A clarification of the entanglement between Solana and FTX, and how far Solana can go

After the collapse of FTX, Solana was immediately placed at the center of the storm, which can be traced back to the DeFi summer of 2020.

After the collapse of FTX, Solana was immediately placed at the center of the storm, which can be traced back to the DeFi summer of 2020.*Original source: **R3PO, *"How far can Solana go? A comprehensive overview of the Solana and FTX entanglement"*

Since the collapse of FTX, the aftershocks have yet to subside. Once considered an Ethereum killer, Solana has also been dragged into the abyss. The simultaneous collapse of Terra and LUNA is understandable, but what ties do the seemingly independent projects FTX and Solana have? How did Solana end up in such a predicament? What consequences will the significant depreciation of SOL bring to Solana? Can this self-proclaimed "highest performance blockchain in the world" survive the storm? R3PO attempts to answer these questions from the perspective of the Solana project itself, while also reflecting on the lessons learned from the FTX incident alongside the web3 industry.

Why Solana?

After the collapse of FTX, Solana was immediately placed at the center of the storm, which can be traced back to the DeFi summer of 2020. At that time, Solana was still relatively unknown, just one of many public chains attempting to solve the "impossible triangle." However, FTX co-founder and CEO, Alameda Research founder SBF (Sam Bankman-Fried), discovered Solana. In addition to participating in multiple rounds of financing for Solana, he chose to build the decentralized trading platform Serum on Solana (the first decentralized trading platform on Solana) and subsequently invested in several Solana-based applications, such as offline maps Maps.me, wholesale broker Oxygen, Bonfida which fully utilizes Solana's potential, and Raydium which integrates AMM/mining/IDO functionalities.

This substantial financial endorsement led many to associate SBF with Solana, and early on, some even mistakenly believed he was the founder of Solana. The large number of tokens held mutually by FTX, Alameda, and Solana caused SOL to plummet on November 9, the day FTX collapsed, with its price halving directly.

*SOL price trend over the past month, * CoinMarketCap

To some extent, the intermingling of FTX, Alameda, and Solana is second only to the symbiotic relationship between Terra and LUNA. Thus, when FTX collapsed, it was akin to announcing the downfall of the financial backers behind Solana, making it natural for attention to shift towards Solana, and the resulting collapse was not hard to foresee.

Especially since Serum, as one of the cornerstones of Solana's DeFi infrastructure, brought not speed and low costs after the FTX collapse, but embarrassment and skepticism, quickly heading towards ineffectiveness and disintegration. On November 13, due to concerns that Serum may have been compromised in FTX's hacking incident, Solana developers urgently forked the FTX-developed DEX Serum. The forked version, OpenBook, quickly launched on the Solana mainnet, with daily trading volume exceeding $1 million, while Serum's trading volume and liquidity had dropped to nearly zero.

Amid the spread of negative sentiment, the funds in the Solana DeFi ecosystem are significantly decreasing. According to DefiLlama data, the total locked value (TVL) in Solana DeFi has plummeted to $280 million (as of the time of writing), far below the levels seen during the significant downturn in the cryptocurrency market in June 2021.

Total locked value in Solana DeFi, DefiLlama

On one side, the DeFi ecosystem is in crisis, while on the other, the NFT ecosystem is facing a sell-off. According to Forbes, the FTX collapse is destroying the Solana NFT ecosystem and triggering a wave of sell-offs. Public data shows that the NFT trading volume on Solana's NFT markets Magic Eden, OpenSea, and Solanart has more than doubled from over 80,000 NFTs daily a week ago, peaking at over 250,000 NFTs, indicating that holders are rapidly selling off their NFTs.

With other new public chains closing in and being caught up in the massive storm of FTX, does Solana still have room for a comeback?

What is Solana?

To answer the above questions, we first need to clarify what Solana is and what its value is.

