SignalPlus Macro Analysis: SPX Hits All-Time High, Inflation Data Raises Market Concerns

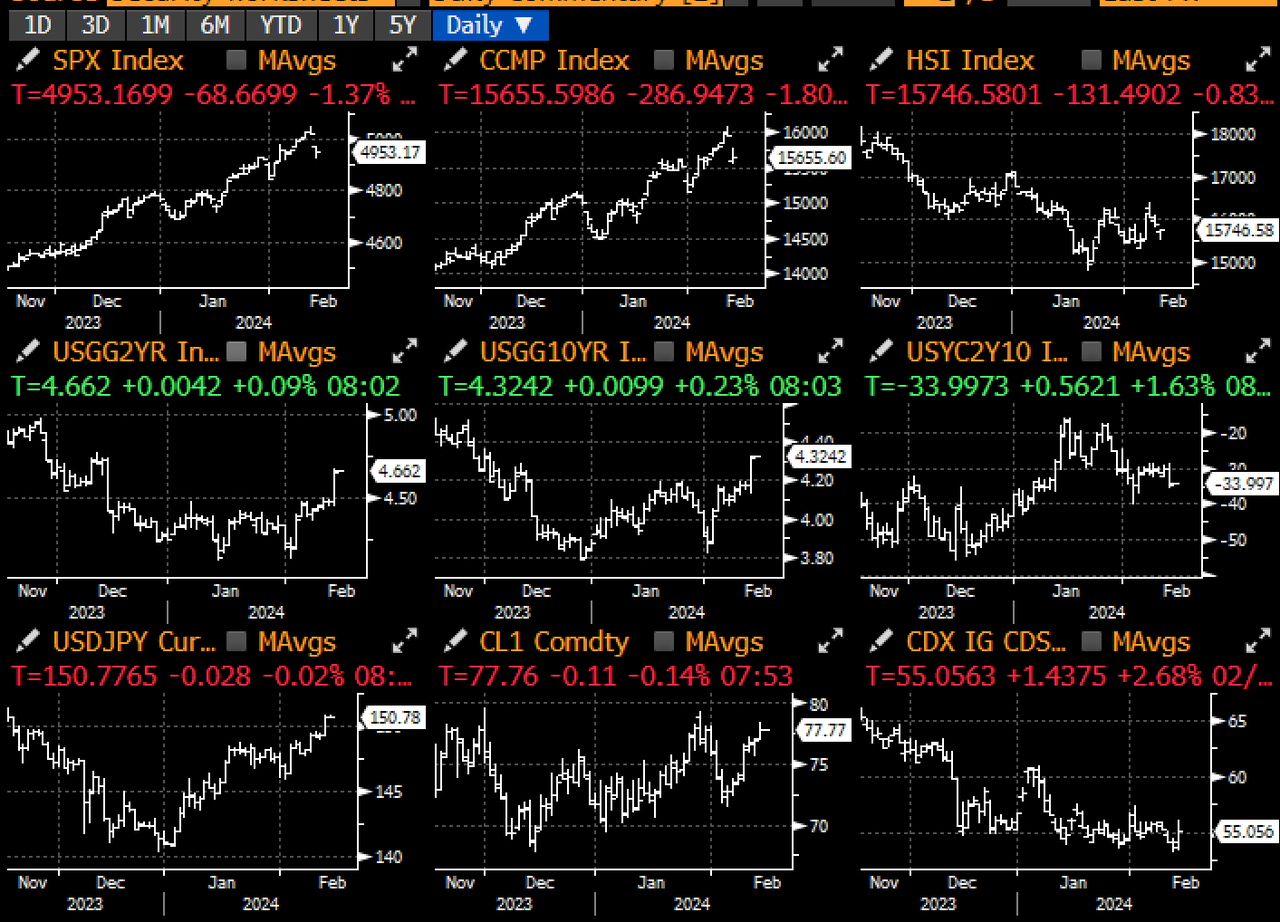

As the Asian holiday market closed, the SPX successfully broke through the historical high of 5,000 points, BTC reached 50,000 dollars, and Nvidia became the fourth largest publicly traded company in the world (surpassing Amazon), indicating that risk sentiment seems to have entered an overheating state.

As the Asian holiday market closed, the SPX successfully broke through the historical high of 5,000 points, BTC reached 50,000 dollars, and Nvidia became the fourth largest publicly traded company in the world (surpassing Amazon), indicating that risk sentiment seems to have entered an overheating state.

Dear friends, Happy Year of the Dragon! May this new year bring prosperity and happiness to you and your loved ones.

As the Asian holiday market closes, SPX successfully broke through the historical high of 5,000 points, BTC reached $50,000, and Nvidia became the fourth largest publicly traded company on Earth (surpassing Amazon). Risk sentiment seems to have entered an overheated state.

