SignalPlus Macro Analysis (20240424): Bad News is Good News

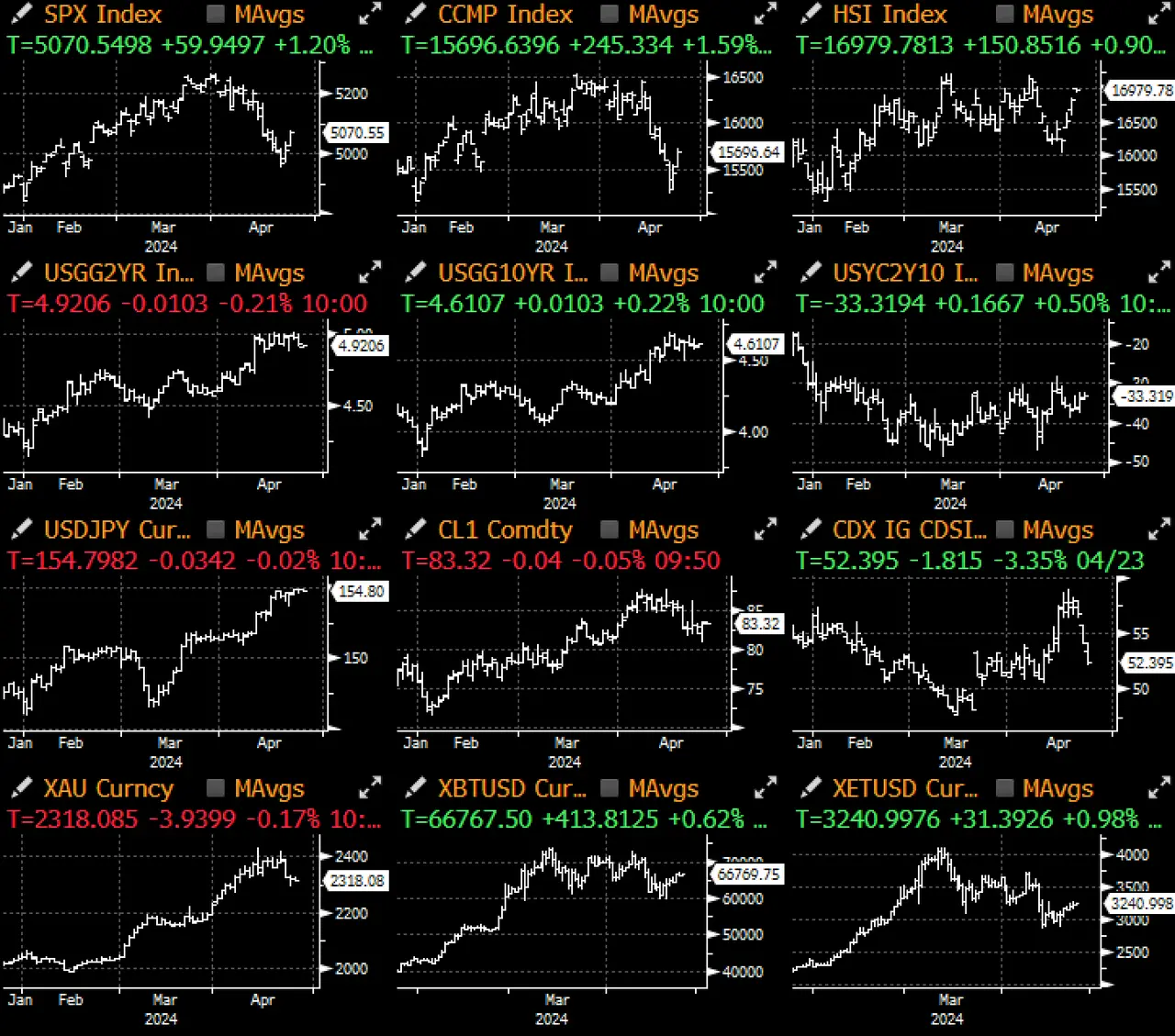

"Bad news is good news" returns again, as the slowdown in the manufacturing PMI in April boosted risk market sentiment, with the overall data falling below 50, lower than the expected 52. Cryptocurrency prices remain strong, with BTC approaching $67,000 again.

"Bad news is good news" returns again, as the slowdown in the manufacturing PMI in April boosted risk market sentiment, with the overall data falling below 50, lower than the expected 52. Cryptocurrency prices remain strong, with BTC approaching $67,000 again.