Solana is a public blockchain co-founded by Anatoly Yakovenko and two former Qualcomm colleagues, Greg Fitzgerald and Stephen Akridge. The solid technical background of the three founders gave investors and the market greater confidence. The founding intention stemmed from a technical response to the blockchain "impossible triangle." Solana attempts to enhance scalability through a new blockchain architecture based on Proof of History (PoH), positioning itself as the fastest high-performance public chain in the world. According to its white paper, PoH is used on Solana to encode untrusted passage of time into the ledger—a data structure that is merely appended. When used alongside consensus algorithms like Proof of Work (PoW) or Proof of Stake (PoS), PoH can reduce messaging overhead in Byzantine fault-tolerant replicated state machines, achieving sub-second confirmation times. Solana also proposed two algorithms that leverage the time-keeping properties of the PoH ledger—a PoS algorithm that can recover from partitions of any size and an efficient proof of replication (PoRep). The combination of PoRep and PoH provides defenses against ledger forgery in terms of time (ordering) and storage. Theoretically, Solana can achieve 710,000 transactions per second (TPS) on a standard 1Gbps network.

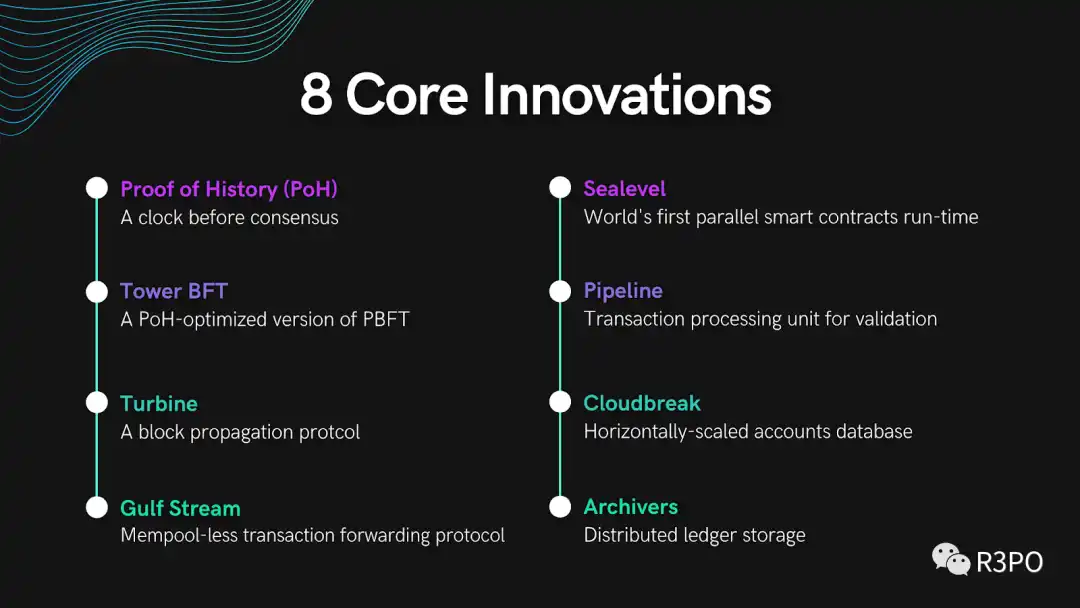

Moreover, Solana's eight core innovative technologies create the possibility for its high performance and low costs.

The eight core innovations of Solana, The Tie

Solana supports the creation of smart contracts, Dapps, DeFi platforms, and NFT markets. To some extent, Solana has indeed realized Anatoly's original intention of building a high-performance blockchain network with low fees and high TPS that can accommodate many projects. Solana achieves massive scalability without sharding, allowing applications to be freely combined on a complete layer network. In contrast, Ethereum, which long relied on a resource-intensive PoW governance system before the merge, has already been overwhelmed. Prepared for a long time, Solana provided a low-cost and fast migration public chain through the Ethereum bridge—the Wormhole protocol—allowing many quality projects and active users to migrate to Solana without needing to rewrite contracts.

Additionally, Solana also possesses "predictability," which is a burden-free programming model: developers know that once they write the code, it will always work, and the cost of executing the code in the future will be lower than it is now. This provides developers and project teams with enough confidence to develop and maintain their projects long-term.

