BTC Volatility: A Weekly Review from September 2 to September 9, 2024

Summary:

2024-09-10 10:41:02

Collection

Key Indicators (Hong Kong Time September 2, 4 PM -> September 9, 4 PM):

- BTC/USD -4.1% ($57,400 -> $55,080), ETH/USD -4.9% ($2,440 -> $2,320)

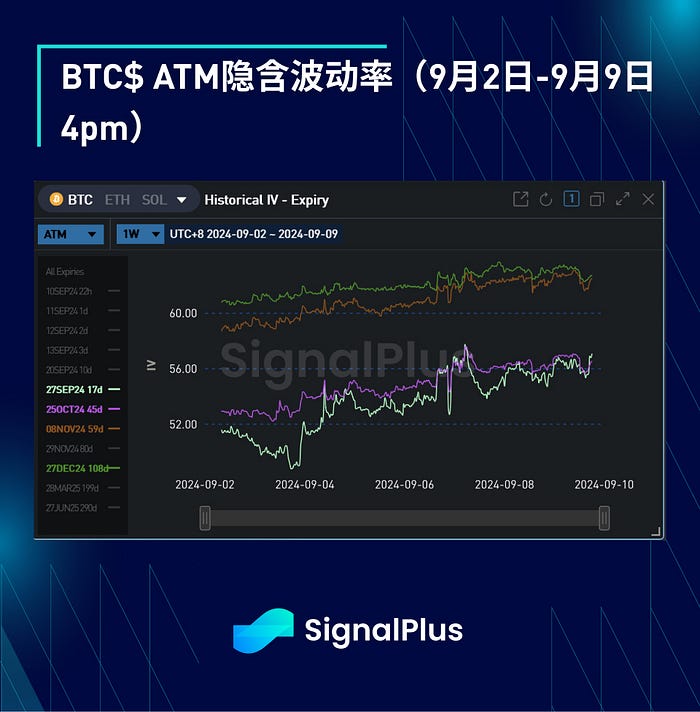

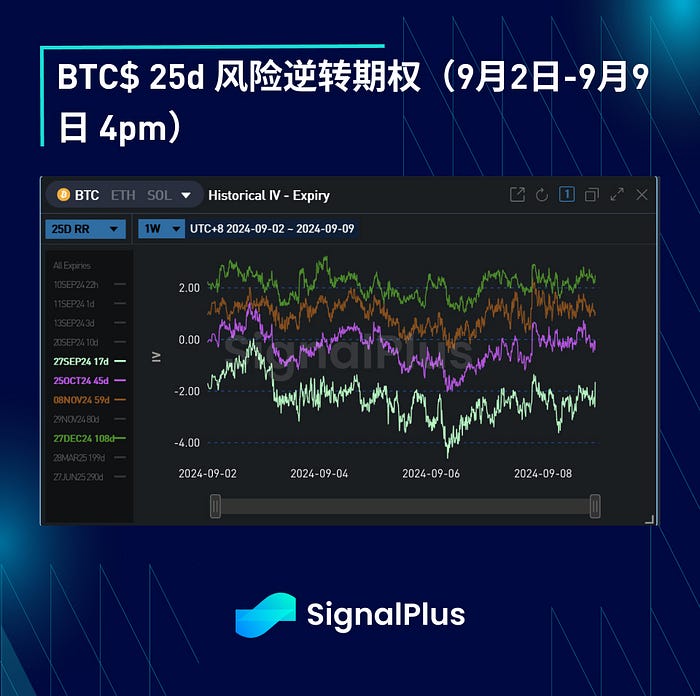

- BTC/USD December (end of year) ATM volatility +1.6 v (60.8 -> 62.4), December 25 d risk reversal volatility +0.2 v (2.3 -> 2.5)

Spot Technical Indicators Overview

- Spot prices continue to decline, challenging the range support level of $53.6k. Although it briefly fell below this level, prices then steadily rebounded. This is likely a significant signal that the market is rejecting further declines. Additionally, the market's failure to break through the $65k high last month is also a test of the support point at the other end of the range.

