USDC is finally at ease, and the data tells you what exactly happened?

The cryptocurrency industry has once again gone through a major crisis, but has a turning point arrived?

The cryptocurrency industry has once again gone through a major crisis, but has a turning point arrived?Author: Kaiko

Compiled by: Peng SUN, Foresight News

On March 11, just hours after the collapse of Silicon Valley Bank, stablecoin issuer Circle announced that $3.3 billion of reserves were held at Silicon Valley Bank, triggering market panic and causing massive chaos in both centralized and decentralized markets. On the morning of the 13th, Circle CEO Jeremy Allaire announced that USDC reserves were 100% safe, and institutions like the Federal Reserve also stated that depositors could withdraw all cash from Silicon Valley Bank, gradually easing market panic.

It felt like another roller coaster ride; the crypto market plunged into extreme panic overnight and then returned to normalcy just as quickly. So, what exactly happened with USDC? What caused USDC to depeg, what were the resulting impacts, how was liquidity in the crypto market during the crisis, and how did the market recover? This article reviews the USDC crisis and uses data to explain what happened at that time.

1. The USDC Depeg That Triggered Massive Market Chaos

(1) The Huge Impact of CEX

USDC is primarily used in the DeFi ecosystem, so its liquidity on CEX is relatively low. As of last week, USDC accounted for less than 0.5% of total trading volume on CEX. However, CEX had a significant impact in igniting the market chaos over the weekend.

This is because, in uncertain situations, traders only think of one thing: where to liquidate their USDC holdings.

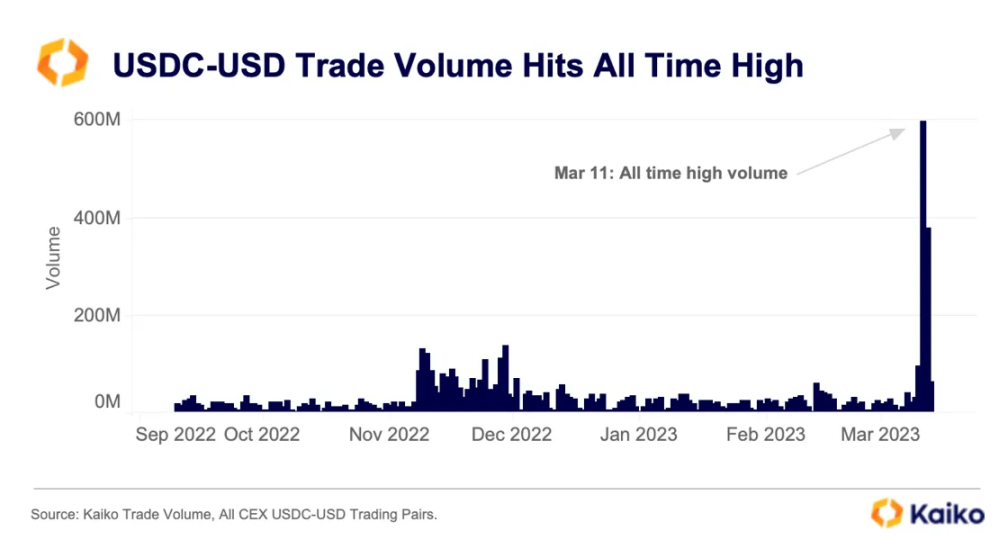

Today, there are only 8 active USDC-USD trading pairs on CEX, which effectively serve as the real-time exchange rate for converting USDC to USD. Over the weekend, with Circle and Coinbase suspending USDC to USD conversions, these trading pairs were the only channels for withdrawals.

The problem is that the liquidity of these USD trading pairs is relatively poor: in the first week of March, the average daily trading volume was only $20-40 million. Last Saturday, the trading volume of these pairs reached a historic high of $600 million, primarily driven by Kraken, which provided the best liquidity for the USDC-USD trading pair.

