SignalPlus Macro Analysis (20240416): Short-term Downside Risk in US Stocks

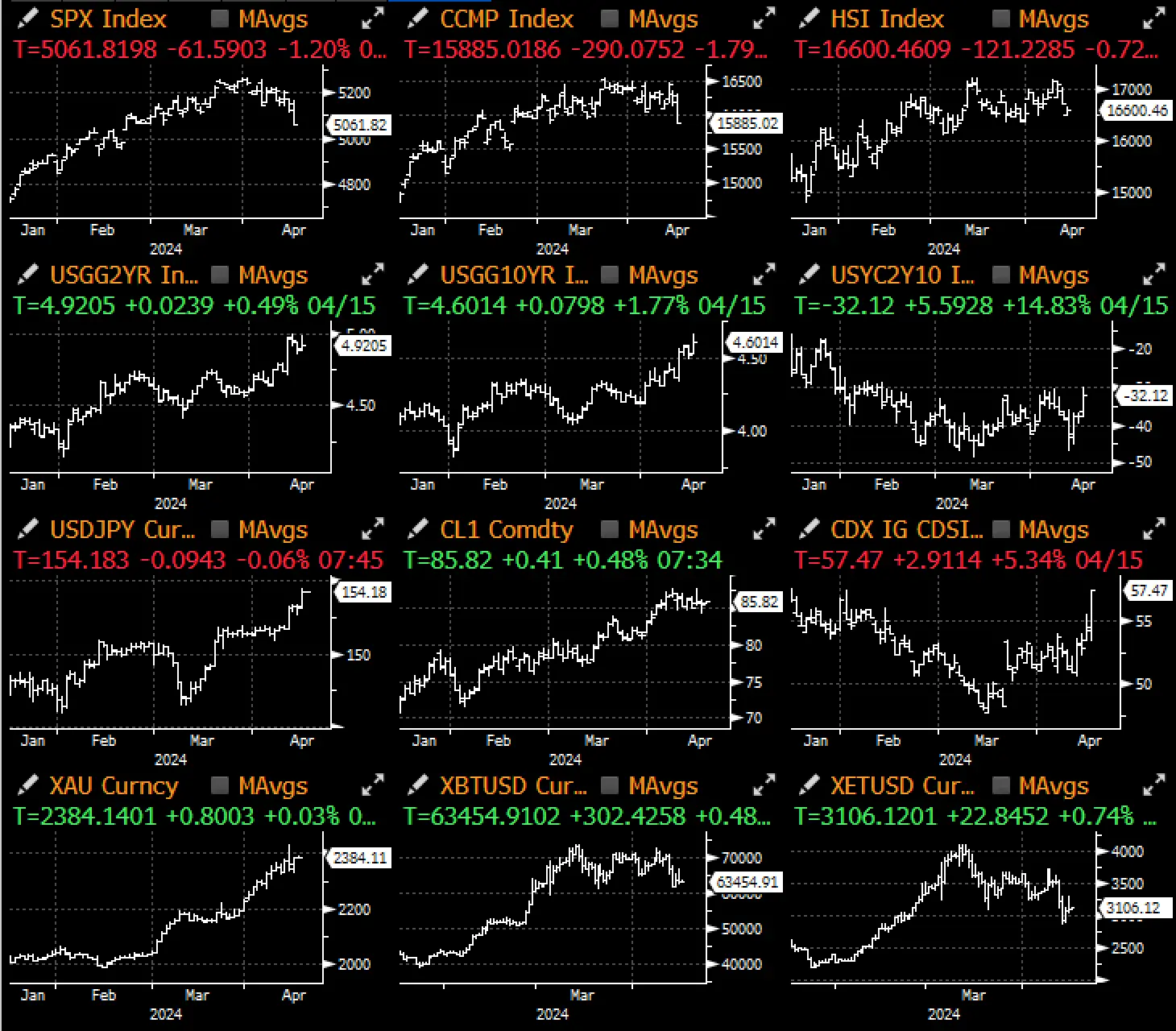

Okay, the market has finally started to focus. Due to reasons such as the AI boom, a dovish Federal Reserve, and a low likelihood of economic recession, the market has been in a complacent state for a long time, ignoring all macro concerns and event risks, and we are finally seeing a significant change in the behavior of American investors...