In summary, Solana's advantages complement Ethereum's shortcomings, providing developers and project teams in the market with an attractive and stable option. Based on this, Solana has begun to vigorously build its ecosystem.

As a blockchain infrastructure, Solana has gained recognition from many applications. For example, the Solana ecosystem project Francium pointed out "three reasons to develop DeFi on Solana":

· The underlying public chain has advantages such as low transaction costs, long-term scalability, higher network value, and decentralization;

· Stateless execution of transactions enables large-scale parallel programming;

· The ecosystem is developing rapidly, has initially taken shape, and provides a foundation for building composable Lego blocks.

Solana is not satisfied with this; it has established a long-term effective ecosystem support plan (Grants), continuously holds hackathons with high rewards, and promotes community exchanges through the Breakpoint conference. Solana has also formed multiple ecosystem funds and creator funds in collaboration with well-known companies in the industry, providing tangible financial support to encourage project development. The influx of new projects, highly active users and developers, and ample financial backing have formed a prosperous ecosystem for Solana.

Additionally, Solana has issued its native cryptocurrency SOL, which uses a delegated PoS consensus algorithm. Miners delegate SOL to validators to participate in maintaining the network and earn rewards. SOL is used to pay transaction fees on the network, for staking, and governance. The token mechanism sets its initial inflation rate at 15%, which decreases by 15% each year until it stabilizes at a long-term rate (1%-2%). This token mechanism allows for rapid growth in the supply of SOL in the early stages, with later supply stabilizing.

Where is Solana headed?

The direct impact of the FTX incident on Solana has gradually reached a bottom. According to information from Solana's official website, the Solana network did not encounter any significant performance or uptime issues during the FTX incident. At the same time, the Solana Foundation clarified the recent SOL token unlocking event that caused community panic, stating that this is a normal event that occurs every two to three days, where token holders can request to unstake at the end of each epoch. The current large-scale unlocking is actually from about 29 million SOL from 250 addresses that canceled their unstaking at the end of Epoch 370, while it was originally expected that a total of 63 million SOL would be unstaked at the end of Epoch 370. However, the 28.5 million SOL that the Solana Foundation originally delegated for unstaking has been delayed, and its unstaking will take effect shortly.

Although this is bad news, another shoe has dropped. According to the Sollet interface announcement, soBTC issued by FTX or Alameda on Solana has been confirmed as non-redeemable. Solana Compass also stated that the 48,636,772 SOL tokens previously controlled by Alameda are now held by the liquidator and are unlikely to be sold for nearly a decade.

Solana Foundation's balance sheet exposure to FTX/Alameda risks

· According to Solana's official website, the Solana Foundation has about $1 million in cash or cash equivalents on FTX.com, which had stopped processing withdrawals at that time. This is less than 1% of the Solana Foundation's cash or cash equivalents, so the impact on the Solana Foundation's operations can be considered negligible.

· The Solana Foundation does not have SOL held on FTX.com.

Solana Foundation's asset exposure to FTX/Alameda

· According to Solana's official website, its assets in the FTX.com account include (as of November 6, when FTX.com stopped processing withdrawals): approximately 3.24 million shares of FTX Trading LTD common stock, about 3.43 million FTT tokens, and approximately 134.54 million SRM tokens, with the latter two having risk exposures of $75.46 million and $107.6 million, respectively.