As expected, the order book could not support a large number of sell orders, leading to a sharp drop in the USDC exchange rate. Before the depeg, there were less than $20 million in bids on the USDC-USD order book, which could not support the billions in sell orders.

Although the USDC-USD trading pair saw unprecedented trading volume, most crypto market activities were not conducted in USD. Most traders used offshore exchanges, which do not provide direct USD conversion for USDC but offer USDC-USDT trading pairs. The issue here is that the world's largest exchange, Binance, had delisted all USDC trading pairs as early as last September.

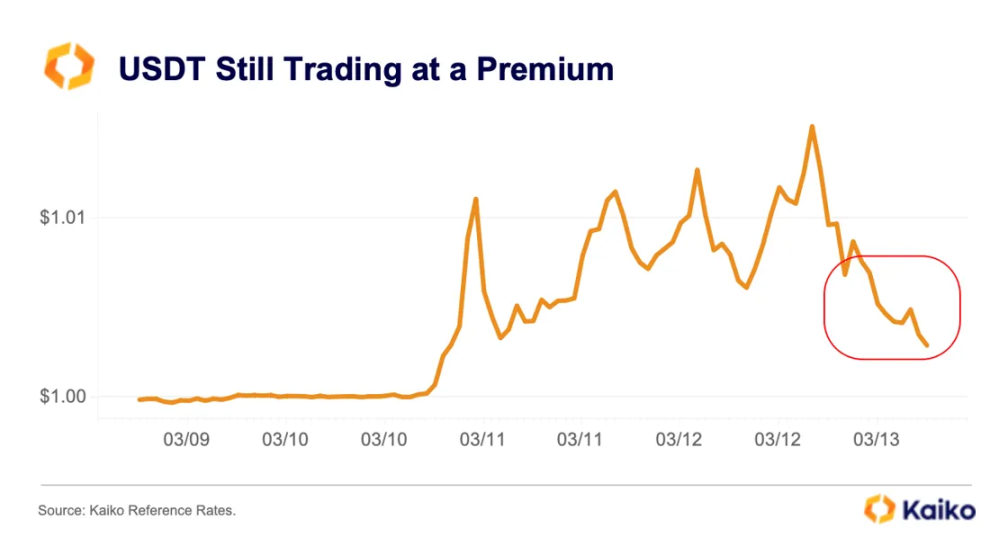

By Saturday afternoon, Binance finally re-listed the USDC-USDT trading pair, but by then, USDC was already trading at a significant discount on the illiquid CEX. Shortly thereafter, the trading volume of the USDC-USDT trading pair reached $9.9 billion, setting a new record, as traders alternately sold or bought USDC at the depeg price.

Overall, there were more sell orders than buy orders, leading to a high premium for Tether against USD and USDC.

