SignalPlus Macro Analysis (20240409): A Wave of Inflation Data is Coming Soon

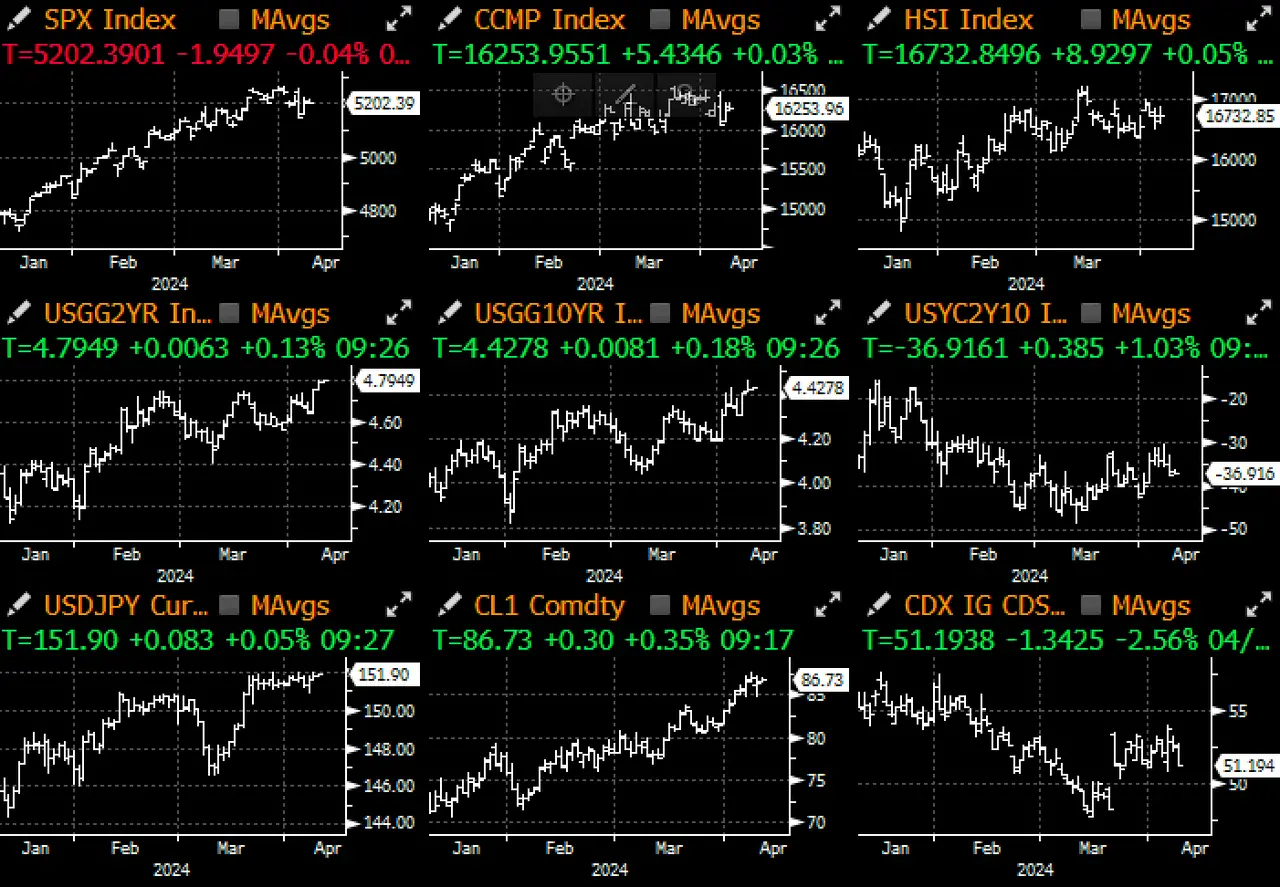

Yesterday, the market was relatively calm, taking a breather before the upcoming busy data releases. After the liquidation of leveraged long positions over the past week, cryptocurrency prices continued to rebound, coming within a step of their historical highs, with various altcoins taking turns to show good performance.

