SignalPlus Macro Analysis Special Edition: Return-Free Risk

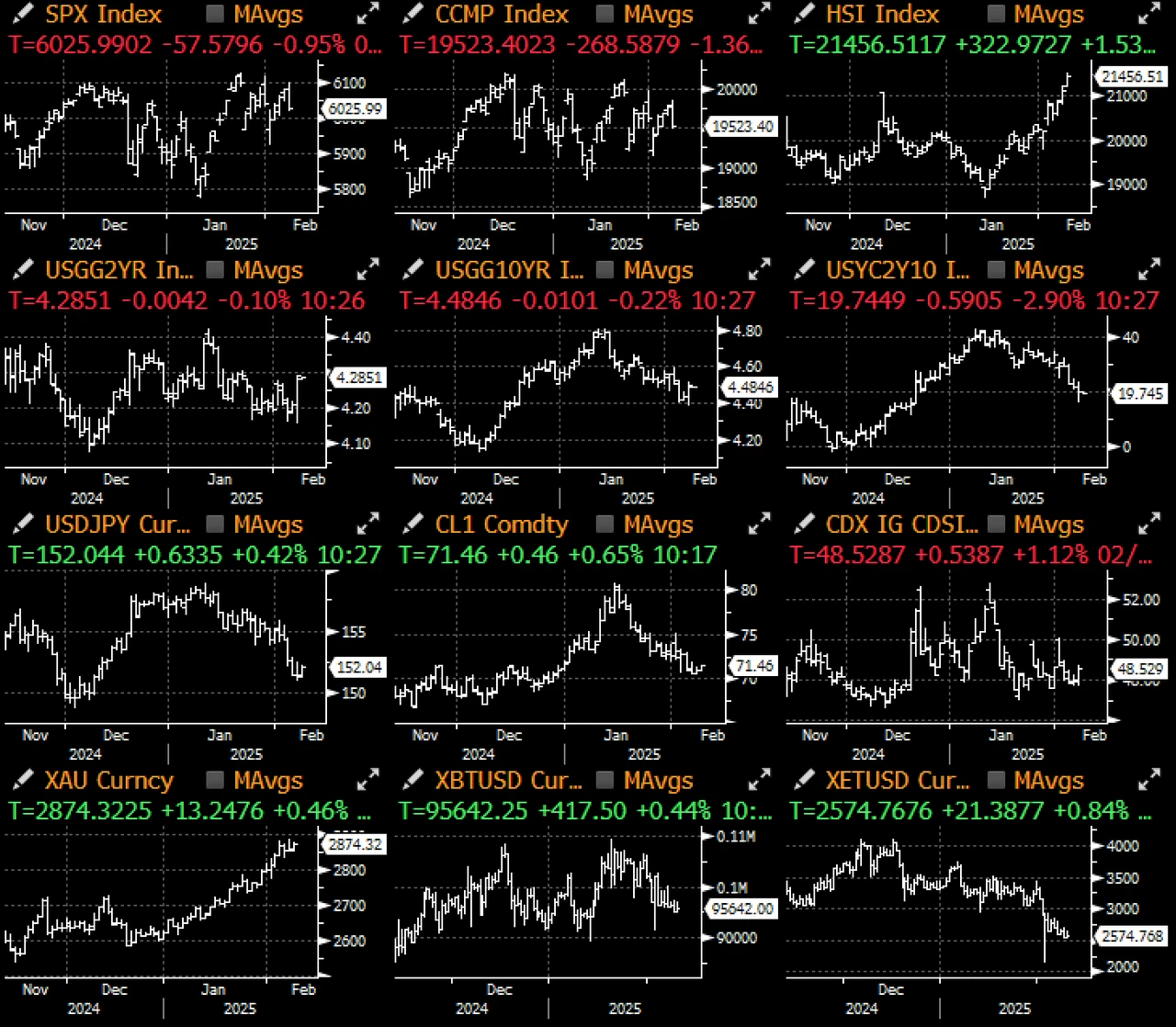

The market has opened 2025 with a series of unfavorable starts and unresolved price movements. Amid the shocking DeepSeek narrative and President Trump's occasional tariff threats, risk assets are struggling to find direction.

Economic data is currently secondary; January's non-farm payroll data came in slightly below expectations, but the unemployment rate also dropped to 4%, leading to a muted market reaction. Federal funds futures currently imply only a 9% chance of a rate cut at the March FOMC meeting, with a complete rate cut priced in only after five meetings in September, diminishing the Fed's influence in the current narrative.

On the other hand, the unpredictability of tariff policies continues, with Trump stating he will announce a 25% tariff on all steel and aluminum imports today (Monday) and immediately implement reciprocal tariffs. As the market prepares for a challenging opening in U.S. stocks, there was selling pressure on U.S. stocks on Friday evening.

Against the backdrop of tariff risks and ongoing global central bank purchases, gold prices are expected to rise to new highs this week. Since Trump took office, the People's Bank of China has increased its gold reserves for the third consecutive month. Notably, even as terminal rates rise and cryptocurrency momentum weakens, gold's upward trend continues, indicating that the structural change in demand is no longer purely influenced by central bank liquidity.