Okay, the market has finally started to focus. Due to reasons such as the AI boom, a dovish Federal Reserve, and a low likelihood of economic recession, the market has been in a complacent state for a long time, ignoring all macro concerns and event risks, and we are finally seeing a significant change in the behavior of American investors...

Finally, the market has started to focus.

Due to the AI boom / dovish Federal Reserve / low probability of economic recession, the market has been in a complacent state for a long time, ignoring all macro concerns and event risks. We have finally seen a significant change in the behavior of American investors, with a massive sell-off in the market at the New York opening after a substantial recovery during overnight trading in Asia.

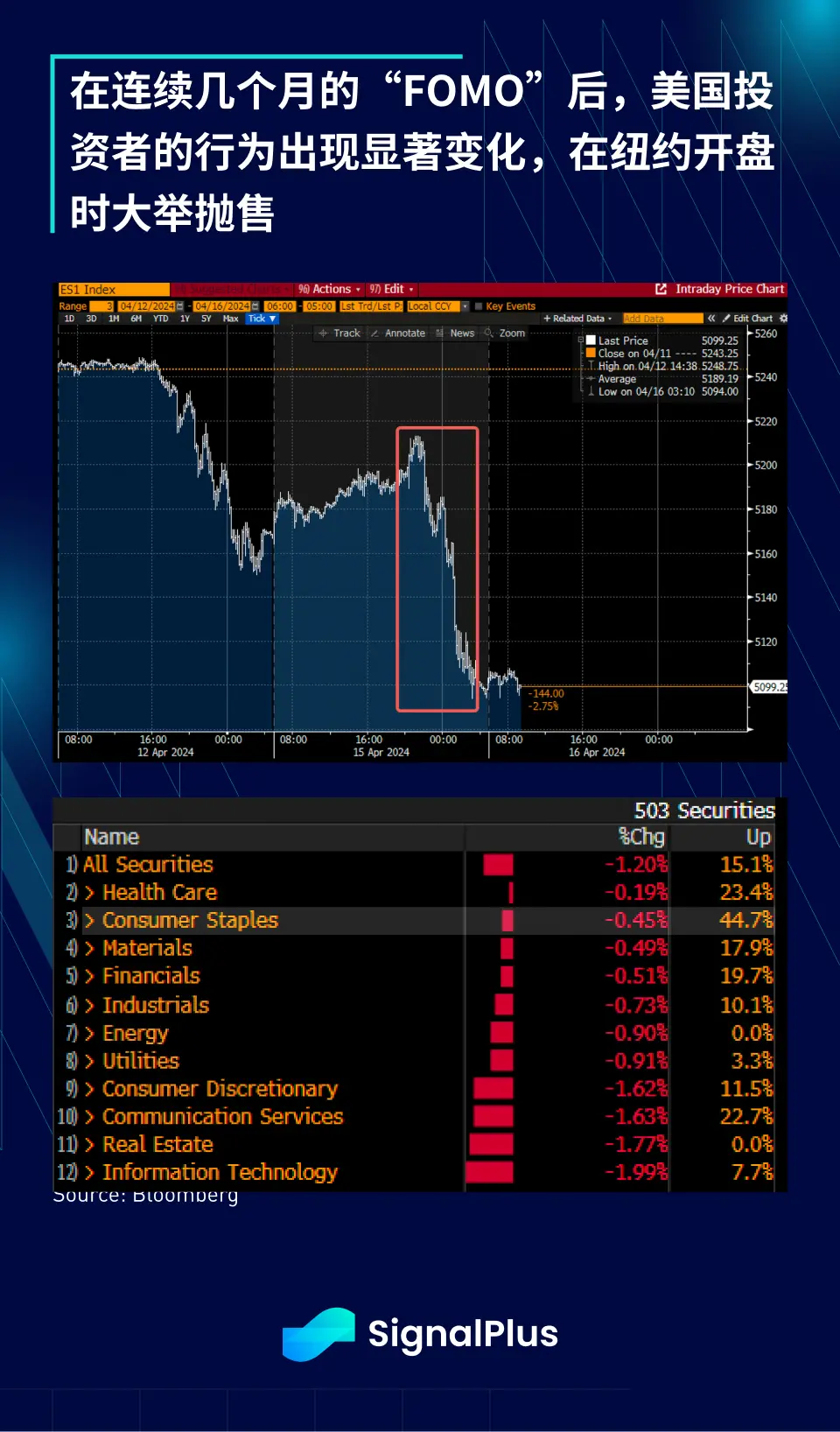

For a long time, we have been accustomed to buying the dip in the U.S. market. After several months of continuous rises, short sellers in the stock market have almost disappeared. Has the recent rise in yields (2-year ~ 4.9%) begun to affect overall sentiment and change the behavior of stock investors? Are the losses in fixed income and cryptocurrency markets enough to prompt a shift to a defensive stance? While it may be too early to draw conclusions, we can certainly feel the early tremors, especially with the earnings season set to unfold in the next 2-3 weeks, which is definitely worth our continued attention.