Yesterday, the market was relatively calm, taking a breather before the upcoming busy data releases. After the liquidation of leveraged long positions over the past week, cryptocurrency prices continued to rebound, coming within a step of their historical highs, with various altcoins taking turns to show good performance.

Yesterday, the market was relatively calm, taking a breather before a very busy schedule of data releases ahead. This week's data releases include China's new RMB loans, social financing scale, M2 money supply, CPI, PPI, trade balance, and in Europe, data on German industrial output, loan surveys, CPI from Sweden and Norway, as well as the European Central Bank meeting. In the UK, employment data, monthly GDP, and industrial production data will be released, while in the US, the focus will be on prices, including the New York Fed's 1-year inflation expectations, CPI, PPI, the University of Michigan consumer sentiment index, and inflation expectations. Central bank activities will include interest rate decisions from Singapore, Sweden, New Zealand, Canada, Thailand, the European Central Bank, and South Korea. Additionally, JPM, Citi, Wells Fargo, State Street, and BlackRock will all release their Q1 earnings reports this week, making it indeed a very busy week!

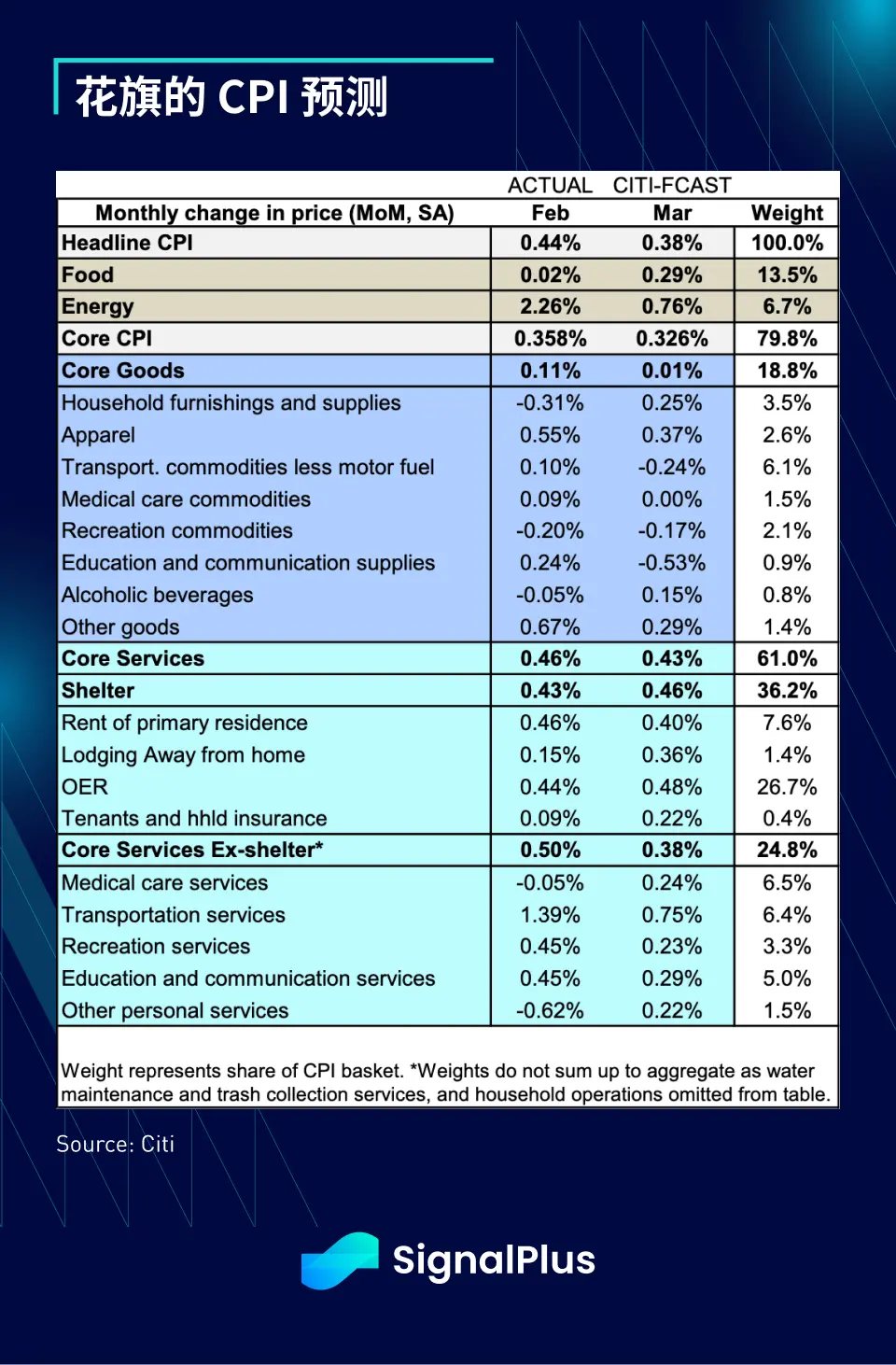

In the US, Wednesday's CPI will be the focus, with the market expecting core CPI year-on-year to slightly decline from 3.8% to 3.7%. Based on the rise in bond yields over the past few days, the market seems inclined to hedge against hawkish surprises. The implied SPX volatility from options straddles for Wednesday is around +/- 1%, while the average volatility on CPI release days over the past 12 months has been +/- 0.7%. It is worth noting that option prices have generally overestimated actual volatility over the past two years, as investors have been paying high prices for tail risk protection given the heightened focus on inflation during this cycle.

