Surf Protocol's "Uniswap Moment" in the Derivatives Market

Although we cannot determine the most efficient mechanism arrangement, the market may gradually approach the highest efficiency through continuous trial and error and selection. With the support of new assets and new paradigms, the "Uniswap moment" of permissionless trading of derivatives is about to arrive.

Although we cannot determine the most efficient mechanism arrangement, the market may gradually approach the highest efficiency through continuous trial and error and selection. With the support of new assets and new paradigms, the "Uniswap moment" of permissionless trading of derivatives is about to arrive.Original Title: “Surf Protocol, "Uniswap" in the Derivatives Market”

Author: Loki, ABCDE

1. Overview

This article mainly introduces the Surf Protocol, which aims to provide an unlimited number of tradable assets, lower fees, and transparent settlements, enabling permissionless derivatives trading for almost any asset.

2. When Will Decentralized Derivatives Experience the "Uniswap Moment"?

2.1 Problem

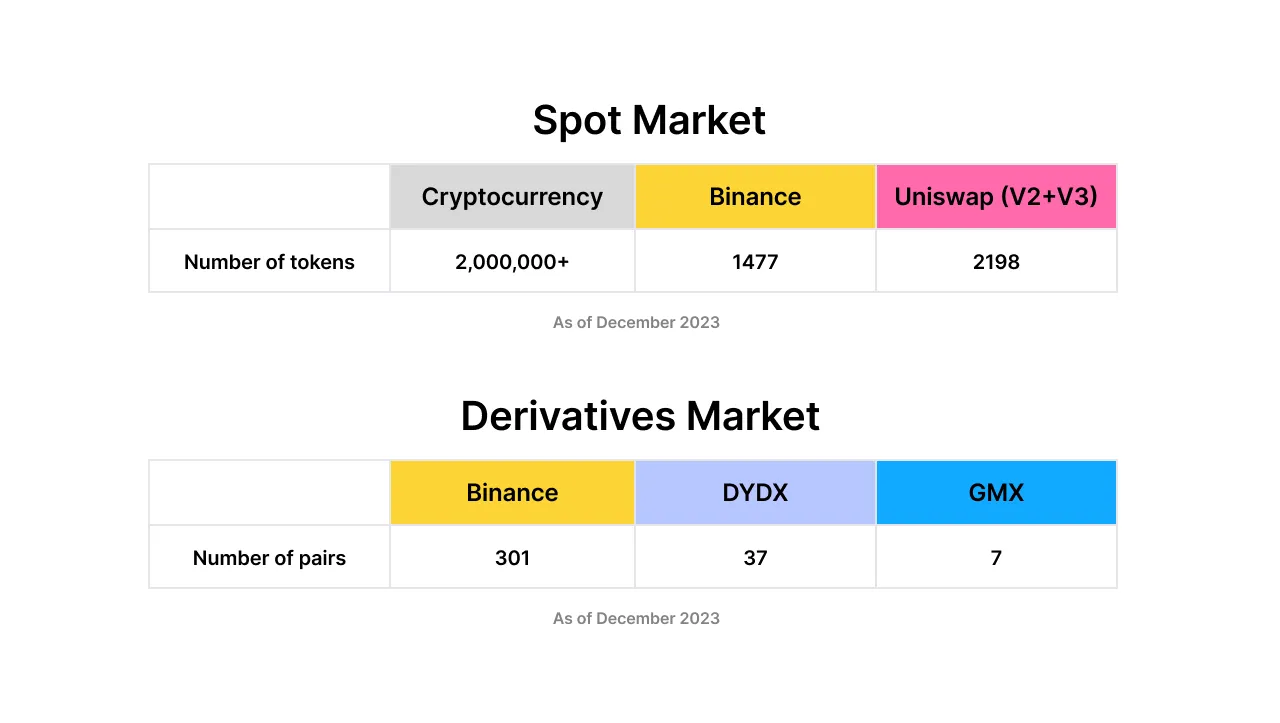

The potential of decentralized derivatives has not yet been fully developed. According to Coinmarketcap data, as of December 2023, there are over 2 million cryptocurrencies issued, with the largest cryptocurrency exchange Binance offering 1,477 trading pairs for 394 tokens, while the largest decentralized exchange Uniswap provides at least 2,198 active trading pairs (v2+v3).