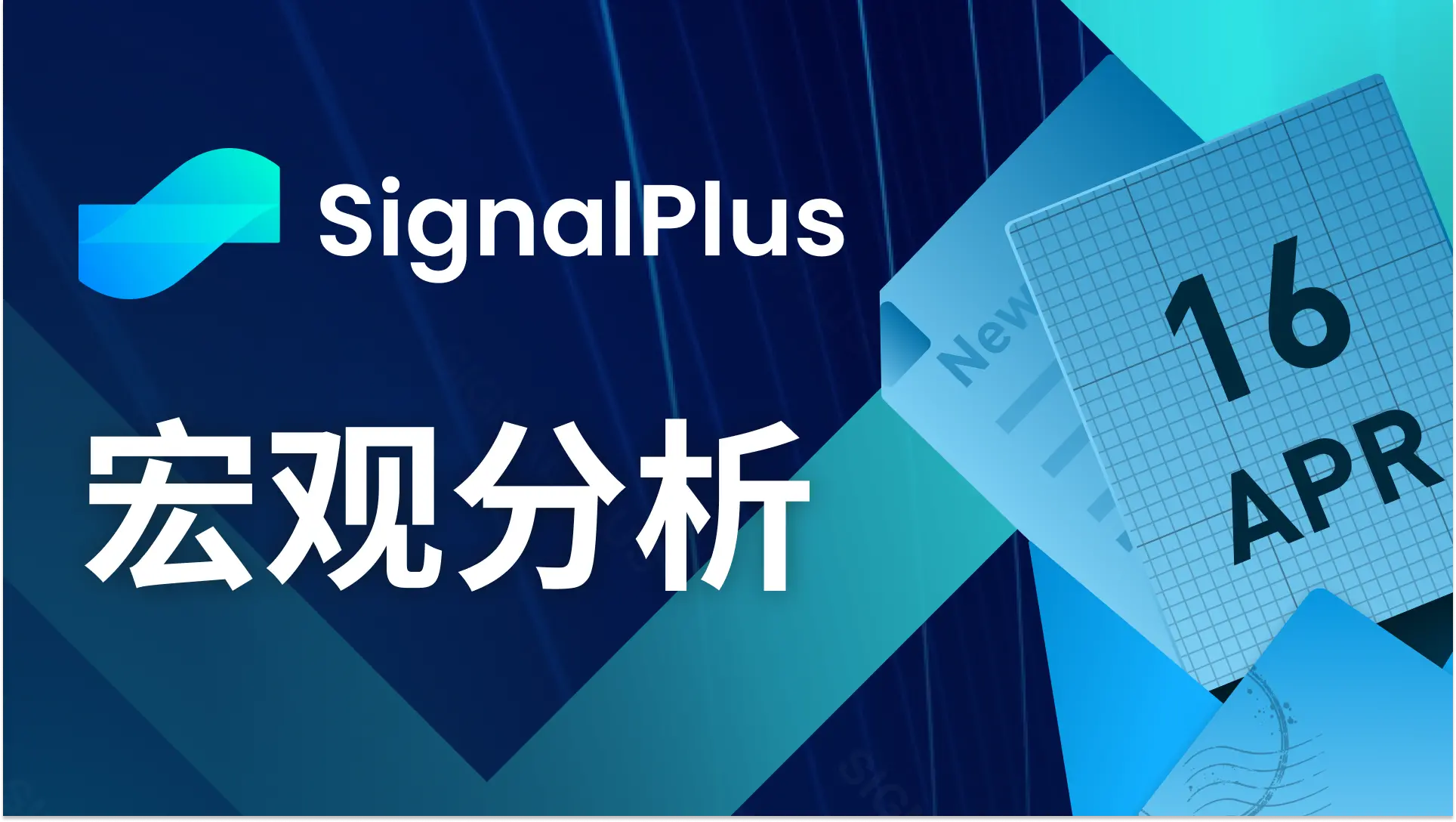

In terms of economic data, the outstanding performance of American consumers continues, with March retail sales showing a significant increase, with a month-on-month growth of 0.7%, and a month-on-month growth of 1.1% excluding automobiles, both significantly exceeding expectations. Core spending, control group, and physical goods all performed strongly. The continued resilience of consumers will help raise GDP forecasts and put pressure on the possibility of interest rate cuts, with the likelihood of a rate cut in June now below 20%.

