Chapter 11: NFTs and DeFi

Fragmentation enables the financialization of NFTs, thereby enhancing their accessibility, liquidity, and fungibility. It demonstrates how the utility of NFTs transcends the stereotypical associations with art or collectibles. In fact, NFTs have indeed played a role in the decentralized finance (DeFi) space.

Decentralized finance, or DeFi, is a movement that allows users to utilize financial services such as lending and trading without relying on centralized entities. These financial services are provided through Decentralized Applications (Dapps), most of which are deployed on the Ethereum platform.

The fragmentation of NFTs showcases the integration of DeFi mechanisms within the NFT world, but its impact is not merely a one-way street.

As DeFi has evolved, several projects have begun to explore the combination of NFTs with DeFi products, resulting in a new asset class known as "financial NFTs." Simply put, financial NFTs are NFTs used as financial instruments, but what is the reason behind this?

Why go through the trouble of integrating NFTs into DeFi? If ERC-20 tokens are already performing so well, what is the point? In this chapter, we will explore how financial NFTs enhance the capabilities and efficiency of DeFi products. The examples we will introduce are Uniswap, Solv Protocol, and Charged Particles.

Uniswap

To fully understand Uniswap, we must first grasp the core concepts of Uniswap V2 and Uniswap V3.

Uniswap V2

Uniswap V2 is an automated market maker (AMM) that allows the creation of any ERC20-ERC20 liquidity pool, which is essentially completely fungible. For example, in the DAI/USDC pool, DAI and USDC are evenly distributed along the x*y=k price curve, covering all prices from $0 to infinity.

Source: https://www.coindesk.com/business/2021/02/04/what-is-uniswap-a-completebeginners-guide/

This means that most assets in most liquidity pools are never utilized unless their respective prices turn extreme. According to Uniswap, the V2 trading pair of DAI/USDC only reserves about 0.50%. The swap capital is concentrated between $0.99 and $1.01, which is the price range where most trades typically occur in stable pools.

While Uniswap V2 is revolutionary, we can observe some issues:

Low capital efficiency - Most of the liquidity provided by liquidity providers (about 99.5% in the above DAI/USDC example) is not utilized.

High slippage - Due to the dispersion of funds across all prices and the lack of liquidity at specific prices, users have to pay high prices when purchasing tokens.

Low fee earnings - Liquidity providers (LPs) only earn fees on a small portion of the funds they provide, which is insufficient to offset the impermanent loss (IL) risk they bear.

Uniswap V3

Uniswap V3 was launched in May 2021, introducing new features and improvements. In this chapter, we will focus on the key implications of Uniswap V3 introducing non-fungible liquidity pools. This fundamental change helps address the shortcomings of Uniswap V2 and serves as an interesting example of the role NFTs play in the core design of DeFi products.

Unlike Uniswap V2, liquidity providers in Uniswap V3 can concentrate their liquidity within custom price ranges. As shown in the figure below, liquidity is not distributed across all prices in the ETH/USDC pool; instead, the LP can choose to allocate their capital within a price range of $250 to $12,000.

Source: https://uniswap.org/blog/uniswap-v3/

What the LP essentially does is create their own personalized liquidity pool that only covers the range between $250 and $12,000. The collective liquidity of all liquidity providers will constitute the ETH/USDC pool. Interestingly, this also means that theoretically, there could be price ranges in a completely illiquid Uniswap V3 pool.

If the above LP provided liquidity to Uniswap V2, their share in the ETH/USDC pool would be represented by a fungible Uniswap-ETH-USD-LP token, but this is not the case in Uniswap V3.

In addition to "quantity," Uniswap V3 also requires consideration of an additional dimension of "liquidity concentration." For example, two liquidity providers may add $100 to the ETH/USDC pool, but their choices regarding the allocation of liquidity within the price range could be very different.

In this sense, their liquidity is non-fungible and therefore non-replaceable. This is where NFTs come into play, as non-fungible ERC-721 tokens are better suited to represent the unique positions of the two LPs.

Thus, Uniswap V3 successfully leverages NFTs effectively in the DeFi space, resulting in:

Improved capital efficiency - Compared to Uniswap V2, Uniswap V3 requires less capital to generate the same expected fees.

Reduced fee slippage - Due to the liquidity depth in high-volume price ranges.

Higher fee earnings - A higher proportion of deployed funds can be used to generate swap fees.

The other side of this user empowerment is that it also requires a skilled understanding of market knowledge to determine the optimal liquidity conditions, which may be limited to a few financially savvy DeFi users. Compared to becoming an LP in Uniswap V2, becoming an LP in Uniswap V3 has a steeper learning curve, as your fund allocation choices significantly impact the trading fees you may earn and the level of risk you face.

However, this reward mechanism for capital efficiency is a positive sign in the long run. It gives us a glimpse of how NFTs play a key role in nurturing the increasingly complex DeFi space, which is crucial for sustainable growth.

Solv Protocol

Solv Protocol is a DeFi platform that supports the minting and trading of financial NFTs called Solv Vouchers.

Solv Voucher example: 20,520 DODO with a two-year linear vesting period.