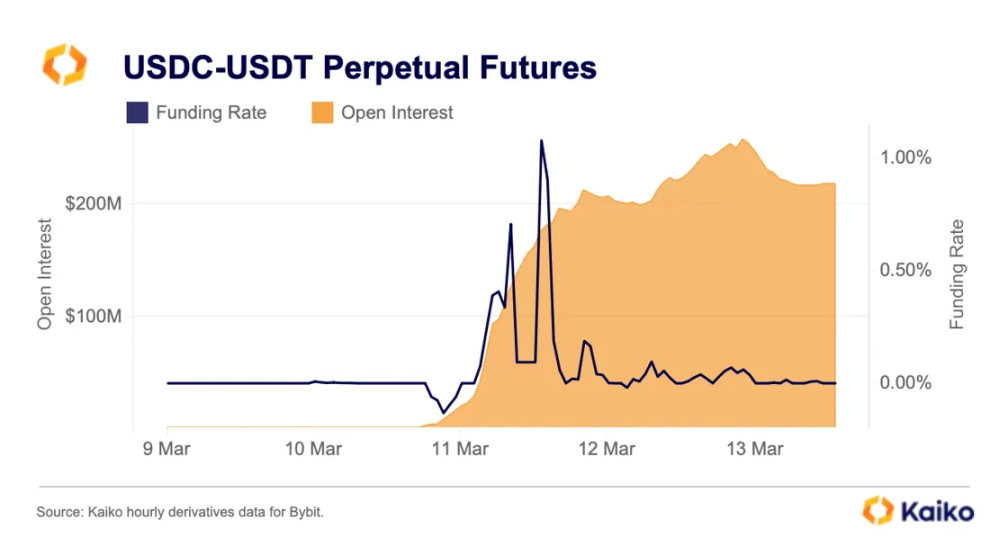

As Binance re-listed a large number of USDC trading pairs, derivatives exchanges also attempted to capitalize on this volatility. Until this weekend, traders could only trade on Bybit, which had lower trading activity. Last weekend, open interest soared to a historic high of $256 million. Funding rates remained volatile, oscillating between -0.13% and 1.08%, as traders simultaneously shorted and went long, but had returned to normal levels by the morning of the 13th.

Several other derivatives exchanges launched USDC perpetual contracts over the weekend, with leverage ranging from 10x on Bitmex, 20x on OKX, to 30x on Binance.

So, if these exchanges do not frequently use USDC, why did trading activity on CEX have such a huge impact amid broader market turmoil? The most direct reason is that the DeFi price feeds for stablecoins cannot provide a real USD exchange rate because you cannot trade fiat currency on DEX. This is why many protocols use decentralized price oracles to determine liquidation levels, and the data often comes directly from CEX.

Another reason lies in how websites like CoinGecko and Coinmarketcap calculate their price feeds, which largely rely on centralized markets. Notably, while Curve is one of the most liquid markets, it is not listed on CoinGecko or CMC's USDC market page.

Overall, the poor liquidity of centralized spot markets, the emergence of multiple USDC derivatives contracts, and the rapid spread of screenshots from price and exchange rate websites exacerbated the depeg event. Like a bank run, the narrative became reality, overwhelming the DeFi ecosystem.

(2) DeFi Bore the Brunt of the USDC Depeg

DeFi is essentially built on USDC. This stablecoin provides crucial stability for lending protocols, accounting for a significant portion of the reserves of decentralized stablecoins like DAI. Many DeFi protocols were built on the assumption that USDC would never depeg.

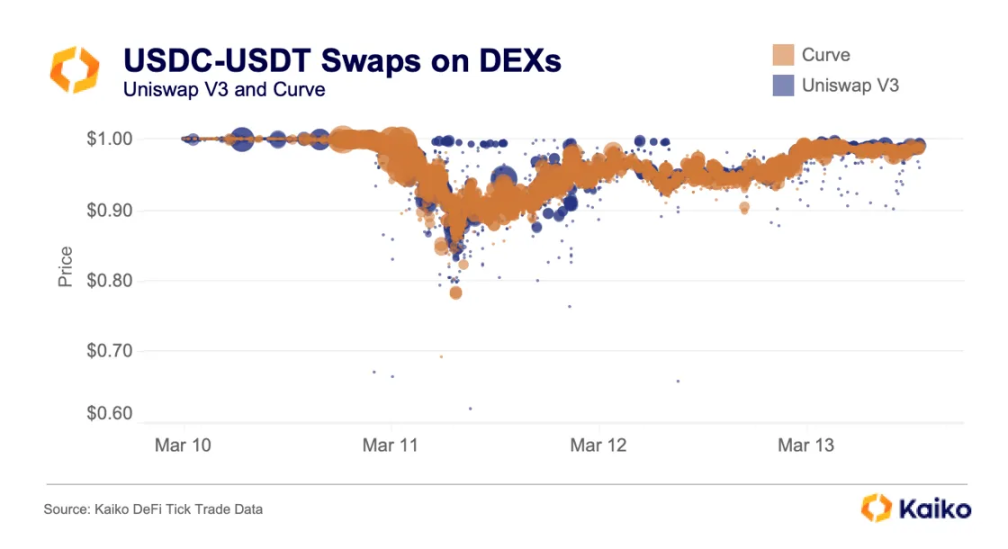

Last weekend, Uniswap and Curve saw record trading volumes as traders exchanged USDC for ETH or other stablecoins like USDT. Since March 10, the trading volumes of USDC-USDT on Curve and Uniswap V3 were nearly identical, at $5.91 billion and $5.96 billion, respectively. On Uniswap V3, the USDC-USDT exchange rate hit a low of 0.6188:1; on Curve, it reached 0.6911:1.

