Coinbase: Is the strong momentum in the crypto market sustainable?

Recent performance is consistent with the constructive outlook we released in early February, but we remain cautious about some negative seasonal factors that may still arise in March.

Recent performance is consistent with the constructive outlook we released in early February, but we remain cautious about some negative seasonal factors that may still arise in March.Written by: David Han, David Duong

Compiled by: DAOSquare

Key Highlights

- The rebound in the crypto market this week was supported by significant capital inflows into U.S. spot Bitcoin ETFs and a short squeeze in leveraged derivative positions. Open interest reached its highest level since January 2022, and funding rates soared to their highest since April 2021 (annualized at 109%).

- The proposal put forward by the Uniswap Foundation on February 23 laid the technical groundwork for implementing a fee mechanism to pay UNI stakers and delegators (participants in governance) in wETH.

- We believe that discussions around blockchain adoption will shift from scalability to how to create a smooth user experience, which not only means abstracting the underlying blockchain but also addressing pain points related to mnemonic phrases, wallet management, and more.

Market Observation

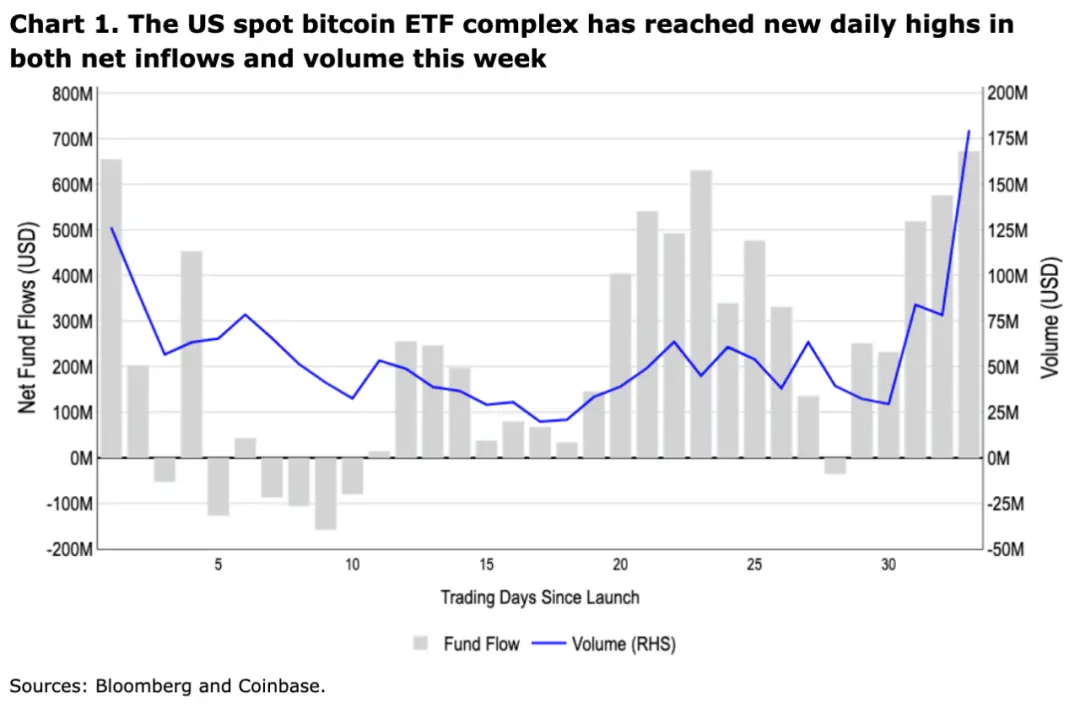

This week’s impressive rebound in the crypto market was supported by significant capital inflows into U.S. spot Bitcoin ETFs and a combination of short squeezes in leveraged derivative positions. The spot Bitcoin ETF saw nearly $1.8 billion in astonishing net inflows in the first three days of the week, with BlackRock's iShares Bitcoin ETF (IBIT) accounting for 70% of that (see Chart 1). Although many large brokerage firms, such as Morgan Stanley, are still conducting due diligence on these products (a prerequisite for offering them to clients), the performance this week is undoubtedly encouraging.

