OKLink Research Institute: Using "beauty" as a mirror to explore the future development of Bitcoin spot ETFs in Hong Kong

Spot ETFs provide a more convenient and standardized investment method for a wide range of investors.

Spot ETFs provide a more convenient and standardized investment method for a wide range of investors.Produced by|OKLink Research Institute

Author|Hedy Bi

According to a report by The Block on January 29, Harvest International has become the first institution to submit a Bitcoin spot ETF application to the Hong Kong Securities and Futures Commission (SFC). As early as December 22 last year, the SFC issued a circular titled "Regarding the SFC's Recognition of Funds Investing in Virtual Assets," clearly stating its readiness to accept applications for the recognition of virtual asset spot ETFs.

In the United States, the development of Bitcoin spot ETFs after approval for listing serves as a good reference for Hong Kong. However, due to Grayscale's continuous selling of Bitcoin, the U.S. Bitcoin spot ETF did not deliver impressive performance just 19 days after its listing. At this point, does it still make sense for Hong Kong financial companies to venture into Bitcoin spot ETFs?

Choosing Central or Wall Street, Multiple Subscription and Redemption Methods May Become the Biggest Advantage

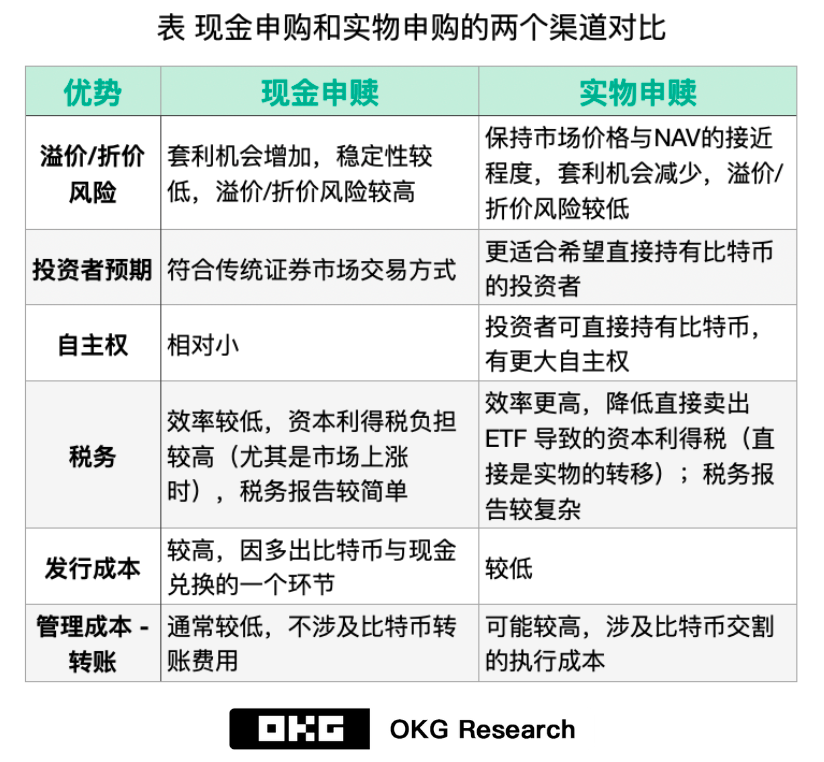

In comparison between the two regions, Hong Kong has some advantages over the U.S. in terms of rules for virtual asset ETFs. According to the SFC's circular, Bitcoin spot ETFs can be subscribed and redeemed in both physical and cash forms (hereinafter referred to as "subscription and redemption").

Although U.S. applicants stated in their early applications that "the subscription and redemption methods allow for both physical and cash options," due to risk considerations, they ultimately modified their applications to use the less risky "cash" redemption method. Compared to the U.S. Bitcoin spot ETFs, which are limited to "cash" redemption, the current content disclosed in the SFC's circular indicates that a variety of subscription and redemption methods, including cash and physical options, are expected to become a major advantage for Hong Kong's future Bitcoin spot ETF market.

Due to the unique nature of Bitcoin as a virtual asset, adding physical subscription and redemption methods brings more challenges in terms of conversion, custody, and transfer of Bitcoin assets. For example, in the case of subscription, participants must first transfer the virtual assets to a custody account recognized and permitted by the SFC, including virtual asset trading platforms (VATPs) or recognized institutions (or their subsidiaries), to ensure compliance with local regulatory requirements. This is primarily to prevent illegal actors from converting and laundering Bitcoin through physical subscription and redemption.

