In-depth analysis of the current market: The theft of large sums of money has raised market concerns and resulted in a resonance of liquidity migration under the competition among major powers

The main reasons for the recent pullback in the cryptocurrency market are twofold. Firstly, from a micro perspective, the series of hacker attacks has raised concerns among traditional investors, increasing risk aversion. Secondly, from a macro perspective, the DeepSeek open-source week further exposed the AI bubble in the U.S., combined with the actual policy direction of the Trump administration. On one hand, this has ignited market worries about stagflation in the U.S., and on the other hand, it has initiated a reassessment of risk assets in China.

The main reasons for the recent pullback in the cryptocurrency market are twofold. Firstly, from a micro perspective, the series of hacker attacks has raised concerns among traditional investors, increasing risk aversion. Secondly, from a macro perspective, the DeepSeek open-source week further exposed the AI bubble in the U.S., combined with the actual policy direction of the Trump administration. On one hand, this has ignited market worries about stagflation in the U.S., and on the other hand, it has initiated a reassessment of risk assets in China.Author: ++@Web3++ ++_Mario++

Abstract: In recent days, the cryptocurrency market has experienced a significant correction, leading to a chaotic environment for consultations. Coupled with the continuous negative impact of massive hacker attacks in the crypto space, understanding the recent market trends in the short term has become challenging. I have some viewpoints on this matter that I would like to share and discuss. I believe there are two main reasons for the current pullback in the cryptocurrency market. Firstly, from a micro perspective, the series of hacker attacks has raised concerns among traditional investors, intensifying risk-averse sentiment. Secondly, from a macro perspective, the DeepSeek open-source week has further exposed the AI bubble in the U.S., combined with the actual policy direction of the Trump administration. On one hand, this has ignited market fears of stagflation in the U.S., and on the other hand, it has initiated a re-evaluation of Chinese risk assets.

Micro Perspective: Continuous Large Financial Losses Trigger Concerns Among Traditional Investors, Intensifying Risk-Averse Sentiment

I believe everyone still remembers the recent theft incidents involving Bybit and Infini. There has been a lot of discussion around these events, so I won't dwell on them here. Instead, I would like to elaborate on the impact of the stolen funds on these two companies and the industry as a whole. Firstly, for Bybit, the loss of $1.5 billion, while roughly equivalent to its net profit for about a year, is certainly not a small amount for a company in an expansion phase. Typically, companies maintain cash reserves for three months to a year, and considering that exchanges operate in a high cash flow industry, their cash reserves are likely closer to the lower end of that range. Looking at Coinbase's 2024 financial report, we can draw some preliminary conclusions. Coinbase's total revenue for 2024 is projected to more than double from last year, reaching $6.564 billion, with a net profit of $2.6 billion, while total operating expenses for 2024 are estimated at $4.3 billion.

Referring to the data disclosed by Coinbase and considering Bybit's current expansion phase, it is reasonable to estimate that Bybit's cash flow reserves are around $700 million to $1 billion. Therefore, a loss of $1.5 billion in user funds clearly cannot be covered solely by its own funds. At this point, methods such as borrowing, equity financing, or shareholder injections will be needed to navigate this crisis. However, regardless of the model, given the concerns about sluggish growth in the cryptocurrency market by 2025, the resulting cost of capital is likely to be significant, which will undoubtedly burden future corporate expansion.

Of course, today we saw news that the core vulnerability of the attack was in Safe rather than Bybit itself, which may provide some incentive to recover some losses. However, a significant issue plaguing the crypto industry is the lack of a comprehensive legal framework, meaning that related litigation processes are bound to be lengthy and costly. Recovering losses will likely not be an easy task. As for Infini, a loss of $50 million is clearly unsustainable for a startup, but it seems the founder is financially strong enough to navigate through this crisis.