The rush to exchange USDC severely disrupted Curve's 3pool, with USDT's share in the pool dropping to around 2%. On March 13, the total value of the 3pool was less than $400 million, with nearly 95% being USDC and DAI, reflecting the strong demand for USDT in the market.

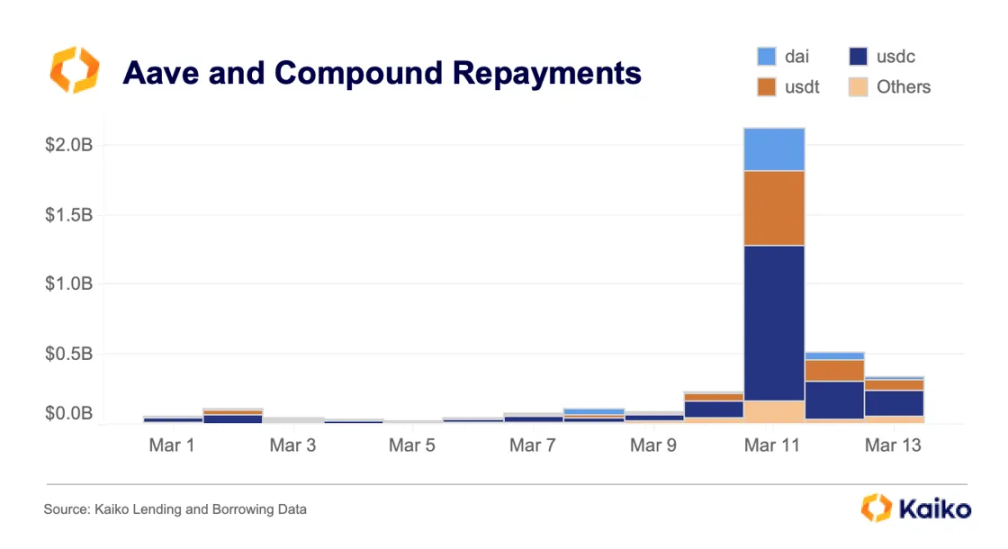

Lending pools were also affected. On March 11, Aave and Compound received over $2 billion in repayments, most of which were in USDC, as borrowers were able to repay loans at a low price due to the depeg.

