Spending $80 million on "subsidies" for growth, Uniswap is taking a big step

The proposal sparked intense discussions within the community as soon as it was issued, with some expressing support while others believed that the plan was meaningless and detrimental to the interests of the DAO.

The proposal sparked intense discussions within the community as soon as it was issued, with some expressing support while others believed that the plan was meaningless and detrimental to the interests of the DAO.Author: BUBBLE, BlockBeats

On February 14, 2025, Devin Walsh, the Executive Director and Co-founder of the Uniswap Foundation, initiated a liquidity incentive proposal for Uniswap v4 and Unichain within the Uniswap Governance DAO. This proposal passed a Temp Check on Snapshot on March 3 and was officially completed on Tally on March 21, with a total of 53 million UNI and 468 addresses participating in the vote. The technical support for the plan, Gauntlet, announced that the first phase of the initiative would last for two weeks and would commence on April 15.

The proposal sparked intense discussions within the community, with some expressing support while others deemed the plan meaningless and detrimental to the interests of the DAO. This article will detail the main content of the plan, how to participate, and the community's views.

Proposal Details

The proposal includes plans for Uniswap v4 over the next six months and for Unichain over the next year. The foundation aims to migrate the 30-day rolling trading volume of $32.8 billion from v3 to v4 on the target chain within six months, requesting a budget of $24 million for this six-month plan.

The activities for Unichain are planned to be implemented over a full year, with the Uniswap Foundation targeting a TVL of $750 million and a cumulative trading volume of $11 billion over the next three months. To achieve these goals, Unichain plans to request approximately $60 million in incentives during the first year, including the $21 million requested this time. It will operate similarly to Uniswap v4 but will consider non-DEX DeFi activities to increase organic liquidity demand, primarily composed of projects built on Unichain and the Uniswap Foundation.

The incentive activities for the two chains differ slightly. Uniswap v4's activities will focus on driving AMM trading volume on each chain, while Unichain's activities will strategically deploy AMM incentives to promote broader DeFi activities across the entire chain and within AMMs.