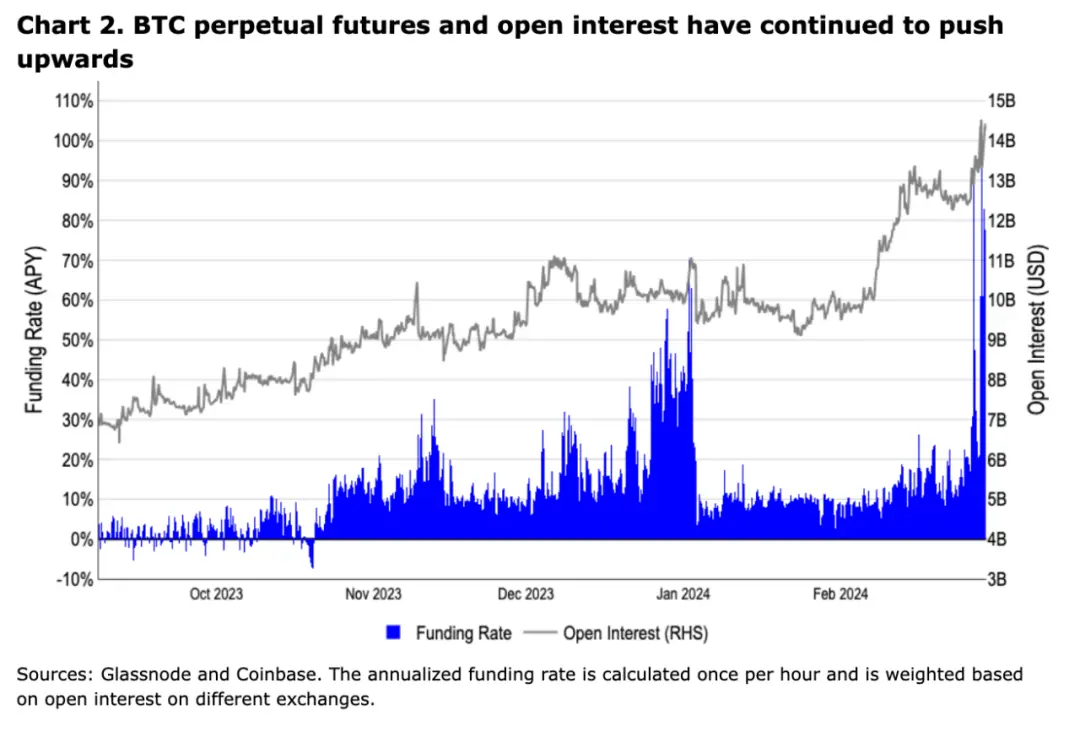

In recent days, the momentum in Bitcoin prices has driven a short squeeze, with open interest in BTC perpetual futures reaching its highest level since January 2022 ($14.2 billion). According to data from Glassnode, on February 28, the annualized funding rate for open interest reached 109%, the highest since April 2021. Subsequently, this rate dropped to around 70% (see Chart 2). Between February 25 and 28, nearly $750 million in shorts were liquidated, setting a new high for the number of shorts liquidated year-to-date. Meanwhile, we believe that the short covering based on the futures long-short ratio may be nearing its end, but it is not yet fully completed.

The recent performance aligns with our constructive outlook published in early February, but we remain cautious about some negative seasonal factors that may arise in March. For example, traditional assets are often influenced by tax-related drivers, which could lead to some temporary downward pressure. If the funding rates and liquidation of open interest lead to a series of long liquidations, then significant and sustained positive fluctuations in funding rates and open interest could also impact the market. Nevertheless, we maintain a generally constructive outlook for the coming months, as many wealth management firms will continue to incorporate spot ETFs, and such net inflows are clearly absorbing liquidity circulation faster than Bitcoin miners can produce.

On-chain: Uniswap Fee Switch

On February 23, the Uniswap Foundation (UF) announced a proposal to upgrade the governance of the Uniswap V3 protocol to allocate part of the trading fee rewards to UNI token delegators and stakers. However, it is important to note that the proposal itself does not initiate the fee switch but rather sets the technical mechanism for how to implement the fee switch. If the proposal passes, the initial fee parameters will be set to 0, but in future proposals, 10% to 20% of trading fees could be allocated to the reward program.