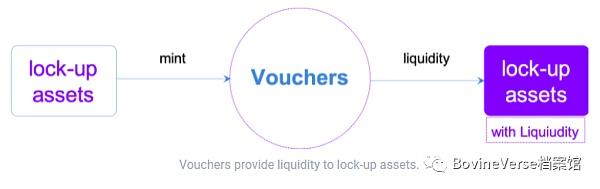

Vesting is the process of locking and releasing tokens after a set period. This helps ensure the long-term commitment of early investors and team members, aligning their financial interests to promote the growth and success of the project.

Through Solv, projects can mint and allocate locked investments to investors in the form of Solv vouchers, granting them rights to any future token liquidity of the associated assets.

Using the above voucher as an example, the allocation of 20,520 DODO is vested linearly over two years, meaning the voucher will unlock for redemption at fixed intervals. For Solv vouchers, linear vesting releases tokens with each Ethereum block, outputting approximately 0.00488 DODO every 15 seconds. Other release methods include one-time releases and phased releases.

Source: https://docs.solv.finance/solv-documentation/

Typically, locked assets lack liquidity, and the only available action is to passively wait for the vesting period to claim these assets. With Solv vouchers, owners of locked assets can now exercise proactive control, including:

Buying and selling vouchers on the Solv market, similar to transferring ownership of established tokens.

Splitting vouchers into smaller parts.

Merging vouchers into larger parts.

This opens up interesting market strategies for vested assets, allowing buyers to enter long-term positions at a discount, while early investors can choose to sell part or all of their vouchers for liquidity.

Interestingly, Solv Protocol has successfully turned around the narrative that "NFTs are illiquid" by innovatively implementing financial NFTs, increasing the liquidity and trading of illiquid, locked homogeneous assets.

But why NFTs?

Essentially, ERC-20 tokens lack the complexity needed to encode certain financial tools. On the other hand, while ERC-721 tokens are suitable for carrying metadata of small penguins, they lack flexibility as they cannot be split or combined.

To circumvent these limitations, Solv Finance had to develop a new token standard called "vNFT," which represents a universal non-fungible token. vNFTs are composed of ERC-20 and ERC-721, allowing Solv vouchers to be encoded with complex vesting contracts, as well as the composability of ERC-20, enabling them to be split or combined.

Charged Particles

Charged Particles can be seen as Russian dolls of NFTs, except that in this case, these dolls do not have to be identical. The protocol allows any token (e.g., ERC-20, ERC-721, ERC-1155) to be deposited into any NFTs. With this, your monkeys and penguins can turn expensive JPEGs into practical NFTs or virtual baskets capable of carrying various digital assets.

This is where things get more interesting. You can also "charge" your NFT by depositing an ERC-20 token supported by Aave, such as DAI. In doing so, DAI will automatically swap into the corresponding aDAI, allowing your NFT to evolve into a yield-generating financial NFT. Then, the accumulated interest can be programmed to "release" to any other wallet - a relative you like, a charity, CoinGecko - it all depends on you.

This innovative approach to treating NFTs paves the way for many new and exciting possibilities. Imagine a loot box (which is itself an NFT) containing a plethora of items, from tokens to LP tokens to other valuable NFTs, which is what Charged Particles has done in collaboration with guilds. This loot box could be embedded into blockchain games as a treasury containing other in-game items, or even reimagined as an album filled with personal music NFTs.

This is just one of the many use cases for Charged Particles; how many more will emerge in the coming months? It is certainly exciting, and we shall see.

So far, Charged Particles only supports NFTs minted on its platform, but in the near future, users will be able to "charge" or deposit digital assets into any NFT.

Project Examples

Aavegotchi

Gotchiverse is an upcoming open social space where players can engage in various activities such as farming, crafting, trading, and battling. Each ghost NFT, called Aavegotchi, requires collateral in the form of Aave's interest-bearing aToken to summon. This means that in addition to serving as avatars in the game, these pixelated ghosts are also financial NFTs that can appreciate over time.

Unvest

Similar to the Solv Protocol, Unvest also facilitates on-chain trading of locked tokens. This is achieved by minting ERC-20 tokens representing vested assets or their versions as financial NFTs called Unvest NFTs.

Revest

Revest can lock ERC-20 tokens within ERC-1155 NFTs. Users can configure the locking mechanism as one of the following: time lock, value lock, and address lock.

NFTfi

NFTfi is the "Aave of NFTs." NFTfi is not a fungible token but facilitates peer-to-peer lending by using NFTs as collateral.

Conclusion

While the application of NFTs in Uniswap V3 revolves around financial utility, financial NFTs such as Solv Vouchers, Charged Particles, and even Aavegotchis also possess the artistic elements typical of NFTs. Therefore, the value of financial NFTs becomes multidimensional and can be summarized through the following aspects:

- The perceived value of their utility (if any).

- Their speculative value based on artwork, design, and rarity.

- The intrinsic value of the underlying assets.

As demonstrated, the use cases for NFTs extend beyond merely tokenizing art and collectibles. The underlying technology also lays the groundwork for the widespread application of financial NFTs in DeFi.

The relationship between NFTs and DeFi is not mutually exclusive. On the contrary, they coexist and reinforce each other. As the crypto ecosystem evolves and flourishes, we may observe more novel combinations and use cases emerging between DeFi and NFTs. The entire ecosystem is still in the experimental phase; what new and exciting breakthroughs will financial NFTs bring? Let’s stay tuned.