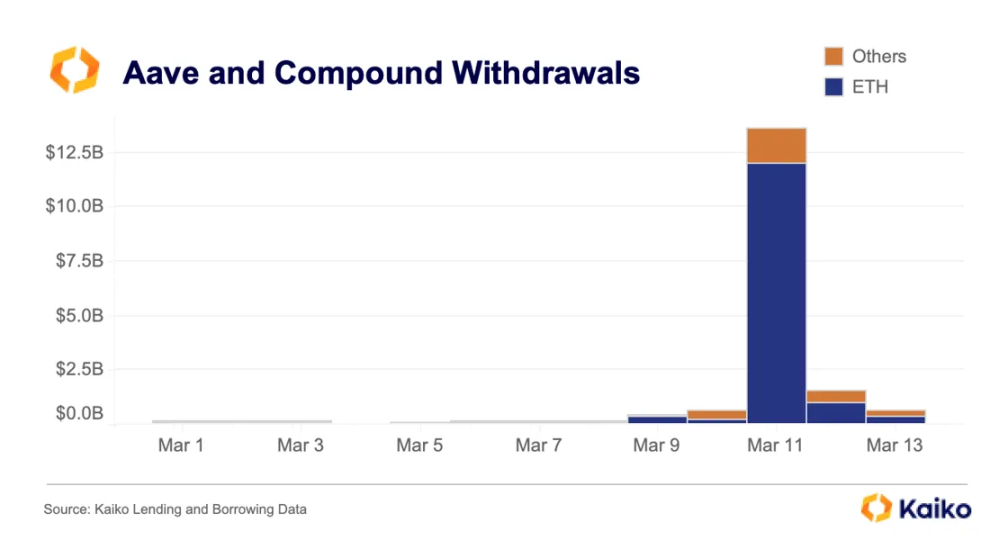

Withdrawals from Compound totaled $400 million, while Aave saw $13.1 billion withdrawn, of which $11.9 billion was ETH. Note that this does not mean that TVL dropped by $13.1 billion; there were $13.6 billion in deposits on Aave that day, as bots were particularly active on that protocol.

Overall, the DeFi market experienced two days of significant price dislocation, creating countless arbitrage opportunities and highlighting the importance of USDC.

2. Market Liquidity Situation

Now, let's broaden our perspective and see how much impact the bank failures have had on the market.

The disruption of USD payment channels means that U.S. market makers have been withdrawing liquidity from exchanges as they determine how to safely restore liquidity provision in the crypto market.

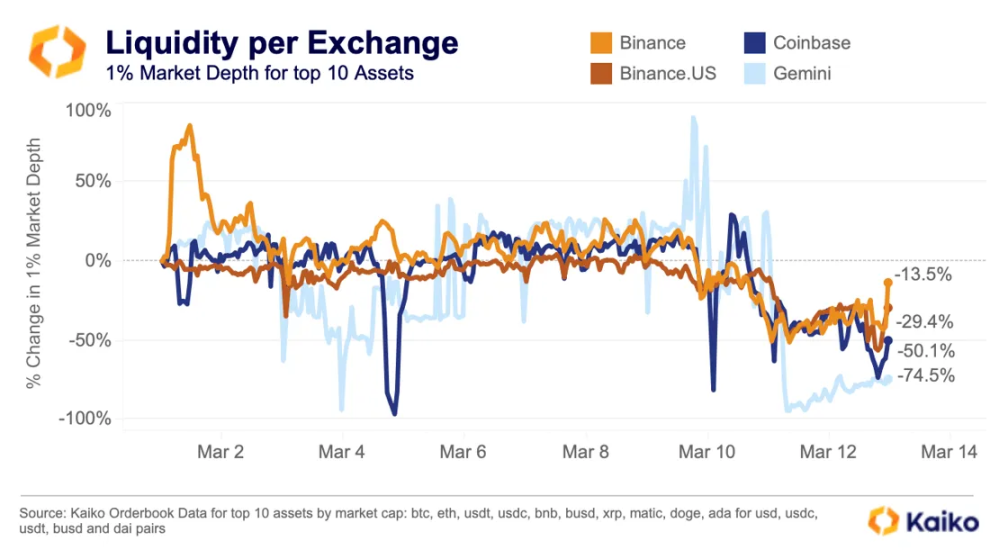

As a result, U.S. exchanges were hit hardest in terms of liquidity, with Gemini's market depth dropping 74% in March, Coinbase down 50%, and Binance.US down 29%. On the other hand, thanks to its greater exposure to global market risks, Binance's liquidity has only decreased by 13% so far this month.