In our view, the biggest concern regarding enabling protocol fees is the impact on liquidity providers, as any such fees would be deducted from their earnings. This could lead to a decrease in total locked value (TVL) and MEV-based traffic. A detailed analysis by Gauntlet (involved with UF) addresses this issue and indicates that the impact on core non-MEV metrics may be minimal, with annual revenue estimates ranging from a conservative $10 million to an optimistic $72 million based on historical activity. If the initial proposal passes, the Gauntlet team will also be responsible for proposing the fee rollout plan.

We believe that, given the proposal has been put forward by UF's governance lead and has received broad support in the forum, it is likely to be implemented. In fact, in a previously rejected fee proposal in June 2023, most participants expressed support, but voting discrepancies between different fee levels ultimately led to a majority for "no fees." Since this proposal does not change any revenue structure, we do not foresee any significant obstacles. Interestingly, the proposal also links revenue to governance (through staking and delegation), which we believe can incentivize UNI holders to engage more actively in the community. The voting period for this proposal is expected to take place between March 1 and 7.

The widespread attention to this proposal has also prompted several other projects to consider following suit, such as Frax. If this trend develops in other mature DeFi protocols, we believe it could begin to bring previously speculative token valuations into a clearer and more fundamentally supported valuation model, especially for tokens and protocols that can generate sustainable fees. At the same time, this shift also represents a change in the accounting mechanism for protocol value, as it directly rewards agents and stakers with wETH (the currently proposed payment token), contrasting with other protocols like MakerDAO that adopt mechanisms of native token buybacks and burns.

On-chain: Surge of Application Chains

Additionally, we would like to discuss the growing rollup space on Ethereum, which has given rise to a new class of Rollup-as-a-Service (RaaS) products that allow for the simple creation and deployment of rollups with just a click. The development of modular blockchains has accelerated with the emergence of various technologies and is being used to deploy Layer 2 (L2) and other application-specific chains. The aforementioned Frax protocol plans to launch its own L2 called Fraxtal, which will make it part of the Optimism superchain. Other major protocols, such as the decentralized perpetual contract exchange GMX, which is currently the top TVL protocol on Arbitrum, are also considering deploying their own chains (it is currently known that the GMX protocol will remain on Arbitrum and Avalanche C-Chain).

As more L2s emerge, we believe there will be increased scrutiny in the cross-chain bridge and interoperability space, and the overall complexity of the ecosystem will also rise, with different solutions having their own considerations regarding security assumptions, confirmation times, development timelines, and costs, which may pose certain barriers for non-technical end-users. Additionally, the fixed costs of rollups (gas costs for Layer 1 infrastructure) are also a factor to consider. In a world of surging L2s, profitability may become increasingly difficult, likely pushing applications further toward Layer 3, which will lead to a reshuffling of profitable L2 chains. This fragmentation of execution environments has led some critics to argue that the shared state provided by a single or integrated blockchain can achieve more use cases and better cross-application security.

Discussions around these two scalability approaches, whether in favor or against, have shown profound implications, although we believe that these technical trade-offs are actually secondary to building a smooth user experience. In our view, the widespread adoption of any application ultimately requires abstracting the technical complexity from consumers, just as the underlying technology stack (and design trade-offs) of large web2 platforms is largely irrelevant to users. In light of this, we believe that enabling users to use passkey-protected wallets (such as Coinbase's wallet solution) is more crucial for expanding the crypto market. Although these tools are often overlooked in scalability debates, we believe these innovations could ultimately have a significant impact on user adoption and onboarding, especially if scalability solutions tend to converge on similar performance in the long run.

