SignalPlus Macro Research Special Edition: Crossing the Rubicon

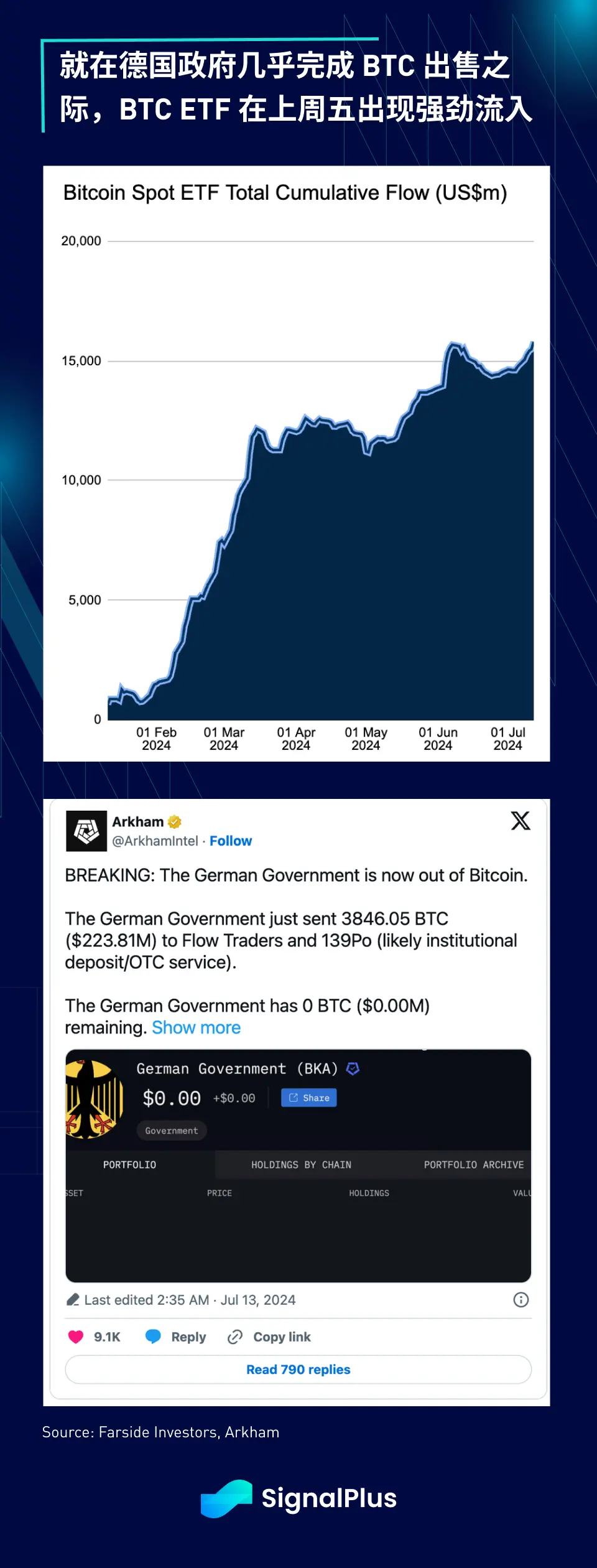

The assassination incident that occurred during former President Trump's speech in Pennsylvania undoubtedly became the weekend's news highlight. Last Friday, there was a significant inflow into BTC spot ETFs, totaling $310 million, the largest inflow since June 5.

The assassination incident that occurred during former President Trump's speech in Pennsylvania undoubtedly became the weekend's news highlight. Last Friday, there was a significant inflow into BTC spot ETFs, totaling $310 million, the largest inflow since June 5.

The assassination attempt that occurred during former President Trump's speech in Pennsylvania undoubtedly became the weekend's news focus. Following the failed assassination, the former president's chances of winning have further surged to around 70%.

Although the United States may be an increasingly polarized and divided country, it stands united on issues of homeland security and attacks on political figures. The 1981 assassination attempt on former President Reagan likely contributed to his subsequent overwhelming victory in the election, and with only a few months left until the November vote, a similar situation may repeat itself. It now seems that the election outcome largely depends on whether Trump can maintain his current advantage, and the liberal media and opposition will have to temper their harsh criticisms in the upcoming campaign.

The macro market may trade with Trump's victory as a baseline scenario, which would have significant implications for all asset classes. While we are not political experts, we believe that a second term for Trump could lead to tougher policies.