Physical subscription and redemption involve the transfer of on-chain assets, which requires financial institutions and regulatory bodies to adopt a compliance approach different from traditional markets—on-chain compliance. On-chain compliance shares some similarities with traditional off-chain compliance, including KYC (Know Your Customer), AML (Anti-Money Laundering), and cross-border compliance. To meet these compliance requirements, compliance technology tools are typically needed, which are primarily used to execute asset risk confirmation for on-chain addresses and continuously monitor asset flows for suspicious transactions.

Given the unique nature of blockchain technology, while transactions on on-chain addresses are immutable, clear, and publicly verifiable, their anonymity makes many institutions hesitant to comply. To address this anonymity, one viable solution is to compare addresses with those already flagged as high-risk for sanctions, money laundering, phishing, etc., to determine whether the on-chain address is involved in high-risk trading activities. For this reason, having a rich and comprehensive address labeling database has become one of the important criteria for financial institutions and regulatory bodies when selecting compliance technology tools.

In terms of continuously monitoring asset flows, when financial institutions choose compliance technology tools, they need to consider not only those with large data volumes and comprehensive labeling dimensions but also the response speed of compliance technology in ongoing risk monitoring. Once a compliance technology tool identifies a suspicious transaction, for example, OKLink can conduct risk monitoring at the millisecond level and quickly proceed with subsequent actions: assessing risk levels and implementing risk control measures based on those levels, such as freezing accounts or rejecting transactions.

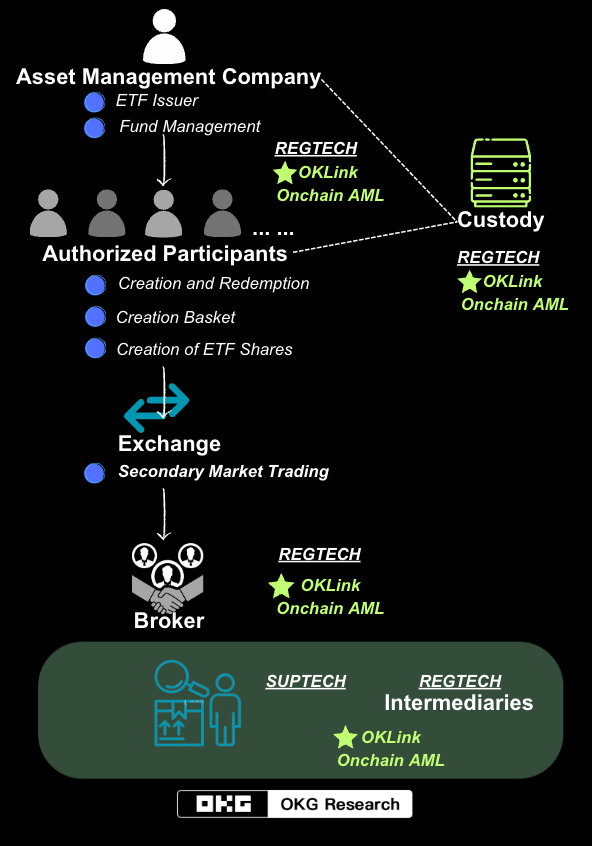

Figure: Using OKLink Onchain AML as an example, a simplified diagram of how compliance technology assists from the issuance to trading of Bitcoin spot ETFs

Note: This is a rough flowchart; regarding compliance technology requirements, it is a more rigorous practice for "Intermediaries" to be supported by compliance technology.

What Qualifications Are Required for Custodians Under Physical Subscription and Redemption?

Currently, Hong Kong has approved futures-based Bitcoin ETFs, with two listed products: the Southern Eastern Bitcoin Futures and the Samsung Bitcoin Futures, both of which have relatively small asset scales, with each fund's AUM being less than $100 million. The trustees for these two funds are both HSBC Institutional Trust Services (Asia) Limited. Notably, HSBC is the first bank in Hong Kong to allow clients to buy and sell virtual asset ETFs listed on the Hong Kong Stock Exchange, and it launched a virtual asset investor education center in mid-last year.

