SignalPlus Macro Analysis (20240129): Strong Performance of US Economic Data

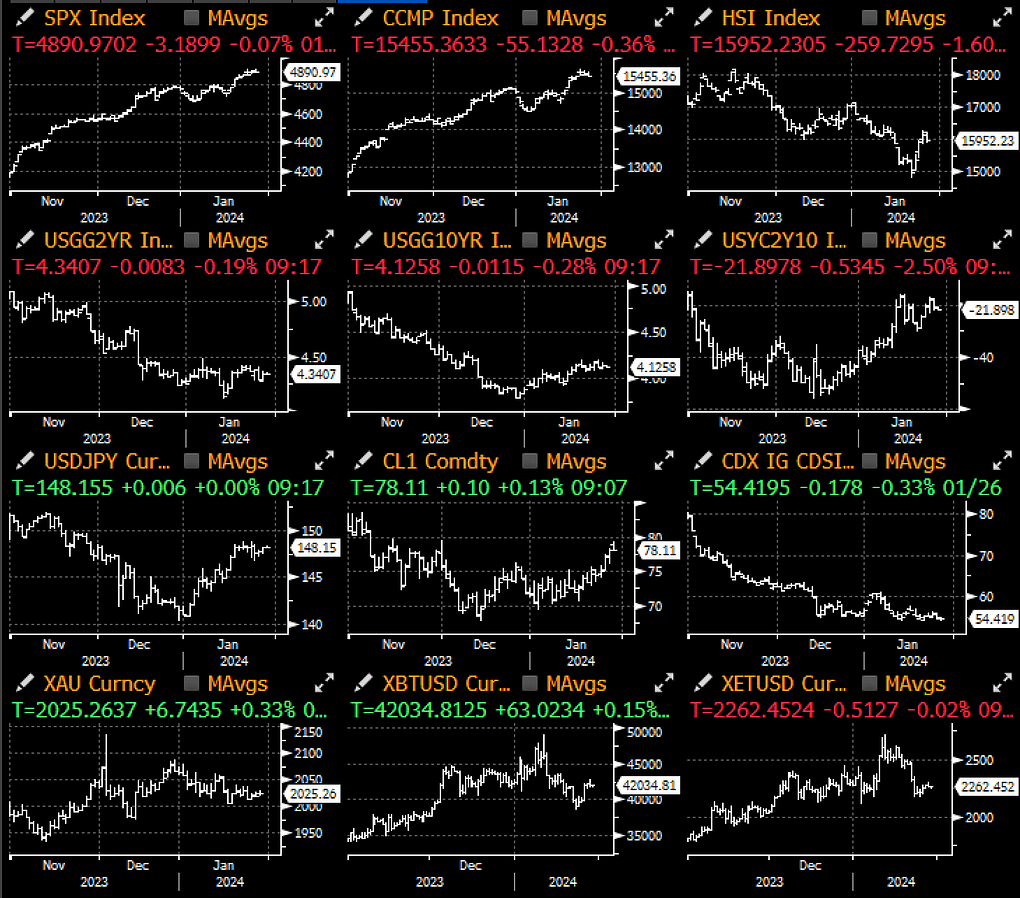

The market wrapped up last week with stronger U.S. economic data, with the overall core PCE in December increasing by 0.17%. However, core service prices excluding housing remained strong, rising by 0.28% month-on-month. There was not much progress in the cryptocurrency sector, as prices rose over the weekend due to some market short covering.

The market wrapped up last week with stronger U.S. economic data, with the overall core PCE in December increasing by 0.17%. However, core service prices excluding housing remained strong, rising by 0.28% month-on-month. There was not much progress in the cryptocurrency sector, as prices rose over the weekend due to some market short covering.