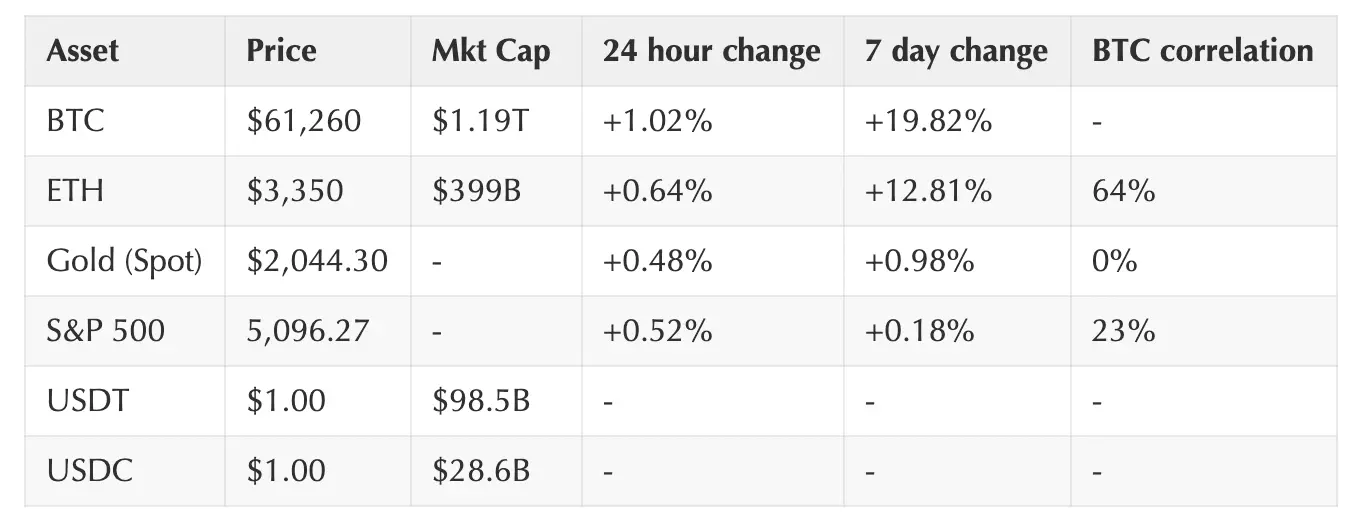

Crypto and Traditional Sector Performance

(As of 4 PM EST on February 29)

Coinbase Exchange and CES Insights

The rebound in BTC continues to surprise many market participants with its strong momentum. Long holders have benefited from this momentum, as over $2 billion in new funds flowed into ETF products over the past week. Nevertheless, high funding rates and the increase in open interest in perpetual futures products may pose risks to the rebound. Over the past 7 days, the average funding rate exceeded 30%, making the cost of holding long positions quite high. Altcoin liquidity has shown a closer correlation with investor trading behavior around sectors and narratives.

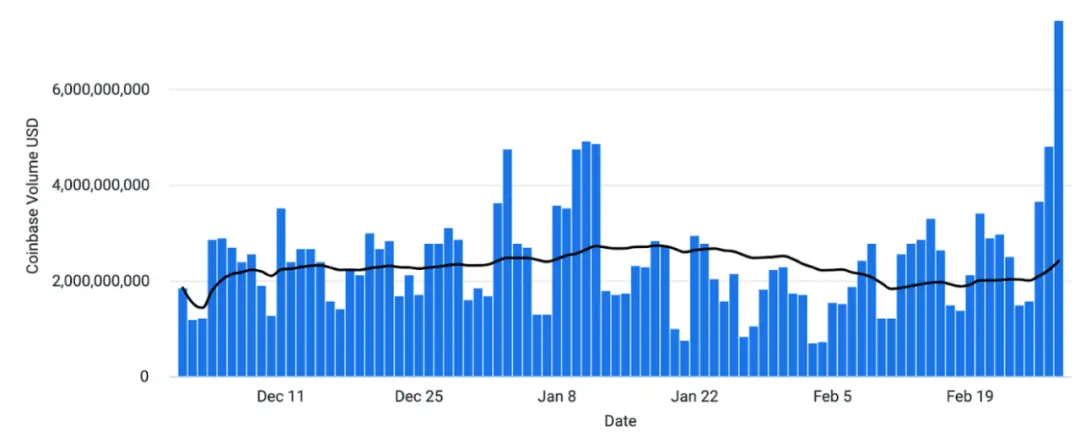

Coinbase Platform Trading Volume (USD)