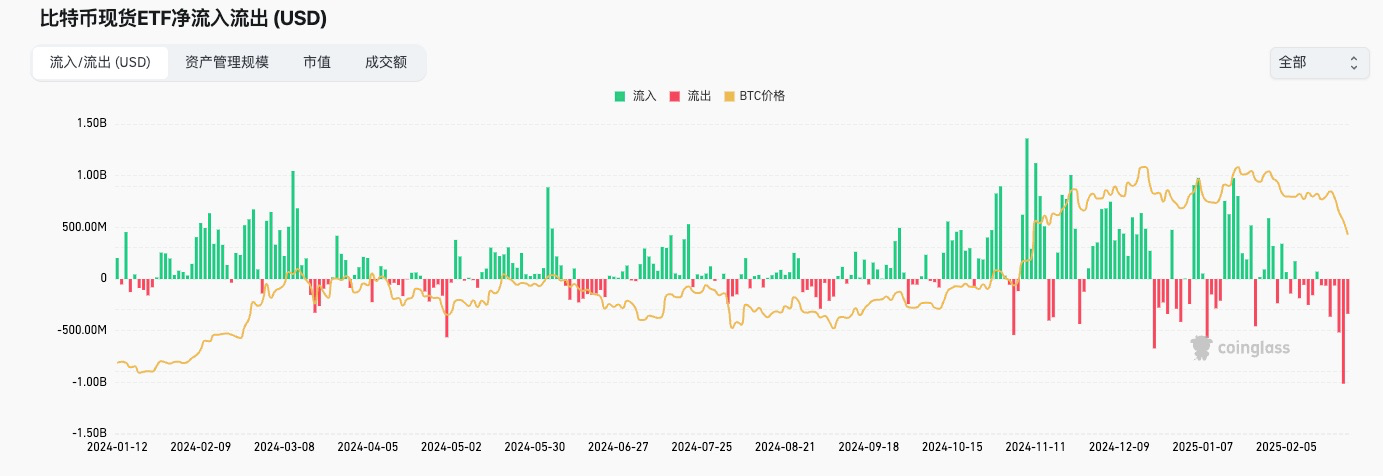

These two consecutive large losses may seem like just another day for traders accustomed to high risks in the crypto space, but they have evidently shaken the trust of traditional investors. This can be seen from the capital flow situation of the BTC ETF, which clearly experienced a significant outflow of funds following the attack on the 21st. This indicates that the impact of this event on traditional investors is likely negative. If the resulting concerns focus on whether it will hinder the establishment of a regulatory-friendly legal framework, then this is a serious matter. Therefore, it can be said that the theft incidents have acted as a catalyst for this round of pullback from a micro perspective.

Macro Perspective: Intensified Geopolitical Rivalry Among Major Powers, DeepSeek Open Source Week Reshaping AI Competition Landscape, and Liquidity Migration Amid China's Risk Asset Revaluation Phase

Now let's look at some macro-level impacts, which clearly indicate unfavorable conditions for the crypto market in the short term. In fact, after a period of observation, the policy direction of the Trump administration has become relatively clear, which is to achieve internal consolidation and industrial restructuring through strategic contraction, allowing the U.S. to regain its re-industrialization capability, as technology and production capacity are the core factors in great power rivalry. The most crucial element in achieving this goal is "money," which is primarily reflected in the U.S. fiscal situation, financing capacity, and the real purchasing power of the dollar. The relationship among these three factors is interdependent, making it challenging to observe changes in the related processes. However, by peeling back the layers, we can still identify some core concerns:

- The U.S. fiscal deficit issue;

- The risk of stagflation in the U.S.;

- The strength and weakness of the dollar.