- From the current trend, technically, it is more inclined to build a bottom before rising again, then return to the key price range (expected to see some volatility when breaking through the $58-$60k area).

- If the support at $53-$53.6k fails to hold, we initially expect prices to quickly return below the $50k major support level. However, given that there seems to be strong buying demand here, we believe that unless there is significant risk aversion in the global market, spot prices will receive strong support at this level.

Major Market Events:

- "Rektember" has finally arrived, bringing a rise in implied volatility in the market, especially in the cryptocurrency market.

- Cross-market risk aversion has made it difficult for cryptocurrency prices to rise. Ultimately, BTC/USD challenged the lower end of the $53-$65k price range and found some support there. Meanwhile, ETH/USD challenged the local low of $2,150 and then gained a brief respite.

- The odds for the U.S. election remain close to 50-50, with a fierce competition between Trump and Harris, especially with the presidential debate scheduled in Philadelphia on September 10.

- The market remains divided on the extent of rate cuts at this month's FOMC meeting (25 bp or 50 bp). However, the cryptocurrency market's reaction to this has not been significant, mainly influenced by the U.S. stock market and VIX price trends.

- If the Federal Reserve does cut rates by 50 bp, we expect cryptocurrency prices to quickly rebound from the current sluggish state. Although this may imply concerns about economic growth prospects, it also clearly indicates that the dollar will weaken, and if the Fed excessively cuts rates, inflation expectations in the U.S. will recover.

ATM Implied Volatility:

- This week's actual volatility has remained relatively calm at high frequency and fixed terms, staying at around 40%; however, as risk aversion intensifies and significant future events approach (such as last week's non-farm payroll data, U.S. CPI, presidential debate, FOMC meeting), front-end implied volatility has gradually risen to 50%, while the long-term has further climbed due to post-election uncertainties.

- As the market shifts focus to the recent "bleak September" events, all forms of demand have emerged, primarily through put options in the $52-$54k range. At the same time, there has been pure volatility demand through straddle and strangle strategies covering various events this month. Generally, the market has reserved an additional volatility spread of about 3-3.5% for the presidential debate on September 10, while CPI and FOMC are closer to 2%.

- As the market's attention turns to the recent "Rektember" events, various forms of demand have begun to surface --- primarily put options in the $52-$54k price range. At the same time, there has been demand for volatility through buying straddles and strangles to address major events this month. The market is expected to have an additional volatility range of about 3-3.5% for the U.S. presidential debate on September 10, while the expected additional volatility range for CPI and FOMC is closer to 2%.

- The market's focus has shifted from the U.S. election premium to the data being released. There has indeed been some supply of December put options, leading to a flatter post-election term structure curve. Given the volatility term structure of other asset classes (such as forex and stocks), the implied volatility for November is higher than that for December and beyond, so we still believe the market will gradually move towards an inverted curve.

Skew/Convexity:

- This week, the market's performance in terms of price skew and convexity has been relatively stable, as the market mainly focuses on local option demand related to this month's events.

- Although very short-term skew has sharply declined due to put demand in the $52-$54k range, this has not transmitted to the forward curve. The market continues to focus on future bullish tail risks, especially in the context of the Fed about to enter a rate-cutting cycle and Trump still having a slight lead in the election.

- Despite the significant price skew in the short term due to demand for put options in the $52-$54k price range, this change has not affected the longer-term skew. Considering the Fed is about to enter a rate-cutting cycle and Trump still has a slight lead in the election, the market continues to focus on the bullish tail in the long term.

Good luck to everyone!

Risk warning

Risk warning

Related tags

Risk warning

Related reading

Bitget UEX Daily Report | Ceasefire expectations rise, U.S. stock market three major indices hit new highs; Dell's earnings report exceeds expectations, night trading surges; Anthropic's valuation surpasses OpenAI (May 29, 2026)

13 小时前

The era of regulatory arbitrage has come to an end, and the competition for the value of cryptocurrency exchange licenses is intensifying

1 天前

He Yideng ranked: Since you're here, you might as well

1 天前