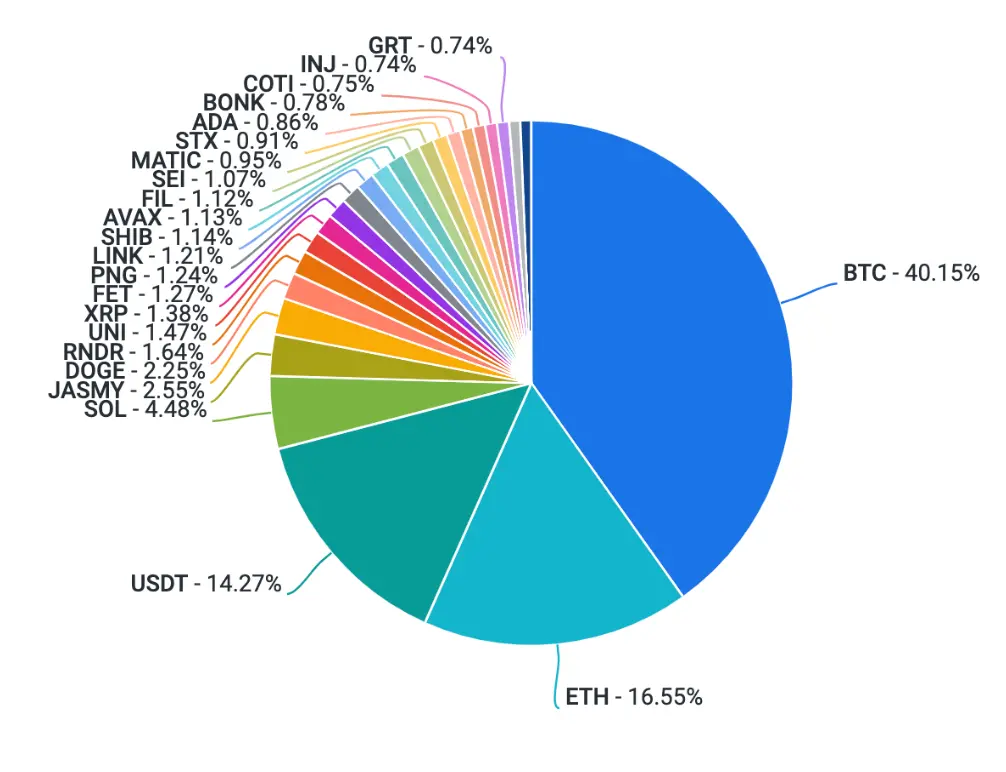

Coinbase Platform Trading Volume (Asset Ratio)

Funding Rates

Notable Crypto News

Institutional

- VanEck launches NFT platform, offering tokenized ownership of watches and wine before March (The Block)

- Ledn launches Ethereum-backed loan services, accepting former Celsius users (The Block)

Regulatory

- Elizabeth Warren willing to "work with" the crypto industry (but reiterates the need to follow traditional financial rules) (The Block)

- Hong Kong ends licensing application activities for cryptocurrency exchanges (Cointelegraph)

General

- Ethereum NFT card game "Gods Unchained" launches on iOS and Android (Decrypt)

Coinbase

- Coinbase announces support for asset recovery on BNB Smart Chain and Polygon (Coinbase Blog)

- Coinbase Cloud adds support for Nethermind and Erigon to enhance diversity in Ethereum execution clients (Coinbase Blog)

- The evolving wallet industry will help onboard a billion users (Coinbase Blog)

Global Perspectives

Europe

- ECB officials state that Bitcoin's fair value remains zero (ECB blog) (Decrypt)

- Paris Saint-Germain becomes the first football team to validate on the blockchain (CoinDesk)

- The Law Commission of England seeks opinions on a legislative proposal to classify cryptocurrencies as property (CoinDesk)

Asia

- Major Japanese companies Mitsubishi UFJ, Rakuten, and Mizuho to launch security tokens (Cryptonews)

- Hong Kong Monetary Authority issues circular regarding the sale and distribution of tokenized products (HKMA)

- Hong Kong's Financial Secretary states that a regulatory sandbox will be launched for stablecoin issuers (The Block)

Risk warning

Risk warning Risk warning

Risk warning