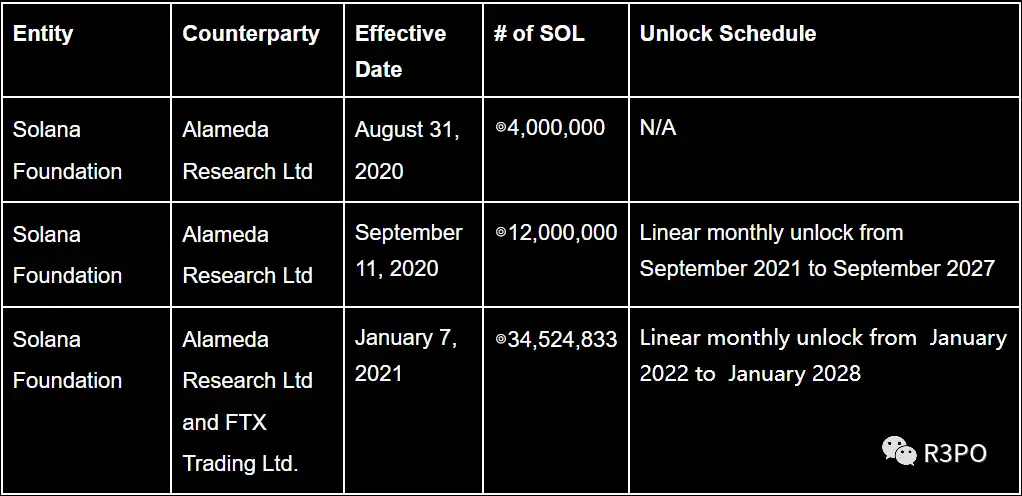

Summary of SOL sales by Solana Foundation to FTX/Alameda

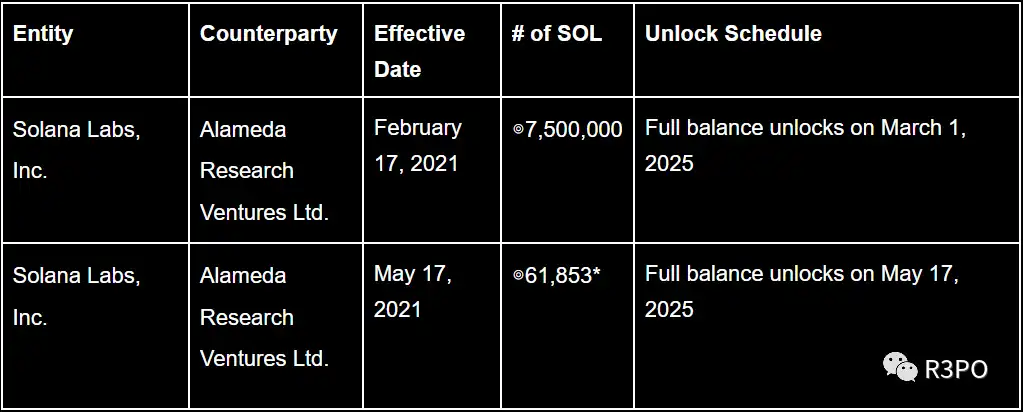

Summary of SOL sales by SolanaLabs, Inc to FTX/Alameda

According to Solana's official website, the total exposure value of assets based on Sollet that are affected by the Sollet custody bridge is approximately $40 million, with the status of the underlying assets currently unknown.

