Andrew Kang's new article: Why I believe Ethereum cannot replicate the success of Bitcoin ETFs?

After the ETF launch, the expected trading price of ETH is between $2400 and $3000.

After the ETF launch, the expected trading price of ETH is between $2400 and $3000.Original Title: “The Impact of the Ethereum ETF ETF - An analysis”

Author: Andrew Kang

Translation: Shenchao TechFlow

The BTC ETF has opened the door for many new buyers to allocate Bitcoin in their portfolios. The impact of the ETH ETF is less clear.

When Blackrock submitted its ETF application, Bitcoin was priced at $25,000, and I was very bullish on Bitcoin. Now, Bitcoin's return has reached 2.6 times, while ETH's return is 2.1 times. From the cycle bottom, BTC's return is 4.0 times, and ETH's return is also 4.0 times. So, how much upside can the ETH ETF bring? I don't think it will be significant unless Ethereum develops a convincing way to enhance its economic benefits.

Traffic Analysis

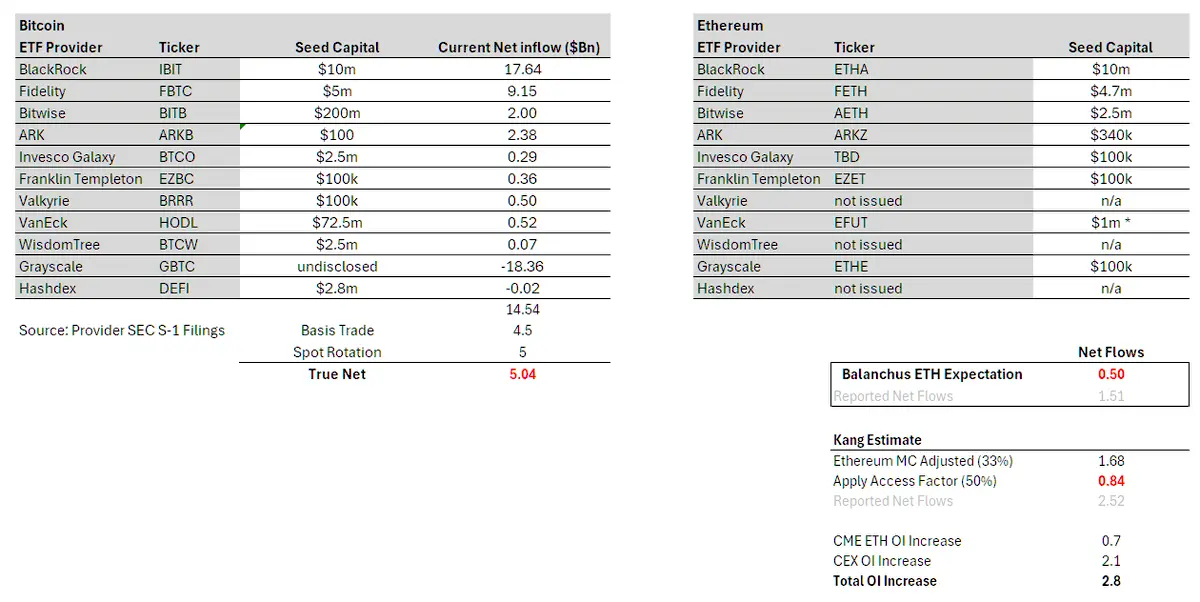

The Bitcoin ETF has accumulated a total of $50 billion in assets under management, which is an astonishing figure. However, if we break down the net inflows since the Bitcoin ETF was launched, excluding the existing GBTC assets under management and rotations, the net inflow is $14.5 billion. However, this is not real capital inflow, as many delta-neutral flows need to be accounted for, namely basis trades (selling futures, buying spot ETFs) and spot rotations. Based on CME data and analysis of ETF holders, I estimate that about $4.5 billion of the net inflow can be attributed to basis trading. ETF experts suggest that large holders like BlockOne have also converted a significant amount of spot BTC into ETFs - roughly estimated at $5 billion. After deducting these capital flows, we can conclude that the true net buying amount for the Bitcoin ETF is $5 billion.

From here, we can simply infer about Ethereum. @EricBalchunas estimates that Ethereum's flow might be 10% of BTC's. This results in a true net buying flow of $500 million over six months, while the reported net flow is $1.5 billion. Although Balchunas has a bias in approval odds, I believe his lack of interest/pessimism regarding the ETH ETF is valuable and reflects broader traditional financial interest.

