iZUMi Research: Curve War New Battlefield, Will Uniswap V3 Be a Better Choice for UST and DAI?

This research report aims to help everyone understand the financial costs that external participants in the Curve War, whose main purpose is to promote the liquidity of their project tokens, need to bear at different levels of the ecosystem.

This research report aims to help everyone understand the financial costs that external participants in the Curve War, whose main purpose is to promote the liquidity of their project tokens, need to bear at different levels of the ecosystem.Author: @0xJamesXXX, iZUMi Research

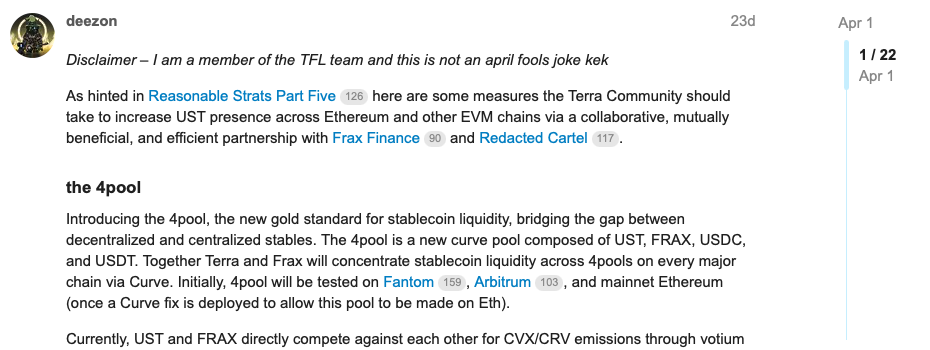

Preface: Terra's 4 Pool Proposal -- The Final Battle of the Curve War?

To broaden the use cases of the UST algorithmic stablecoin across Ethereum and various compatible public chains, and to find new ways to alleviate the high funding costs of providing a 20% annual yield through the Anchor lending protocol, on April 1, 2022, Terra member Zon (@ItsAlwaysZonny) officially launched the 4Pool proposal in the Terra Research Forum, announcing a collaboration with Frax Finance and Redacted Cartel, with Olympus joining shortly after.

The four parties will collaborate to launch a new stablecoin trading pool, 4Pool, on the stablecoin trading platform Curve: USDT, FRAX, USDC, and UST, challenging the existing largest stablecoin trading pool on Curve, 3Crv (USDC, USDT, DAI), thus igniting a new wave of the Curve Ecosystem War. (Supplement: BadgerDAO and TOKEMAK also joined the collaboration of 4Pool on April 10)

Curve, as a decentralized exchange focused on stablecoin and pegged asset trading, utilizes its Stable Assets AMM algorithm. Compared to other DEXs, Curve can provide a lower slippage trading experience under the same liquidity conditions, making it suitable for large-scale stablecoin and pegged asset trading. Additionally, the Curve platform offers CRV tokens as liquidity mining rewards to incentivize liquidity providers to enhance the liquidity depth of its various trading pools.

However, the CRV token rewards for different trading pools need to be determined through platform governance and voting with the yield-bearing token veCRV. Users must lock CRV to obtain veCRV, after which they can vote for the supported trading pools to increase their CRV liquidity mining rewards, thereby attracting more liquidity. Consequently, many stable asset projects choose to accumulate veCRV to compete for liquidity incentives on the Curve platform, leading to the emergence of the Curve War.

Convex is a DeFi protocol built on Curve's veTokenomics. The goal of Convex is simple: to absorb as many CRV tokens as possible and lock them to obtain veCRV, thereby influencing the release of CRV liquidity incentives. Users will receive an equivalent amount of cvxCRV tokens to release the liquidity of their locked CRV tokens and earn Convex's platform token CVX as an additional reward.

