Macro Monthly Report: Global Risk Aversion Rises, Risk Assets May Face Short-Term Pressure

The characteristics of the bottom of the cryptocurrency market are evident, and the sentiment is also experiencing the most difficult "dark night before dawn."

The characteristics of the bottom of the cryptocurrency market are evident, and the sentiment is also experiencing the most difficult "dark night before dawn."Written by: WealthBee

1 The Strong Momentum of the U.S. Economy Slows Down

From the economic data released in August, the U.S. economy—this speeding locomotive—has finally shown some signs of slowing down.

The U.S. CPI in July rose by 3.2% year-on-year, ending a consecutive decline for the previous 12 months, with an estimate of 3.3% and a previous value of 3.0%; the core CPI in July rose by 4.7% year-on-year, with an estimate of 4.8% and a previous value of 4.8%. Although the CPI has increased, it is still below market expectations, indicating the effectiveness of the Federal Reserve's interest rate hikes.

From the employment perspective, the U.S. labor market has also shown signs of slowing down. In July, the non-farm payrolls added 187,000 jobs, below market expectations. In terms of hourly wages, the average hourly wage growth in the second quarter was 4.5%, slightly down from 4.8% in the previous quarter. The latest salary tracking data from job site Indeed shows that the annual growth rate of salaries in job postings on the site is 4.7%, down from 5.8% in April and 8% in July of last year. The labor market has always been an important reference for the Federal Reserve's interest rate hikes, as wages and prices often rise in tandem. The current reduction in wage expectations undoubtedly aligns the labor market with the Federal Reserve's stance.

Similarly, the preliminary Markit Services PMI for August in the U.S. is 51 (expected 52.2, previous 52.3); the preliminary Markit Manufacturing PMI for August is 47 (expected 49.3, previous 49). The manufacturing sector is in contraction, and the expansion of the services sector is also below expectations.

Numerous economic data indicate that the U.S. economy has slowed down this month; however, economic data from a single month is insufficient to determine the medium to long-term trend of the economy. The strength of the U.S. economy is still at a relatively high level. Powell also made hawkish remarks at the Jackson Hole meeting, stating that given the strong performance of the U.S. economy, further interest rate hikes may continue.

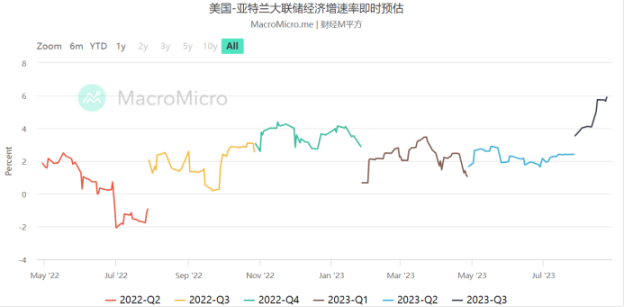

Institutions are in a "stalemate": the Atlanta GDP model predicts that the U.S. economy will grow by 5.8%, but Fitch has downgraded the U.S. credit rating.

The Atlanta Fed's GDP Now model predicts a U.S. GDP growth rate of 5.9% for the third quarter based on currently available data. However, the market believes that the data used for the model's predictions (such as July retail sales, auto sales, new housing starts, etc.) only reflect short-term conditions, and as future data is released and adjusted, the model's predictions will also be adjusted.

On one hand, the model provides overly optimistic expectations, while on the other hand, Fitch has downgraded the municipal bond ratings related to the U.S. sovereign rating to "AA+", marking the first downgrade of the U.S. credit rating since Fitch issued this rating in 1994. Blackstone's Schwarzman also echoed this sentiment, stating that Fitch's downgrade is "in line with the data." Fitch not only downgraded municipal bonds but also indicated that it might downgrade the ratings of dozens of U.S. banks, including JPMorgan. Institutions generally express concerns about the long-standing fiscal and debt issues of the federal government, and Fitch's downgrade may be a concentrated reflection of this dissatisfaction.

