Leading indicators of the "U.S. recession trade" in the coming month: Number of people filing for unemployment benefits in the U.S. at the beginning of the week

In the coming month, the "number of initial unemployment claims in the U.S." will become very important and is expected to influence the price trends of short-term risk assets to some extent, as it is the most direct differential indicator for the "U.S. recession trade."

In the coming month, the "number of initial unemployment claims in the U.S." will become very important and is expected to influence the price trends of short-term risk assets to some extent, as it is the most direct differential indicator for the "U.S. recession trade."Author:++@Web3Mario(https://x.com/web3_mario)++

Abstract: Last Monday, I wrote an analysis article about the market and macroeconomics, and I found that everyone is quite interested in this topic. I have a background in science and engineering and have been engaged in Web3 product design, operation, and research and development. I am not formally trained in economics, but I have a strong interest in political and economic issues and have been self-studying. Therefore, I believe the reason why my content from my perspective can be appreciated is that it is more friendly to non-professionals, as it includes explanations of some concepts, which are mostly questions I encountered during my learning process. I think it is necessary to explain them in detail to friends who have a similar journey. In the future, I will continue to produce content on related topics for us to learn and communicate together. Back to the point, in the comments from friends on the last article, I saw a viewpoint that basically means that such analysis articles are essentially hindsight analysis. Indeed, this is an analysis and outlook on the results. I believe this kind of review is still necessary as part of learning and improvement, but I also hope to provide some forward-looking analysis content. Therefore, in this article, we will discuss a macro indicator that has suddenly become very important in the next month and will to some extent influence the price trends of short-term risk assets: the number of initial jobless claims in the U.S. This is the most intuitive differential indicator for the "U.S. recession trade."

A Brief Review of the Current Market Status: The Yen Arbitrage Trading Liquidation Wave is Gradually Diminishing, and the U.S. Recession Trade Takes Over

First, let’s briefly review the current market status. Overall, the liquidation of yen arbitrage trading is basically nearing its end. The market's focus of concern has shifted from the uncertainty of interest rate hikes by the Bank of Japan to worries about the U.S. falling into a hard landing, which is the so-called "U.S. recession trade."

In the previous article, we pointed out that the main reason for the massive market volatility on Monday was the aggressive interest rate hike by the Bank of Japan. I also mentioned that in the U.S.-Japan alliance, Japan usually plays the role of a supporting party due to its lack of complete financial sovereignty. Therefore, this round of liquidation trading coincided with a press conference held by Bank of Japan Deputy Governor Masayoshi Amamiya at 9:30 AM Beijing time on Wednesday, August 7, to reassure the market that the liquidation phase was coming to an end. ++He made detailed comments on the rapid rise of the yen, which triggered a stock market crash, and the future direction of the central bank's monetary policy.++ The core points include:

- Recent fluctuations in the stock and foreign exchange markets have had an impact. If market volatility affects the outlook, the interest rate path will change.

- The Bank of Japan will not raise interest rates during periods of market instability and currently needs to firmly implement accommodative policies.

- If the outlook becomes a reality, the degree of accommodation will be adjusted. The interest rates are not lagging behind the situation and are being monitored with a sense of urgency regarding the market's impact on the economy.

At this point, it can be said that the Bank of Japan has temporarily surrendered to the market, which means it will not raise interest rates in a way that affects risk market prices and may even continue to implement accommodative policies. This indicates that there is still room for yen arbitrage trading to exist, with the Bank of Japan's guarantee, making this investment portfolio effectively hedged against yen exchange rate risks by the government. Therefore, we can see that after Amamiya's speech, the yen's exchange rate against the dollar quickly rebounded, plummeting to 146. Of course, the Nikkei index and Japanese government bonds also saw corresponding upward corrections. It can be said that the liquidation wave of yen arbitrage trading triggered by the Bank of Japan's aggressive interest rate hikes has ended in the short term, and the market is no longer overly panicked about the future aggressive interest rate hikes by the Bank of Japan.