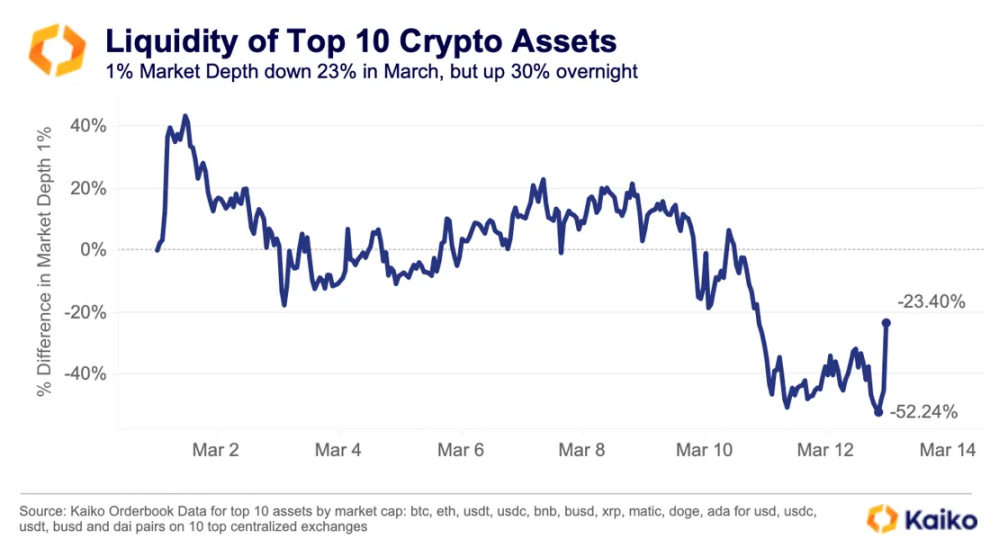

When liquidity declines across the board, we can see extreme price volatility, and the lack of liquidity undoubtedly affects the response to rescue news. Among the top ten cryptocurrencies by market capitalization, liquidity in the crypto market dropped by 52% until news broke that Silicon Valley Bank depositors would be compensated, exacerbating the subsequent price volatility.

However, as price effects facilitated the recovery of exchange USD liquidity, market depth increased by over $125 million overnight, accounting for 30%.

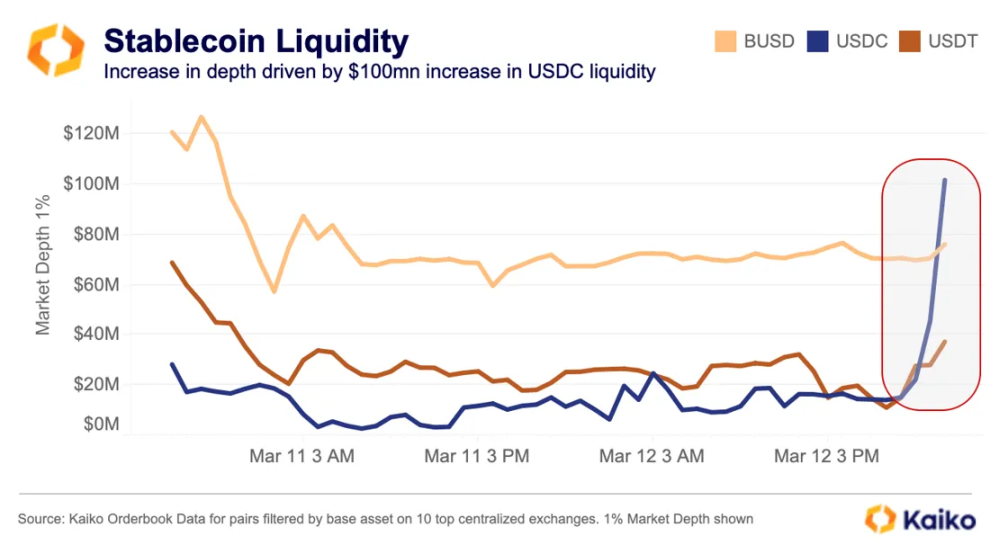

While prices affect exchange USD liquidity data, a closer look at liquidity at the trading pair level reveals that a significant portion of the growth actually came from the recovery of USDC liquidity. It is clear that Circle would receive its $3.3 billion held at Silicon Valley Bank on Monday morning, bringing USDC closer to its pegged rate, and market makers were eager to start providing liquidity for USDC pairs again.