Currently, Republicans and Trump's supporters believe:

The opposition is attempting a political witch hunt, sentencing a former president to 700 years in prison.

The recent push for voting rights for non-citizens may allow Trump's opponents to gain a large number of immigrant votes.

The assassination attempt occurring in broad daylight indicates serious security lapses.

If Trump is re-elected, the market may anticipate:

Radical fiscal spending and extravagant tax policies.

Further escalation of tensions between the U.S. and China.

Increased pressure on Europe to pay over $200 billion in NATO protection fees, especially considering the ongoing Russia-Ukraine conflict.

A crackdown on illegal immigration.

A similar shift to a conservative Supreme Court as seen during his first term, with a radical "cleansing" of key civil servants, government employees, and others in the Washington ecosystem.

Radical spending plans will further worsen the already severe bond supply and budget deficit situation, and bond yields are likely to experience a bear steepening trend. During Trump's first term, the 10-year yield rose by about 200 basis points within 18 months.

As Trump potentially gains a second term, both U.S. economic growth and inflation are slowing. Last week's CPI data fell to its lowest level since 2021 due to a slowdown in housing costs, with core CPI rising just 0.1% since May, the slowest growth in three years, and the overall index showing a decline for the first time since the pandemic.

The market clearly views last Thursday's CPI as a watershed moment in the current cycle, with the probability of a rate cut in September now as high as 95%. We can imagine that the Trump administration will certainly pressure the Federal Reserve to implement more aggressive rate easing policies in 2025 as a means of stimulating the economy.

Speaking of economic slowdown, the earnings reports from major U.S. banks confirm a general deterioration in consumer conditions. Most banks have set aside more cash to cope with customer loan defaults, as consumers deplete their savings accumulated during the pandemic, leading to increased loan write-offs at Citigroup, Wells Fargo, and JPMorgan Chase. The credit card delinquency rate at small banks has risen to its highest level in 30 years, and the overall credit card delinquency rate in the banking industry has also reached its highest level in a decade.

Last Friday's University of Michigan Consumer Sentiment Index also fell below expectations for the fourth consecutive month, with respondents indicating that a weak job market combined with high prices is dampening overall confidence. The official survey report noted, "Nearly half of consumers spontaneously complained that high prices are eroding their living standards, approaching the record high set two years ago."

Outside the United States, last week's economic data also confirmed the sluggish recovery of the Chinese economy, with CPI rising only 0.2%, below the expected 0.4%. Loan and credit growth in June hit historic lows, with weak end-user demand, and new RMB loans, social financing scale, and import data (year-on-year -2.3%, below the expected +2.5%) also remained bleak. As the third plenary session in July approaches, the Chinese government is undoubtedly disappointed with the pace of recovery.

Back to the U.S. stock market, the SPX index continues to hover near historical highs, with bears capitulating. JPMorgan estimates that long positions in stock futures have returned to their highest level in the past decade (as a percentage of open interest), while cash allocation has fallen to its lowest level since 2000. However, despite rising stock prices, global new stock supply has remained negative for the third consecutive year, and the IPO market remains closed for most issuers.