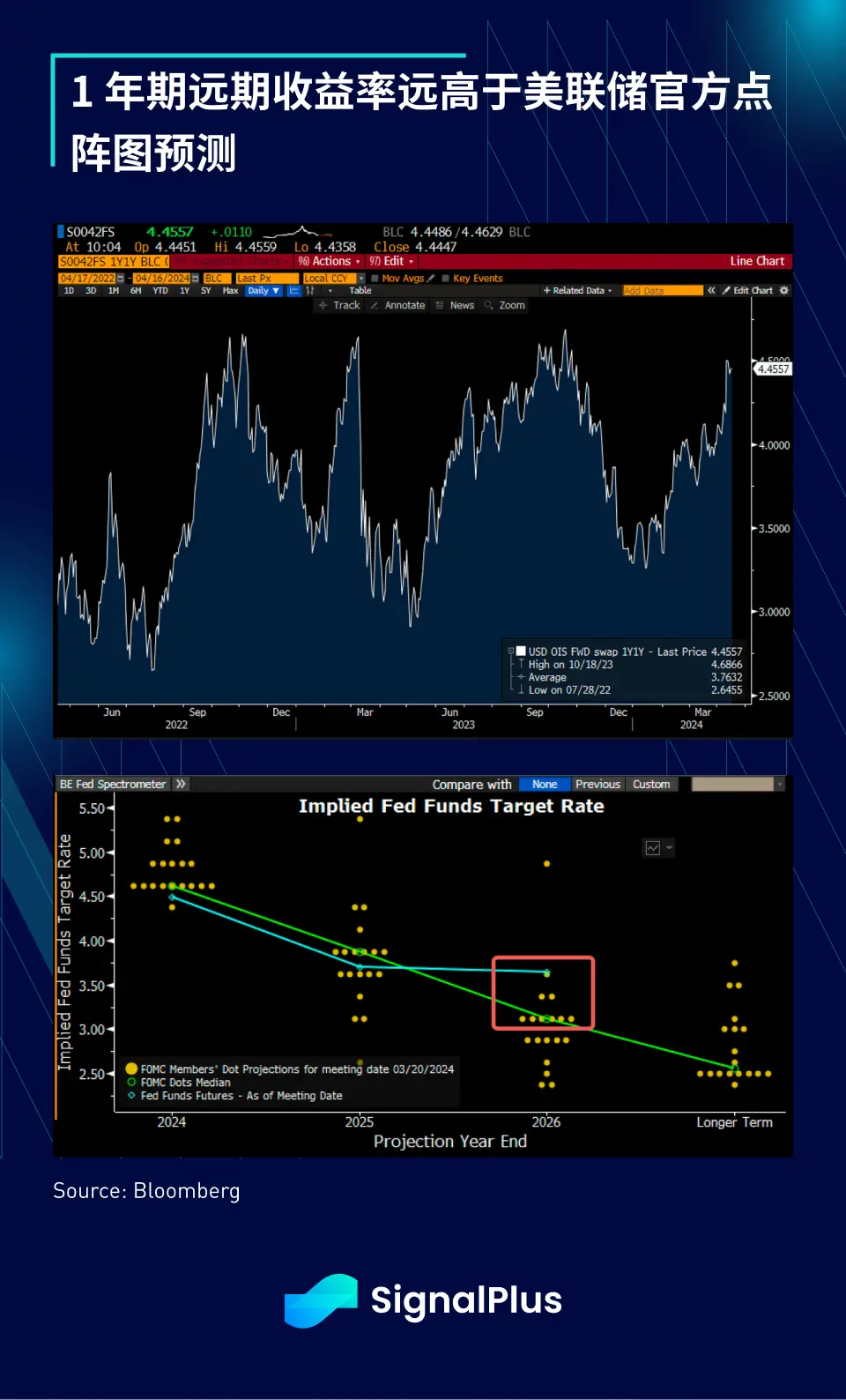

While the Federal Reserve continues to seek creative narratives to support its dovish stance (New York Fed's Williams: "Still expect rate cuts to begin this year"), inflation expectations have risen sharply, and the interest rate market is undergoing self-adjustment, with the 5-year breakeven inflation rate returning to above 2.5%, the highest level in over a year, while the CPI trajectory at that time was vastly different from now. The 2-year U.S. Treasury yield is close to 5%, indicating that the