Personally, my benchmark is 15%. Starting from the $5 billion true net value of BTC, adjusting based on ETH's market capitalization (which is 33% of BTC) and a 0.5 access coefficient*, we arrive at a true net buying amount of $840 million and a reported net value of $2.52 billion. There are reasonable arguments that ETHE's turnover is lower than GBTC's, so in an optimistic scenario, I believe the true net buying amount is $1.5 billion, and the reported net buying amount is $4.5 billion. This is about 30% of BTC's flow.

In any case, the true net buying amount is far below the derivative flow at the ETF front end ($2.8 billion), not including the spot front end flow. This means that the ETF's pricing has exceeded the actual price.

*Due to the different holder bases, ETFs can benefit BTC significantly more than ETH, so the access coefficient adjusts the flow for the ETF. For example, BTC is a macro asset, more attractive to institutions with access issues—macro funds, pensions, endowments, sovereign wealth funds—while ETH is more like a tech asset, appealing to venture capital firms, crypto funds, tech experts, and retail investors who face fewer restrictions in accessing cryptocurrencies. By comparing the CME OI to market cap ratio of ETH to BTC, we can derive 50%.

From CME data, prior to the ETF launch, ETH's OI was significantly lower than BTC's. OI was about 0.30% of the supply, while BTC was 0.6%. Initially, I thought this was a sign of "prematurity," but it could also be said that it masked the smart trading capital's lack of interest in the ETH ETF. Traders on the street made good trades on BTC, and they often have good information, so if they are not repeating the trades on ETH, there must be a good reason, which could indicate weak liquidity intelligence.