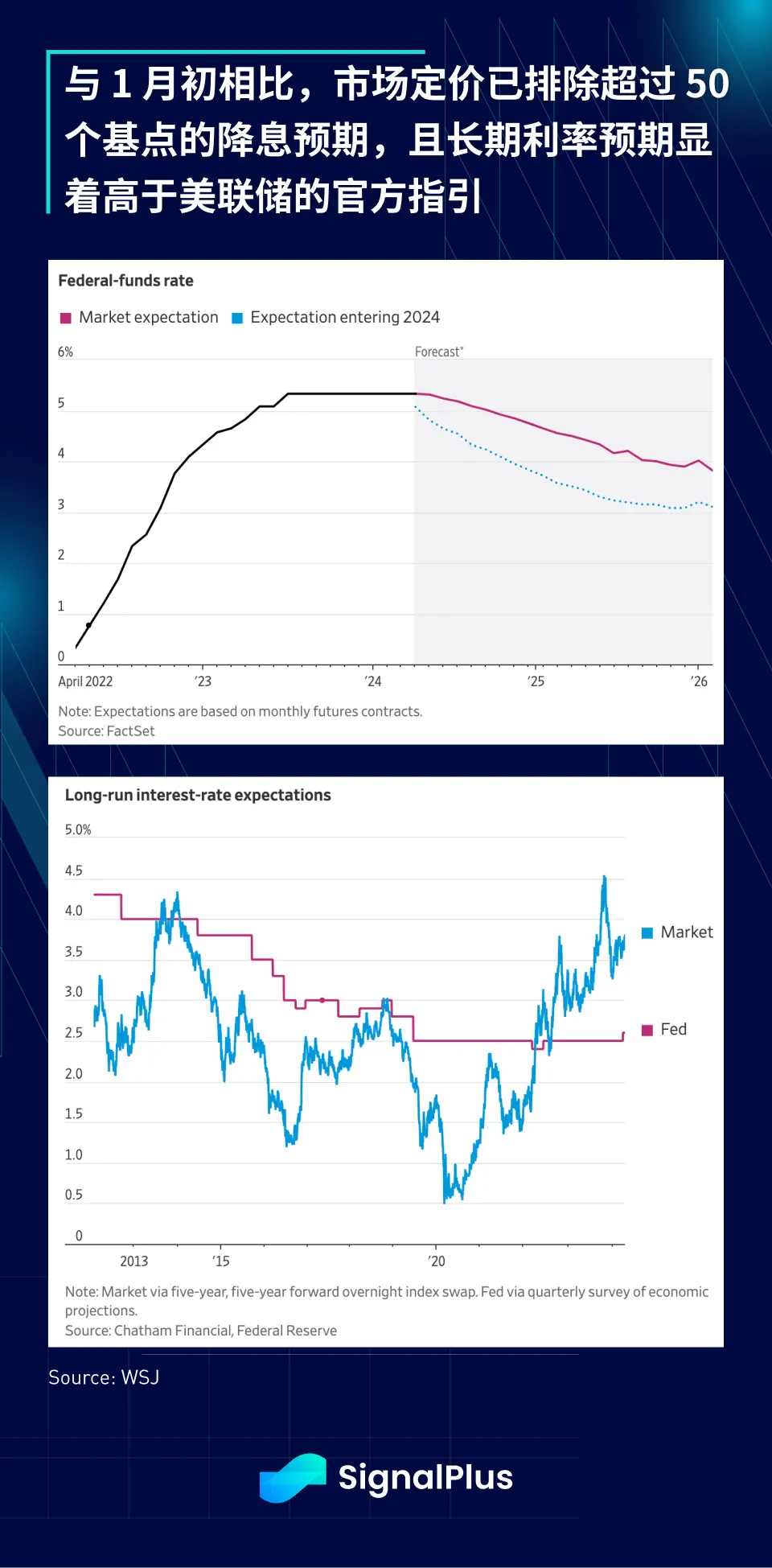

The fixed income market has fully returned to the belief that "high rates will last longer," with market pricing excluding more than 50 basis points of rate cut expectations compared to early January, and the current pricing of 2-year yields and long-term rates is significantly above the Federal Reserve's official guidance.

Speaking of volatility, Citigroup reports that the SPX has risen 23% over the past 6 months, with a maximum/minimum trading range of 24.4%, while actual volatility is at a low of 11.7%. The ratio of volatility to trading range is at its lowest level since January and is in the 1st percentile since 1983. As macro event risks have nearly dissipated, implied correlation has also fallen to a 10-year low, indicating that in a context of strong economic performance and corporate profits, market complacency is at an extremely high (extreme?) level.

In other words, since February 2023, the SPX has not experienced a -2% day (while BTC seems to have a 2% fluctuation every 8 hours recently). According to Citigroup's data, this is the 12th longest streak since 1928, with the longest record occurring from 2005 to 2008, lasting over 900 days. However, the current complacency in the US stock market undoubtedly contrasts sharply with the global situation.