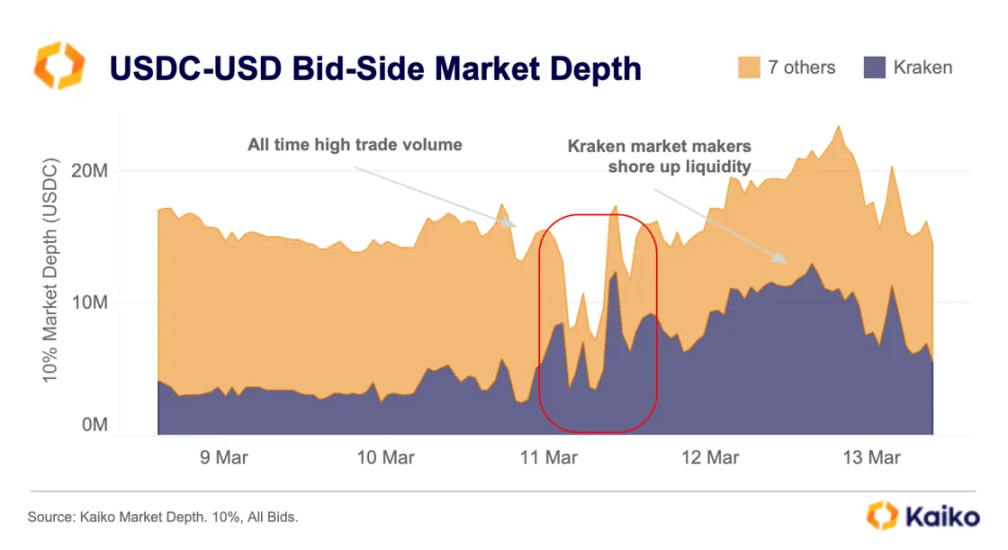

With USDC as the base asset, the additional liquidity provided overnight exceeded $100 million, with over $60 million belonging to the re-listed USDC-USDT trading pair on Binance, while the USDC-USD trading pair on Kraken injected $20 million in liquidity.

3. Bull Market Reversal: Binance Industry Recovery Fund

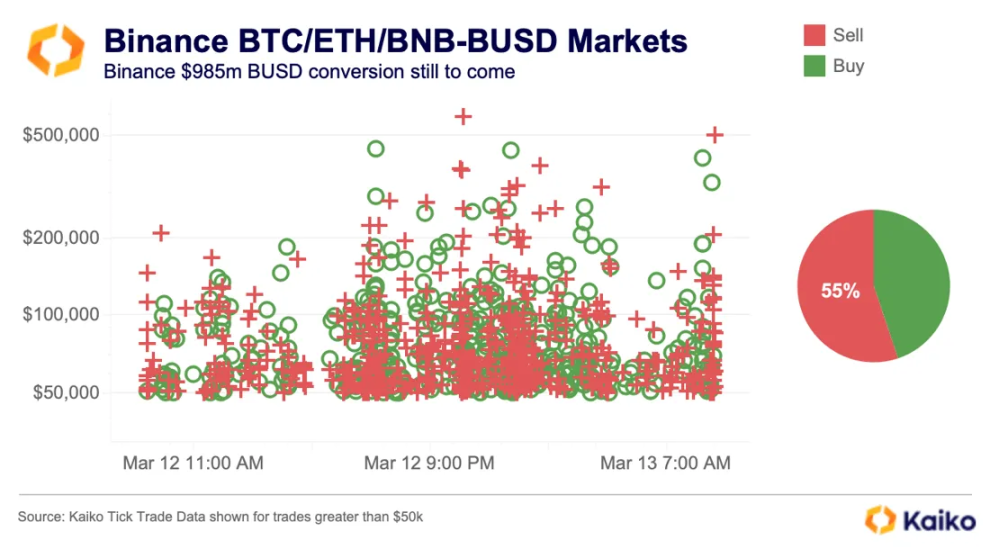

Meanwhile, Binance announced that it would convert the remaining assets of its $1 billion industry recovery fund from BUSD to BTC, ETH, and BNB. This announcement came after the volatility of stablecoins, with BUSD being affected as its $250 million reserves were held at the now-closed Signature Bank. While U.S. government officials stated that all depositors would be compensated, from the perspective of volatility and liquidity, Binance clearly views BTC, ETH, and BNB as safer short-term options.

