Blockin.ai: There are gold mines in the small pools of Uniswap V3, and LPs showcase their skills on the road to gold mining

LP mining in small and medium-sized liquidity pools is partly due to the higher fees brought by the scarcity of liquidity in these pools, and partly because they are optimistic about the small tokens in this trading pair, using high fees to reduce the risks brought by price volatility, or utilizing the "grid" model of the AMM curve for automatic high-selling and low-buying actions.

LP mining in small and medium-sized liquidity pools is partly due to the higher fees brought by the scarcity of liquidity in these pools, and partly because they are optimistic about the small tokens in this trading pair, using high fees to reduce the risks brought by price volatility, or utilizing the "grid" model of the AMM curve for automatic high-selling and low-buying actions.Author: Blockin.ai

In the previous article, we mentioned that most LPs in the Uni-V3 protocol experience long-term losses in USD terms, but we still found some liquidity pools with good profitability. We speculate that these types of pools are usually not dual stablecoin pools or pools with large locked amounts. This is because the prices of dual-token pools are more stable and carry lower holding risks, while higher liquidity in these pools leads to lower average fees.

We believe that LPs mining in small to medium-sized pools do so partly because these pools offer higher fees due to liquidity scarcity, and partly because they are optimistic about the smaller tokens in these pairs, using high fees to reduce the risks associated with price volatility, or employing the "grid" model of AMM curves for automatic high-selling and low-buying actions, which can be seen as a disguised form of speculation. Additionally, institutions will provide substantial liquidity for their native utility tokens and stablecoin pools to enhance market liquidity.

To validate this viewpoint, we first analyze from the perspective of pure mining returns. Taking July 2022 as an example, we found that the distribution of LP mining yields in pools does not simply follow a normal distribution, and the kurtosis values of different pools vary significantly. Kurtosis reflects the sharpness of a distribution's peak; when kurtosis is greater than 3, the distribution exhibits a steeper peak than a normal distribution. When the mining yield of LPs in a pool does not present a normal distribution, it indicates that LP returns are often heavily influenced by their strategies, with only a small portion of LPs able to achieve high mining yields. In short, competition for fees within the pool is more intense, making it more "competitive." From the largest TVL pools, WBTC-WETH 0.05% is the most "competitive," followed by USDC-WETH 1.0%, USDC-WETH 0.3%, and USDC-WETH 0.05%.

Based on the hourly profit and loss situation of all positions in Uniswap V3, we compiled the monthly profit and loss of each pool from May 2021 to November 2022. From the distribution of annualized returns for each month, we found that there is clustering in the returns of different months, such as in August 2021, October 2021, and July 2022, where the overall distribution was relatively high.

In pools with insufficient liquidity, the price may be artificially inflated due to the influence of initial liquidity providers and may not be genuinely liquid. Therefore, we selected pools with an average daily locked amount greater than $1 million for analysis (see Appendix 1). Among the top three pools by monthly yield, we found that only 5 pools had an average daily locked amount greater than $10 million, with Nvir-WETH 0.3% having the highest average daily locked amount of $77.76 million in March 2022, confirming the hypothesis that the highest-yielding pools are often small to medium-sized pools.

From the perspective of fee income, there are 35 records where the annualized fee yield exceeds 100%, and 22 records where the annualized fee yield exceeds 300%. However, there are only 21 records where the fee yield accounts for more than 50% of the net yield, while 27 records have fee yields below 20% of the net yield. This indicates that although the overall fee yield of these pools is relatively high, the positive impermanent loss caused by actual price increases is the most significant factor affecting net returns.

Additionally, it is not difficult to find that 95% of the pools in the list contain WETH or stablecoins USDC, USDT, DAI, FEI, with WETH-LUNA 1.0% and KROM-WETH 0.3% being the two most frequently appearing pools, each appearing three times. Similarly, we plotted the distribution of mining yields in the pools with the highest net yields in July 2022, showing that, except for MM-USDC 1.0%, the kurtosis values of other pools are generally not high compared to large pools, reflecting that LPs can more easily achieve high returns from some promising small to medium-sized pools.

In the crypto space, we have witnessed many tokens suddenly surge and quickly plummet, including the decoupling of the largest algorithmic stablecoin UST from the dollar and the LUNA crash. LPs hold a wait-and-see attitude toward the future of certain tokens; for them, directly holding tokens they are uncertain about in the long term carries significant risks. At this time, the AMM "grid" model becomes a disguised form of speculation, helping them actively sell small tokens for Ethereum or stablecoins when their prices rise, while the high fees from small pools partially offset the impermanent losses from price declines, making the market-making risk far lower than simple holding risks.