trajectory of the 1-year forward yield is much higher than the Fed's own dot plot forecast.

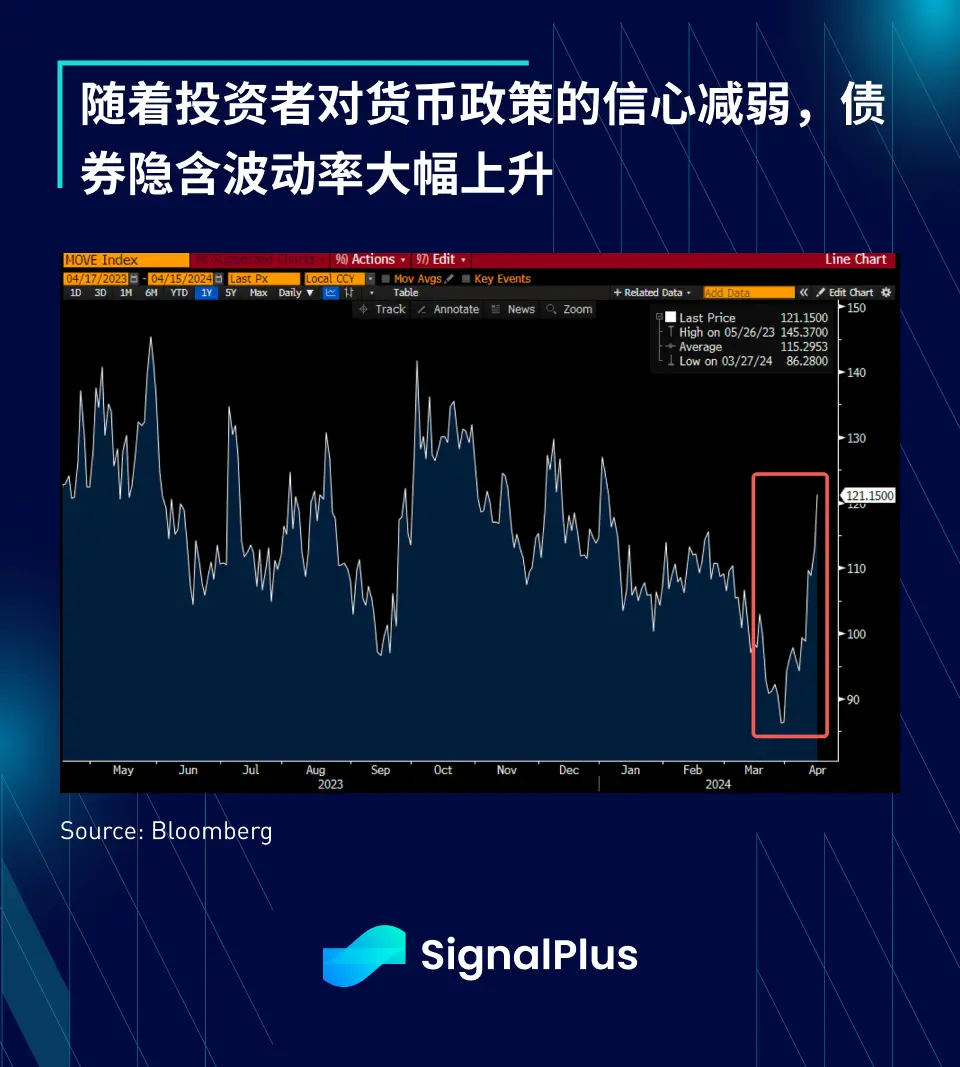

The MOVE index, representing implied volatility in fixed income, has risen sharply, highlighting market unease with the Fed's dovish narrative. Fed officials have attempted to suppress bond volatility through carefully orchestrated talks in the first quarter; however, as dovish guidance becomes increasingly inconsistent with economic strength and inflation pressures, the market has shown some degree of resistance.

