BTC Volatility: A Weekly Review from August 12 to August 19, 2024

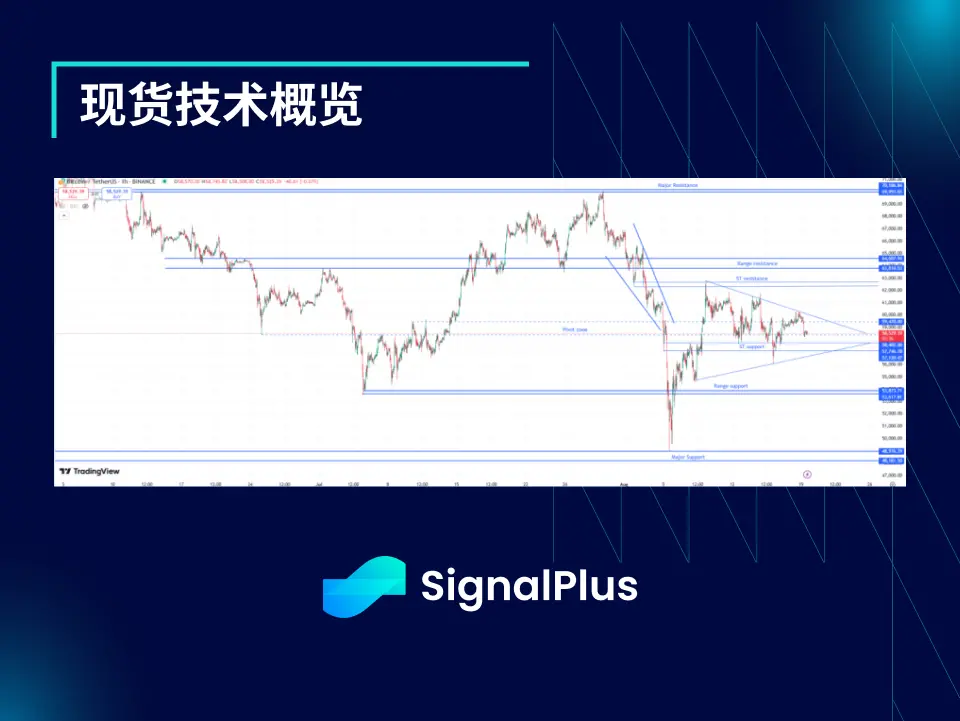

Overall, the global risk market performed well, with BTC prices fluctuating within a very narrow range. Although BTC's volatility is low, we still observe that high-frequency volatility remains elevated, as the market repeatedly oscillates in the key range of 58.5k-59.5k, struggling to stabilize at a balanced level...

Overall, the global risk market performed well, with BTC prices fluctuating within a very narrow range. Although BTC's volatility is low, we still observe that high-frequency volatility remains elevated, as the market repeatedly oscillates in the key range of 58.5k-59.5k, struggling to stabilize at a balanced level...

Key Indicators (Hong Kong Time August 12, 4 PM -> August 20, 4 PM):

BTC/USD + 0.2% ($58,500 -> $58,600), ETH/USD + 2.75% ($2,550 -> $2,620)

BTC/USD December (Year-End) ATM Volatility + 0.7% (61.5 -> 62.2), December 25 d Risk Reversal Volatility + 0.5% (3.6 -> 4.1)

Overall, global risk markets performed well, with BTC prices fluctuating within a very narrow range. Despite the low volatility of BTC, we still observed high-frequency volatility remaining elevated, as the market repeatedly oscillated in the key range of 58.5k-59.5k, struggling to stabilize at a balanced level.

BTC is expected to maintain a price range of 54k to 64k in the short term.

The market seems to be forming a gradually tightening wedge/triangle pattern, indicating that we may see a turning point before the weekend. However, if the price fails to break through this range, we expect actual volatility to struggle to rise significantly.

Major Market Events:

Last week, traditional financial markets rebounded strongly, but interestingly, the cryptocurrency market lagged significantly. This reminds one of the trend in U.S. Treasury yields (which rebounded from lows but did not show significant volatility thereafter).

The focus this weekend is on Powell's speech at the Jackson Hole meeting. The market expects at least one rate cut (with a possibility of a 50 basis point cut).

Geopolitical conditions were relatively calm last week, and as the U.S. Labor Day holiday approaches, the market is beginning to exhibit more of a summer atmosphere.

ATM Implied Volatility:

Despite high-frequency realized volatility being high, front-end volatility continued to decline throughout the week, mainly due to the narrowing of the volatility range (i.e., terminal distribution). However, at the beginning of the week, Vega saw decent buying interest, which made the volatility curve steeper.

With increasing market attention on the elections, there has been more demand for election day put spreads. Overall, the weight of election impacts reflected in pricing seems quite reasonable.

If the spot range remains stable, volatility in August is expected to narrow further, making September steeper.

Skew/Convexity:

This week, convexity and skew remained flat; due to the decline in ATM volatility, the front-end butterfly spreads saw a slight increase.

The spot-volatility correlation remains negatively correlated within a limited range, but has weakened compared to last week. Below the 55-56k price level, Gamma demand is expected, while at the 61-62k price level, volatility is expected to remain weak.

Wishing you successful trading this week!