However, in the derivatives space, there remains a significant gap in the richness of underlying assets between decentralized and centralized markets. Currently, Binance offers 301 derivatives trading pairs, while dYdX and GMX only provide 37 and 7 trading pairs, respectively.

Since the collapse of FTX, the market has shown a particularly strong interest in decentralized custody of derivatives trading assets, with both centralized and decentralized exchanges exploring various decentralized solutions. But just as people associate Uniswap with decentralization while overlooking permissionlessness, the derivatives market also needs a permissionless "Uniswap."

2.2 Solution

In the derivatives market, especially for niche assets, NFTs, and emerging assets, the issue is not a lack of buying and selling demand, but rather a lack of sufficient liquidity providers and effective supply-demand matching mechanisms. Surf Protocol achieves permissionless derivatives trading by encouraging liquidity providers (LPs) to voluntarily provide liquidity and accept trades of specific asset positions in profit or loss. Contract prices are determined by Oracle and TWAP average prices. Different assets have different risk structures in terms of liquidity, market capitalization, and volatility, allowing limited partners to choose their fee structures. With enough LP providers, market competition will ultimately lead to optimal allocation.

3. Surf Protocol Design Scheme

3.1 Trading Structure

Let’s first review the design of Spot DEXs, whether Uni V2, V3, or Curve, which operate through LPs. Providing liquidity essentially involves placing a certain number of orders within different ranges to collectively provide liquidity for traders. LPs are passive traders and provide paid services to become counterparties. From a risk structure perspective, providing liquidity is akin to shorting volatility. Impermanent loss represents the realization of volatility gains and losses. In the contract, LPs are not necessarily equivalent to shorting volatility. Due to leverage, users are more likely to stop-loss and liquidate during high volatility, potentially bringing additional profits to LPs. In other words, LPs can not only avoid impermanent loss but also achieve "impermanent gains," which is contrary to the usual saying of "the price hasn't changed, but the position is gone." The "leverage" behavior of LPs is beneficial to them, similar to how casino operators do not engage in 1:1 gambling but run businesses with guaranteed profits. It is evident that to create a trading market, one must "pay a reasonable price and have unconditional counterparties." Surf Protocol is built on this premise. On Surf, liquidity providers (LPs) provide liquidity and take the opposite trading approach for specific trading pairs. This model is based on the following assumptions:

Ignoring trading friction, when there are enough trading activities, the overall mathematical expected profit of traders tends to 0. Based on consensus in stock and forex markets, it is often negative.

Considering trading friction (fees, slippage, settlement), when there are enough trading activities, the limit of overall profit's mathematical expectation for traders is < 0.

The limit of the overall profit's mathematical expectation for traders refers to the limit of the profit expectation for counterparties > 0.

In the long run, this will generate a positive expected value. Each asset's liquidity pool is independent, as each asset is considered to have unique risks that should not spread to other trading pairs. This structure isolates risks between different assets, ensuring asset independence while also expanding liquidity for newly issued assets.