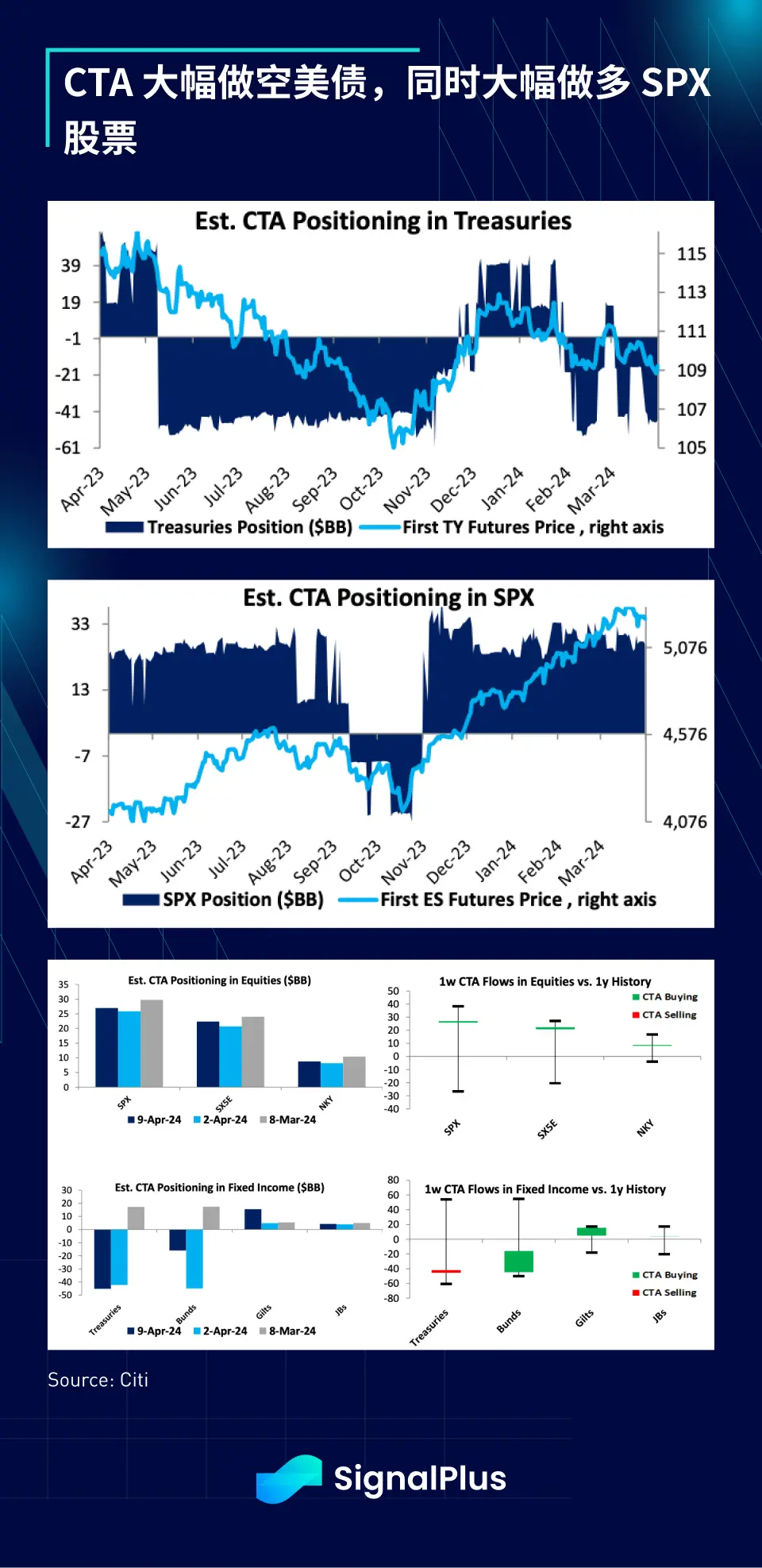

In fact, beyond interest rates, the overall volatility of macro assets, including stocks and high-yield bonds, is rising, and the leverage positions in bonds and stocks are in relatively extreme situations, with CTAs heavily shorting bonds (as yields rise) while going long on stocks to the extreme.