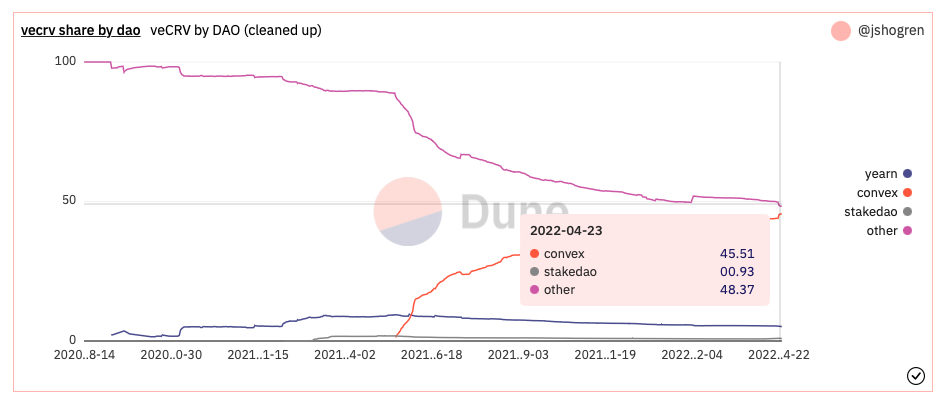

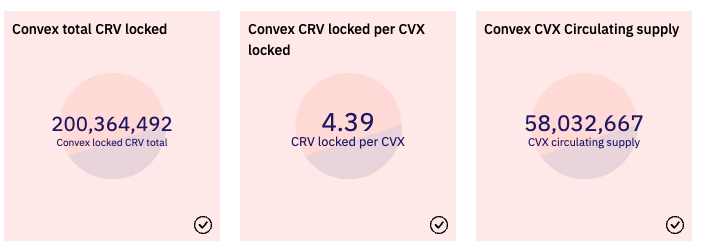

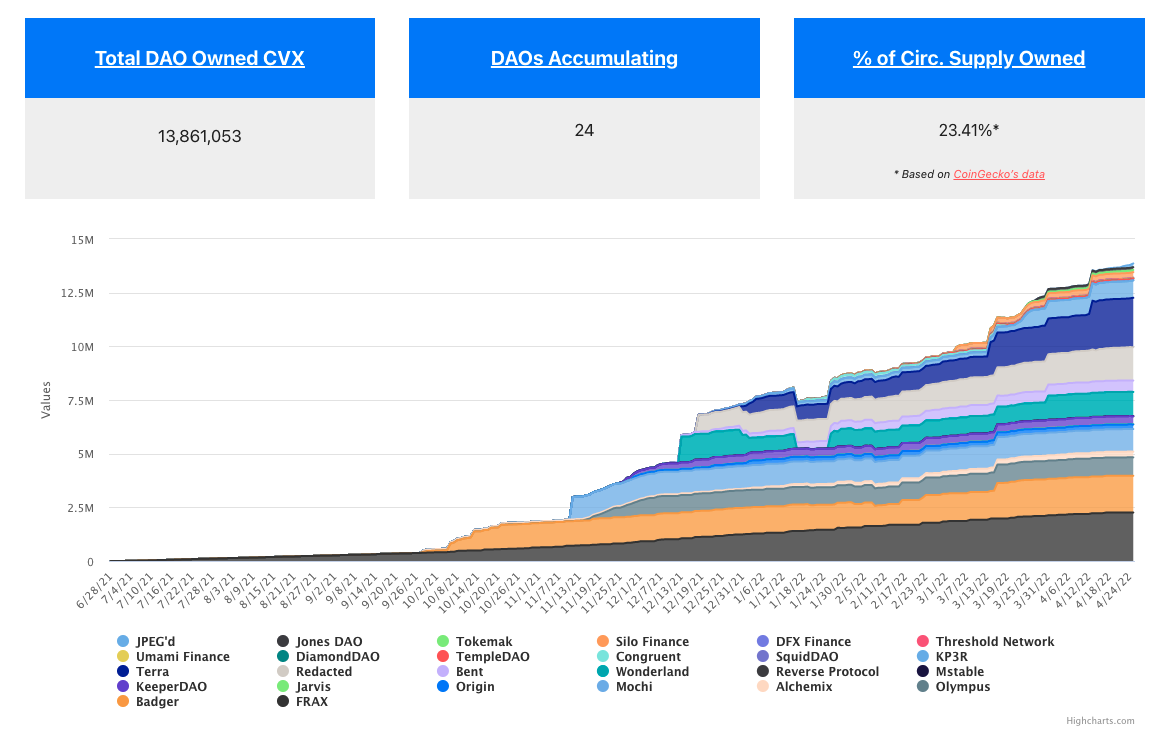

By helping users release veCRV liquidity, Convex has accumulated a large amount of veCRV, currently reaching 45% of the total veCRV supply. Convex also employs veTokenomics, requiring users to lock CVX to obtain vlCVX for voting to guide the veCRV voting rights acquired by the Convex protocol. Therefore, at a higher level, control over Convex is equivalent to control over Curve, making Convex a new battleground in the Curve War, with different protocols competing for control of CVX, including the initiators of 4Pool: Terra, Frax, and Redacted.

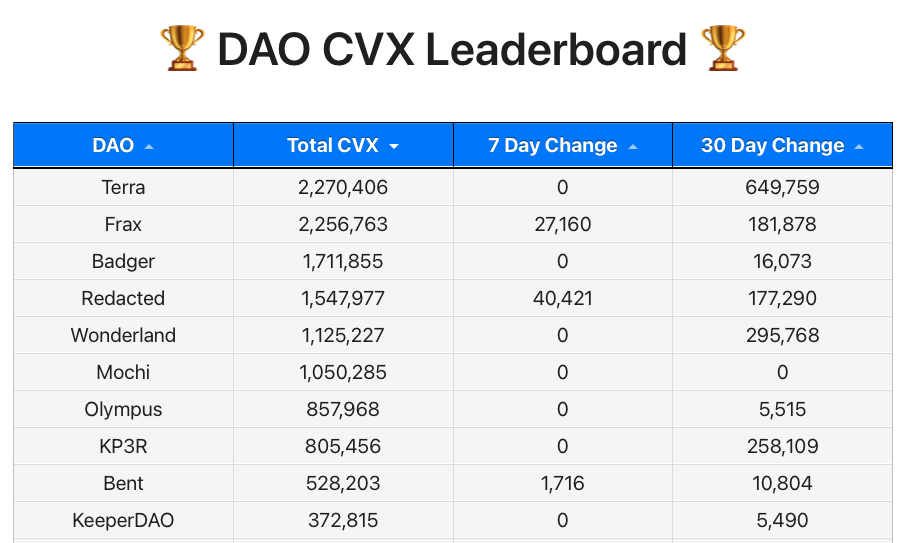

(Top 10 CVX Holding DAO)

Although the four initiators of 4Pool currently control approximately 6.9M CVX tokens, accounting for 50.3% of the total CVX held by the DAO (approximately 13.7M), the founder of Terra declared the end of the Curve War on Twitter by stating they control 50%. However, in reality, they only control 15% of the total vlCVX supply (45.9M). To gain control over Convex, Terra and Frax chose to bribe CVX holders through the Votium platform, but this requires a significant financial cost.

Through this article, we will analyze from the perspective of Terra, a major participant in the Curve War, the corresponding financial costs required to obtain CRV liquidity rewards to incentivize the liquidity depth (TVL) of their trading pools on the Curve, Convex, and Votium DeFi protocol platforms. We will then analyze the current trading environment of the corresponding stablecoins on Uniswap V3, hoping to provide valuable reference information for all stable asset project parties and DeFi investors.