First, let's look at the U.S. fiscal deficit issue, which has been analyzed extensively in previous articles. In simple terms, the core reason for the current U.S. fiscal deficit can be traced back to the Biden administration's extraordinary economic stimulus measures in response to the COVID-19 pandemic, as well as Treasury Secretary Yellen's adjustments to the U.S. debt issuance structure, which led to an inverted yield curve due to excessive issuance of short-term debt, thereby harvesting wealth globally. The specific reason is that excessive issuance of short-term debt depresses the prices of short-term U.S. Treasury bonds on the supply side, thereby increasing short-term U.S. Treasury yields. The rise in short-term U.S. Treasury yields naturally attracts dollars back to the U.S., as investors can enjoy excess risk-free profits without incurring time costs. This temptation is significant, which is why capital represented by Warren Buffett chose to sell off risk assets in large quantities during the previous cycle to increase cash reserves. This has put immense pressure on the exchange rates of other sovereign countries in the short term. To avoid excessive currency depreciation, central banks around the world have had to sell short-term debt at a loss, converting unrealized losses into realized losses to stabilize exchange rates. Overall, this is a global harvesting strategy, particularly targeting emerging countries and trade surplus nations. However, this approach also poses a problem: the U.S. debt structure will significantly increase its short-term repayment pressure, as short-term debt must be repaid with both principal and interest. This is the origin of the debt crisis triggered by the current U.S. fiscal deficit, which can also be seen as a time bomb left by the Democrats for Trump.

The biggest impact of the debt crisis is on U.S. credit, which in turn reduces its financing capacity. In other words, the U.S. government will need to pay higher interest rates to finance through Treasury bonds, which overall raises the neutral interest rate in U.S. society. This neutral rate cannot be influenced by the Federal Reserve's monetary policy, and the elevated neutral rate puts immense pressure on corporate operations, leading to economic stagnation. Economic stagnation, in turn, transmits through the job market to ordinary citizens, resulting in a contraction in investment and consumption. This creates a negative feedback loop that can trigger an economic recession.

The focus of observation on this main line is how the Trump administration will reshape U.S. fiscal discipline to address the fiscal deficit issue. The specific policies involved include the DOGE Efficiency Department led by Musk, which focuses on reducing U.S. government spending and cutting redundant staff, as well as the impact on the economy during this process. Currently, it appears that Trump’s internal consolidation efforts are quite strong, and reforms have entered a deep-water phase. I won't delve into tracking progress here, but I would like to share some of my observational logic.

- Pay attention to the aggressiveness of the Efficiency Department's policy implementation. For example, if cuts and reductions are too drastic, it will inevitably raise concerns about the economic outlook in the short term, which is usually unfavorable for risk assets.

- Monitor the feedback of macro indicators on these policies, such as employment data and GDP data.

- Keep an eye on the progress of tax reduction policies.