Among these high-yield pools, we discovered some "smart addresses." Taking the operations of a certain LP (0x7bbe7140e8f62404d320c87fa1655f69b2cb2f26) in the FXS-WETH 1.0% pool as an example, after WETH and FXS experienced a decline in April and May 2022, the price began to stabilize in June. This address started injecting positions at the end of June 2022, with a strategy of maintaining a neutral range within a single position, setting the range width at approximately 5%-20% above and below the current price. When the price falls below the lower limit or rises above the upper limit, it swaps positions, and the width of the next position references the price fluctuations over the past period. This indicates that the LP does not have a clear inclination toward the future price trend and volatility but is optimistic about this token pair over a certain period.

We used the net value of the first injected funds as the initial principal and plotted the unit net value trend of this LP under its strategy, as well as the net value trend of holding two tokens equally with the initial principal. We found that this strategy significantly outperformed the holding strategy, with the total net value in the latest pool reaching 1.6 times the initial amount, while the net value of the holding strategy remained roughly the same as the initial amount.

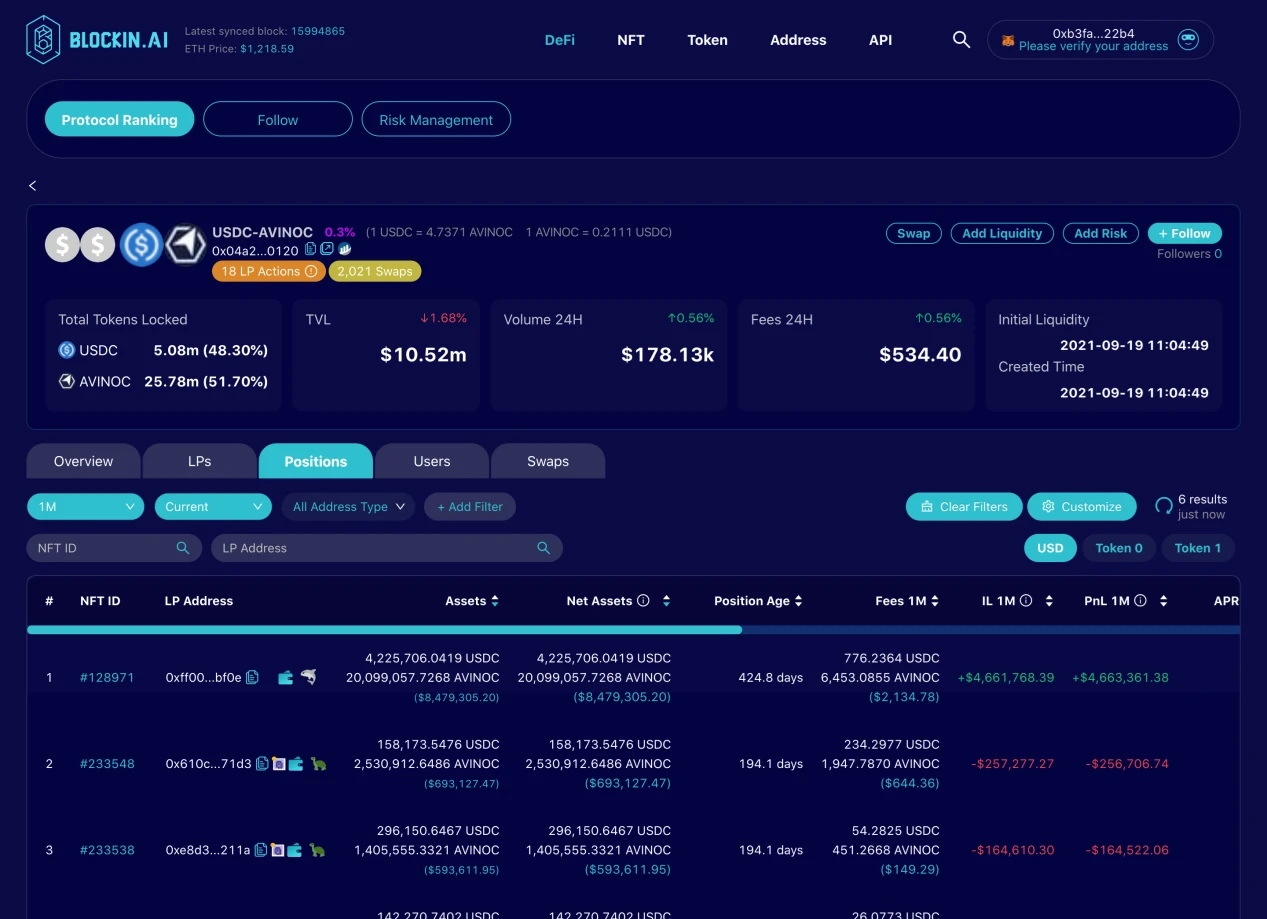

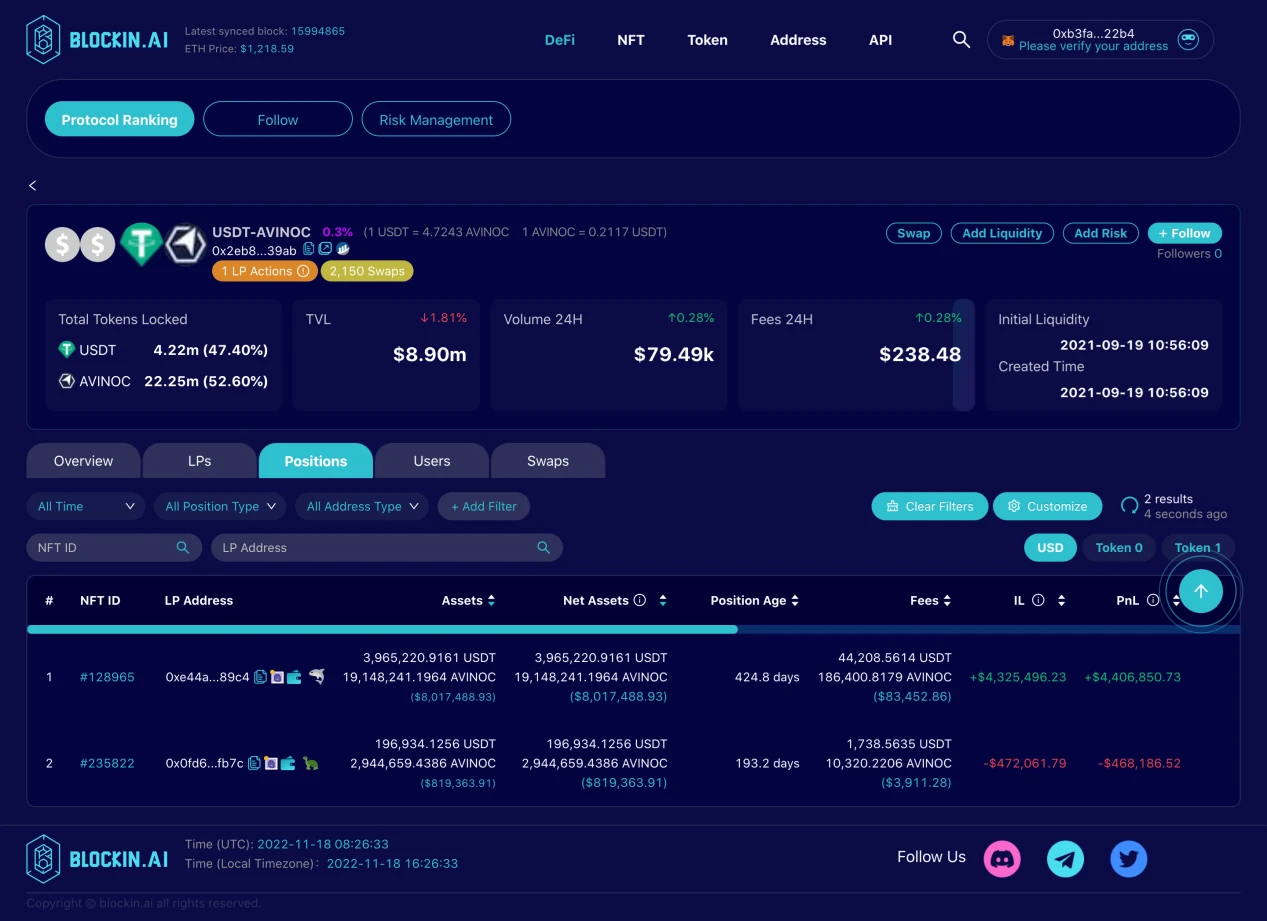