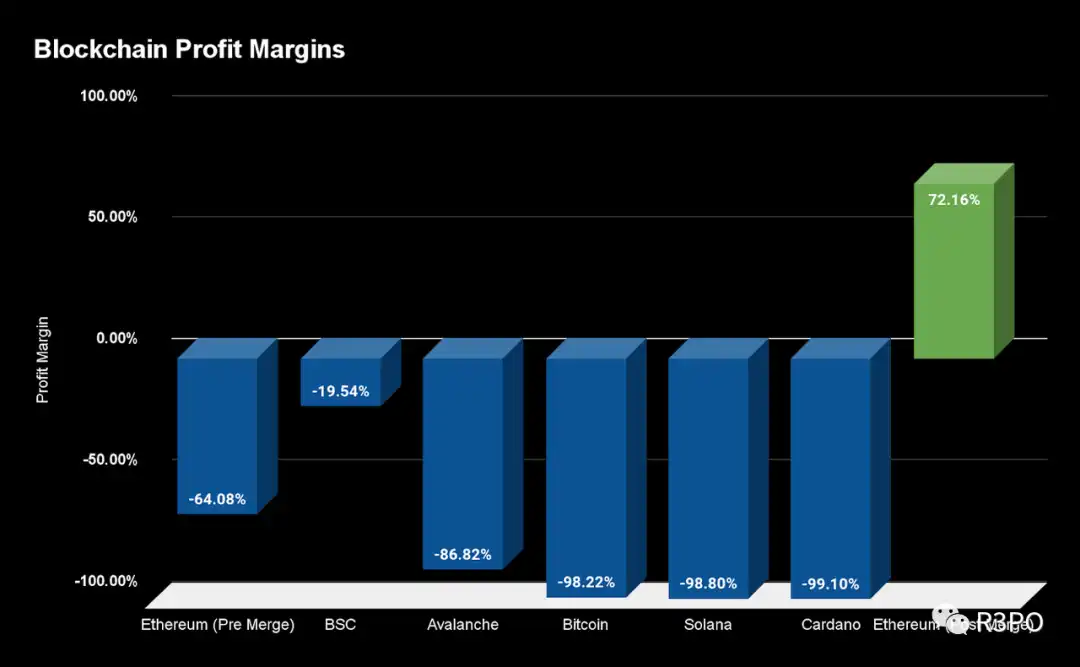

Although the risk exposure has been clarified, the aftershocks of the FTX incident have not yet ended, and the price of SOL has not yet bottomed out. Particularly for Solana, even without the FTX incident, it faces many issues, such as fierce competition in the blockchain infrastructure race, entering the market late, lack of substantial commercial content and clear functionality lists, heavy VC allocations, frequent network outages (three times since March 2022), transaction fees being too low to cover costs, and a target customer base that is too narrow. The FTX storm has swept away not only funds but also opportunities and confidence, leaving little time for Solana. How to solidify its fragile foundation is currently a top priority for Solana. Optimistically, from the perspective of the overall blockchain infrastructure race, there is currently no sufficiently excellent product that can completely replace Solana's functions and position in the market. The much-anticipated Aptos mainnet launch has not performed well, failing to successfully take over from Solana, leaving Solana with a glimmer of hope.