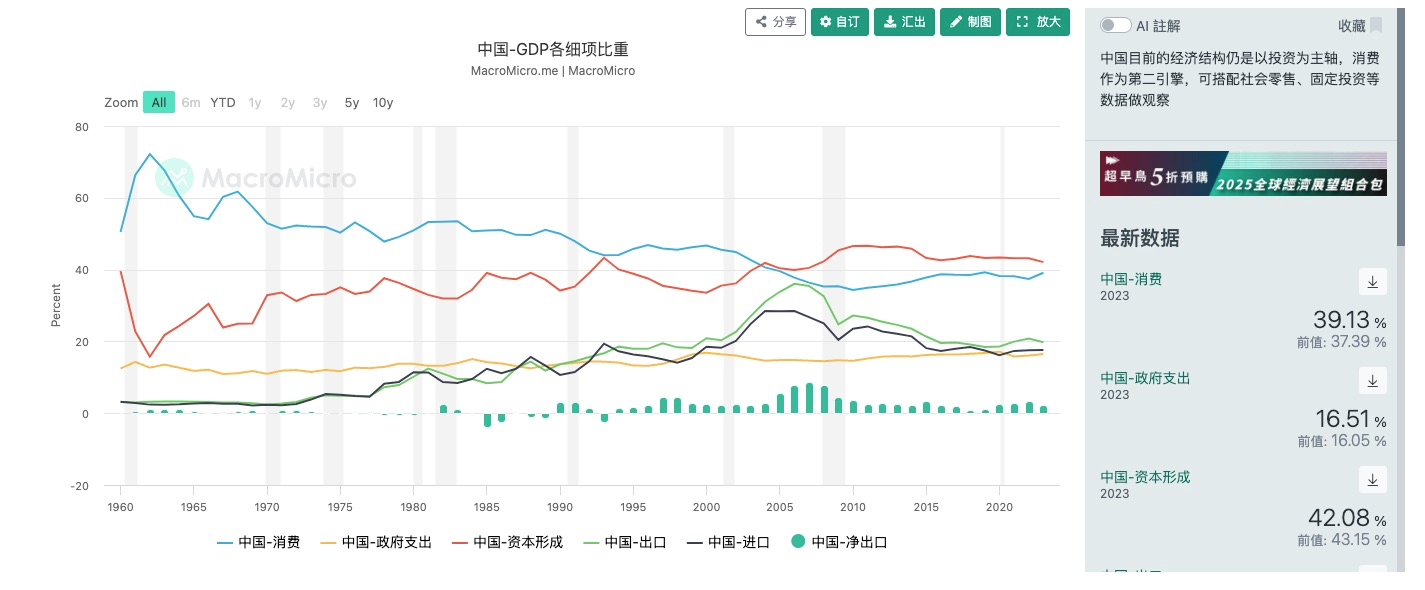

We cannot underestimate the impact of government spending and government employees on the U.S. economy. Typically, we might think that China's government spending as a percentage of GDP is higher than that of the U.S., but this is actually a misconception. U.S. government spending accounts for 17.2% of GDP, while China's is 16.51%. Moreover, government spending usually transmits through the industrial chain to the entire economic system. The structural differences mainly reflect that consumption accounts for a high proportion of U.S. GDP, while imports and exports account for a higher proportion of China's GDP. This represents two different approaches to stimulating the economy. For the U.S., expanding external demand and increasing exports is a means to boost the economy, while for China, there is still significant potential to tap into domestic demand.

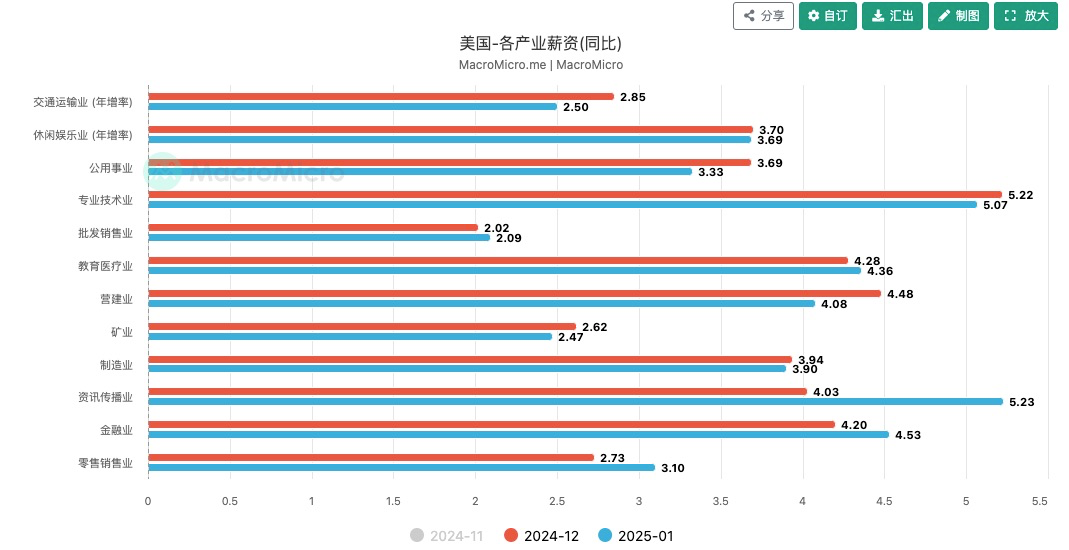

The same applies to consumption. In this chart, we can see that the salary levels of government departments are not low across the entire industrial chain, and reducing government redundancy also impacts U.S. economic growth on the consumption side. Therefore, overly aggressive policy implementation will certainly trigger fears of economic recession. Some matters require a gradual approach, but they must also align with the overall pace of policy advancement by the Trump administration. As for the progress of tax reduction policies, it currently seems that Trump's focus is not on this, so the concerns about reduced revenue in the short term do not appear to be significant, but vigilance is still necessary.