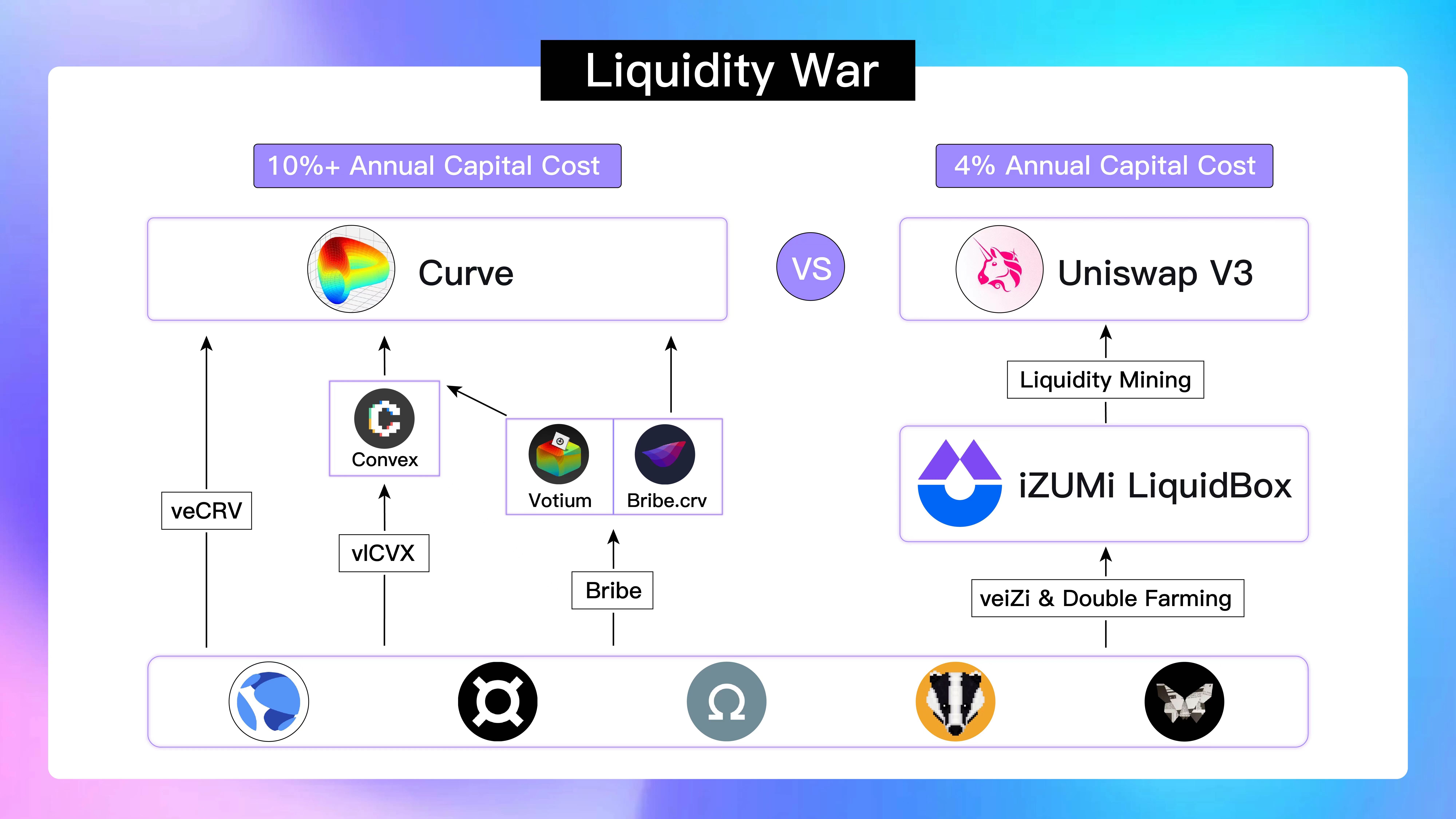

Curve Level

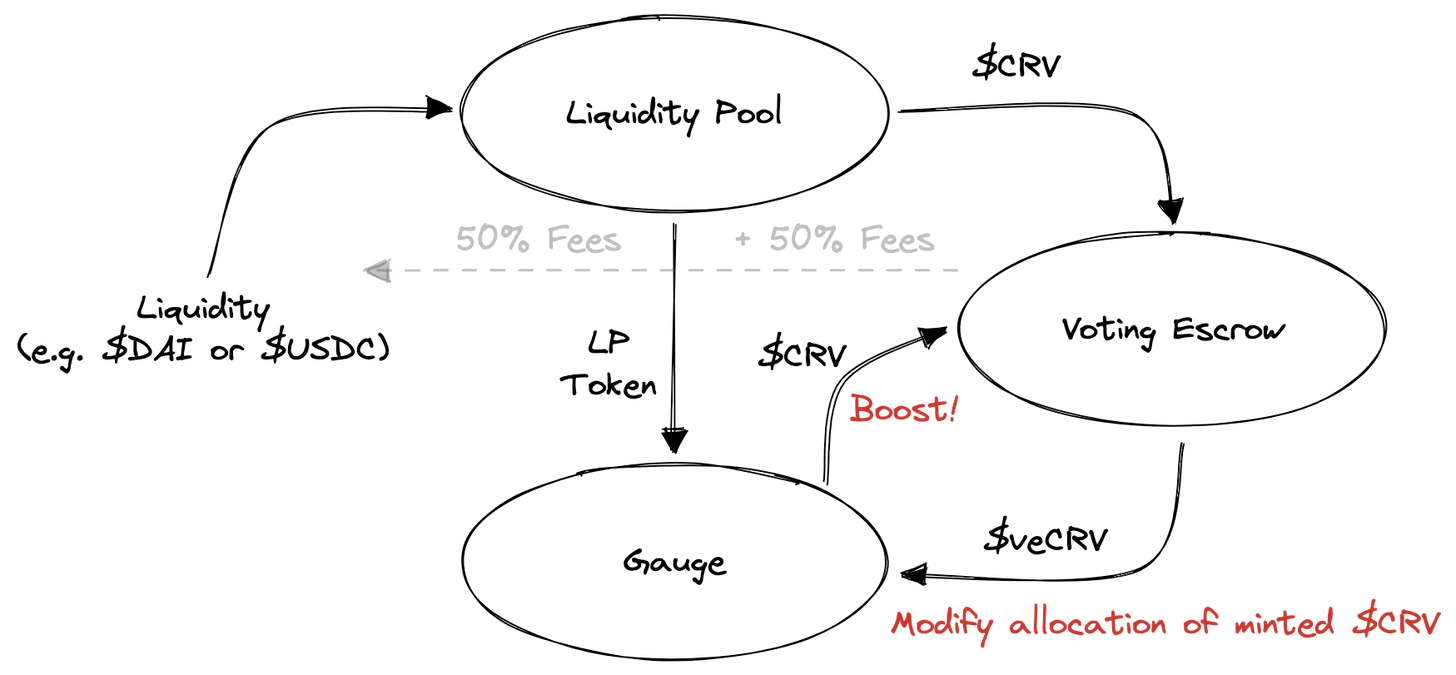

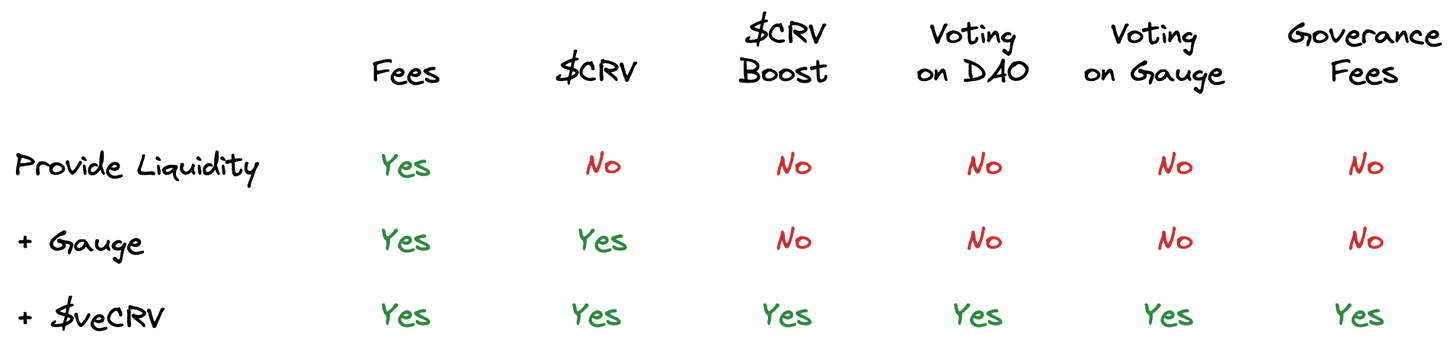

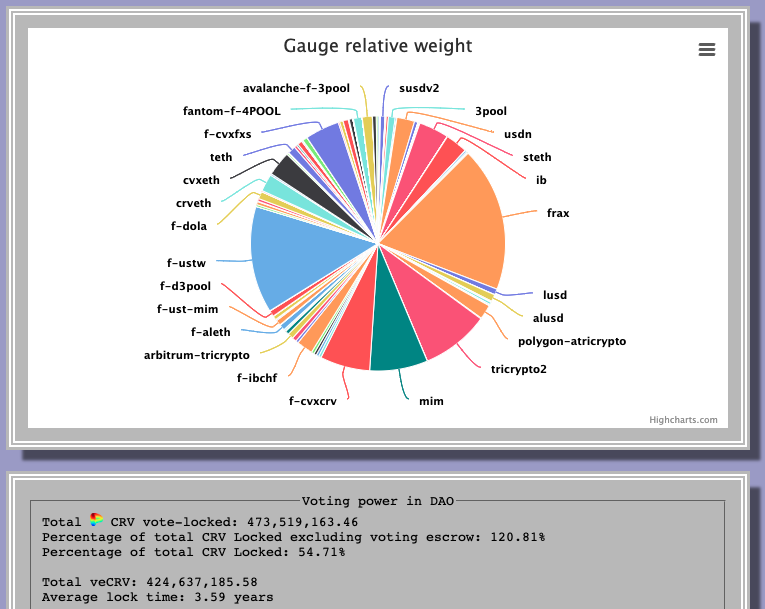

From the perspective of liquidity providers on Curve, when they provide liquidity to the liquidity pools on Curve, they will receive 50% of the corresponding trading fees and liquidity mining rewards in $CRV tokens. To earn more, they need to lock CRV tokens to obtain veCRV tokens to share the remaining 50% of trading fees and can boost their $CRV rewards up to 2.5 times. Additionally, based on the Curve Gauge mechanism, veCRV holders can vote to support the funding pools to increase their weight, thereby allowing the corresponding LP of the funding pool to receive more $CRV rewards.

Therefore, at the Curve level, if project parties wish to join the Curve War to compete for CRV liquidity incentives and increase the liquidity depth of their project token's corresponding funding pool, they need to purchase CRV on the open market and lock it to obtain veCRV to directly participate in the voting for Curve Gauge Weight, increasing the expected returns of the corresponding funding pool to attract more liquidity providers and funds. According to the data in the chart below, the main source of benefits for liquidity providers corresponding to UST and FRAX on Curve is the liquidity mining rewards of the $CRV platform token, with recent trading fee benefits even accounting for only 2-10% of the value of CRV rewards.