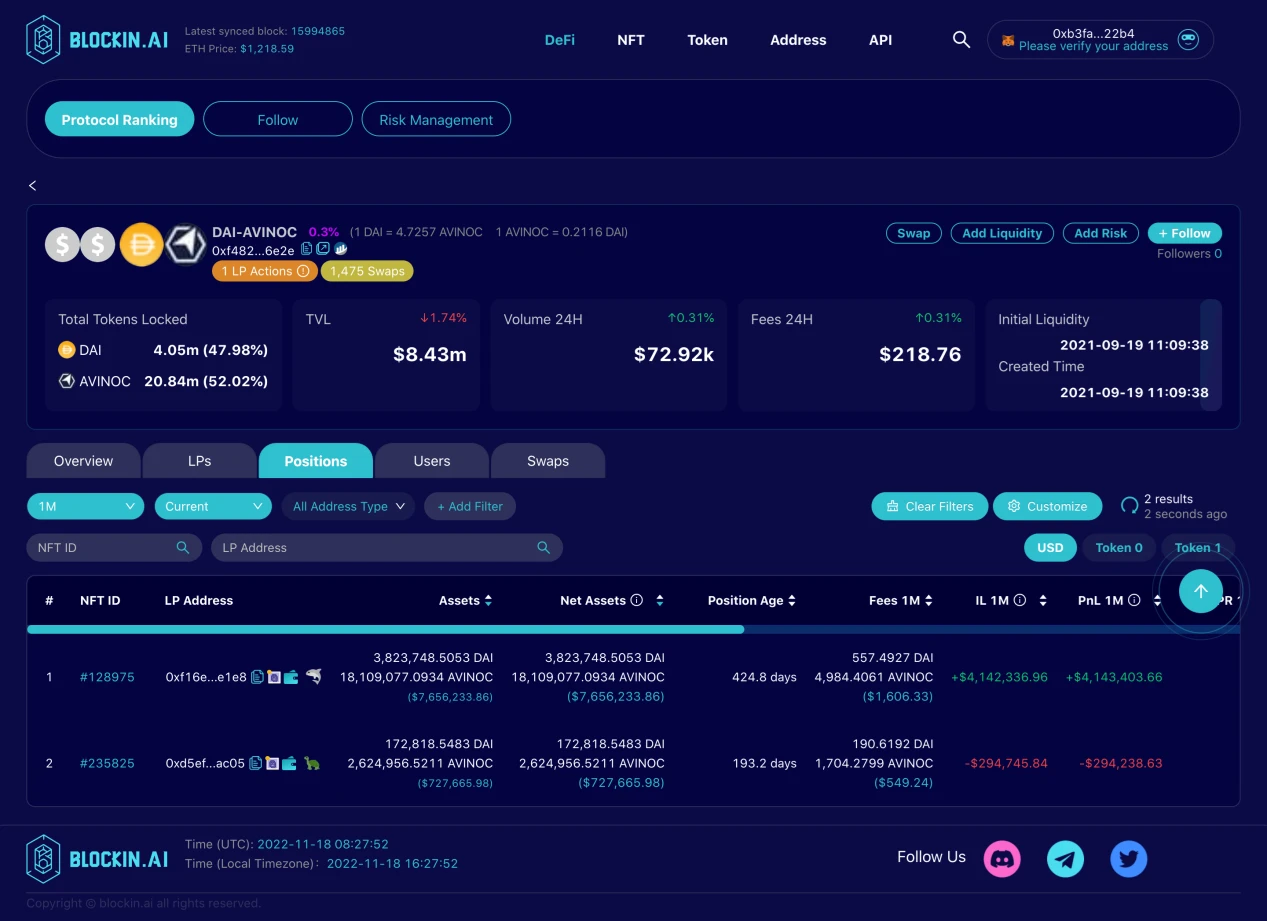

From the top ten pools ranked by monthly yield with positive net yields, we found that besides large tokens paired with smaller tokens, such as WETH and stablecoins, tokens like AVINOC, SHIB, and APE appeared frequently in the rankings, with some small tokens resembling the situation of LUNA. We also observed monopolistic phenomena in some small pools, such as the three largest pools related to AVINOC, which are suspected to be operated by the same institution (see Appendix 2). This institution may be the issuer of AVINOC, and some institutions can quickly circulate small tokens by providing substantial liquidity, thereby driving up token prices.

Appendix:

Appendix 1

Appendix 2