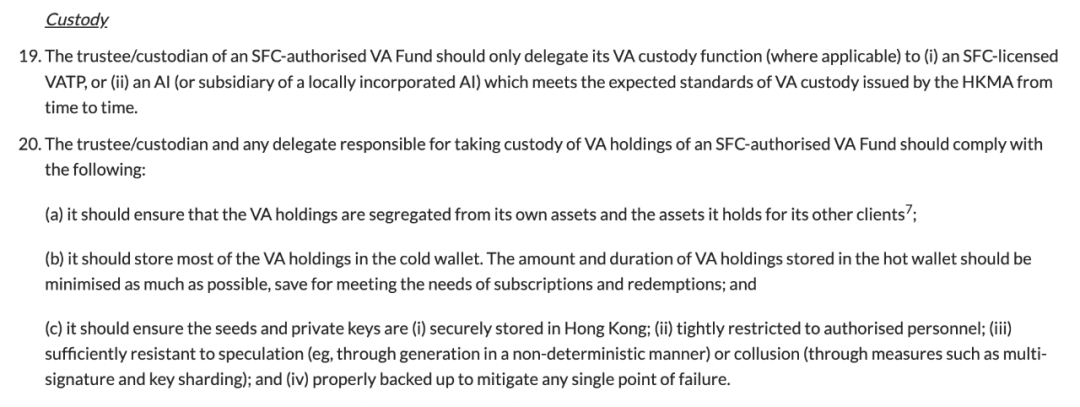

Unlike the custody requirements for futures ETFs, which only involve cash, the challenge for spot ETFs is that custodians need to be responsible for the custody of Bitcoin. Currently, according to the SFC's circular, the trustees/custodians of virtual asset funds authorized by the SFC can only delegate the custody function of virtual assets to virtual asset service providers (VATPs) holding SFC licenses or financial institutions or local subsidiaries that meet the virtual asset custody standards published by the HKMA.

Figure: Excerpt from the SFC's circular regarding the recognition of funds investing in virtual assets

This means that, based on the current development of financial institutions and virtual asset service providers (VASPs) in Hong Kong, financial institutions and licensed VATPs will be responsible for the custody of fiat currency and virtual assets, respectively, and their cooperation will be the key to the success of Bitcoin spot ETFs.

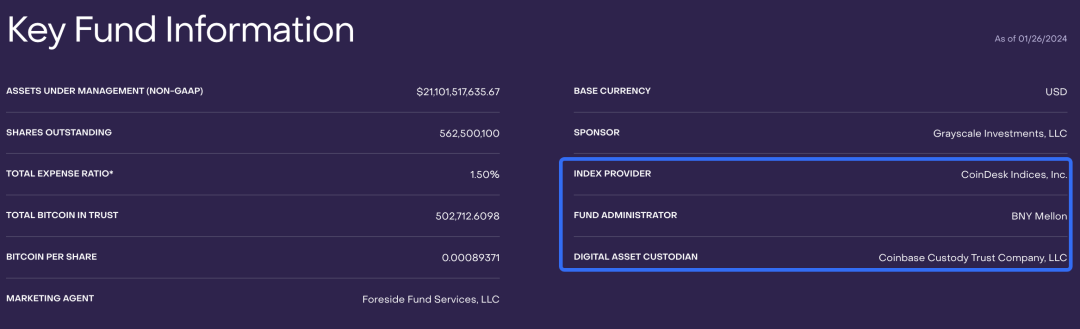

The same is true in the U.S.; among the 11 ETFs approved so far, 8 have chosen Coinbase as their virtual asset custodian. For example, the two largest AUM firms, Grayscale and BlackRock, have both chosen Coinbase and BNY Mellon as their virtual asset custodian and cash custodian, respectively, adopting a dual-custody model separating virtual assets and fiat currency.

Figure: Basic information on Grayscale GBTC

In terms of VATPs, several companies in Hong Kong are actively applying for relevant licenses. This indicates that there will be multiple VATPs available for fund companies to choose from in the future, thus avoiding the "single point" risk of multiple Bitcoin ETFs in the U.S. choosing only one custodian.