3.2 Effectiveness of Economic Incentives

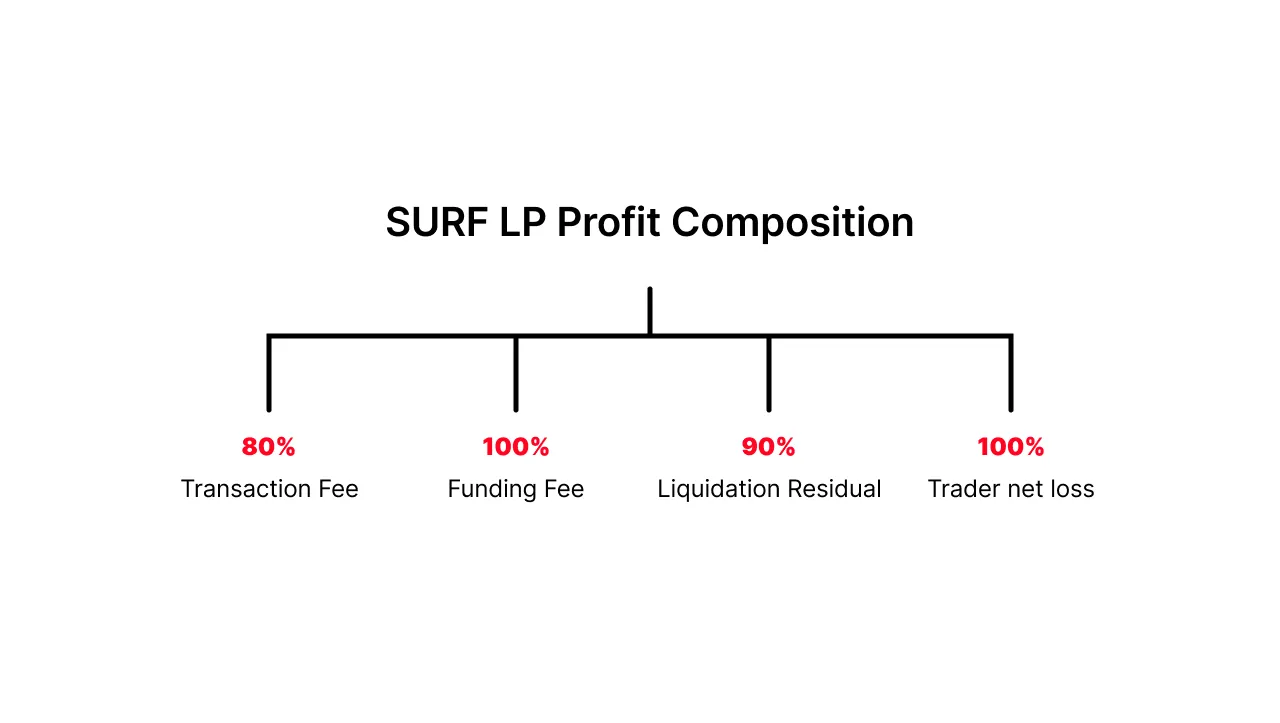

The essence of providing liquidity is to become a counterparty to traders. Therefore, the key issue is how to ensure the effectiveness of economic incentives. On Surf, LPs can earn at least 80% of trading fees, 100% of funding rates, 90% of liquidation residuals, and 100% of users' net gains and losses. These earnings ensure that limited partners have a positive mathematical expectation in the long term to compensate for the risks they undertake. Moreover, since operating LPs have significant earnings, new asset LPs are motivated to attract more users to join the trading pairs they create to maximize profits.