If we calculate based on the current market price of Curve (April 25, 2022) at approximately $2.5, and assume that the price remains stable when the project party purchases Curve tokens on the open market, to have the same amount of veCRV voting power as Terra, they would need to purchase 57.75M CRV tokens and lock them for 4 years, resulting in a direct financial cost of approximately $144.374M, attracting about $1.3B of TVL, corresponding to an annualized CRV liquidity mining yield of 2.74-6.85%, with UST's TVL being approximately $650M.

Convex Level

Convex is currently the main platform for competing for dominance in the Curve War among mainstream DeFi projects. As mentioned in the previous section, the biggest cost of competition at the Curve level is the need to lock CRV for four years to obtain the maximum amount of veCRV, which is an excessively long time in the DeFi space.

Convex effectively addresses this issue because when users deposit CRV into the Convex platform, they receive cvxCRV tokens on a 1:1 basis, which can circulate freely in the market. Due to the ample liquidity on the Curve platform, the price of cvxCRV has achieved a good 1:1 peg with CRV tokens, providing cvxCRV holders with a highly liquid exit channel. As a result, Convex has accumulated a large amount of CRV tokens, with its veCRV holdings accounting for approximately 45% of the total veCRV supply.

To compete for the voting rights of the approximately 45% veCRV held by Convex, CVX holders also need to lock CVX to obtain vlCVX for voting. However, compared to veCRV, vlCVX is more favorable for users because the locking period is uniformly set at 16 weeks, saving users a lot of time compared to the maximum 4-year locking period of veCRV, thus increasing the liquidity of the CVX token itself.