Next, there are concerns about stagflation in the U.S. Stagflation refers to a situation where economic growth stagnates while inflation intensifies, which is socially unacceptable according to the misery index. In addition to the impact of government spending cuts on economic growth mentioned earlier, there are some important points to consider:

- How DeepSeek will further impact the AI sector.

- The progress of U.S. sovereign funds.

- The impact of tariff policies and geopolitical conflicts on inflation.

Among these, I believe the most significant short-term impact is the first point. Those interested in technology may know that the DeepSeek open-source week has produced numerous shocking results, all pointing to one thing: the demand for computing power in AI has significantly decreased. This explains why, during the previous interest rate hike cycle, the stock market in the U.S. remained stable due to the enormous narrative surrounding the AI sector and the monopolistic position of the U.S. in the upstream and downstream of AI. The market assigned extremely high valuations to U.S. AI-related stocks, naturally fostering optimism about a new round of economic growth driven by AI in the U.S. However, all of this will be reversed by DeepSeek. The biggest impact of DeepSeek lies in two aspects: on the cost side, it greatly reduces the requirements for computing power, which significantly pulls back the growth potential of upstream computing power providers represented by Nvidia. On the other hand, it breaks the U.S. monopoly on downstream AI algorithms through open-source means, thereby suppressing the valuations of algorithm providers represented by OpenAI. Moreover, this impact has just begun, and we will have to see how the U.S. AI sector responds at that time, but in the short term, we are already seeing a pullback in valuations of U.S. AI stocks and a return to valuations of Chinese tech stocks.

