% coming from Voyager Digital Ltd.

· Signature Bank's clients held $24.67 billion in digital asset-related deposits as of Q3 2022, and the bank indicated it would reduce cryptocurrency-related deposits to $8-10 billion by Q1 2023.

· Silvergate Bank's Q3 2022 client digital asset deposits were $11.9 billion, while recently disclosed Q4 data showed that deposits fell to $3.8 billion, a 68% decrease quarter-over-quarter.

R3PO believes that as leading players in the crypto banking sector retract their businesses, some still unprofitable crypto banks will face a dual dilemma of revenue generation and financing in 2023, or even reach their end.

Abra Bleeds During the Bear Market

R3PO has learned that as a popular player in the crypto banking sector, Abra just completed a $22.6 million bond financing in December 2022, while also disclosing that it is undergoing layoffs and business restructuring. According to online media citing three informed sources, the crypto investment management company Abra is restructuring several of its business lines and considering cost-cutting measures as a buffer against the bear market.

Founded in 2014, Abra is a global crypto asset financial services company offering services including crypto asset trading, custody, investment, interest earning, lending, payments, and credit cards. Due to the rapid expansion of the crypto market in 2021, Abra's business experienced explosive growth. In September 2022, Abra announced plans to launch a digital asset bank, Abra Bank, which is expected to obtain the first fully regulated U.S. bank license in January 2023, allowing U.S. citizens to use digital assets for deposits and banking in a manner similar to traditional banking. The bank plans to establish branches in various states across the U.S. and become the first regulated cryptocurrency bank in the country, with plans to later launch a global project, Abra International, to serve clients outside the U.S.

Key Information Summary for Abra in 2022:

· Partnering with American Express as an issuing bank to offer customers a 2.5% cashback crypto credit card.

· Focusing on solving industry pain points for crypto institutional users, which may smooth out industry cycle fluctuations.

· Significant losses in 2022, with the company facing a considerable survival crisis.

· Expected to obtain a fully regulated U.S. bank license in January 2023.

Abra's business data from 2020-2021 is impressive, and notably, Abra's international layout, with the launch of Abra International targeting overseas markets (Canada, EU, Japan, etc.).

Source: Abra Company Data

Highlights of Abra's 2023 Roadmap:

· DeFi/NFT: Providing access to DeFi applications and protocols for institutional and individual clients, offering NFT custody services.

· Cash Management: Offering real-time conversion services between crypto assets and fiat currencies.

· Credit Card: Partnering with American Express to offer customers a 2.5% cashback crypto credit card.

· U.S. Bank License: Wyoming SPDI bank charter; Ex-U.S. bank license: Bermuda DABA.

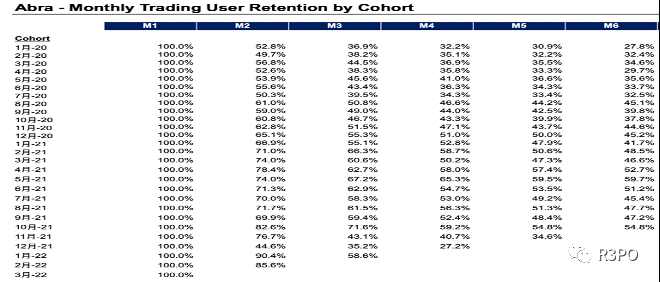

However, data from the first half of 2022 shows that Abra's user retention rate, which is typically high in the banking industry, fell below 50% for users who have used Abra for more than six months. Even considering the negative impact of the macro environment, this data still has significant room for improvement. Additionally, the average monthly trading volume per user also decreased by 90% in February-March of this year, and this data may continue to remain low in the contracting cryptocurrency environment of 2022-2023.

Abra's Financial Situation is Concerning

· Abra has a high debt-to-asset ratio, with its parent company Plutus Financial holding a total of $533 million in assets in its H1 2022 balance sheet, of which $496 million is in stablecoins and various cryptocurrencies, with debts amounting to $525 million.

· Abra faces issues of reducing expenses, downsizing, losses, and improving profit margins. Plutus Financial's H1 2022 profit and loss statement shows a decline in revenue quarter-over-quarter, with losses rapidly expanding. In the first half of 2022, total revenue was $23 million, but losses reached $42 million, with gross profits being negative in March and June.

· Based on the company's losses from April to June, Abra's cash flow encountered problems in the second half of 2022. In H1 2022, the company had $12 million in cash, while cash flow was -$26 million. Recent disclosures of bond financing information in December also corroborate this, and it remains to be seen how long the $22.6 million can sustain Abra, prompting timely layoffs and adjustments in business lines.

Financing and Valuation

· In December 2022, Abra secured $22.69 million in bond financing, with its current valuation being unclear, and there is a possibility of a flat or even downward adjustment in valuation.

· In September 2021, Abra raised $55 million in financing led by Ignia and Blockchain Capital, with other investors including Kingsway Capital, AmEx Ventures, and CMT Digital Ventures. Based on the previous round of financing and changes in the Cap Table, it is roughly estimated that the previous round of financing accounted for about 22% of Abra, suggesting a post-financing valuation of approximately $250-$300 million.

R3PO's Perspective on Abra's Future

Abra's business performance during the 2020-2021 period was impressive, showcasing excellent growth capabilities and a strong product mix. The dual benefits of obtaining a compliant banking license and partnering with Amex for credit card issuance in 2023 may allow it to maintain a certain growth rate and attract traditional users during the bear market.

Abra's financial model predictions and past valuations are based on optimistic expectations for the macro crypto market, while the sluggish macro environment poses significant risks to Abra's customer acquisition capabilities and user retention. The decline in trading activity will lead to decreased operating revenue and profits, and the low returns in the market will reduce the attractiveness and expected returns of Abra's asset management products.

Conclusion

As 2023 arrives, whether Abra's subsequent business and licensing plans can be realized will determine its future customer growth and financing progress. The revival of the crypto banking sector directly depends on the macro environment of cryptocurrencies, and under increasingly strict regulatory conditions, crypto banks will drift further away from blockchain fundamentalism and gradually embrace regulatory trends.

R3PO believes that only a cryptocurrency market with sound asset safety policies can attract traditional capital. The competition for licensing compliance in the crypto banking sector continues to intensify, but the path to internationalization will become more challenging due to the difficulties in obtaining regulatory licenses in various regions. In the future, the entry barriers for the U.S. crypto banking market will gradually increase, and smaller participants may emerge in relatively conservative national markets.

Whether high-speed growth can be restored on the basis of compliance will continue to test each crypto bank's technical strength, the completeness of the blockchain payment network, and the comprehensiveness of the product mix. R3PO will bring more analysis on cryptocurrency credit cards and crypto bank licenses in future articles.