Therefore, the main focus of participants in the Curve War, such as Terra and Frax, is currently on the competition for control over Convex. We can also see various DeFi protocols continuously accumulating the amount of CVX they control, locking them to obtain vlCVX and then voting to guide the voting of the underlying veCRV controlled by Convex.

However, assuming the current market price of CVX is approximately $26, the total funding cost for the approximately 4.56M CVX controlled by Terra and Frax is about $118.55M. Although both have firmly occupied the top two positions in terms of DAO CVX holdings, their total control only accounts for about 10% of the locked CVX amount, which is still far from achieving control over the Convex platform.

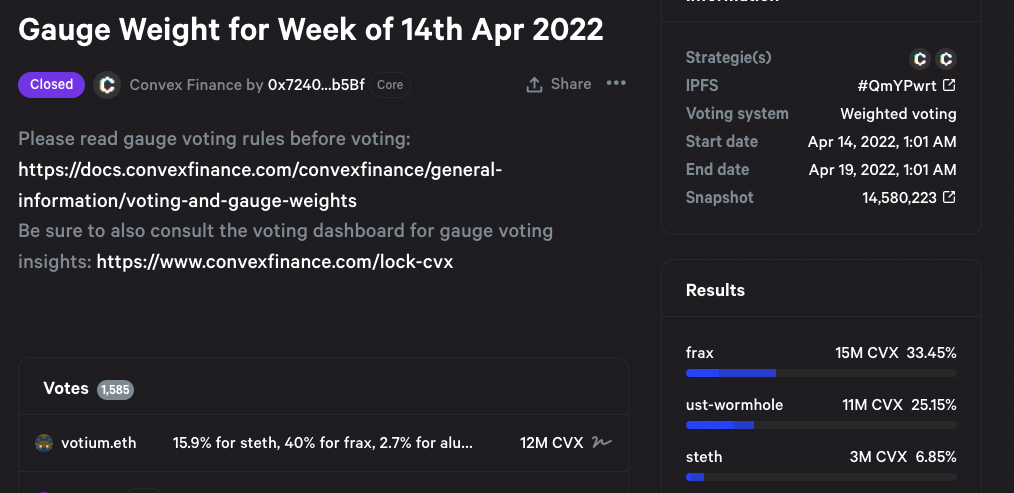

Assuming that all CVX held by Terra and Frax will be used for voting on 4Pool, according to the results of the last vlCVX voting, Terra and Frax collectively received about 58.6% of the Gauge Weight votes (a significant portion of which was obtained through bribery, which will be analyzed later). Considering that the total veCRV held by the Convex protocol is currently about 215M, Terra and Frax will obtain approximately 126M veCRV Gauge votes through Convex. Therefore, in the past two weeks, Terra and Frax have received approximately $7.3M in CRV emission rewards, providing about $4B of TVL for Terra and FRAX trading pairs.

Bribery Protocol Level

In addition to directly purchasing CRV and CVX tokens to increase their funding pool incentives, project parties now have a more efficient way to obtain the necessary voting rights: bribery platforms based on DeFi's Lego attributes ------ Bribe and Votium.

Bribe.crv--Curve

Bribe.crv is a bribery platform directly targeting veCRV holders, currently supporting third-party funding to guide veCRV holders in voting for Curve DAO Proposals and Gauge Weights.

However, its main use case is still for project parties to provide token rewards to bribe veCRV holders to vote for their project tokens' Gauges, increasing the proportion of their liquidity mining $CRV rewards. This also innovatively provides liquidity mechanisms for the voting rights of veCRV itself, as different project parties need to bid to bribe more veCRV votes, providing efficient market pricing for veCRV voting rights and bringing additional income to veCRV holders.

VeCRV holders only need to vote for the funding pools with bribery rewards, and they will automatically receive bribery rewards according to their voting weight. The Convex protocol itself is also part of the "veCRV holders" group, so it will also receive bribery rewards provided on the Bribe platform and distribute them proportionally to Convex protocol users.

Votium-Convex

Unlike Bribe, which directly serves veCRV holders (including the Convex protocol), Votium directly serves vlCVX holders.

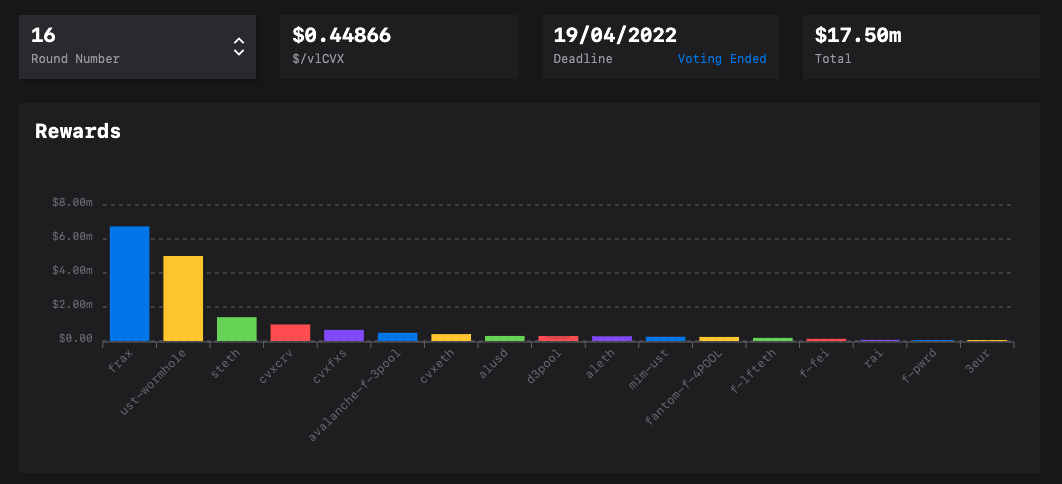

Similar to the logic of the Bribe platform, buyers of voting rights can provide bribery rewards on the Votium platform to guide more vlCVX voting rights into their designated funding pools. Voting on the Votium platform occurs every two weeks, meaning buyers need to provide a new round of bribery funds every two weeks. In the last round of voting, FRAX and Terra collectively provided approximately $11.74M in bribery funds, with each vlCVX token receiving about $0.45 in bribery rewards.