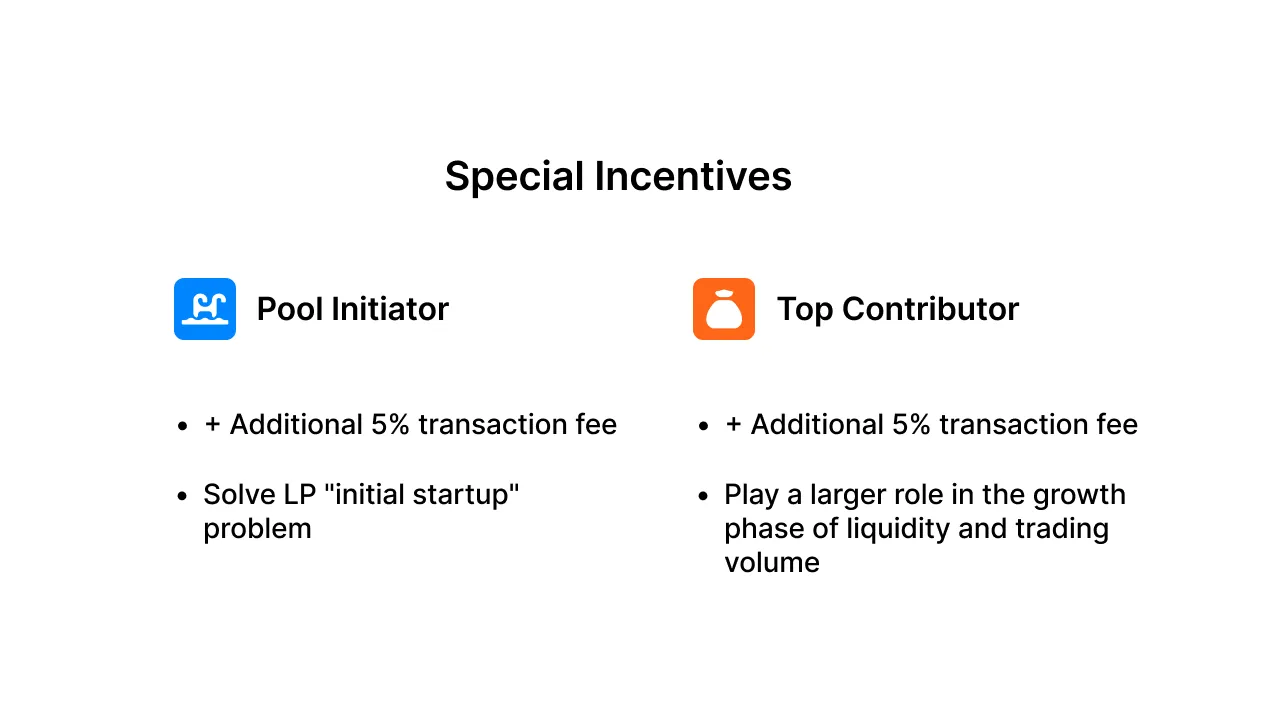

In addition, Surf provides two extra designs:

(1) Special Incentives. Each pool creator on Surf can earn an additional 5% of trading fees, and the largest LP in each pool can also earn 5% of trading fees. A common issue in the DeFi space is whether trading demand comes first or liquidity comes first; the 5% initial reward can effectively address the "initial launch" problem, while the 5% reward for the largest LP will play a greater role during the liquidity and trading volume growth phase.