Profitability status of various public chains, Bankless

Profitability status of various public chains, Bankless

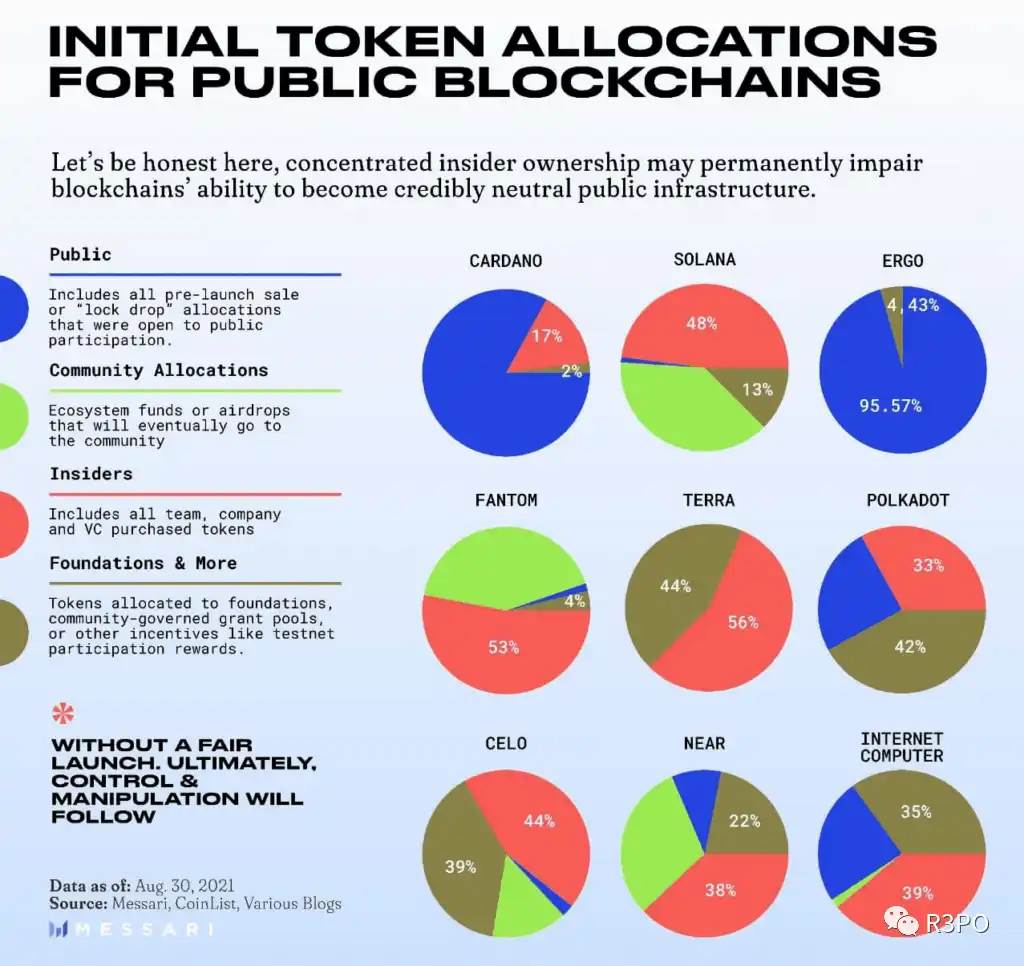

Initial token distribution of various public chains, Merssari

Discussions about Solana on social media are also rampant, but there seems to be a general consensus that Solana's future lies in its ecosystem (if it has a future). Fortunately, this belief exists not only among those within Solana and SOL holders but also among many project teams and developers within the Solana ecosystem. Particularly for NFT projects, Solana is currently the second-largest blockchain after Ethereum, with sales exceeding $1.7 million, more than eight times that of the third-place Cardano. Solana provides a globally scalable tool that can meet the development needs of project teams of various sizes, serving as both a small and beautiful and a large and comprehensive infrastructure development platform, with all tools being open-source and free, allowing participants to create NFT artworks and build communities for free. If Solana were to collapse, it would undoubtedly be something NFT project developers do not wish to see.

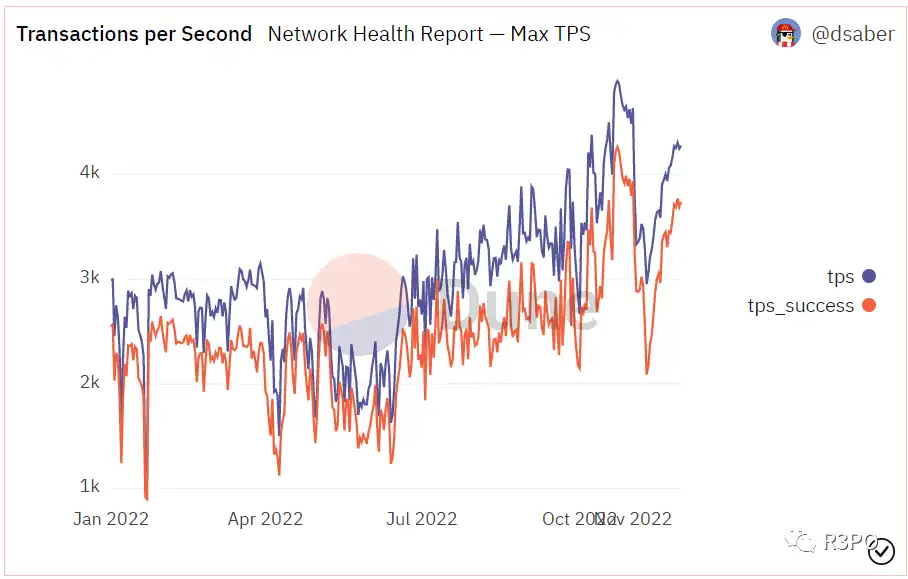

Some technical data also supports that Solana is currently on a development trajectory, with the maximum transaction volume (TPS) continuing to grow since the beginning of the year. Although it was temporarily affected by the FTX incident, it quickly resumed an upward trend.