Although the market rebounded after the news that Silicon Valley Bank depositors would be compensated, BTC, ETH, and BNB may attract more positive funds, as Binance seems not to have converted BUSD into the aforementioned assets yet. Our trading data shows that in the past 24 hours, sell orders for BUSD on exchanges still outnumbered buy orders, with no excess buy orders.

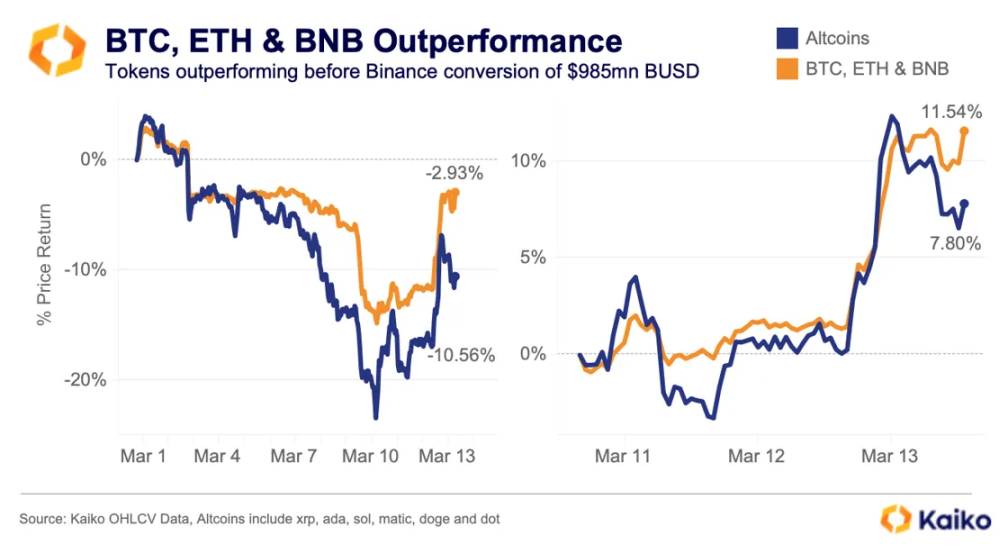

Given that this conversion has not yet been completed, BTC, ETH, and BNB are likely to outperform the market in the short term. Since the beginning of this month, these three cryptocurrencies have outperformed a basket of altcoins by 7.5%, despite being affected by recent market volatility, having only dropped by 2.9%. Since the market bottomed on March 11, these three cryptocurrencies have risen by 11.5%, while the return rate for altcoins was 7.8%.

4. Consequences

While the full consequences of the collapses of Silvergate and Signature are yet to be seen, I have thought of the following potential outcomes:

First, the impact on market liquidity will be widespread. With the closures of Silvergate and Signature, the infrastructure of the crypto market has regressed, as the relationship between the crypto industry and the traditional banking system has become more severed.

Real-time payment networks such as the Silvergate Exchange Network (SEN) and SigNet are crucial for managing overnight and weekend liquidity—facilitating OTC trades, arbitrage between exchanges, and stablecoin redemptions outside normal business hours. With the disappearance of these solutions and no temporary alternatives, fiat inflows may worsen, making price volatility more likely.

Although the Federal Reserve has improved market liquidity through the newly established Bank Term Funding Program (BTFP), uncertainty in monetary policy has increased, which may further fuel risk aversion among institutional traders. According to U.S. interest rate futures, market expectations for the Federal Reserve's terminal rate have dropped from nearly 6% last week to around 5% on Monday morning. According to the CME FedWatch tool, expectations for a 50bps rate hike at next week's Federal Reserve meeting have fallen from 40% to zero within a few days.

Overall, the crypto industry has once again weathered a significant market crisis, and as of Monday morning, the market is in a relatively stable state.