If the bribery costs remain unchanged, then Terra and Frax would spend approximately $306M on bribery over a year, corresponding to the current TVL of the two project tokens on the Curve platform, with their bribery annualized cost reaching as high as 13.5%. Considering that Terra and Frax have already spent a significant amount on purchasing CVX tokens, this does not effectively reduce the cost of maintaining the circulation of their tokens through incentives compared to the approximately 20% annualized interest cost of Anchor. Moreover, with the increasingly fierce competition for Convex voting rights, the bribery costs will gradually increase.

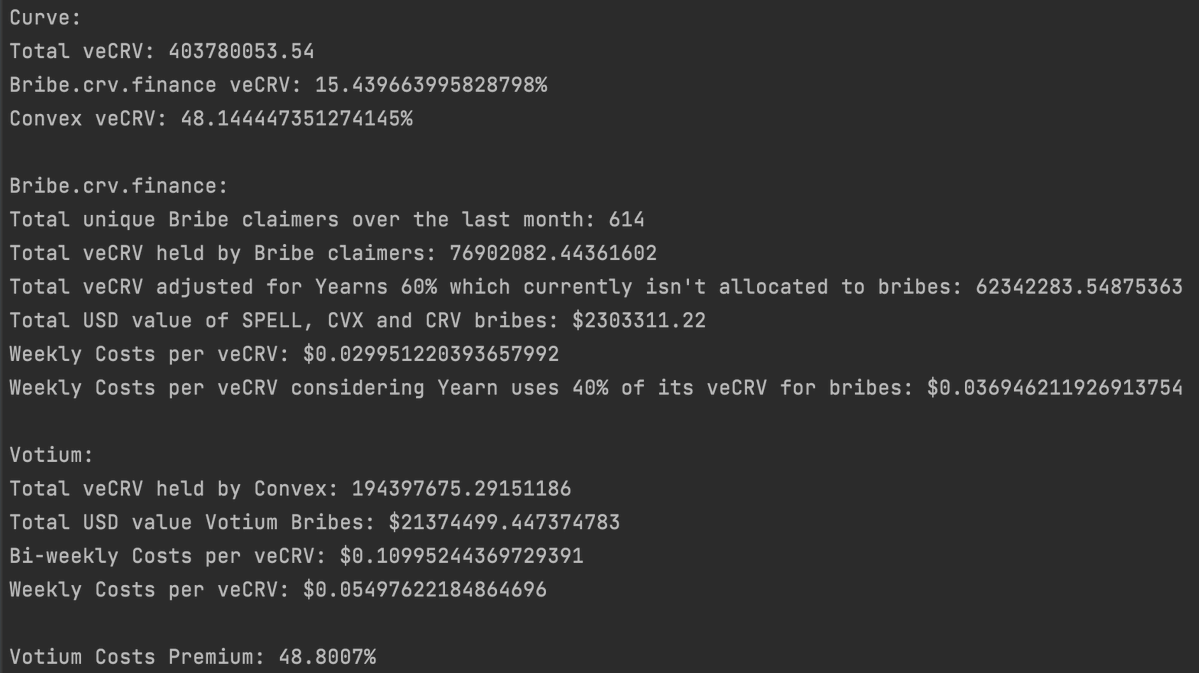

Regarding the comparison of bribery costs on the two platforms, @0xSEM compared the data from March Bribe.crv and Votium Round 15, concluding that the bribery costs on Votium are about 48% higher, meaning that bribery parties on Votium can achieve higher capital efficiency if they use Bribe.crv. However, once participants in the Curve War realize this cost difference, the bribery cost gap between the two platforms has already narrowed and will gradually converge.

Is Uniswap V3 Ending the Curve War?