2 Bond Market Yields Soar, High Risk Aversion

In August, U.S. Treasury yields skyrocketed, becoming a "beautiful landscape" in the global financial market, with both short-term and long-term government bonds soaring. The yields on 10-year and 30-year U.S. Treasuries reached their highest levels since 2007 and 2011, respectively; short-term Treasury rates, such as those for 1-year, 2-year, and 5-year bonds, remain high and have been flat for months.

It's not just U.S. Treasuries; bond yields in countries like Japan and Germany are also high.

Why have U.S. Treasury yields surged so rapidly? The current wave of rising interest rates is likely a quick response to the interest rate hikes. With the U.S. economy remaining strong, many scholars no longer expect a recession this year, which fuels market expectations for further interest rate hikes by the Federal Reserve, leading to a sustained rise in rates. Additionally, Fitch believes that the government's fiscal risks are continuously worsening, which also undermines market confidence in U.S. Treasuries, inevitably leading to an increase in financing costs for U.S. debt.

The result of soaring U.S. Treasury yields is significant pressure on risk assets. This month, all three major U.S. stock indices fell, and the risks of cryptocurrencies like Bitcoin were also concentratedly released on August 18, but have yet to recover from the losses. Although Nvidia, the "global AI leader," has continued to trade at high levels and set new highs, other tech stocks have shown a persistent downward trend. This month, Nvidia released its second-quarter report, which showed revenue doubling year-on-year, exceeding expectations by 22%, and EPS growth of over four times, nearly 30% above expectations. The revenue guidance for the third quarter is $16 billion ± 2%, a year-on-year increase of 170%, exceeding expectations by 28%, significantly surpassing market expectations. Subsequently, Nvidia announced it would allocate $25 billion for share buybacks. This move further shocked the market, providing endless imagination for investors. Various institutions have raised their price expectations for Nvidia, with the most optimistic bulls raising their price target to $1,100 (Rosenblatt).

As the "largest arms dealer of the AI era," Nvidia's momentum is unending. Indeed, AI remains the most certain and vast new track in the market. Generally speaking, when a giant company exceeds market expectations for two consecutive quarters, it is an important signal indicating good synergy in the industry chain. AI may be the most certain track in the U.S. stock market under the pressure of U.S. Treasuries, likely leading to institutional clustering.

3 The Crypto Market is Bottoming: Volatility, Sentiment, and New Opportunities

Currently, the crypto market is showing bottoming characteristics.

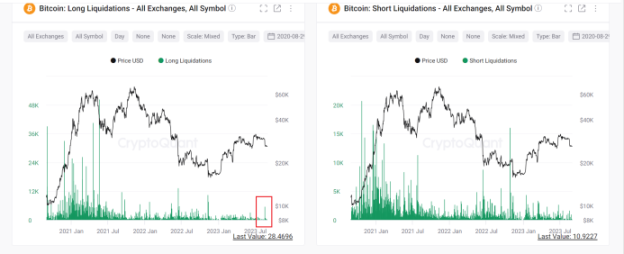

First, the sudden plunge in Bitcoin prices in August led to long liquidations and intensified market speculation. On the 18th, the crypto market experienced a "quake": major cryptocurrencies crashed, with Bitcoin dropping to a low of $24,220 USDT and ETH falling to a low of $1,470.53 USDT, and has yet to recover from these losses. As mentioned above, this plunge was primarily a concentrated release of risk aversion, not triggered by specific news. In this plunge, $990 million was liquidated across the entire network within 24 hours, an increase of 737.87% compared to the previous trading day, indicating a significant volume of long liquidations.