Solana TPS from January 2022 to present, Dune@Dsaber

In its report released in October, Solana addressed some existing issues through technical transformations aimed at solving current network stability problems, increasing revenue without raising transaction fees, and expanding the user base:

Applying QUIC on the mainnet test version:

QUIC is a protocol built by Google designed for fast asynchronous communication. This is an improvement over the existing UDP-based protocol, which Solana previously used to transmit transactions between RPC nodes and the current block leader. UDP lacks flow control and receipt confirmation, so it failed to provide a meaningful way to prevent or reduce abuse. To address this issue, Solana's transaction ingestion protocol is being re-implemented on top of QUIC, which can control sessions and traffic and is currently running on the testnet and mainnet test version. However, the mainnet test version still supports both UDP and QUIC. QUIC is planned to become the default transaction ingestion and forwarding protocol on the mainnet testnet. Once adopted, there will be more options available to optimize data ingestion and prevent abuse.

Increasing transaction size:

Transactions on the Solana network are currently limited to a maximum of 1,232 bytes. This limitation restricts the ability of programs to combine with each other. With the implementation of QUIC, the possibility of increasing transaction size is within reach.

Stake-weighted Quality-of-Service (QoS):

This is being built in parallel with QUIC and will be enabled before QUIC is adopted on the mainnet testnet. Currently, block producers accept transactions without considering their source. Solana is a proof-of-stake network, and stake-weighted QoS will extend the utility of stake-weighting to transaction quality. In this model, a node with 0.5% stake will have the right to transmit at least 0.5% of the packets to the leader. Regardless of the traffic from nodes without stake, transactions submitted by validators with stake in the network will always be accepted by block producers.

Fee market:

The fee market has been partially introduced and is expected to be further implemented after QUIC is fully adopted. The first part of the fee market implementation is to support priority fees. Previously, the network processed transactions on a first-come, first-served basis, which did not allow users any way to express the urgency of transaction execution. Priority fees changed this by allowing users to decide to pay extra fees when executing transactions and including them in blocks. Priority fees are calculated based on the estimated computational resources required for the transaction. For example, a simple token transfer requires a lower total priority fee compared to an NFT mint with the same urgency. Since July 2022, priority fees have been running on the mainnet test version. Future versions will add additional features to the fee market, including new RPC methods that will help users and applications determine the minimum extra fee required to be included in the next block, higher fees for competitive accounts, and improvements in block scheduling. These pending improvements are expected to create a more efficient fee market for all Solana participants.

From an ecosystem perspective, there are currently over 500 ecosystem projects built on Solana, forming an ecosystem that covers eight major areas: DeFi, NFT, gaming, tools, wallets, dApp applications, and development, with subfields including DEX, derivatives, trading analysis visualization, lending, synthetic assets, and stablecoins. With the support of these large submarkets, Solana still has the confidence to impact the most important infrastructure of Web3.

Solana also revealed that in terms of mobile business, the first-generation Saga developer toolkit will be shipped in December, and the SolanaMobile dApp Store will open in January 2023, with consumer devices set to launch in early 2023. Punching Ethereum and kicking Apple, Solana seems confident about the future.

Conclusion

Solana rose due to SBF and stumbled because of SBF. R3PO believes that throughout this process, Solana itself has not encountered serious issues. When it met SBF, it gained his full support due to its own strength, and SBF's downfall may have given Solana an opportunity to prove itself. In the public chain race, Solana's characteristics, advantages, and functions are currently irreplaceable, but opportunity windows are often fleeting. Whether Solana can seize this opportunity and achieve success remains to be seen. R3PO believes that Solana's urgent task is to solidify its foundation, resolve its outage issues and profitability problems, rather than recklessly leading the market, as the tender shoots sprouting in winter face not only sunshine but also frost.

References:

Reference 1, Reference 2, Reference 3, Reference 4, Reference 5, Reference 6, Reference 7, Reference 8, Reference 9, Reference 10, Reference 11, Reference 12