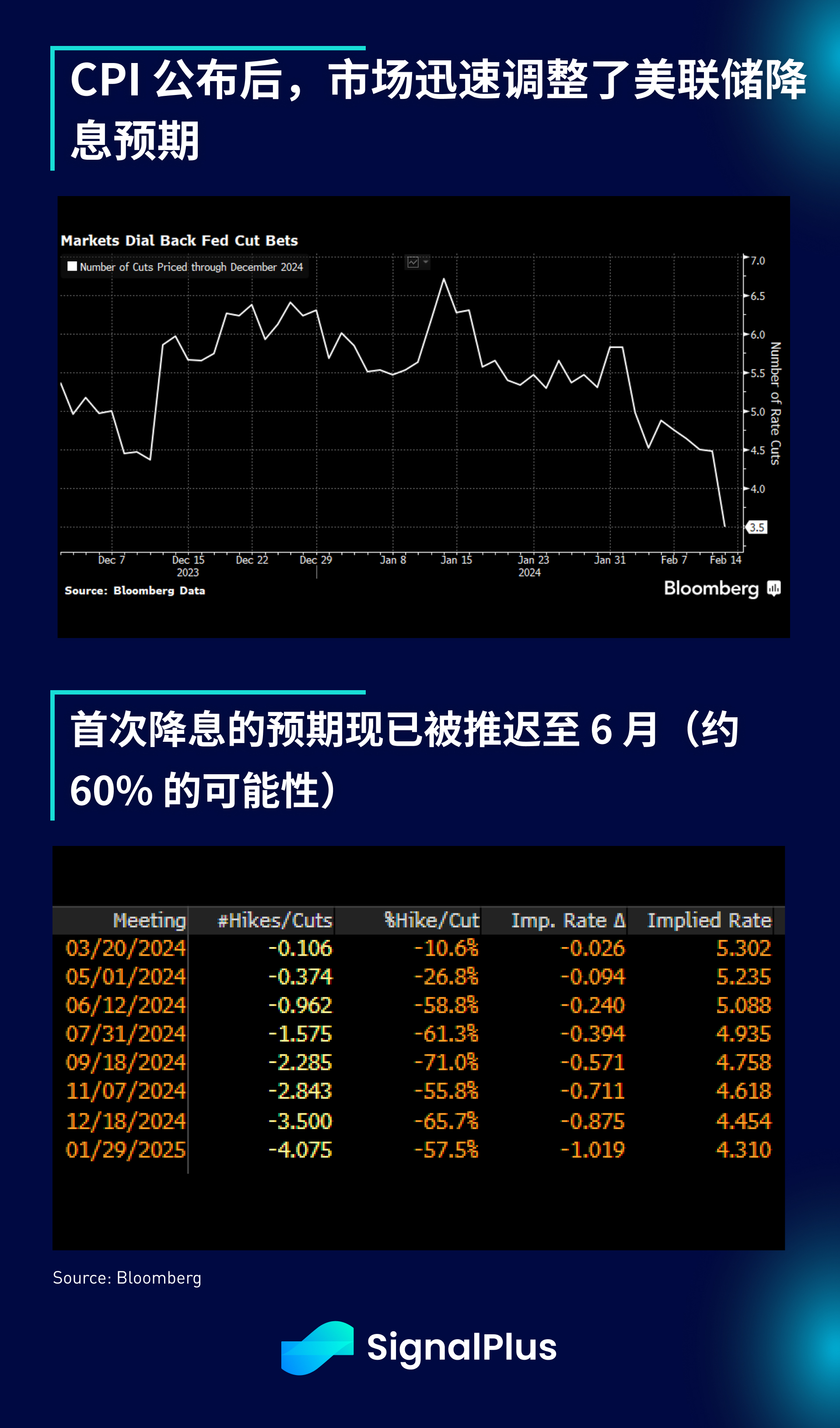

However, the market clearly had other ideas. Yesterday's CPI delivered an unwanted number, with core CPI rising 0.39% month-on-month, and Owners' Equivalent Rent (OER) increasing by 0.56%, leading to a 3-month annualized core CPI growth of 4% (up from 3.3%). Meanwhile, super core inflation rose 0.8% month-on-month (the largest increase in two years), posing a severe challenge to the Federal Reserve's narrative of slowing inflation. Worse still, the share of core expenditures experiencing inflation slowdown dropped from 44% to 29%, while the share of categories with persistently high inflation (4%+) surged from 38% to 58%. In summary, this is a CPI report that is very unfavorable to risk sentiment, significantly increasing market attention on the retail sales and PPI data to be released later this week.

The market quickly reacted to the unfavorable economic data, with short-term U.S. Treasury yields rising by 17 basis points, the 5/30s curve flattening by 9.5 basis points, and the stock market dropping by 1.5% to 2%. Gold prices also fell, and as financial conditions tightened rapidly, credit spreads widened. SOFR H4-H5 (March) futures prices reflect that the market has ruled out expectations for a rate cut, and the U.S. 1y1y rate surged by 25 basis points, with the 10-year real rate rising back to 2%, a level last seen on the morning of the December FOMC meeting (before the dovish pivot). In short, following the CPI release, market expectations for rate cuts by the end of this year have been adjusted from 6.5 times to "only" 3.5 times.