This extreme positioning could lead to more volatile price movements in the coming weeks, especially considering the highly tense geopolitical situation and the extremely high earnings expectations for this quarter. If the SPX closes below the 200-day moving average this week, it may force CTAs to change their long positions, which last occurred in the summer of 2023, followed by a further decline of about 5%.

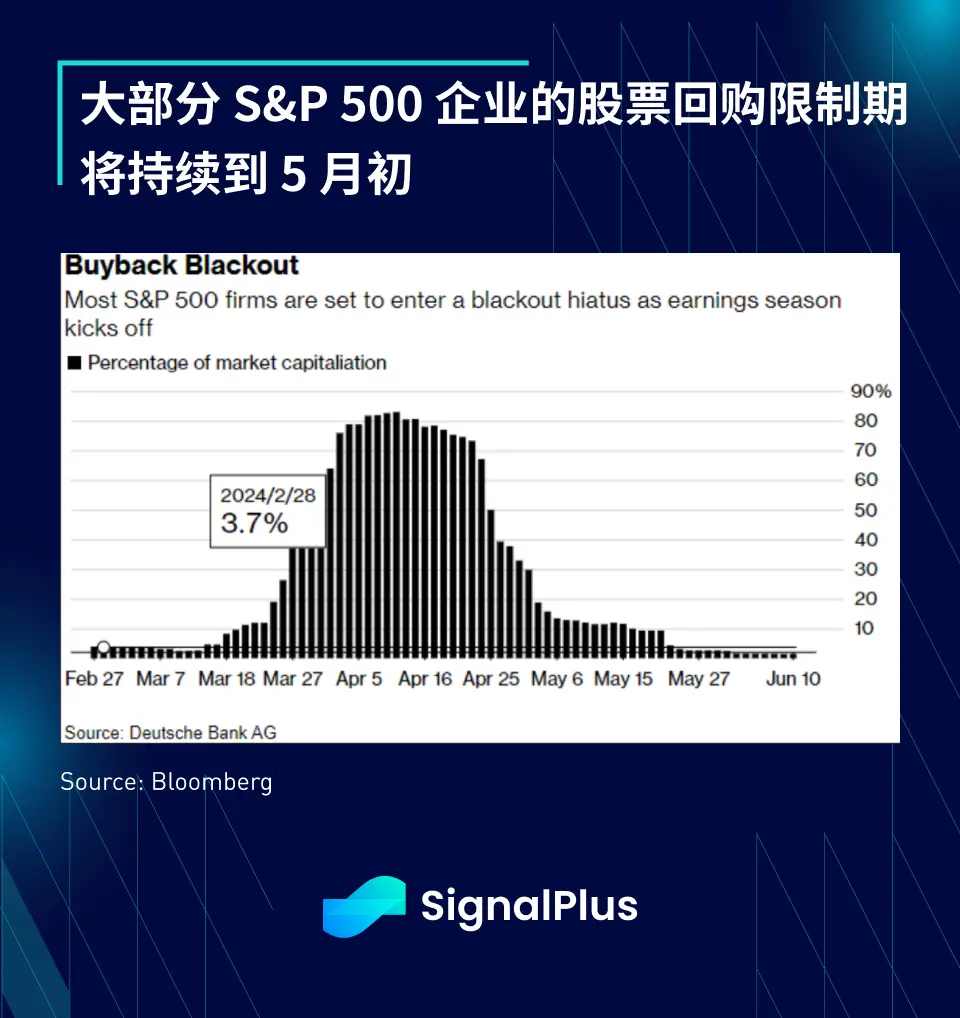

Finally, the blackout period for stock buybacks will last until the first week of May, posing further downside risks to the stock market in the short term, and caution is advised against bottom-fishing too early.

Cryptocurrency is also struggling in the overall gloomy sentiment, with BTC/ETH prices dropping 10% this week, while other major altcoins fell about 20% during this period, leaving traders facing very real losses and liquidation losses. Given the extent and speed of the decline, we believe that profit and loss management will become the main driving force in the coming weeks, rather than the halving narrative or other mainstream narratives, prompting investors to significantly reduce leverage.

The macro environment still needs some time to reach a new consensus and obtain clearer guidance and more certainty from the Federal Reserve, while fundamental investors will need corporate earnings to support their firm confidence in U.S. stocks at current high valuations. Good luck to everyone.