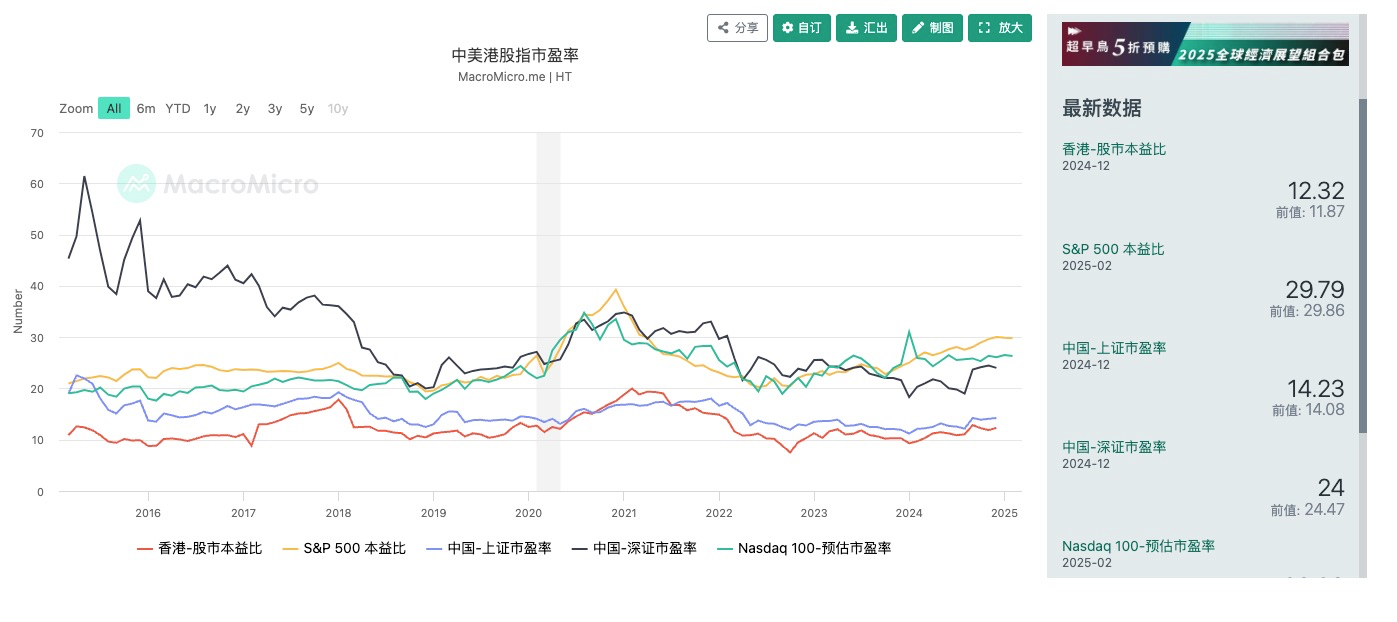

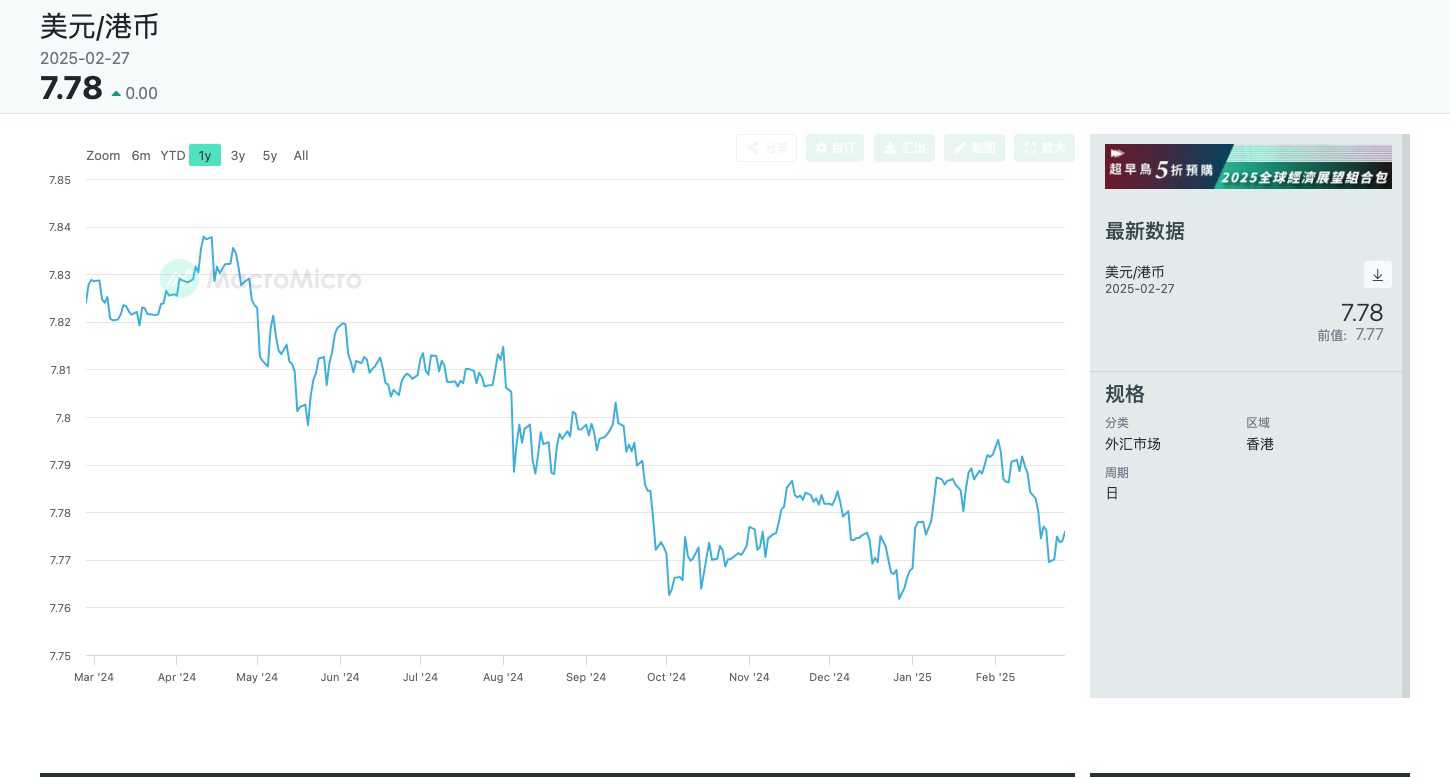

In fact, for a long time, the U.S. has used public opinion suppression to keep the valuations of Chinese companies low, effectively placing them in an undervalued state. However, benefiting from the grand narrative brought by DeepSeek for the upgrading of Chinese manufacturing, along with the relatively mild attitude of Trump’s policies on China-related issues, the geopolitical risks have decreased, leading to a return in valuations of both U.S. and Chinese companies. According to a report from CICC, the recent rise in Hong Kong stocks has mainly benefited from southbound capital, which refers to capital inflows from the mainland, as well as passive capital inflows from overseas. However, overseas active funds have not shown significant changes due to Trump's investment restrictions on Chinese companies. Nevertheless, observing liquidity is still very important, as there are many ways to bypass direct investment and still enjoy the dividends of the return in valuations of Chinese companies, such as investing in markets with high relevance like Singapore. Changes in capital flows can be easily identified through the Hong Kong dollar exchange rate. We know that the Hong Kong dollar operates under a linked exchange rate system with the U.S. dollar, meaning that the exchange rate of the Hong Kong dollar against the U.S. dollar will stabilize between 7.75 and 7.85. Therefore, when the Hong Kong dollar approaches 7.75, it indicates a stronger willingness of foreign capital to invest in Hong Kong stocks.

Another point worth noting is the construction of U.S. sovereign wealth funds. We know that sovereign wealth funds are a good supplement to government revenue for any sovereign nation, especially for trade surplus countries with large amounts of dollars. Among the world's top ten sovereign wealth funds, China has three, the Middle East has four, Singapore has two, and the largest is Norway's