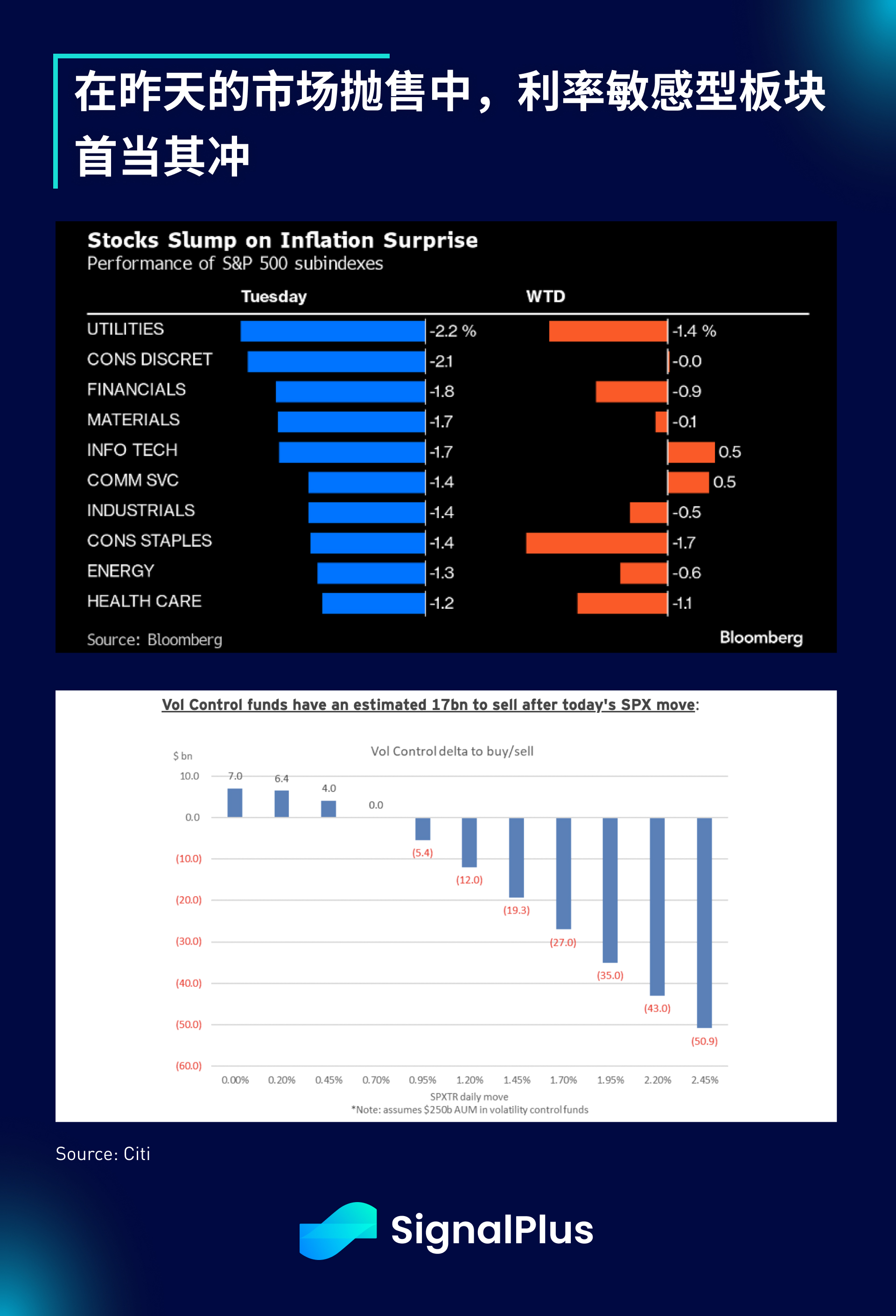

The SPX index fell by 1.4%, and the Nasdaq index dropped by 1.8%. Growth stocks performed poorly as expected in the rising yield environment. Precious metals, regional banks, gold miners, and other interest rate-sensitive sectors faced sell-offs. The upcoming retail sales and PPI data have suddenly become quite important in driving short-term sentiment, as in the context of softening economic data, the return of "high rates for a longer time" essentially implies an increased likelihood of recession, which could pose a real headwind to risk assets in the short term. Additionally, as actual volatility begins to increase, Wall Street expects systematic volatility control funds to reduce equity exposure, further increasing the downside risk to the market amid wavering risk sentiment.

Despite BTC spot prices breaking through $50,000, the cryptocurrency market remains relatively quiet, with futures liquidations still moderate despite the rapid price rebound. Analysts report that 9 BTC spot ETFs, aside from GBTC, have attracted a total of $1.46 billion in funds since their launch, offsetting outflows from GBTC. However, as price movements increasingly reflect TradFi activities (ETFs replacing risk positions, and BTC futures open interest continuing to decline), it is advisable to closely monitor the impact of further tightening financial conditions on cryptocurrency prices, particularly the trends in gold prices and real rates in the short term.