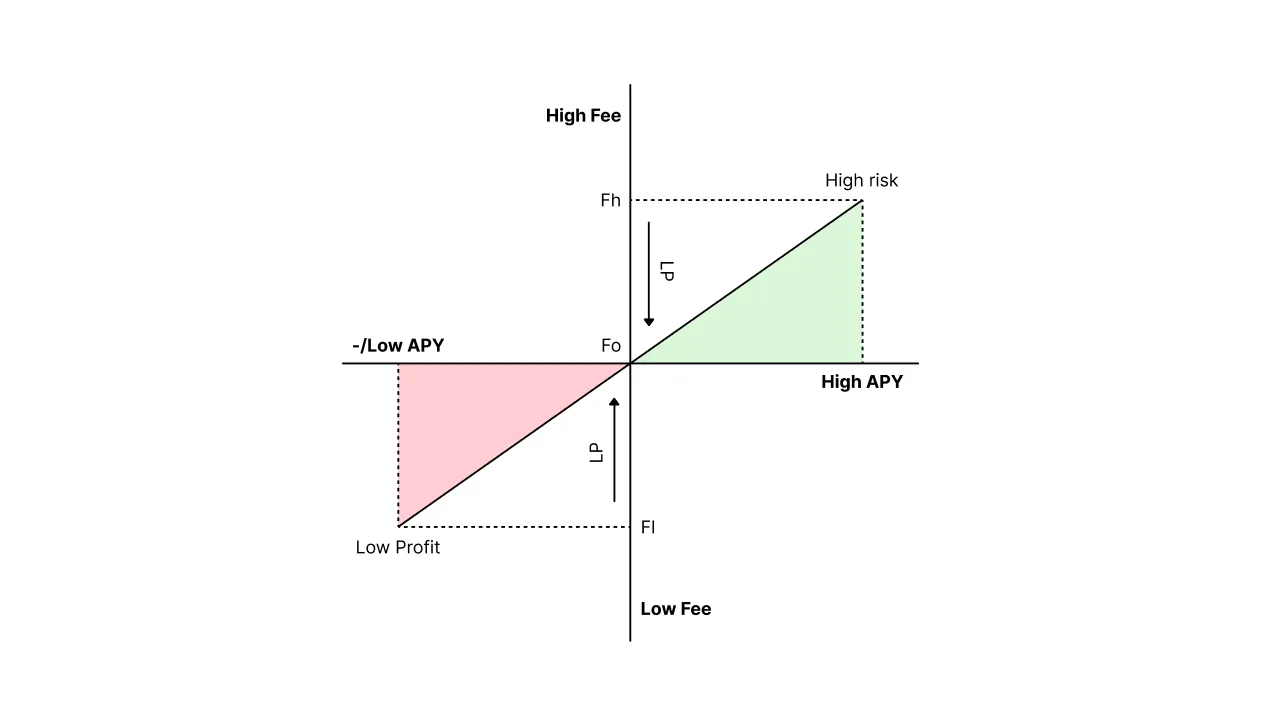

(2) Gradient Fees. Surf currently sets five fee options: 0.05%, 0.1%, 0.3%, 1%, and 3%. Liquidity pools are used as counterparts for all traders' positions, executing orders in order from the lowest to the highest fee level. The purpose of this design is to accommodate as many asset classes as possible and facilitate effective resource allocation in the market. If the current fees provided by LPs are too high, other LPs will have the incentive to offer lower rates when profitable, continuously competing until market balance is achieved. The same LP can also allocate its funds across different fee levels.