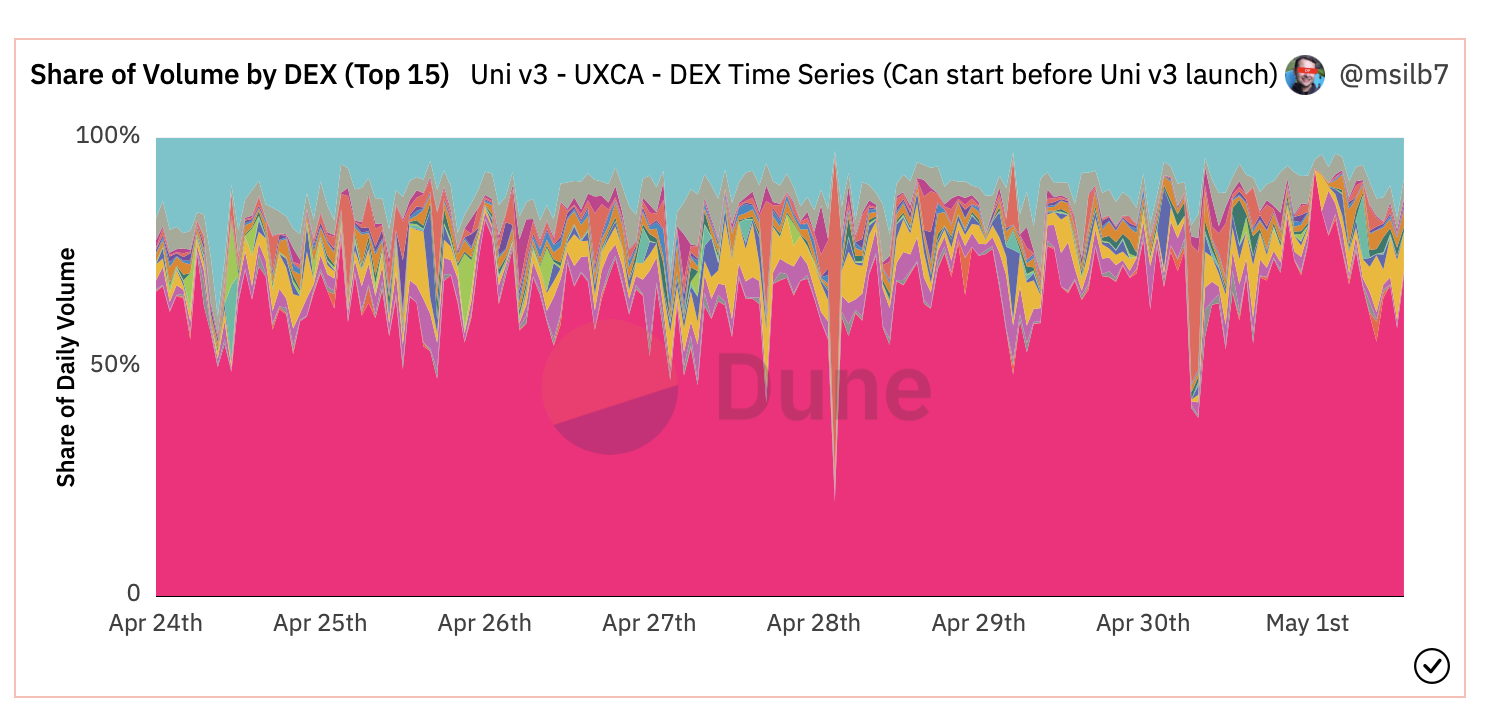

Uniswap V3 officially launched on May 5, 2021, and after nearly a year of operation, it has proven its dominance in on-chain trading volume: accounting for about 70% of trading volume on Ethereum, and nearly 80% of DEX trading share when including Uniswap V2.

(The pink area represents Uniswap V3)

Although most of the trading volume comes from non-stable assets, the innovative design of Uniswap V3's concentrated liquidity AMM allows liquidity providers for stablecoin trading pairs to concentrate liquidity around the value of 1, for example, the DAI/USDC trading pair's liquidity is concentrated within the (0.999, 1.001) value range, which significantly reduces the slippage of stablecoin assets during trading compared to traditional AMMs, thus providing an alternative for stable asset trading outside of Curve.

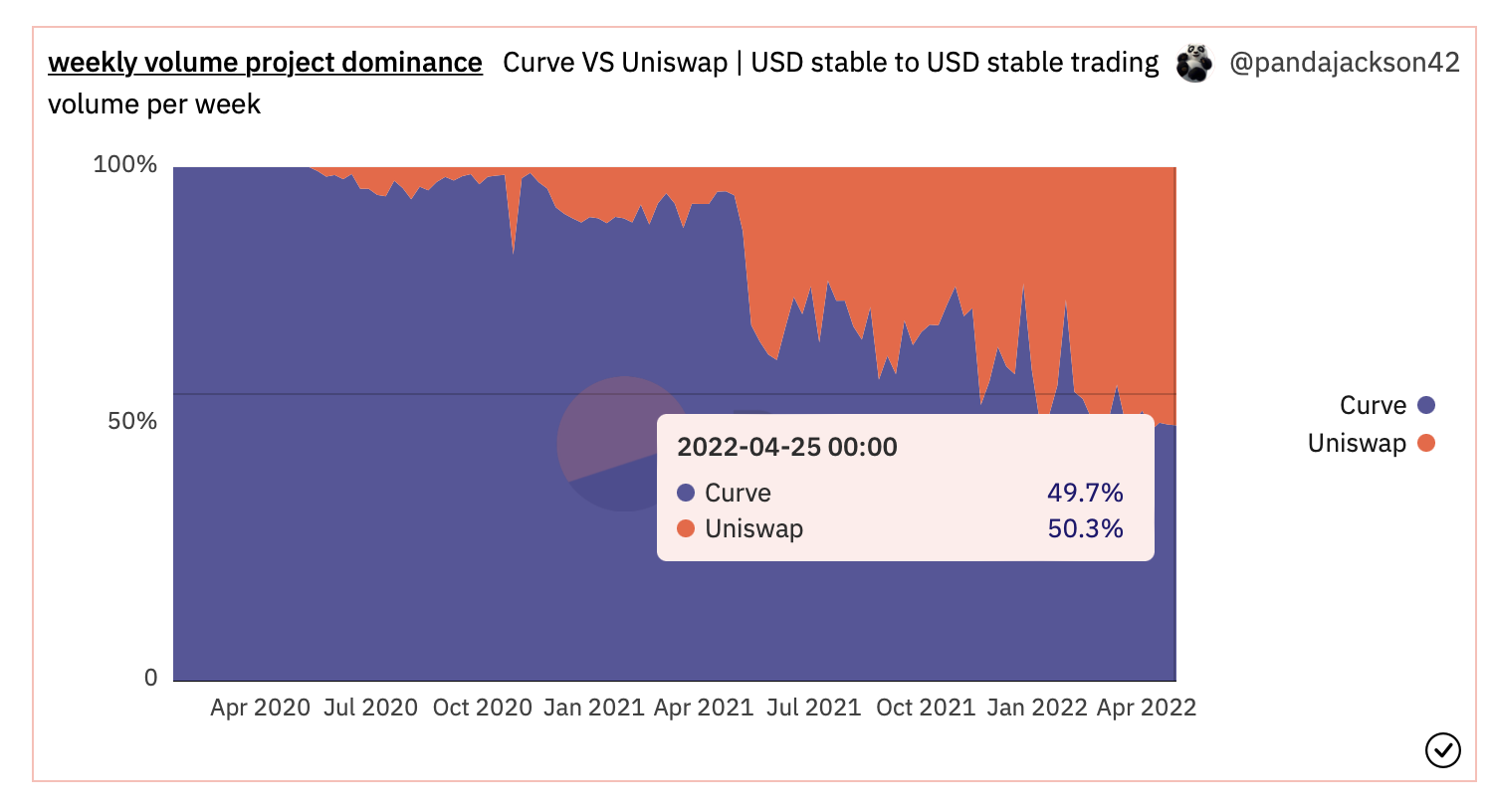

On-chain data shows that Uniswap V3's share of on-chain dollar stablecoin trading volume has been continuously increasing, gradually eroding Curve's market share. Currently, Uniswap V3 has surpassed Curve to become the largest decentralized exchange for dollar stablecoins on-chain.