Government Pension Fund Global, with a total asset size of about $1.55 trillion. However, due to the constitutional framework of the U.S. federal government, establishing a sovereign wealth fund is quite challenging, as the federal government can only receive direct taxes, resulting in limited revenue sources. The U.S. is currently also experiencing a fiscal deficit dilemma. However, Trump seems to have instructed the Treasury to establish a trillion-dollar sovereign wealth fund, which is naturally a means to alleviate the fiscal deficit. The question here is where the money will come from and what it will be invested in.

Currently, according to the statements of the new U.S. Treasury Secretary, it seems there is a desire to reprice U.S. gold reserves to provide $750 billion in liquidity for the sovereign wealth fund. The reason behind this is that according to Title 31, Section 5117 of the U.S. Code, the statutory value of the U.S. government's 8,133 tons of gold is still $42.22 per ounce. If calculated at the current market price of $2,920 per ounce, the U.S. government has $750 billion in unrealized returns. Therefore, by amending the law, additional liquidity can be obtained, which is undoubtedly a clever approach. However, if approved, the dollars used for investment or to alleviate debt pressure will inevitably come from selling gold, which will certainly impact the gold market.

As for what to invest in, I believe it will likely revolve around the goal of bringing production capacity back to the U.S. Therefore, the impact on Bitcoin is likely limited. In previous articles, I have analyzed that in the short to medium term, Bitcoin's value relative to the U.S. is to become a safety net for the economy, based on the premise that the U.S. has sufficient pricing power over this asset. However, in the short term, there is no clear sign of economic recession, so this is not the main focus of Trump's policies but rather an important tool to navigate through the pains of reform.