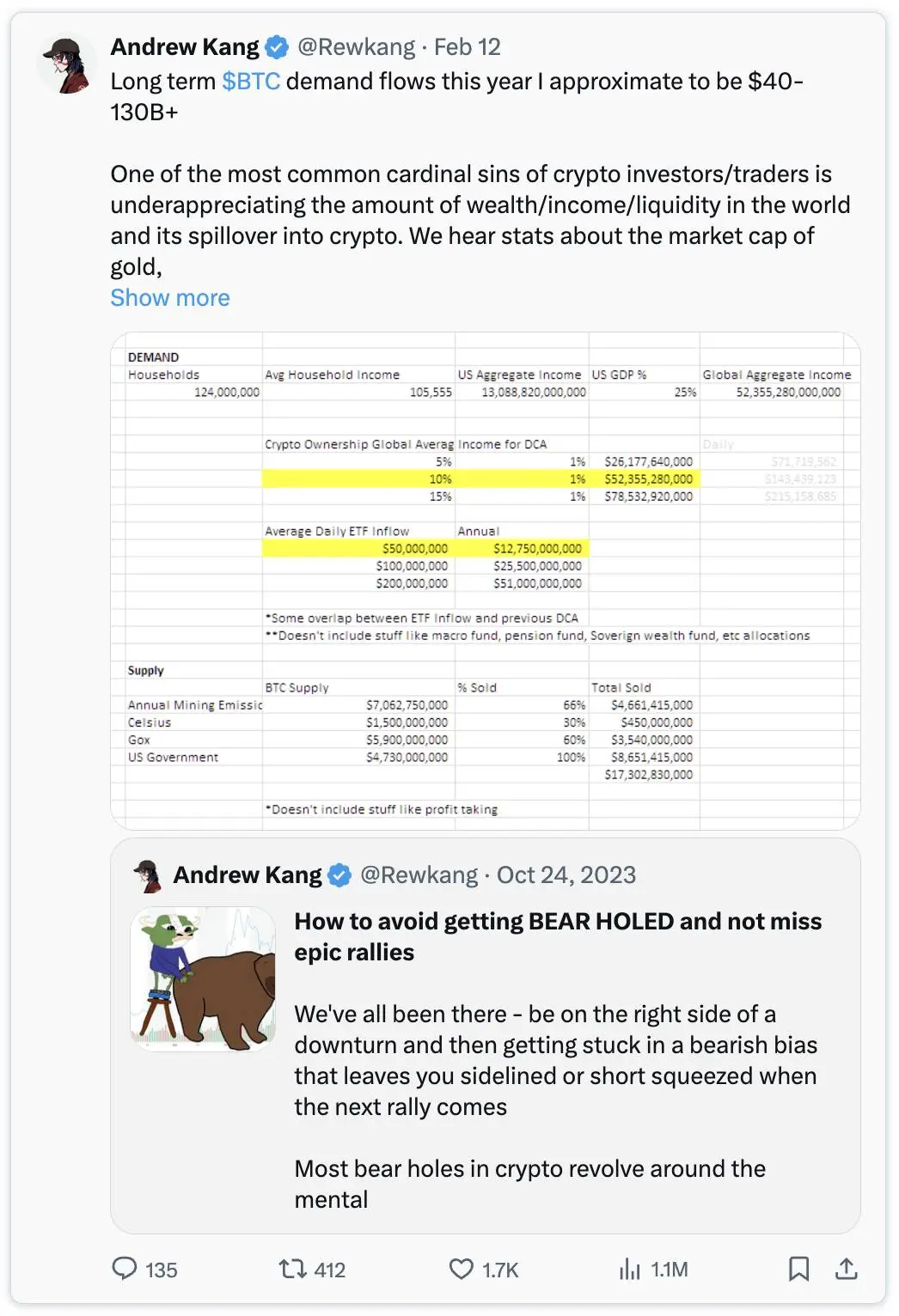

How did $5 billion take BTC from $40,000 to $65,000?

The short answer is no. There are many other buyers in the spot market. Bitcoin is a truly validated asset globally, an important portfolio asset, and has many structural accumulators—Saylor, Tether, family offices, high-net-worth individuals, etc. ETH also has some structural accumulators, but I believe their number is lower than BTC's.

Keep in mind that before the ETF appeared, Bitcoin's holdings had already reached $69,000/1.2T+ BTC. Market participants/institutions hold a significant amount of spot cryptocurrencies. Coinbase has $193 billion in custody, with $100 billion coming from its institutional program. In 2021, Bitgo reported an AUC of $60 billion, and Binance's custody exceeds $100 billion. Six months later, the ETF held 4% of Bitcoin's total supply, which is meaningful but only part of the demand equation.

Between MSTR and Tether, there have already been billions of additional buy orders, but not only that, the positions entering the ETF are insufficient. At that time, there was a popular view that ETFs were sell-the-news events/market tops. Therefore, billions of short-term, medium-term, and long-term momentum sells need to be bought back (2x flow impact). Additionally, once ETF capital flows experience significant fluctuations, shorts also need to cover. After entering the issuance phase, open interest actually declined—this is truly incredible.

The positioning of the ETH ETF is quite different. ETH's price is 4 times the low, while BTC's price is 2.75 times the pre-launch price. The native CEX OI of cryptocurrencies increased by $2.1 billion, bringing OI close to ATH levels. The market is (semi) efficient. Of course, many crypto natives see the success of the Bitcoin ETF and have similar expectations for ETH, positioning themselves accordingly.

I personally believe that the expectations of crypto natives are overly exaggerated and disconnected from the real preferences of trading allocators. Those deeply involved in the cryptocurrency space naturally have a relatively high awareness and purchasing power for Ethereum. In fact, Ethereum, as a major portfolio allocation for many non-native crypto capitals, has a much lower purchasing rate.

One of the most common promotions to traders is to position Ethereum as a "tech asset." Global computers, Web3 app stores, decentralized finance settlement layers, etc. This is a good promotion, and I have bought into it in previous cycles, but when you look at the actual numbers, it becomes hard to sell.

In the last cycle, you could point to the growth rate of fees and argue that DeFi and NFTs would create more fees and cash flow, presenting a compelling tech investment case similar to tech stocks. But in this cycle, the quantification of fees has backfired. Most charts will show you flat or negative growth. Ethereum is a "cash machine," but its 30-day annualized income is $1.5 billion, with a PS ratio of 300 times, and inflation-adjusted earnings/PE ratio being negative. How can analysts justify this price to their family office or their macro fund boss?

I even expect that due to two reasons, the fugazi (delta-neutral) flow in the first few weeks will be relatively low. First, the approval was unexpected, and the issuers did not have much time to persuade large holders to convert their ETH into ETF form. The second reason is that the appeal of conversion is lower for holders, as they need to give up the gains from market watching, farming, or using ETH as collateral for DeFi. But note that the staking rate is only 25.

Does this mean ETH will go to zero? Of course not, at a certain price, it will be considered valuable, and when BTC rises in the future, it will also be dragged up to some extent. Before the ETF launch, I expected ETH to trade between $3,000 and $3,800. After the ETF launch, my expectation is $2,400 to $3,000. However, if BTC rises to $100,000 by the end of Q4 2025/Q1, this could drag ETH to reach ATH, but the ETHBTC trading pair will be lower. In the long run, the development is promising; you must believe that Blackrock/Fink is doing a lot of work to put some financial trajectories on the blockchain and tokenize more assets. How much value this will bring to ETH and the timing is still uncertain.

I expect the ETHBTC trading pair to continue to decline, next year it will be between 0.035 and 0.06. Although our sample size is small, we do see ETHBTC making lower highs in each cycle, so this is not surprising.