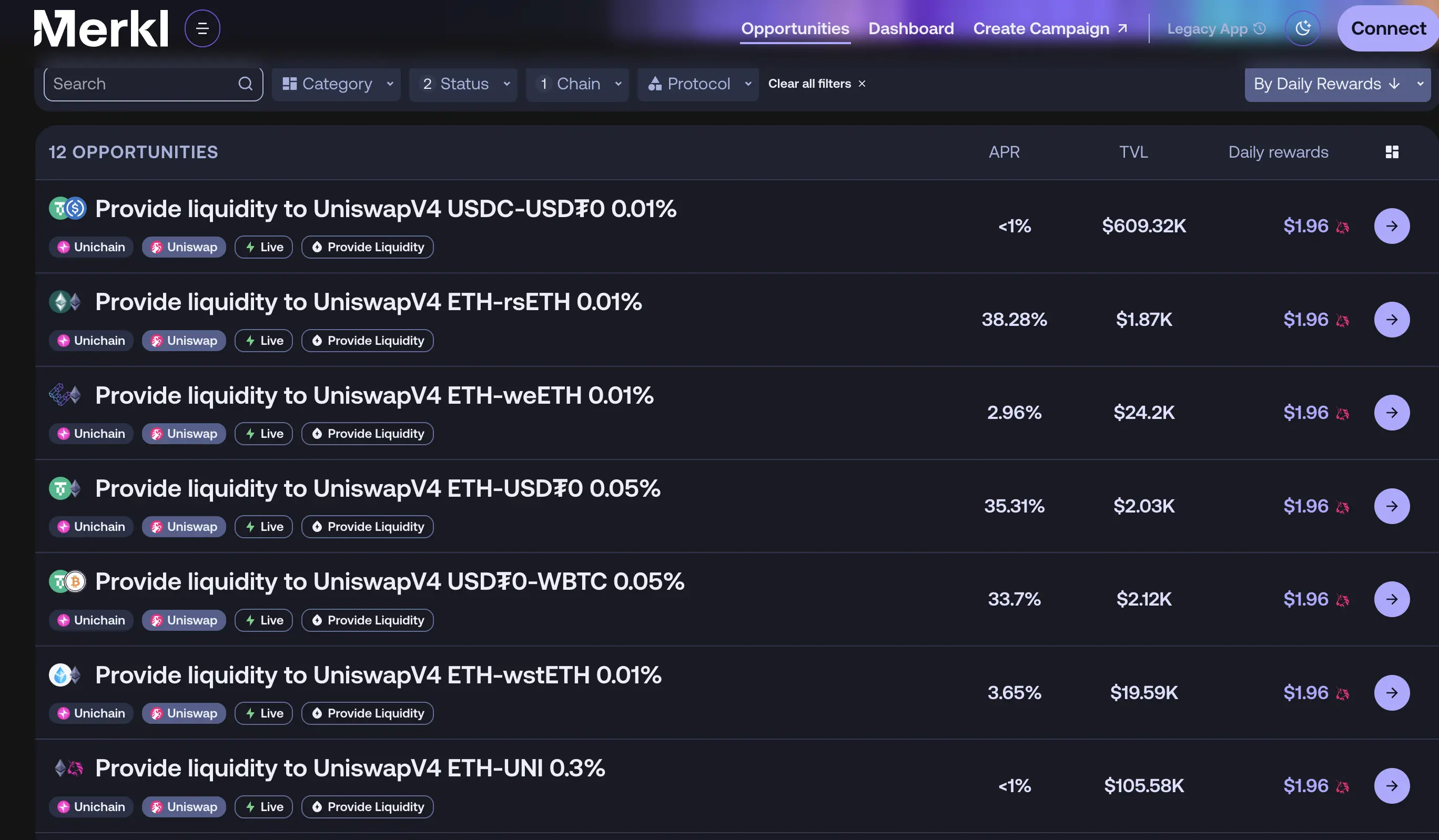

The first Unichain activity will launch on April 15, 2025, lasting for three months and distributing millions of dollars in incentive funds. The $UNI incentives will be distributed across 12 different Unichain pools rewarding LPs. In the first two weeks, the following 12 mining pools will receive $UNI rewards: $USDC/$ETH, $USDC/$USDT0, $ETH/$WBTC, $USDC/$WBTC, $UNI/$ETH, $ETH/$USDT0, $WBTC/$USDT0, $wstETH/$ETH, $weETH/$ETH, $rsETH/$ETH, $ezETH/$ETH, $COMP/$ETH.

In this activity, Gauntlet and Merkl play significant roles. Gauntlet is a simulation platform for on-chain risk management that adjusts key parameters of protocols through agent-based simulations to enhance capital efficiency, fees, risks, and incentives. Merkl, incubated by a16z, is a one-stop platform integrating DeFi investment opportunities across multiple chains and protocols.

For this activity, Gauntlet provides its "Aera" vault technology, which will store funds in the vault after DAO voting approves the funding request. Gauntlet will determine the liquidity pools with the highest trading volume on each network and calculate the additional returns needed to make Uniswap v4 a more economically attractive option. Adjustments will be made every two weeks, and the selection of which pools will receive how much incentive and how to claim rewards will be announced on the Merkl website.

Aggressive Growth Targets, Conventional Growth Strategies

Discussion on Incentive Effects and Subsequent Retention

Member "UreNotInD" was the first to oppose the proposal in the DAO voting discussion, primarily because the funding needed in the proposal was compared to the liquidity spending of other projects ("Aerodrome spends $40-50 million monthly, ZkSync Ignite $42 million over 9 months, Arbitrum has spent nearly $200 million since last March"). He believes this is a conventional strategy that many projects have already tried with little success.