However, a simple outlook here indicates that the Bank of Japan's interest rate path in the medium to long term has basically been confirmed. This contradiction has shifted from a short-term contradiction to a medium- to long-term contradiction. The reason is simple: Japan's current inflation rate has reached 2.8%. Considering that the yield on short-term Japanese government bonds has just begun to rise and is still at a relatively low level, the real interest rate in Japanese society remains negative. This means that the accommodative monetary environment will further push up Japan's inflation level. Given that the current inflation level has exceeded a globally recognized target level of 2%, and Japan's wage growth is generally below the rising inflation level, coupled with the strong challenges faced by some of Japan's traditional pillar industries, such as automobiles, from countries like China, the employment market is not very optimistic. Therefore, at this time, inflationary pressure will increase Japan's misery index, putting pressure on the Japanese people. Thus, raising interest rates is basically the only choice for the Bank of Japan, but for the sake of global financial stability, the people still need to endure a bit longer.

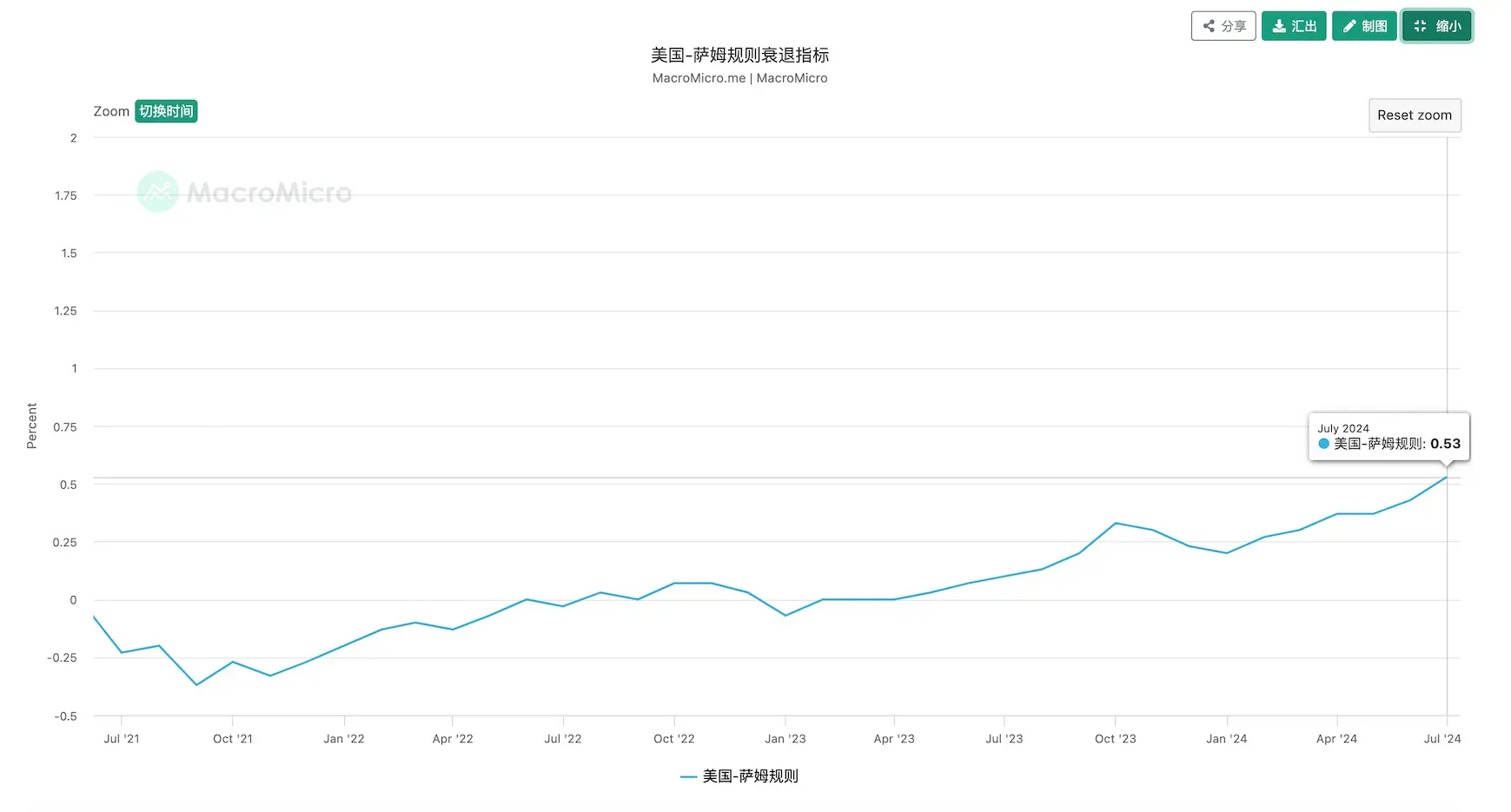

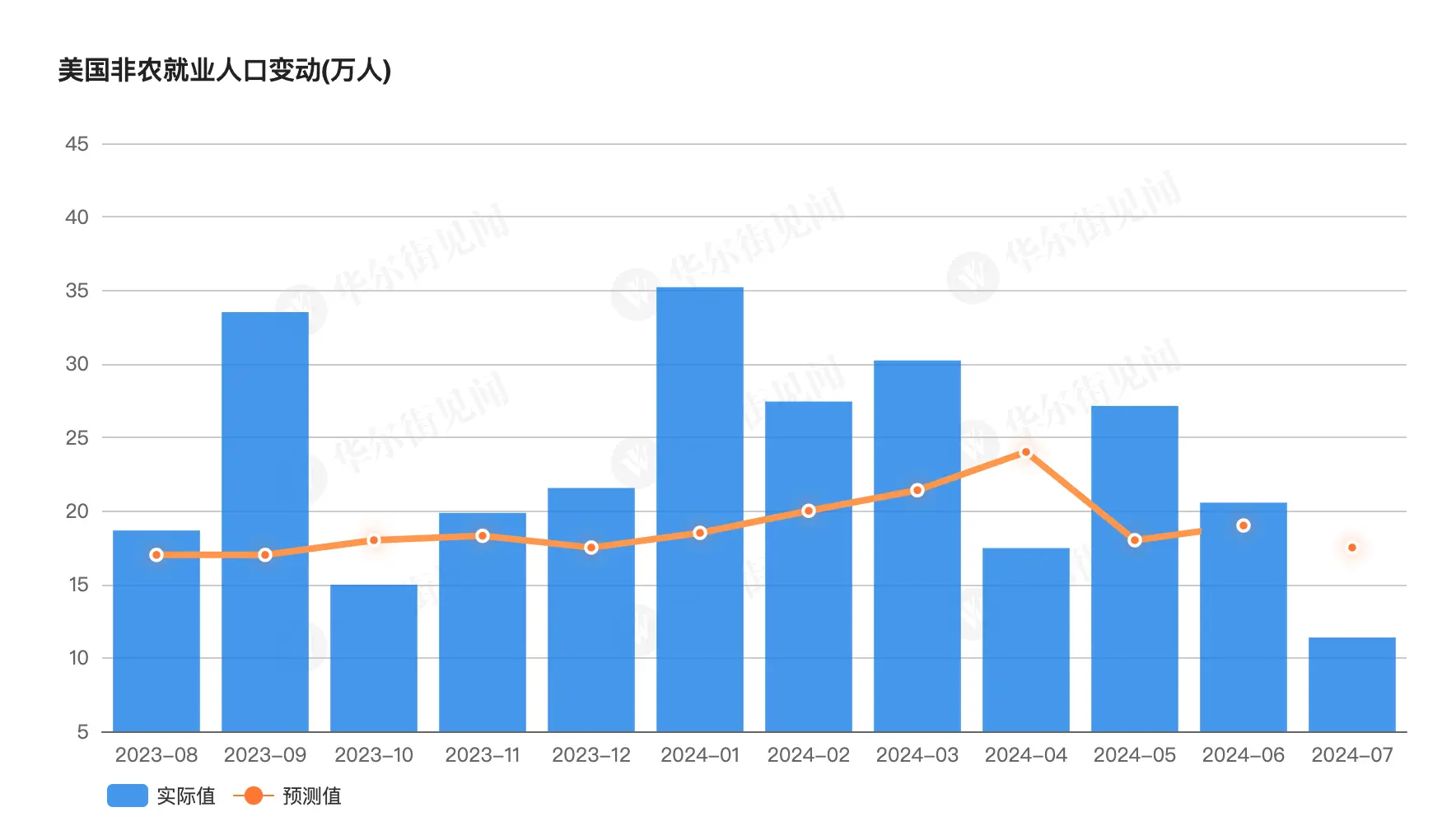

At this point, the focus of market trading has shifted to the second topic of concern, which is the so-called "U.S. recession" trade. So where does this concern come from? It can be traced back to the two macroeconomic data released by the U.S. on August 2: the non-farm payroll data for July and the unemployment rate for July. First, the non-farm data was far below expectations, and second, the unemployment rate for July reached 4.3%, triggering a judgment indicator used to assess whether a country has entered the early stages of an economic recession, known as the Sahm Rule.