3.3 Oracles and Liquidation

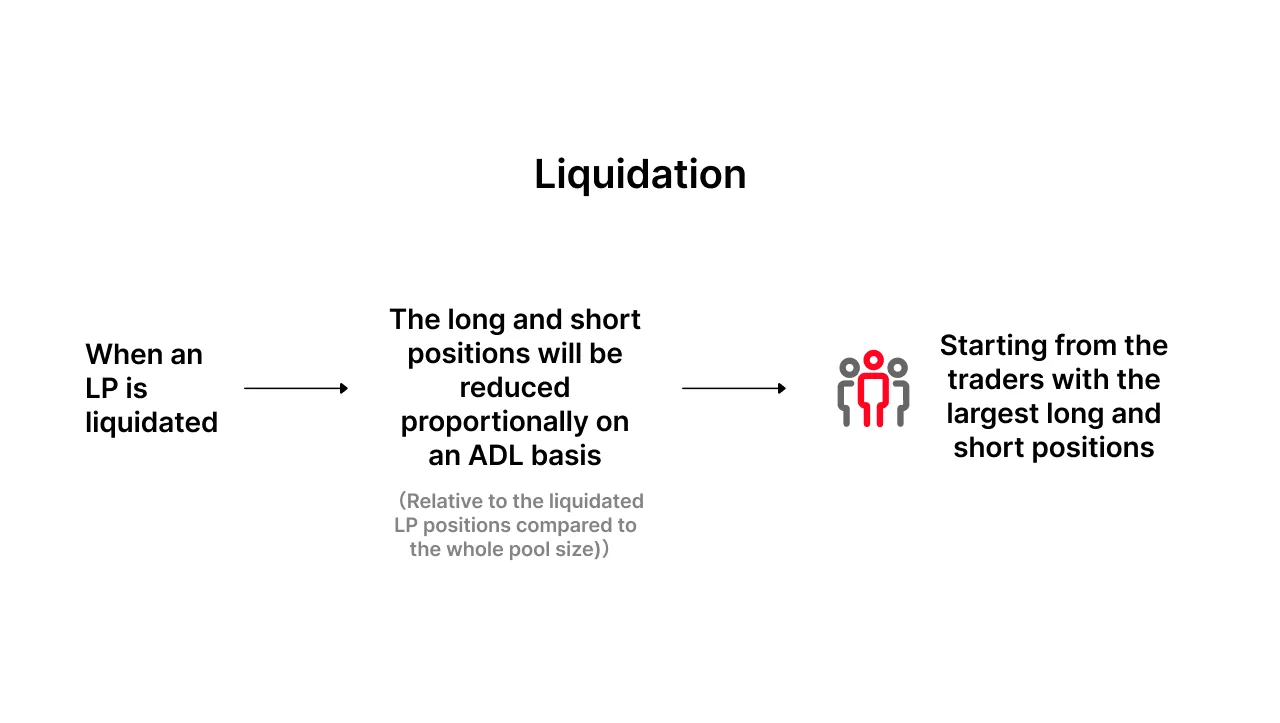

No derivatives solution can bypass the issues of oracles and liquidation, and the same exists in Surf Protocol. For mainstream assets, Surf uses a common weighted average method for calculation, ensuring prices are relatively fair and secure; for assets on Uniswap, Surf innovatively proposes a 30-block TWMP average price + spot price comparison scheme, ensuring the stability of oracles against common attacks such as flash loans and cross-block attacks, while also preventing the risk of arbitrage for LPs caused by price delays due to the introduction of average prices.  Additionally, Surf Protocol introduces the concept of "leveraged LPs," meaning LPs can achieve higher capital efficiency but also amplify corresponding risks. Treating LPs and traders as both sides of a trade, when the profit of either side approaches the capital of the other, it indicates a potential for liquidation. In such cases, long and short positions will be proportionally reduced based on the ratio of LP's closed positions to the total pool size, starting from the largest long and short positions.

Additionally, Surf Protocol introduces the concept of "leveraged LPs," meaning LPs can achieve higher capital efficiency but also amplify corresponding risks. Treating LPs and traders as both sides of a trade, when the profit of either side approaches the capital of the other, it indicates a potential for liquidation. In such cases, long and short positions will be proportionally reduced based on the ratio of LP's closed positions to the total pool size, starting from the largest long and short positions.

4. Moving Towards the Future of Decentralized Derivatives

In addition to the protocol itself, we also see some interesting directions:

Non-Custodial and Permissionless:

Looking back at history, after the competitive landscape of leading centralized exchanges was basically established, we still saw many medium-sized exchanges thriving between 2018 and 2020, followed by the emergence of permissionless decentralized exchanges like Uniswap and Curve. This pattern is likely to be replicated in the derivatives space. Since 2023, NFTs, Brc-20, and Socialfi have brought us a massive influx of new assets, and the demand for these new and niche assets urgently needs to be met.

Netting of Trading/Counterparty Value:

The initial value of LP tokens for each specific pool in Surf is 1. All subsequent activities and accrued values revert back to the pool and will be reflected in the token's price. This includes trading fees, gains and losses against traders, borrowing fees, and liquidation fees. This feature provides us with an idea—can we net the value of both sides of the counterparty/token issuance? A simple example is "order tokenization," where buying "order tokens" is equivalent to buying a fund operated by traders. Another example is LP ETFs, which distribute funds across different LP pools to reduce single-point risks and provide possibilities for more professional liquidity management.

Competitive Market for Optimized Allocation:

The market may not need to recreate a Binance or GMX, but a "Perp version of Uniswap" that accommodates as many new assets as possible is necessary. Providing derivatives liquidity for different assets carries varying degrees of risk, thus requiring different fee rates to meet the needs for risk compensation. Similar cases include NFTs, which previously charged high trading fees + high royalties, and some MEME tokens that charged 5%-10% trading taxes.

Although we cannot determine the most efficient mechanism arrangement, the market may gradually approach maximum efficiency through continuous trial and error and selection. With the support of new assets and new paradigms, the permissionless trading "Uniswap moment" for derivatives is about to arrive.