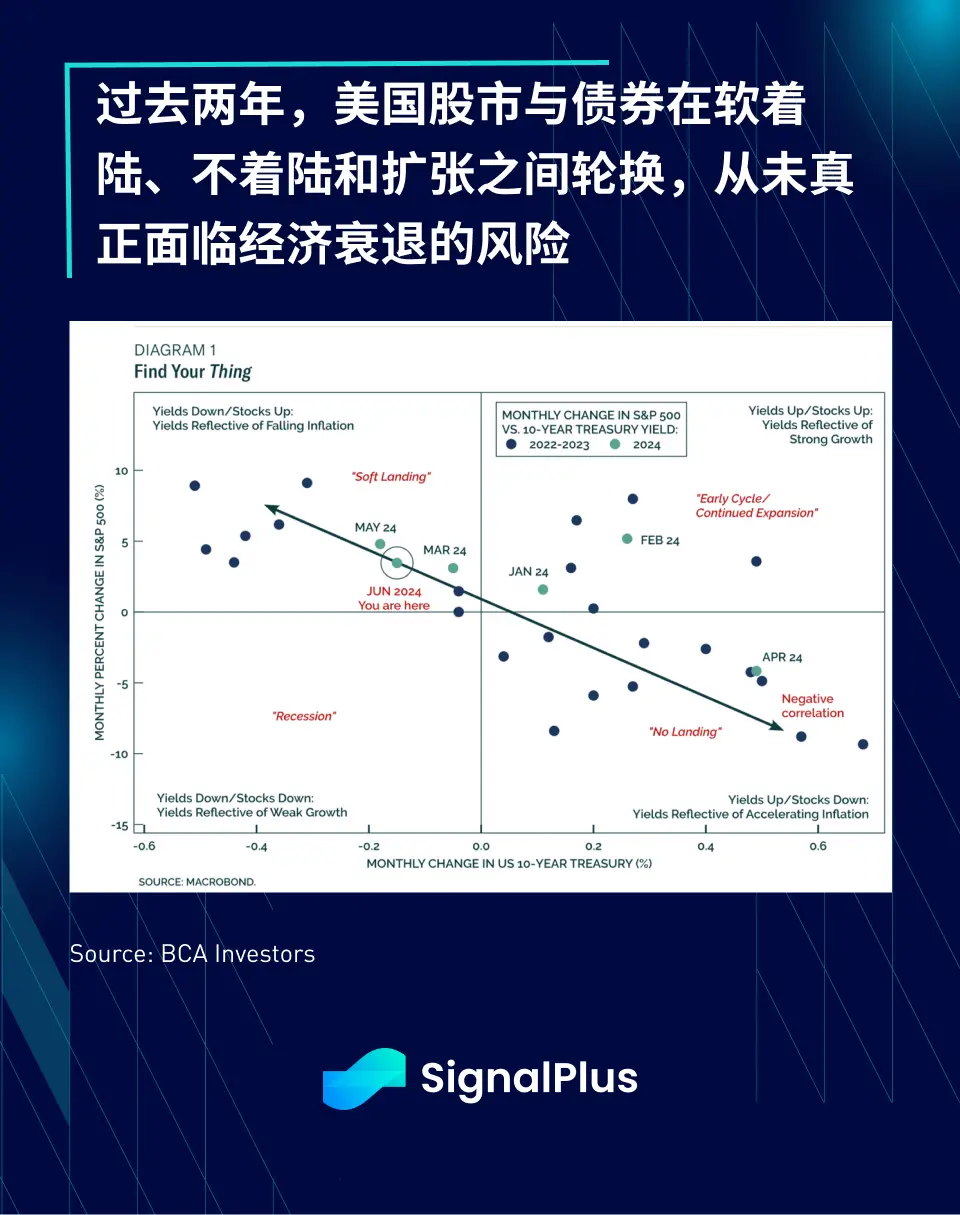

Interestingly, macro bears may be surprised to find that the correlation between bonds and stocks (yields do not always move in the same direction as stock prices) indicates that the risk of the U.S. economy falling into recession has never been present in the past two years. This correlation oscillates between expansion expectations that occasionally arise during soft landings, no landings, and strong data bursts. This reminds us that while macro assets are highly forward-looking and self-correcting, it is often the interactions between assets that tell the complete story, rather than the absolute level of a single variable (such as yield curve inversion). Watch closely for when yields begin to fall alongside stock prices; that will be the first true sign that the market finally believes we are heading into a slowdown phase.

In terms of cryptocurrency, prices have clearly benefited from the rising probability of Trump's victory, with BTC rebounding to around $62,500, recovering more than 10% after the last wave of sell-off. The Bitcoin Conference has confirmed that Trump will still attend the event in Nashville at the end of July, as his campaign statement claims he will continue to support cryptocurrency.

In terms of capital flows, last Friday saw a significant inflow into BTC spot ETFs, totaling $310 million, the largest inflow since June 5. According to Arkham's data, investors believe the German government has sold all BTC and returned to a buy-the-dip mode. Nevertheless, the market still needs to deal with the repayment issues from Mt. Gox, with approximately 140,000 BTC (worth $8.5 billion) expected to hit the market. However, there is always light at the end of the tunnel; the upcoming rate cut in September and the potential for Trump's victory are expected to provide further support for cryptocurrency.

In terms of price trends, it is reassuring that BTC successfully held the $50,000 area during the recent sell-off, which is the breakout area since BTC was approved in January. Market sentiment may shift towards selling put options/buying on dips.

Wishing everyone successful trading!

You can search for SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time cryptocurrency information. If you want to receive our updates instantly, feel free to follow our Twitter account @SignalPlus_Web3, or join our WeChat group (add the assistant's WeChat: SignalPlus 123), Telegram group, and Discord community to interact and communicate with more friends. SignalPlus Official Website: https://www.signalplus.com