Here, let me briefly introduce how the Sahm Rule recession indicator is calculated, proposed by Federal Reserve economist Claudia Sahm. Sahm found that when the three-month moving average of the unemployment rate in the U.S. minus the previous year's low unemployment rate exceeds 0.5%, it indicates that the economy is experiencing a recession phase. This has been true for every past recession phase, hence the indicator is named the Sahm Rule recession indicator. The unemployment rate in the U.S. for July has just brought the Sahm Rule indicator to 0.53%, officially entering its recession period. This has raised some concerns in the market.

Of course, we see that after reaching the target, the effectiveness of the Sahm Rule has begun to be widely discussed among big players, including institutions like Nomura. Even Claudia Sahm, the proposer of the "Sahm Rule," stated in an interview on August 6 that considering the changes in the current U.S. job market, the Sahm Rule has become less effective and cannot prove that the U.S. economy has fallen into recession. Nevertheless, this indicates that this indicator has attracted widespread attention in the market. Especially for some large capital players, risk is more critical than return, so it is very normal to make more cautious adjustments to the market at this time. This means that for a period of time in the future, observing whether the U.S. has fallen into recession will continue and become more critical, leading us to the theme of this article: the leading indicator of the "U.S. recession trade" in the next month: the number of initial jobless claims in the U.S.

The Number of Initial Jobless Claims in the U.S. Will Become an Important Differential Assessment Indicator for Recession in the Next Month