Currently, the strongest competitor, Fluid, is capturing market share without offering any incentives. The most popular L2 network, Base, has successfully gained market share without user incentives. These measures do not address the structural issues that could help Unichain grow, such as interoperability between superchains, developing unique use cases for DeFi, and improving the issuance of on-chain native assets ("RWA, meme coins, AI tokens"). Native assets are the stickiest, and the foundation should attract and fund more developers through these means.

Member "0xkeyrock.eth" shared similar concerns, suggesting that Gauntlet's report should be publicly shared in the forum. This report cost a significant amount of money, but the information presented in the forum was superficial and insufficient to justify such a large-scale incentive.

He pointed out several unreasonable points in the report. For example, Aerodrome's high incentives are due to 100% of the fees being redistributed to veHolders, making it incomparable to this type of liquidity incentive. Additionally, zkSync's $5 million monthly token rewards only increased TVL from $100 million to $266 million.

At this point, Unichain's total TVL is only $10 million, indicating insufficient market demand for Unichain. Gauntlet's claim that it can elevate Unichain's TVL to $750 million with $7 million in monthly incentives seems lacking in authenticity.

Even if the incentive subsidy temporarily boosts activity, how to sustain demand remains a question. Historical cases like MODE ("TVL dropped from $575 million to $19 million"), Manta ("$667 million to $46 million"), and Blast ("$2.27 billion to $233 million") suggest that Unichain may face a similar fate.

Based on previous comparisons by Forse Analytics regarding the "TVL growth per dollar spent on incentives" for Uniswap across various chains, in the L2 with the most developed infrastructure, Base, the best-case scenario is $2,600 in TVL per dollar, while the worst-performing Blast is about $500. To reach the target of $750 million in TVL, simple calculations show that the former would require $300,000 daily, while the latter would need $1.5 million.

Although the comparative data is not comprehensive, it can represent a certain range. To use $7 million to elevate Unichain's TVL to $750 million within three months, it would require improving the surrounding infrastructure and user levels to be similar to Base, while the worst-performing Blast chain currently has a TVL over ten times that of Unichain.

The member also shared data from the 2024 Uniswap v3 incentive plan results during new chain deployments, showing that the best-performing DEX TVL in the Sei ecosystem ranked 6th with only $718,000, while the worst-performing Polygon zkEVM had a TVL of merely $2,600, ranking 13th in DEX TVL within that chain ecosystem. None of these deployments exceeded $1 million in TVL, and hardly any entered the top DEX of their respective chains. Most of these deployments have completely lost vitality, with the only trading volume coming from arbitrageurs correcting outdated prices.

A table created by 0xkeyrock.eth showing the TVL and DEX rankings Uniswap achieved after deploying incentives across multiple chains.

These incentive pool deployments have almost all failed to generate a flywheel effect, showing a cliff-like drop after the activities ended. Uniswap spent $2.75 million on these deployments (not including matching amounts in the protocol), while the annualized fees for these deployments were $310,000. Even if fees were converted to recover costs (assuming a 15% share), the DAO would only earn about $46,500 annually, equivalent to a 1.7% return rate, and it would take 59 years to break even.

The area between the two dashed lines represents the incentive activity period, showing that almost all liquidity pools experienced a cliff-like drop after the activities ended.

Of course, some members noted that while there is generally a cliff-like drop in liquidity after incentives end, this incentive plan remains the most effective strategy. Member "alicecorsini" referenced data from Forse Analytics regarding the challenges of retaining users, liquidity, and trading volume after incentives end for Uniswap v3 on Base.

In the case of Base, Uniswap's biggest competitor is Aerodrome, and the data presents a more complex situation. 27.8% of Uniswap's incentivized LPs provided liquidity to Aerodrome after the incentives ended, with 84.5% completely leaving Uniswap, and about 64.8% of users who left Uniswap did not turn to Aerodrome, even though they had better APR than the non-incentivized Uniswap v3.