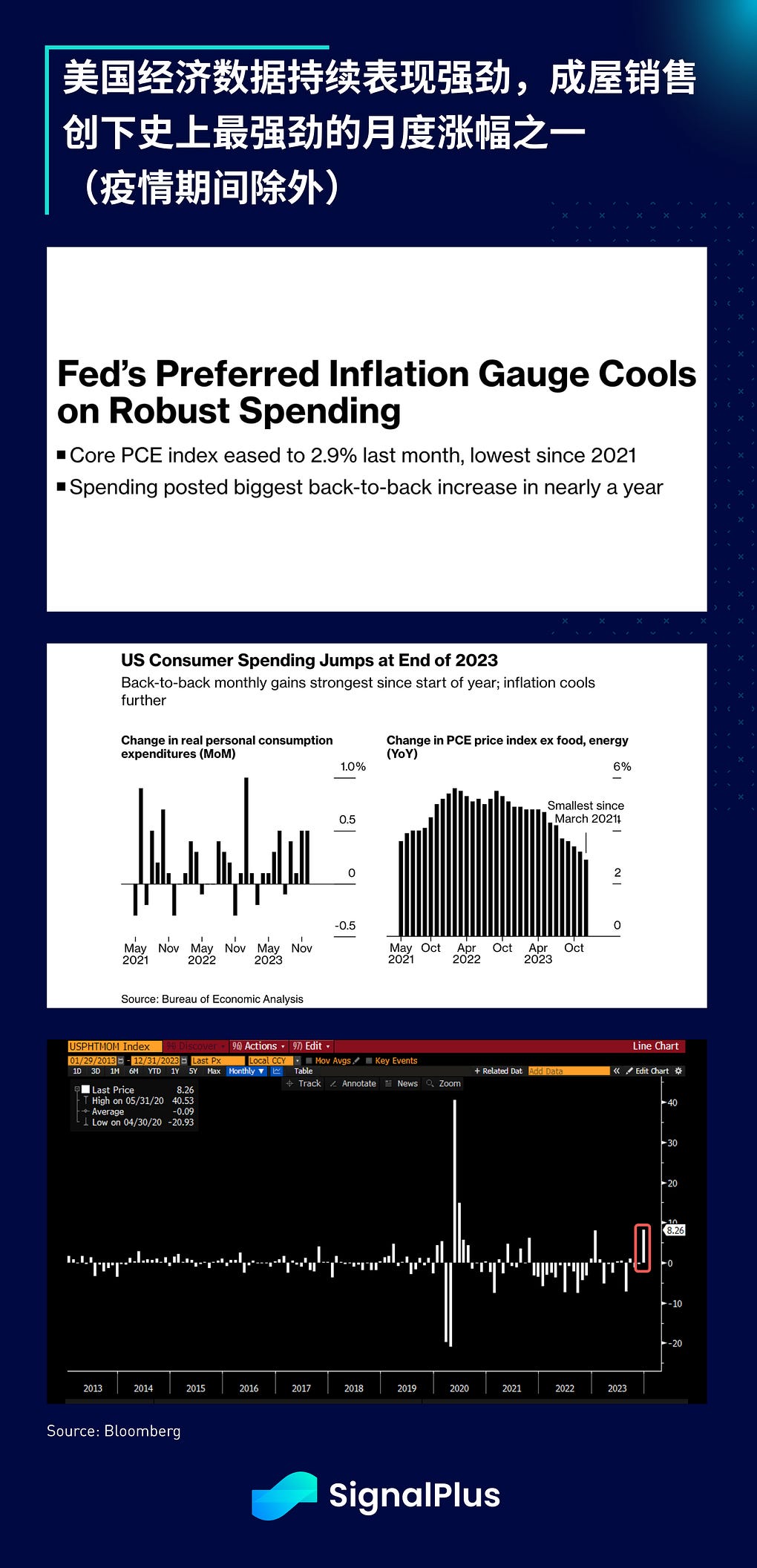

The market wrapped up last week with stronger U.S. economic data, with December's overall core PCE rising by 0.17% month-on-month. However, core service prices excluding housing remained strong, increasing by 0.28% month-on-month; personal income and consumption expenditures were in good shape, and existing home sales saw one of the largest monthly increases in the past decade (excluding the pandemic period) at +8.3%.