Why has this indicator become so important? It stems from an interpretation of the rising unemployment rate in July. Some believe that the poor employment data in July was due to the impact of Hurricane Barry, which lasted from June 28, 2024, to July 9, 2024. Objective factors such as infrastructure damage caused short-term fluctuations in the job market, so the poor employment data in July is not representative. Therefore, the employment data in August becomes particularly critical, as it will determine whether this argument can be broken.

However, considering the date of the release of U.S. macro data, the non-farm payroll and unemployment rate for August will only be publicly available on the first Friday of September, which is September 6. Therefore, in this month, the market needs to find some other evidence to predict the results for September in advance. Among these pieces of evidence, the most critical is the number of initial jobless claims in the U.S., and we also need to pay attention to some statements from Fed officials.

The reason it is necessary to remind everyone to pay attention is that this indicator has not been particularly important in the past. It is only because the market has mainly been engaged in recession trading recently, and the number of initial jobless claims can serve as a differential data point to observe the monthly unemployment rate. Generally, the number of initial jobless claims indicates first-time unemployment, thus reflecting changes in the job market for the month.

This indicator is released every Thursday at 8:30 PM Beijing time. A specific observation standard is that when the published data is below expectations, it indicates that the job market remains strong this week, reducing the probability of recession, making it easier for risk asset markets to rise. When the data is above expectations, it indicates that more people have started to lose their jobs this week, increasing the probability of recession, making it easier for risk asset markets to decline.