While some LPs shifted to Aerodrome, a larger proportion of users simply exited without turning to direct competitors. This indicates broader structural challenges in retaining users and liquidity. He believes that brainstorming methods to improve retention "simultaneously" while deploying incentives is a worthwhile effort, but this incentive plan remains the most effective strategy for the first step in the traffic funnel.

Community Doubts About Gauntlet's Capabilities

Community member Pepo "@0xPEPO" expressed concerns about Gauntlet on social media X, pointing out that the Uniswap Foundation had already paid $1.2 million and $1.25 million in participation fees to Aera and Gauntlet, respectively, even before the proposal was approved. However, there is a lack of performance records to demonstrate whether the Aera team can complete such a project.

He mentioned that Peteris Erins, the Uniswap Growth Manager designated by Gauntlet, was the founder of Auditless and a member of the Aera team. However, apart from his work at Aera, Peteris has almost no public performance records. The only notable public achievement is that his protocol achieved over $80 million in TVL in its first year.

However, he believes this total locked value may not reflect genuine performance, as every client of Aera is also a client of Gauntlet. When a company's performance relies on its parent company, the growth data becomes questionable. He further cited data from Aave and Gauntlet, indicating that Gauntlet may have been suppressing growth, as Aave's TVL and profitability significantly improved after parting ways with Gauntlet.

In response, Devin Walsh, the Executive Director and Co-founder of the Uniswap Foundation, stated that Gauntlet underwent a more rigorous review than typical collaborators and has gone through two due diligence processes.

The first was in early 2023 when they were selecting a consultant for incentive analysis. To choose a vendor, they provided similar proposals to three potential collaborators and evaluated the final results based on the rigor, comprehensiveness of the analysis, and the ability to drive execution after analysis. At that time, Gauntlet's results far exceeded those of other companies. The second review occurred in the third quarter of 2024, where the foundation evaluated a batch of candidates to determine who was best suited to collaborate on the incentive activities for Uniswap v4 and Unichain. They assessed the candidates' past records, relevant experience, and ability to achieve expected outcomes. Based on the analysis, they believed Gauntlet was best suited for the task. Meanwhile, they took this opportunity to renegotiate the contract, which is now planned to be paid per activity, with the rate locked until 2027.

Recurring Security Issues with USDT0's Underlying Technology Layer0

Before the activity began, analyst Todd "0x_Todd" pointed out security risks associated with USDT0 on social media X. USDT0 is the cross-chain version of USDT, with the parent asset USDT existing on ETH and crossing to other chains via Layer0, becoming USDT0. Chains supporting USDT0 can also cross-chain with each other, such as ETH-Arb-Unichain-BearChain-megaETH, etc.

USDT0 is led by Everdawn Labs, utilizing Layer0's underlying technology and backed by Tether and INK. Todd expressed trust issues with Layer0, stating, "My trust in Layer0 is limited, and there have been numerous cases of top cross-chain bridges failing, from multichain to thorchai; cross-chain technology has no barriers, it's just multi-signature."

Given the current situation, in addition to bearing the risks of Tether and Uniswap, there are four additional risks to consider: the security of Everdawn, the security of Layer0, the security of Unichain, and the security of other public chains supporting USDT0. If other public chains are hacked, USDT0 could be infinitely minted, which would also contaminate Unichain's USDT0.

How Can Users Take Advantage?

Visit Merkl to check the incentive pools; these incentive mechanisms may increase or decrease over time. If you want to efficiently mine $UNI, you need to keep an eye on the reward changes in the 12 pools.

Providing liquidity to these pools can be done from any interface, allowing you to earn liquidity activity rewards.

Users can claim rewards through the Merkl interface or any interface connected to the Merkl API.

Overall, most community users are not optimistic about this proposal. They believe it poses risks to the rights of $UNI holders in various aspects. However, for retail investors simply looking to mine $UNI, they need to be cautious of the potential risks and pay attention to the bi-weekly changes in liquidity pool rewards. We will continue to follow up on any potential developments.