SignalPlus Macro Analysis (20240510): Market data is generally favorable for risk assets

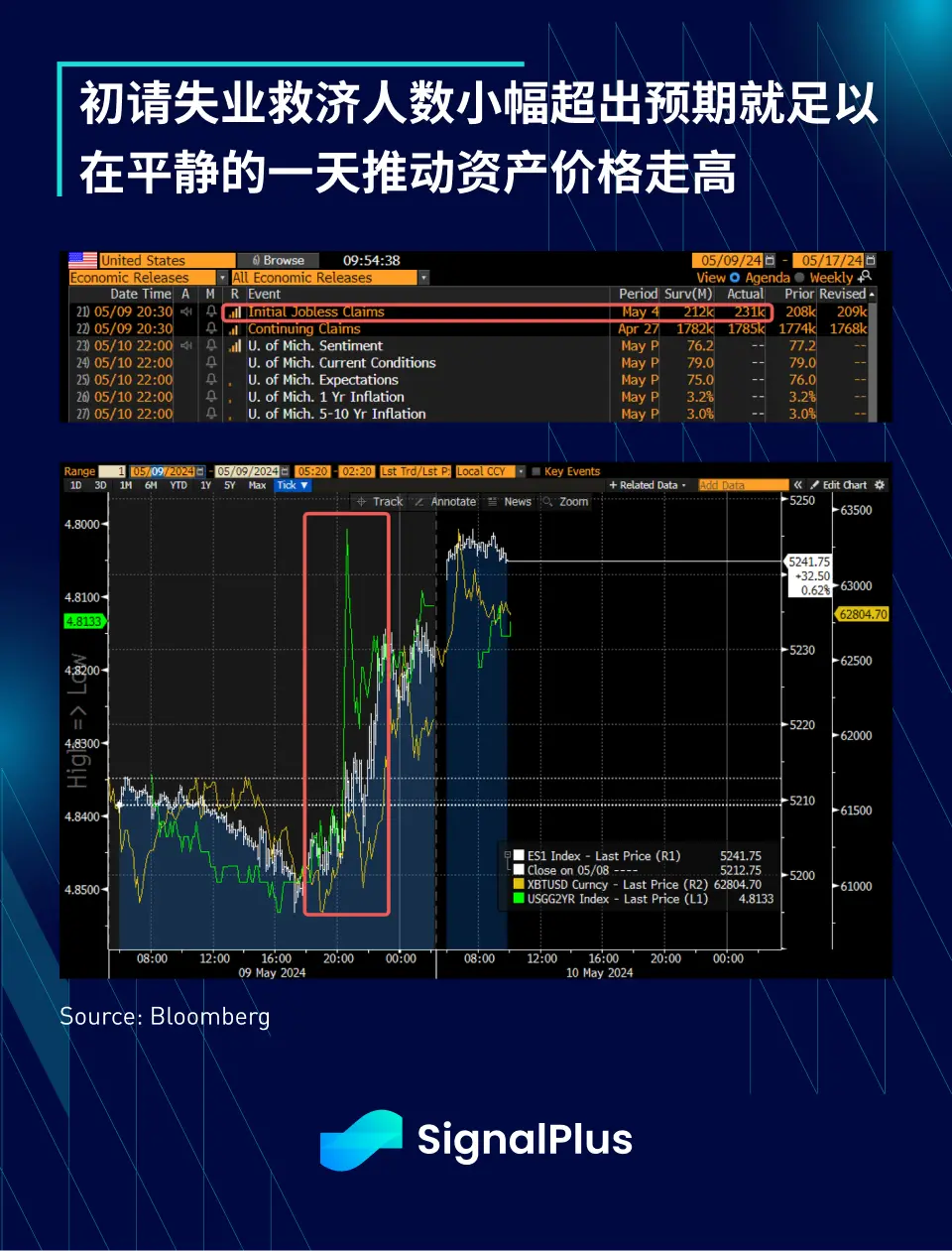

This week, there was obviously nothing significant happening, just a slight increase in the number of initial unemployment claims exceeding expectations (231,000 vs 212,000) was enough to drive all major asset classes higher.

This week, there was obviously nothing significant happening, just a slight increase in the number of initial unemployment claims exceeding expectations (231,000 vs 212,000) was enough to drive all major asset classes higher.

This week, there were obviously no major events, and the slight increase in the number of initial unemployment claims (231,000 vs. 212,000) was enough to drive all major asset classes higher. Given that the Federal Reserve has recently shifted its focus to the weakness in the labor market, the market undoubtedly places significant importance on this information and is actively seeking all signs of a slowdown in the job market to reignite hopes for interest rate cuts. As previously mentioned, the current asymmetric risk-return setup (the Fed ignoring high inflation while looking for signs of labor market slowdown) should generally favor risk assets, so after the unemployment claims data was released, stock prices, bond prices, and even BTC all rose in tandem.

A deeper analysis of the recent employment data shows that while the non-farm payrolls increased by 175,000, which is still relatively healthy, and the unemployment rate of 3.9% remains low, some alternative labor market indicators are starting to show cracks. Powell himself specifically mentioned the decline in hiring rates and the weakness in employment surveys during the Q&A as signs of weakening labor demand. Additionally, other sub-indicators, such as the increase in permanent unemployment rates, the decline in turnover rates, the reduction in hiring plans, and the widening "hard to find work" ratio, all suggest that the U.S. economy may experience a more pronounced slowdown in the job market in the second half of the year, while the excess savings accumulated during the pandemic have already been depleted.

Next week, CPI data will be released, and the market should become active again, challenging the recent ideal outlook. Wishing everyone a pleasant weekend!