"Bad news is good news" makes a comeback, as the slowdown in April's manufacturing PMI boosted risk market sentiment, with the overall data falling below 50, lower than the expected 52. The main reasons for this were the weak performances in new orders (49.5 vs 52.6), output (51.1 vs 54), and employment (51.9 vs 52.2). The subsequently released services PMI also unexpectedly softened to 50.9, below the expected 51.7, with new business and employment (47.3 vs 51.1) experiencing a significant decline, the latter hitting its lowest level since the pandemic.

U.S. Treasuries rebounded, with the 2-year yield showing a bull steepening trend, retreating from around 5% to 4.92%. The dollar also softened, with the euro rising above 1.07 against the dollar, while the dollar remained below 154.85 against the yen. The weak economic data reignited hopes for rate cuts, with tech stocks leading the market rebound, gaining 1.5%.

More notably, the official comments from S&P economists indicated that recent economic activity "may slow in the coming months, as new business inflows in April saw a decline for the first time in six months," which "prompted companies to cut jobs at a pace not seen since the global financial crisis (excluding the pandemic)." This indeed presents a sobering outlook.

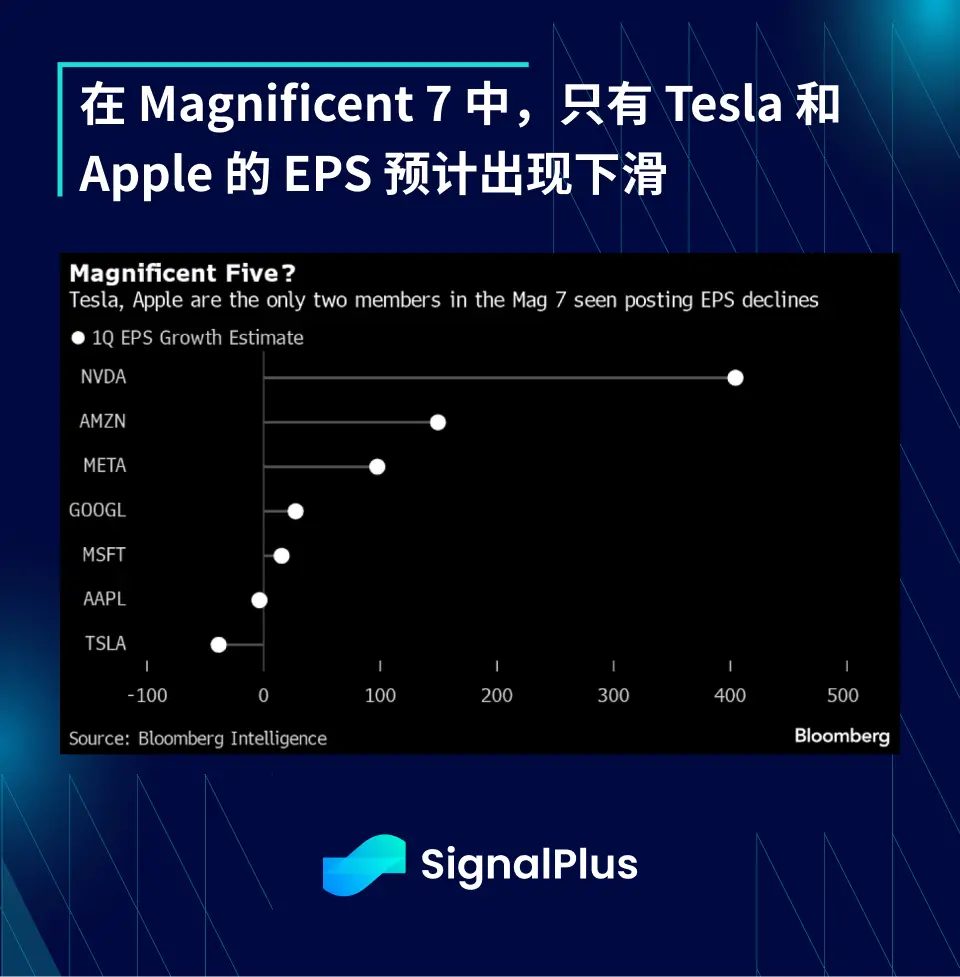

Additionally, as a sign of further short-squeeze, Tesla's stock rose 13% in after-hours trading following its Q1 earnings report, despite its profits, revenue, and margins falling significantly below market expectations. The company's global inventory jumped from a supply of 15 days to 28 days, indicating signs of slowing demand; however, from the price trends, investors seem well-prepared for the weak earnings report.