Finally, regarding tariffs, the concerns about tariffs have been well addressed. Currently, it seems that tariff policies are more of a bargaining chip for Trump rather than a necessary choice, as can be seen from the relatively restrained tariff rates imposed on China. This is naturally due to considerations of the impact of high tariffs on domestic inflation. The next step I am particularly interested in is the tariffs on Europe and what returns the U.S. can negotiate in exchange. Of course, I am concerned about the EU's process of rebuilding its independence, as harvesting Europe to restore its own strength is the first step for the U.S. to participate in this great power rivalry. As for inflation risks, although the CPI has been rising for several months, considering that it remains at a controllable level, coupled with the mild nature of Trump's tariff policies, the current risks do not seem significant.

Finally, let's discuss the dollar's performance, which is a crucial issue that requires continuous observation. In fact, there has been ongoing debate about the strength of the dollar under Trump's new term. Some key figures' statements have significantly influenced the market. For example, Trump's newly appointed economic advisor, Chief of the White House Economic Council Stephen Moore, stated that the U.S. needs a weak dollar to boost exports and promote internal re-industrialization. In contrast, after causing panic in the market, U.S. Treasury Secretary Yellen reassured the market during an interview on February 7, stating that the U.S. will continue its "strong dollar" policy, although the yuan is somewhat undervalued.

In fact, this is quite an interesting situation. Let's examine the impact of a strong or weak dollar on the U.S. economy. First, a strong dollar has two main effects on asset prices. As the dollar appreciates, dollar-denominated assets perform better, which is beneficial for the U.S. government, particularly for U.S. Treasury bonds and globally oriented U.S. stocks, as it increases market enthusiasm for purchasing U.S. debt. Secondly, in terms of industry, a stronger dollar benefits U.S. global companies by reducing costs but suppresses the competitiveness of domestic industrial products in the international market, which is unfavorable for internal industrialization. Conversely, the effects of a weak dollar are the opposite. Considering that Trump's overall policy vision is based on returning production capacity to the U.S. to enhance competitiveness in great power rivalry, a weak dollar policy seems to be the correct approach. However, there is a problem: a weak dollar will lead to the depreciation of dollar-denominated assets. Given the current fragility of the U.S. economy and financing pressures, an overly rapid weak dollar policy could prevent the U.S. from weathering the pains of reform.

A representative event illustrating this pressure occurred in Warren Buffett's annual letter to shareholders on February 25, where he expressed dissatisfaction with the U.S. fiscal deficit issue, which clearly intensified market concerns. We know that Buffett's recent strategy has been to liquidate overvalued risk assets in the U.S. in exchange for more cash reserves to allocate to short-term U.S. Treasury bonds, while also including some allocations to Japan's five major trading companies. However, this is clearly a form of interest rate arbitrage, and I won't elaborate on that here. What I want to emphasize is that Buffett's views have a strong influence on the market, and capital that is overweight in the dollar naturally shares a common concern about the real purchasing power of the dollar, which is the worry about dollar depreciation. Therefore, the pressure associated with entering a depreciation phase too quickly is substantial.

Nonetheless, both the U.S. and China will likely choose to trade space for time and gradually reduce debt. The dollar's trajectory will likely follow a pattern of initially strengthening and then weakening. The fluctuations in dollar-denominated assets will also move with this cycle. Cryptocurrencies are among the assets affected by this wave.

Finally, I would like to share my views on the cryptocurrency market. I believe that the current market has too many uncertainties, so individual investors can adopt a barbell strategy to enhance the anti-fragility of their investment portfolios. On one hand, allocate to blue-chip cryptocurrencies or participate in some low-risk DeFi yields; on the other hand, take small positions to buy some high-volatility assets on dips. As for the short-term market trends, the accumulation of many unfavorable factors has indeed led to some price pressure, but there seems to be no clear structural risks. Therefore, if the market experiences an excessive pullback due to panic, appropriately building positions may not be a bad choice.