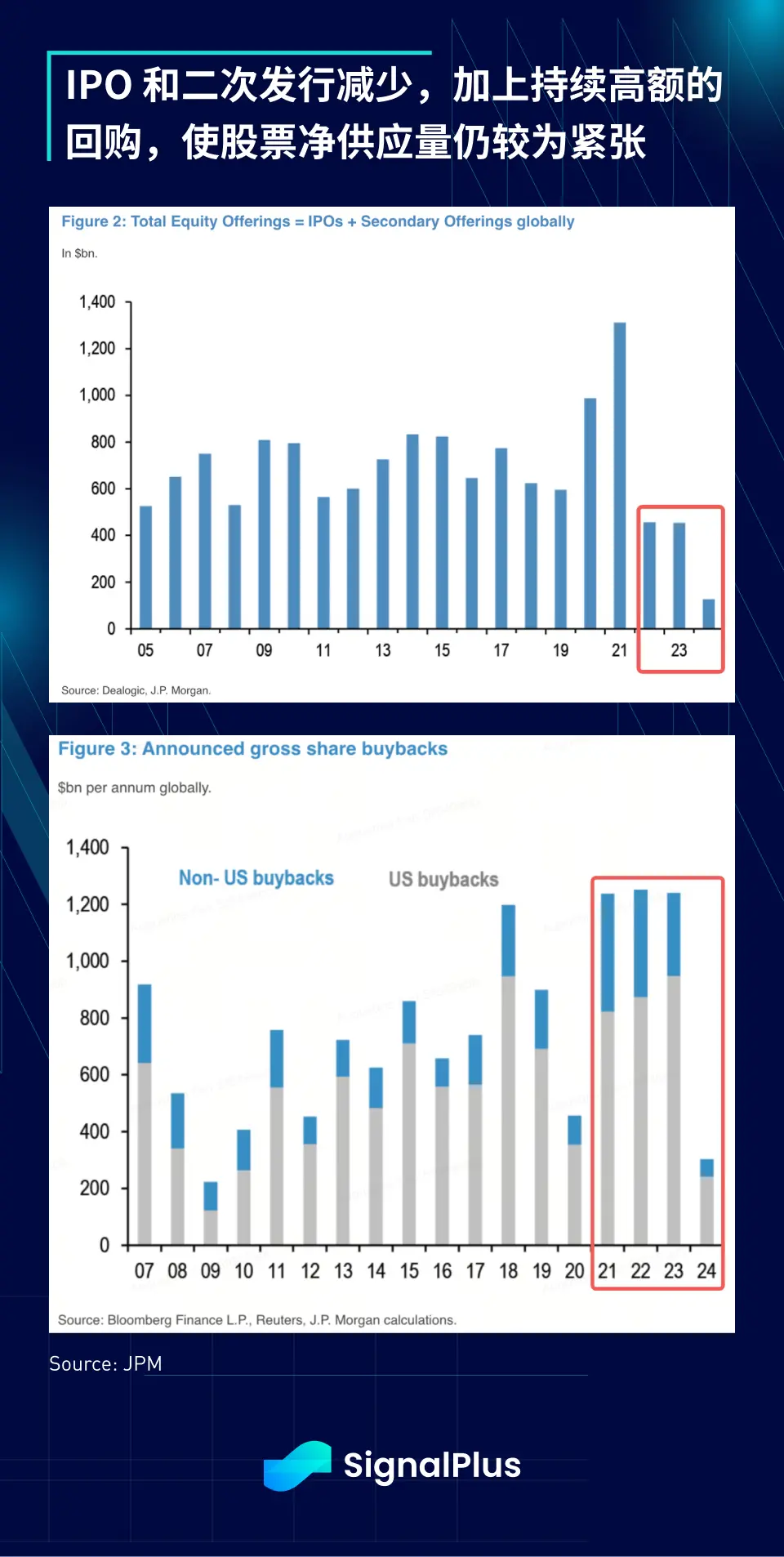

From a corporate fundamentals perspective, strong profit growth and historically high profit margins continue to support the stock market. Compared to the past few years, the net supply of stocks (secondary offerings + IPOs) continues to shrink, while corporate buybacks remain strong, with an estimated annual buyback amount of around $1.2 trillion in 2024, marking the fourth consecutive year. It seems that scarcity applies not only to BTC but also to high-quality stocks, which appear to be in short supply relative to the expanding fiat currency base.

After clearing leveraged long positions in the past week, cryptocurrency prices continue to rebound, nearing historical highs, with various altcoins taking turns showing good performance. Yesterday, ETF inflows were moderate at $64 million, with BlackRock's inflows roughly offsetting the outflows from GBTC. Finally, Bloomberg reports that venture capital deployed in cryptocurrencies rebounded in Q1 2024, which is a good sign, but still far from 2022 levels, even though BTC prices have recovered all losses during this period.