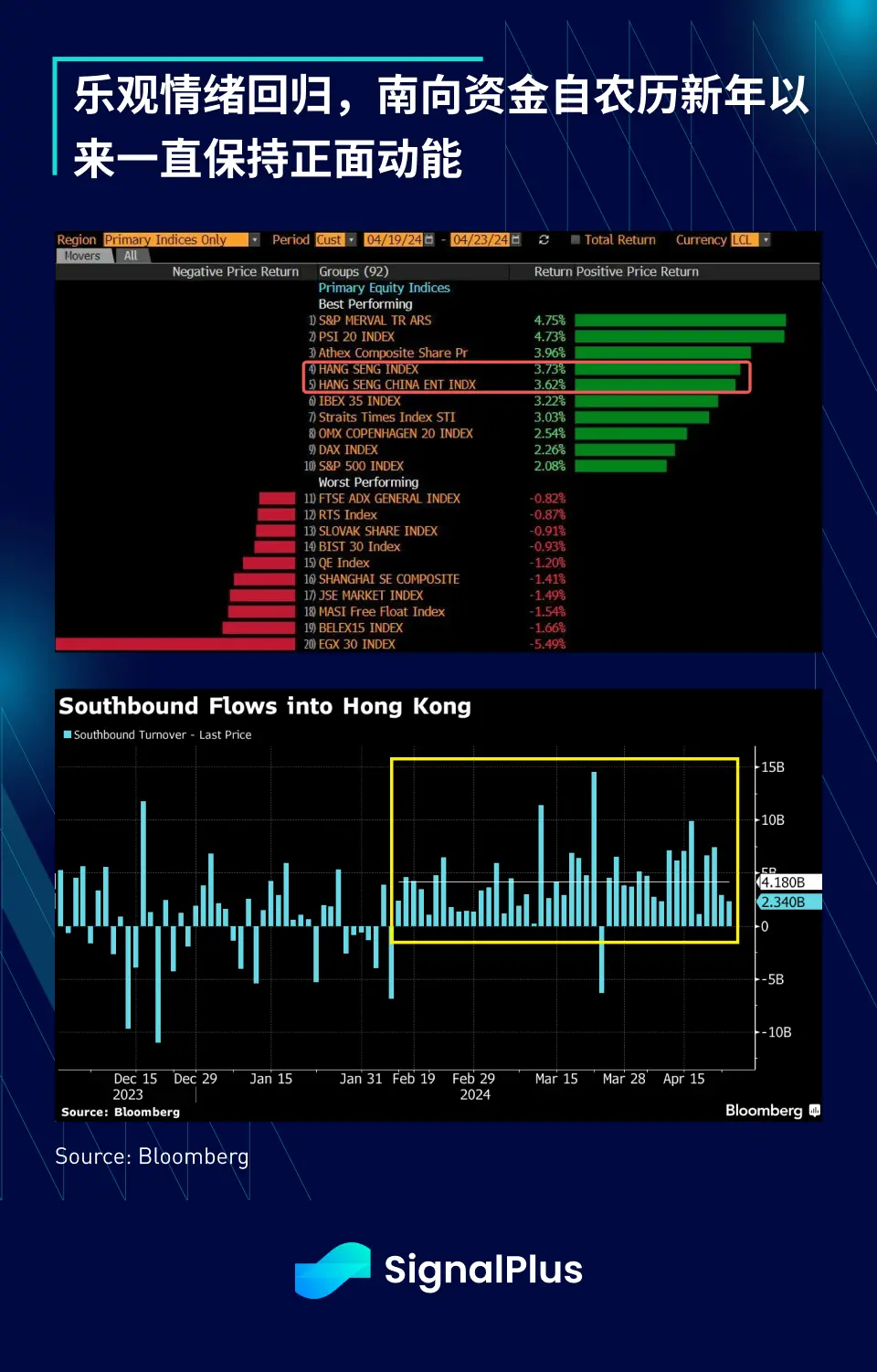

On other fronts, some optimism has re-emerged in Asia, with the HSI and HSCEI outperforming most developed market indices last week, something that hasn't happened in a long time. Since the Lunar New Year, with the exception of one week, the weekly inflow of southbound funds into Hong Kong has been positive, indicating that the actions of regulatory authorities following the supportive policy shift earlier this year have indeed brought some substantial positive effects.

