BTC Volatility: A Weekly Review July 22–29, 2024

2024-07-30 15:24:20

Collection

Key Metrics: (Hong Kong Time July 22 4 PM -> July 29 4 PM):

- BTC/USD +3.4% ($67,240 -> $69,500), ETH/USD -3.2% ($3,480 -> $3,370)

- BTC/USD December (end of year) ATM volatility -11% (68.5 -> 61.1), December 25d RR volatility -45% (7.3 -> 3.3)

- Last week, after a local breakout, BTC price continued to rise (triggered during traditional financial market clearing) --- initial support at 68--68.25k, strong support at 66.75--67k.

- Major resistance is around 70k-70.25k; if it breaks through completely, it will challenge the historical high again.

- If it falls below 66.75k, there may be a volatile consolidation period in the 63.5--67k range.

Major Market Events:

- The ETH ETF launched on July 23 still did not drive spot prices up, resulting in the liquidation of ETH long positions, with the ETH/BTC exchange rate falling below 0.05.

- At the highly anticipated Bitcoin 2024 summit, Trump delivered a keynote speech, in addition to his usual support for cryptocurrencies, he announced that the U.S. would not sell its held BTC but would use it to establish a strategic reserve (but did not mention previous rumors about new BTC purchases for reserves).

- Before the ETH ETF launch and Trump's speech, the implied volatility of BTC and ETH at the front end fluctuated sharply, with high-frequency actual volatility performing strongly during the event, but the final actual volatility was much lower than the implied volatility.

- The traditional financial market experienced higher volatility, while macro trading quickly closed positions, leading to noticeable differentiation and sector rotation within the stock market.

ATM Implied Volatility:

- This week, the implied volatility of short-term contracts showed significant fluctuations, especially during Trump's keynote speech at the Bitcoin 2024 summit, with related straddle option premiums concentrated in the 4.0--5.5% range. Despite bullish announcements, spot prices failed to break through 70k, leading to a significant drop in implied volatility of front-end futures contracts after the event, waiting for new catalysts to continue pushing spot prices up. The upcoming week in the cryptocurrency market is relatively quiet, with market focus shifting to the Federal Reserve, as the market expects a 15% probability of interest rate cuts given recent U.S. data trends.

- In longer maturities (September and beyond), although BTCUSD spot reached a new high this week, implied volatility continues to show a linear downward trend, as the bullish narrative has not garnered much attention, and long-term top demand is weak. At the same time, a large supply of December top contracts is noted.

- Despite BTC/USD spot prices reaching a new high this week, implied volatility in longer maturities (September and beyond) has been steadily declining. This is due to the market's bullish sentiment gradually calming, and the demand for long-term call options has also weakened. Additionally, a large supply of December call options is noted.

- High-frequency actual volatility increased during the event, approaching 50 (up from the low 40s last week), while the daytime fixed actual volatility also approached 50, despite underperforming during the actual event.

Skew/Convexity:

- This week, the slope of implied volatility significantly declined (the IV on the bullish side relative to the bearish side premium narrowed), completely retracing last week's increase and further decreasing.

- A negative correlation between spot prices and implied volatility was observed in the far forward contracts, meaning that as spot prices rise, implied volatility decreases.

- This is mainly due to the continued supply of year-end call options this week, while the demand observed last week has weakened. If spot prices fail to break through 70k and return to the established range, it can be expected that the slope of implied volatility will face further pressure.

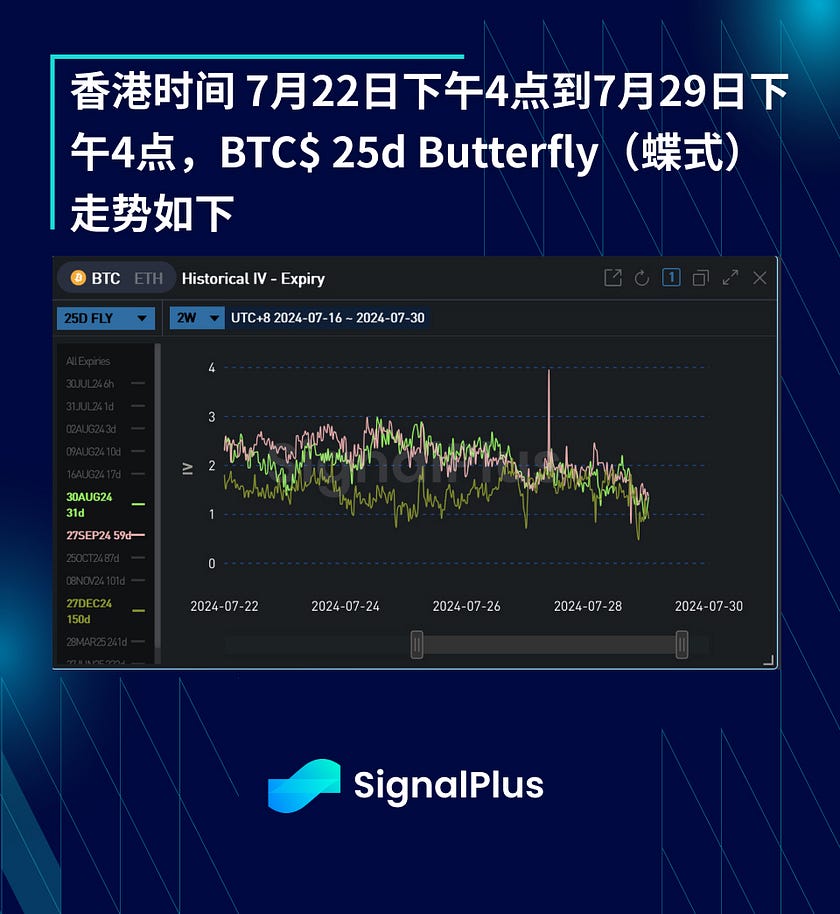

- This week, convexity changes were relatively flat, consistent with the downward adjustment of the benchmark volatility, facing some downward pressure.

- Although volatility remains high in the current environment, the correlation between risk reversal and spot has weakened locally due to supply and demand dynamics, thus weakening the performance of convexity locally.

- Overall, we can still observe structural supply of wing premium in covered strategies and call spreads, with an increase in selling of wing options this week.

Wishing you good luck this week!

Related tags

ChainCatcher reminds readers to view blockchain rationally, enhance risk awareness, and be cautious of various virtual token issuances and speculations. All content on this site is solely market information or related party opinions, and does not constitute any form of investment advice. If you find sensitive information in the content, please click "Report", and we will handle it promptly.

Related reading