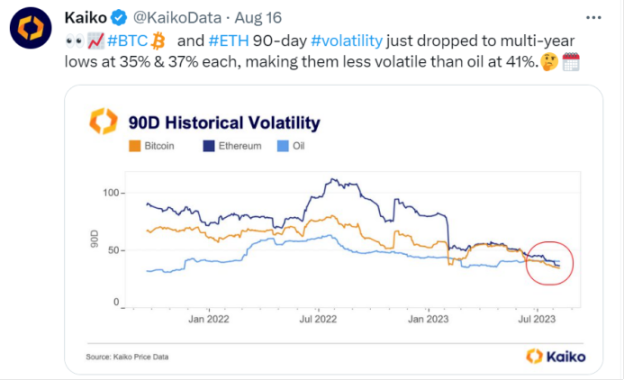

Secondly, Bitcoin's volatility and trading volume are at historical lows, with price performance being sluggish. This month, European Jacobi Asset Management launched the Jacobi FT Wilshire Bitcoin spot ETF, which went live on August 15 on the Amsterdam Euronext, but the market reacted almost indifferently to this news, instead experiencing a panic sell-off. This reflects a market sentiment that is quite sensitive and lacking in confidence. One characteristic of a secondary market bottom is insensitivity to good news but high sensitivity to bad news, making it prone to pessimistic sell-offs. Currently, both from a market perspective and an emotional perspective, the likelihood of a bottom in the crypto market is high.

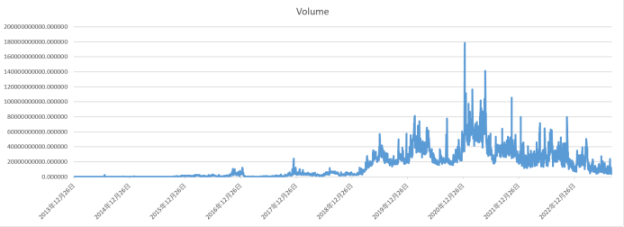

Additionally, this month, the DeFi TVL (Total Value Locked) has continued to decline, reaching its lowest point since February 2021, currently around $38.134 billion. This is a drop of over 70% from the peak of over $170 billion during the 2021 DeFi Summer.

On the other hand, globally, the Web3 industry is continuously receiving positive news. Since the beginning of this year, nearly ten major financial institutions, including BlackRock, have submitted applications for Bitcoin spot ETFs to the U.S. SEC. On August 30, reports emerged that a U.S. federal court approved Grayscale Investments' launch of the first Bitcoin ETF in the U.S., and the court overturned the SEC's decision to block this ETF, paving the way for the first Bitcoin ETF.

At the same time, various regions are improving their crypto regulations, especially in Hong Kong, where the crypto market is accelerating. From the Vice President of Hong Kong University of Science and Technology suggesting that the government expedite support for a Hong Kong dollar stablecoin, to Chief Executive John Lee publicly stating that they are "fully exploring regulatory matters for stablecoins," and HashKey Exchange supporting compliant "Hong Kong drift" account trading, Hong Kong's "crypto-friendly" pace is accelerating. Currently, the first batch of "licensed" cryptocurrency exchanges in Hong Kong has been established, with HashKey Exchange and OSL Digital Securities announcing in August that they have received approval from the Hong Kong Securities and Futures Commission to provide virtual asset trading services to retail users. As one of the three major financial centers globally, Hong Kong's ability to set an example in the compliance construction of digital asset trading gives us hope for the future of crypto assets.

4 Conclusion

The economies of China and the U.S. are experiencing a "dislocation," intertwining the resilience of the U.S. economy with the temporary pressure on the Chinese economy, casting an uncertain shadow over global investors. Risk aversion dominated the performance of the global secondary market this month, with both U.S. stocks and Chinese A-shares performing poorly, and the crypto market experienced a significant drop that led to many liquidations.

However, the crypto market shows clear bottoming characteristics, and the sentiment is undergoing the most challenging "darkness before dawn." From the establishment of the first batch of "licensed" cryptocurrency exchanges in Hong Kong to the imminent release of Bitcoin spot ETFs, these all indicate that the development of Web3 is in its early stages. From a market perspective, the current bottom of the crypto market has been showing a trend of fluctuating upwards, and future events may stimulate prices to break through the $30,000 resistance level, potentially ushering in a new wave of increases.