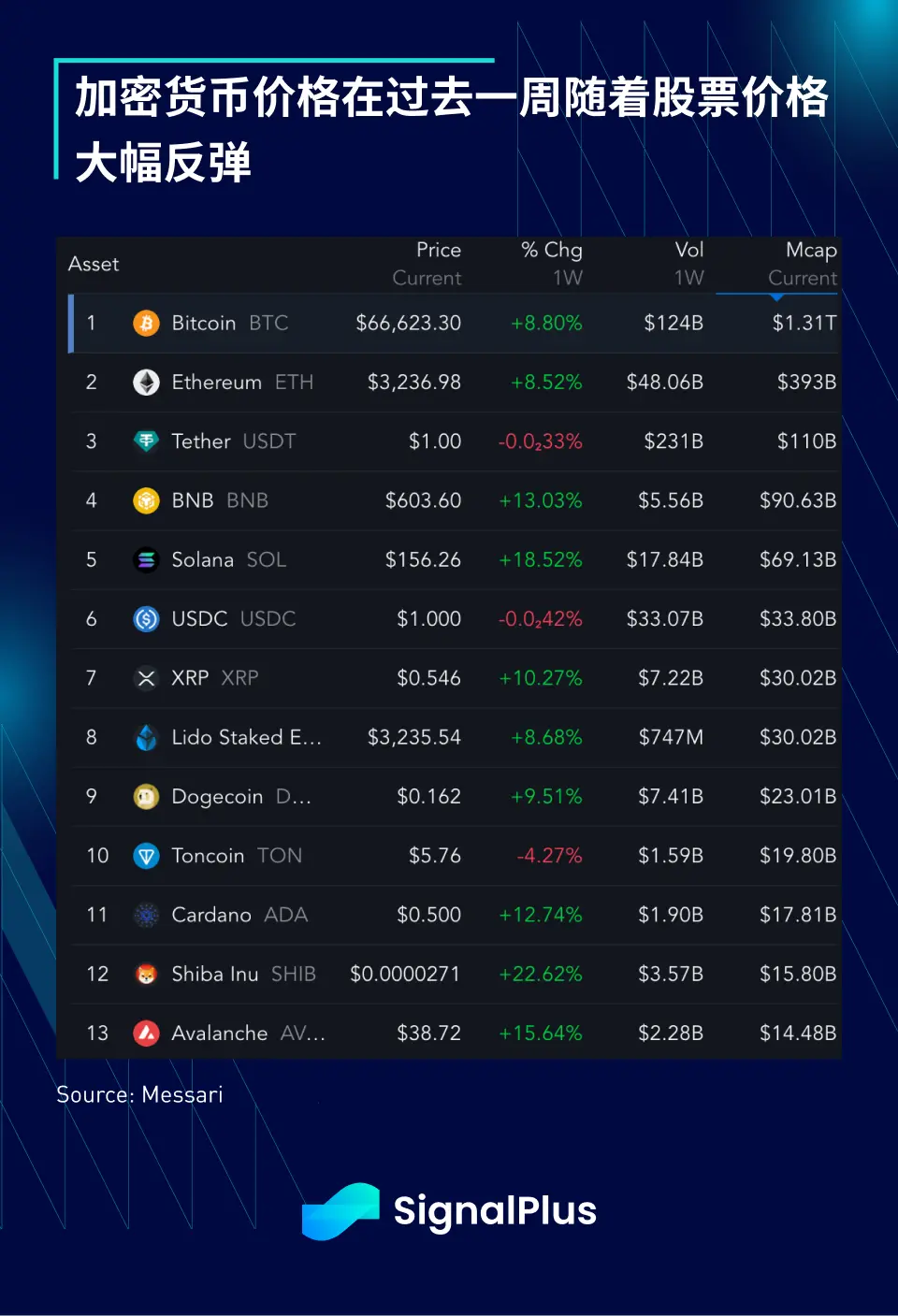

Cryptocurrency prices remain strong, with BTC once again approaching $67,000, and altcoins rebounding 10-20% over the past week. While some may view the halving as the main positive driver for the market, we believe that the multiple dips to the $60,000 level have cleared out a significant number of short-term bulls, intensifying the current short squeeze. Prices are expected to reflect the recovery of stock market sentiment in the coming days, leading up to the release of PCE data, which, if weak, could serve as a catalyst for BTC to pull back above $70,000. Good luck!