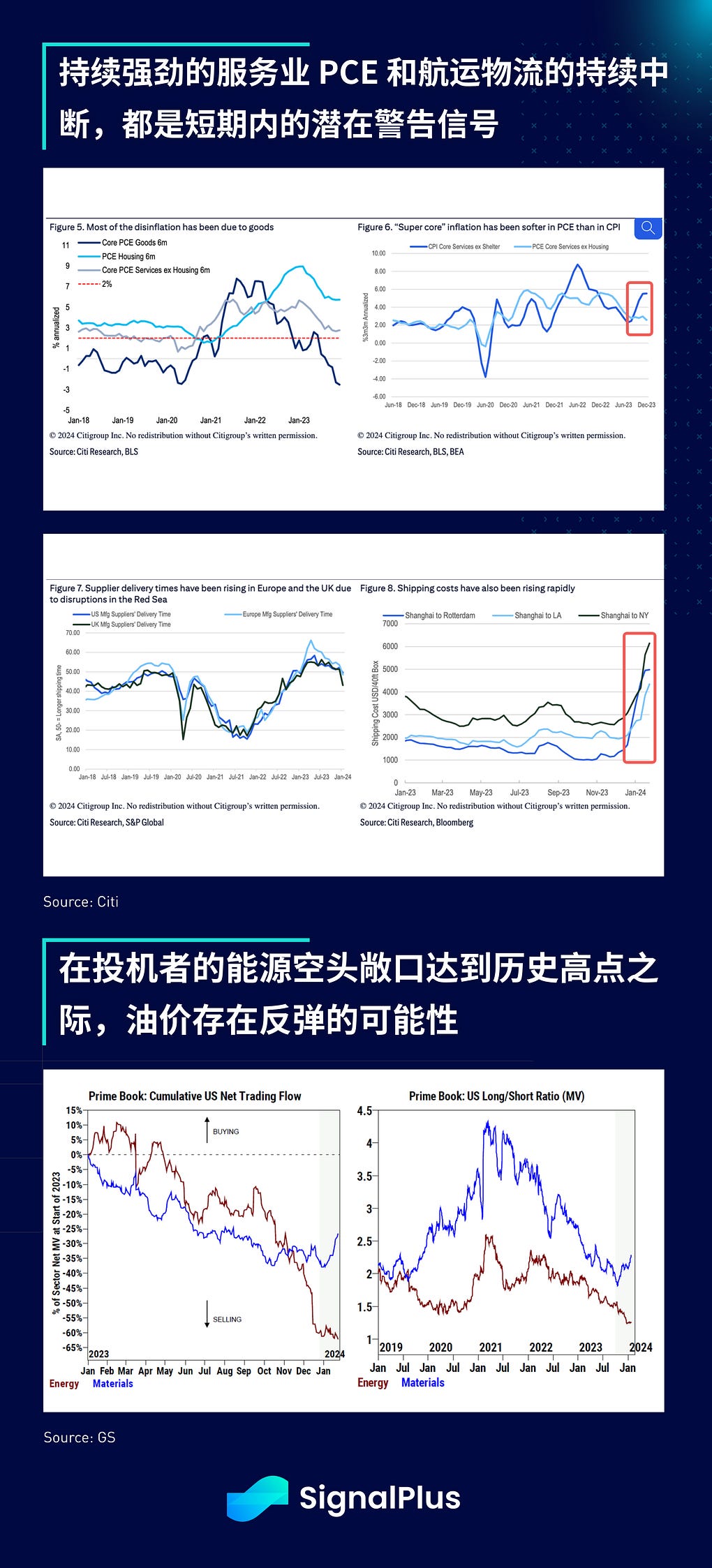

Concerns about rising service prices have intensified, coupled with record corporate bond issuance of $721 billion so far in January, which has largely satisfied investment demand, leading to poor performance in fixed income. Additionally, shipping and logistics continue to be affected, and with the escalation of conflicts in the Middle East (a U.S. military base in Jordan was attacked by drones), oil prices may have the opportunity to break $80 per barrel, potentially posing a threat to easing inflation.

This week will be the busiest macro week of the year so far. On Tuesday, consumer confidence survey results and JOLTS job openings will be released; Wednesday will bring the Bank of Japan's summary of opinions, China's PMI, Germany's CPI and unemployment rate, U.S. ADP, FOMC meeting, and quarterly refinancing announcements, followed by Thursday's Caixin manufacturing PMI, Bank of England's decision, and U.S. ISM manufacturing index. The busy week will conclude on Friday with U.S. non-farm payroll data and the University of Michigan consumer confidence survey.

The U.S. earnings season is also busy, with 32% of S&P 500 companies set to report earnings this week, including Alphabet, Microsoft, AMD, Apple, Amazon, and Meta.

This week will see a wealth of new information in three major areas: corporate earnings, monetary policy, and economic data. We believe that employment data may be the most critical, while the FOMC's decisions will cover the broadest range. In a market that has trended upward since the beginning of the year but still shows risk-averse sentiment, corporate earnings performance may have the greatest impact on the relative market trend. If the results in these areas are all positive, the market may rise further, eliminating reasons for investors to remain cautious.

Currently, the market predicts nearly a 50/50 chance of an FOMC rate cut in March, but this week's FOMC meeting itself may not bring significant surprises, as no economic forecasts will be released, and the market generally expects the Federal Reserve to continue its current tone to manage market expectations. Citigroup's report indicates that the implied volatility of the options straddles for January 31 is currently +/- 1%, lower than the actual volatility of +/- 1.3% on FOMC meeting days since 2022.