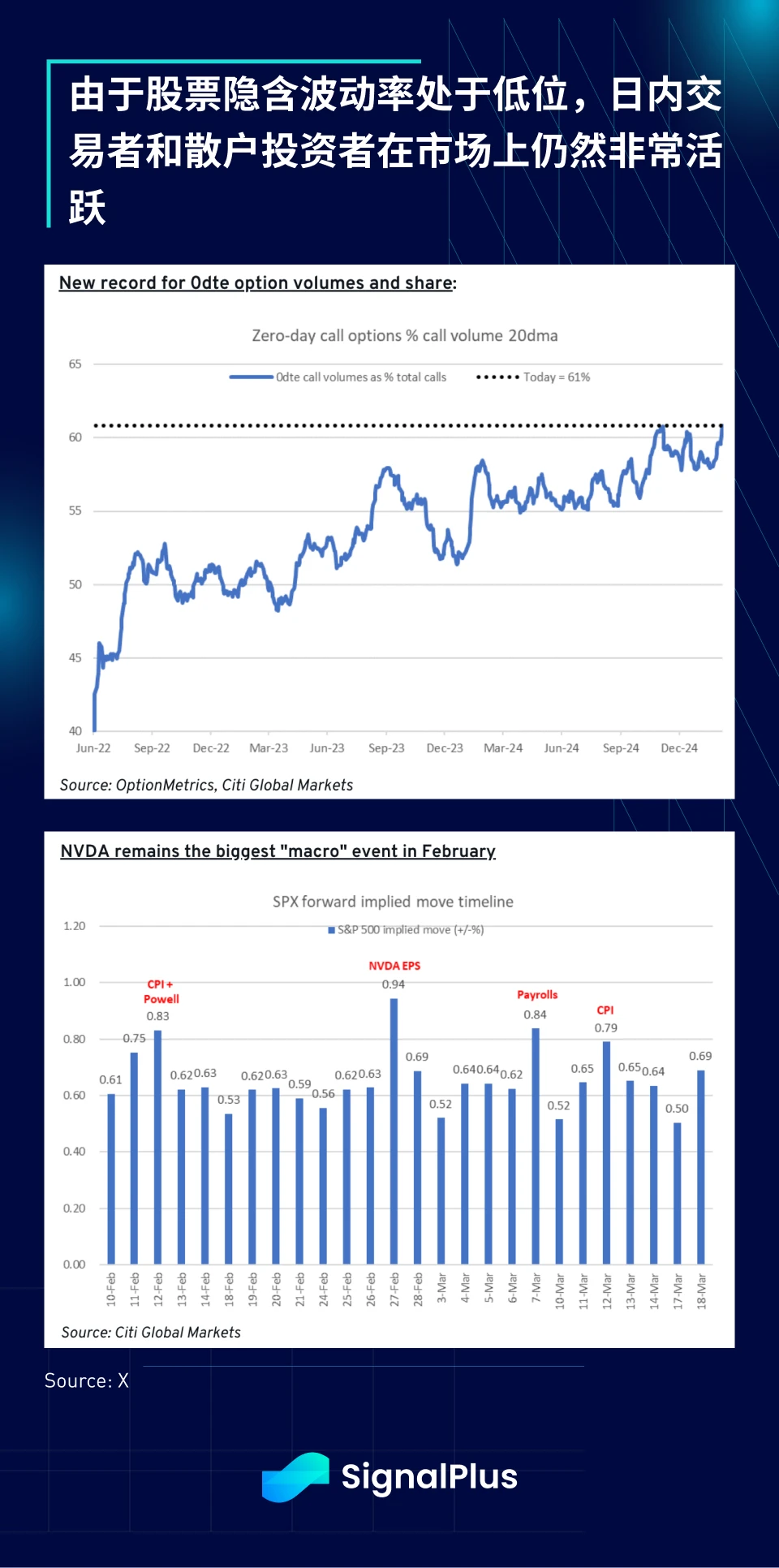

Despite the volatility at the start of the year, U.S. retail investors and day traders remain actively engaged in the stock market, with daily options trading volume rebounding to historic highs. Aside from events like CPI/Powell and Nvidia's earnings report, implied volatility in stocks remains low.

The extremely optimistic market sentiment seems close to triggering "sell" signals in various sell-side trading models. In fact, the earnings outlook for the SPX index shows a declining trend for both Q4 2024 and 2025 forecasts, and we maintain a cautious outlook on the recent stock market.

In the cryptocurrency space, price movements have been disappointing. While the market remains excited about developments such as BTC potentially being included as a reserve asset and mainstream institutional participation, major altcoins have dropped 15-20% since the beginning of the year. We previously expressed concerns about the issuance of the $TRUMP Memecoin and its potential negative impact on the cryptocurrency industry; so far, this concern has been validated, as trading volumes in cryptocurrencies have significantly declined since the new year, and recent large-scale liquidations have severely impacted trading account profits and losses.

BTC's strong performance relative to other assets is most evident compared to ETH, which is currently facing record short pressure and intense FUD sentiment. This second-largest token has dropped 23% since the beginning of the year, significantly lagging behind BTC's +2.5%. The lack of L1 catalysts and narrative dominance may continue to pressure Ethereum.

Worse still, analysts point out that over $30 billion in altcoin supply will be released over the next 12 months. These unlocked tokens will flow into a market with limited demand and significant wallet losses. However, the TradFi funds entering the market may only focus on BTC or the top three tokens, unlikely to spill over into the altcoin market. This weak market state is also reflected in the performance of newly listed tokens, even on Binance. This time, it seems genuinely different for the current cycle moving towards maturity.

Finally, let's talk about something lighter. After the issuance of $TRUMP, will more countries issue their own memecoins to raise budget funds? I sincerely hope this is just a joke and not a phenomenon that will be normalized in the coming year!