Grayscale Is Just an Example; Hong Kong Will Not Repeat the Mistakes

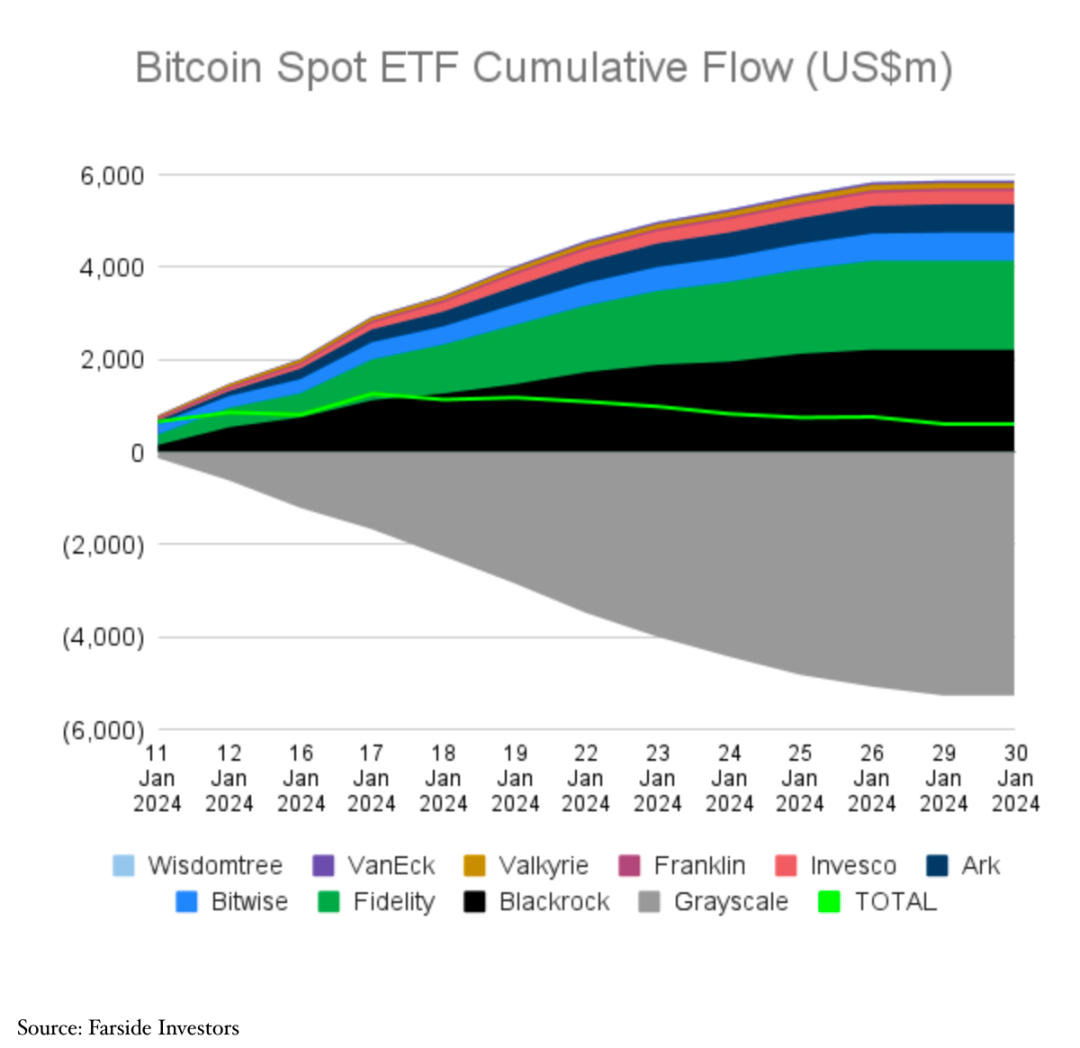

Since the U.S. approved Bitcoin spot ETFs, one of the most discussed topics has been Grayscale's continuous large-scale selling. However, the Hong Kong market does not have a Bitcoin trust as large as Grayscale, so even if the Bitcoin trust in Hong Kong converts to an ETF and begins redemption operations, it is unlikely to see such large-scale selling.

However, even with Grayscale's continuous selling, the overall flow of Bitcoin spot ETFs in the U.S. has shown a net inflow as of 9 AM today (UTC+8), with OKLink statistics indicating approximately $605 million. Specifically, only Grayscale has been experiencing continuous outflows, while other funds have shown inflows.

The reasons for Grayscale's continuous selling are mainly twofold: first, compared to other fund companies, Grayscale has the highest management fees, meaning that investors buying $1 million of IBIT and the same amount of GBTC would save $13,800 in management costs; second, unlike other newly issued Bitcoin spot ETFs, Grayscale operates by converting its trust into an ETF. This allows investors who previously bought GBTC at a discount to take advantage of the discount and the rise in Bitcoin prices to arbitrage sell without needing to redeem and repurchase.

According to observations from OKLink Research Institute and on-chain data from OKLink, Grayscale began transferring on-chain assets to Coinbase Prime hot wallet addresses almost every working day two weeks ago. Moreover, since January 23, 2024, Grayscale's continuous outflow trend has also been gradually weakening.

The launch of Bitcoin spot ETFs has achieved a close connection between traditional financial markets and virtual asset markets, marking the opening of structured financial markets to the virtual asset field. According to Technavio's estimates, from 2023 to 2028, the global structured financial market (Note 1) is expected to grow by approximately $997.68 billion, with an annual growth rate of 11.8%.

With the continuous improvement of compliance practices and market maturity, the launch of Bitcoin spot ETFs will signify the standardization of financial products through Bitcoin in the form of spot ETFs.

Spot ETFs provide investors with a more convenient and standardized investment method. Moreover, standardized products can enhance the effective operation of the market and improve risk management and investor protection. The widespread adoption of compliance assistants that we proposed at the beginning of 2023 is approaching us in full bloom.

Note 1: The global structured financial market encompasses various complex financial instruments characterized by being supported by a pool of underlying assets. Some common structured financial products include: securitization products, derivatives, debt instruments, structured derivatives, financial engineering products, etc. Here, Bitcoin ETFs, as a type of securitization product, belong to the structured financial market.