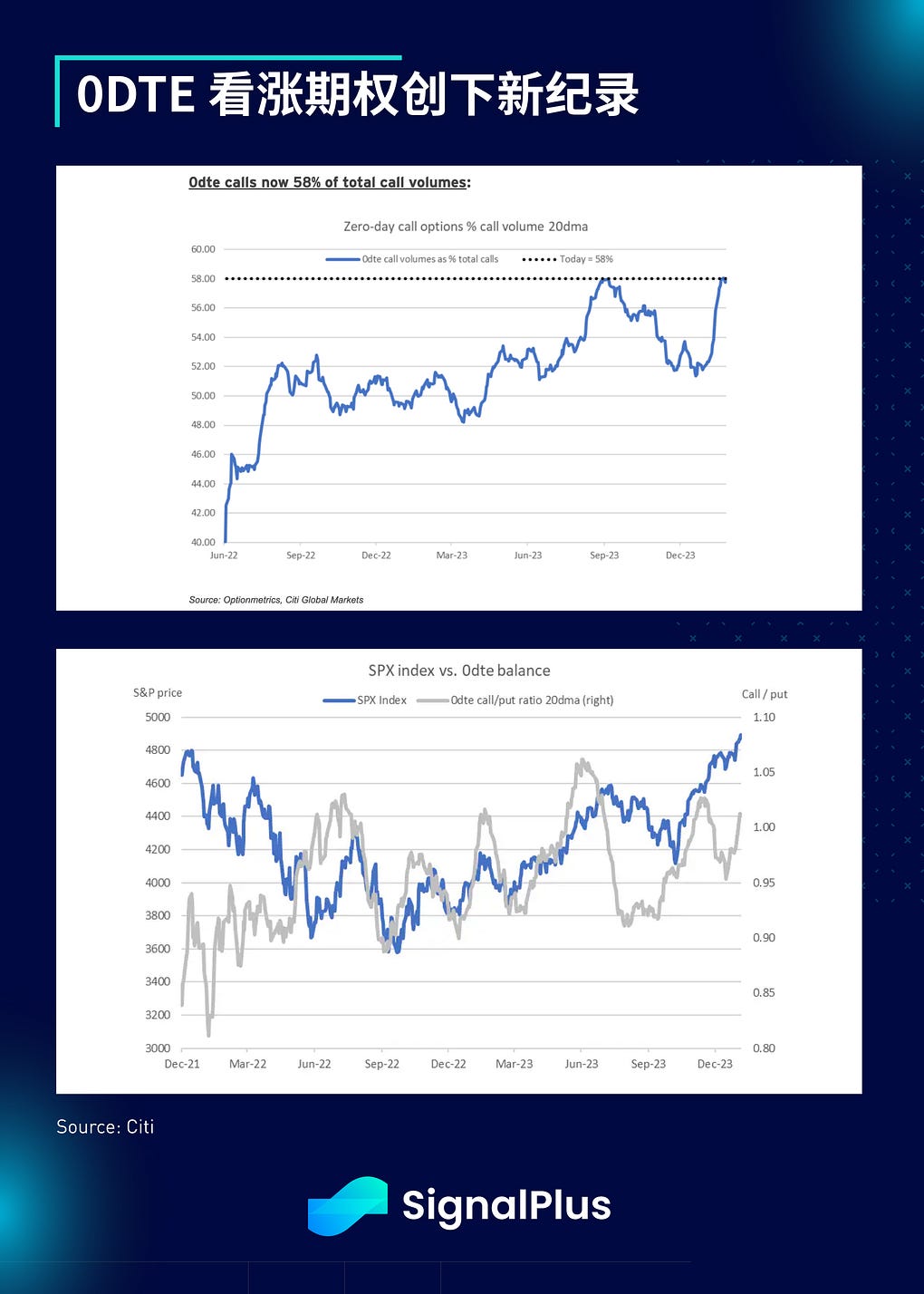

In terms of investor sentiment, options traders remain generally bullish, with 0DTE call options hitting a new record, over 58% of 0DTE trading volume being call options, pushing the call/put ratio back above 1.

There hasn't been much progress in the cryptocurrency space. Over the weekend, prices rose due to some market short covering, and reports indicated that Google would begin allowing certain BTC and cryptocurrency ads on its platform, although this policy change was announced back in December.

The fund flows for ETFs remain largely the same, with 9 ETFs still collectively responding to the outflows from GBTC. However, we are starting to see an increase in trading volume for Blackrock's IBIT, reaching $481 million, gradually approaching Greyscale's $649 million, and far exceeding its average trading volume in the first week. Will IBTC's trading volume have the chance to surpass GBTC before mid-February? Does this signal the arrival of the next bull market, at the cost of TradFi continuing to take over cryptocurrency? Let’s keep a close watch!