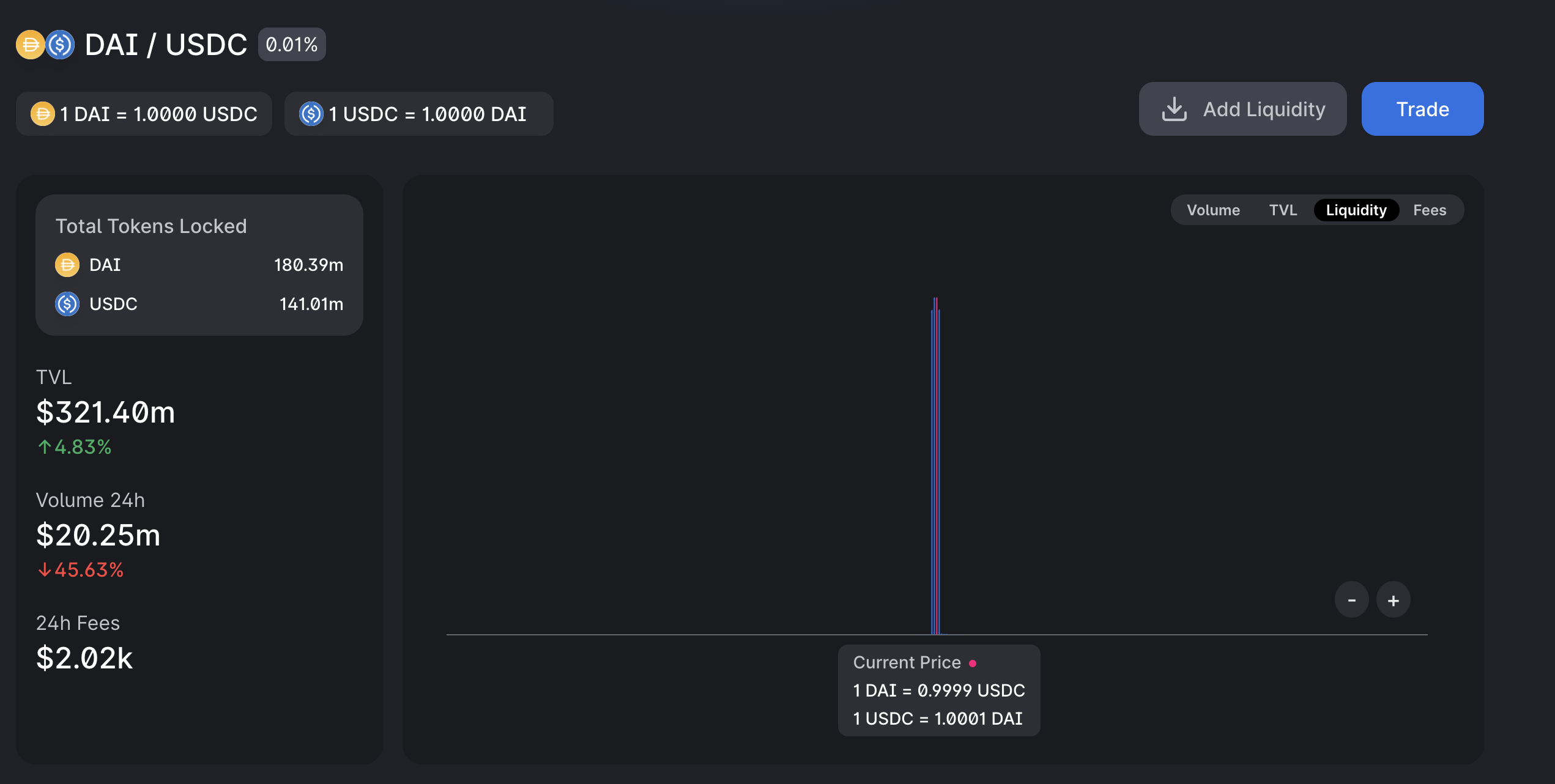

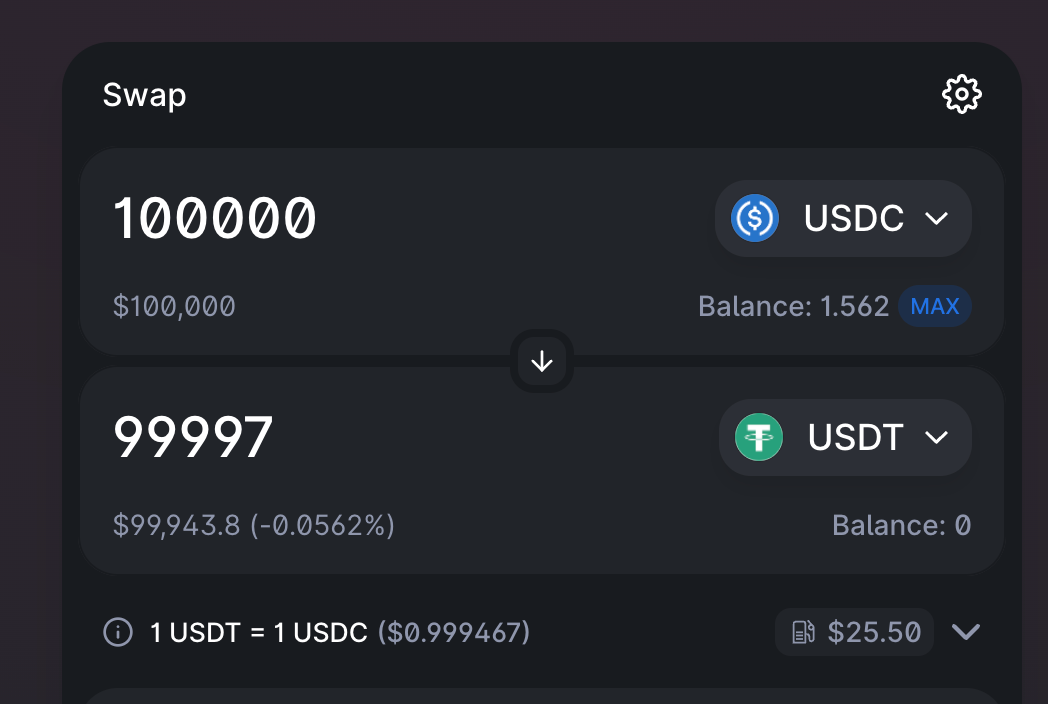

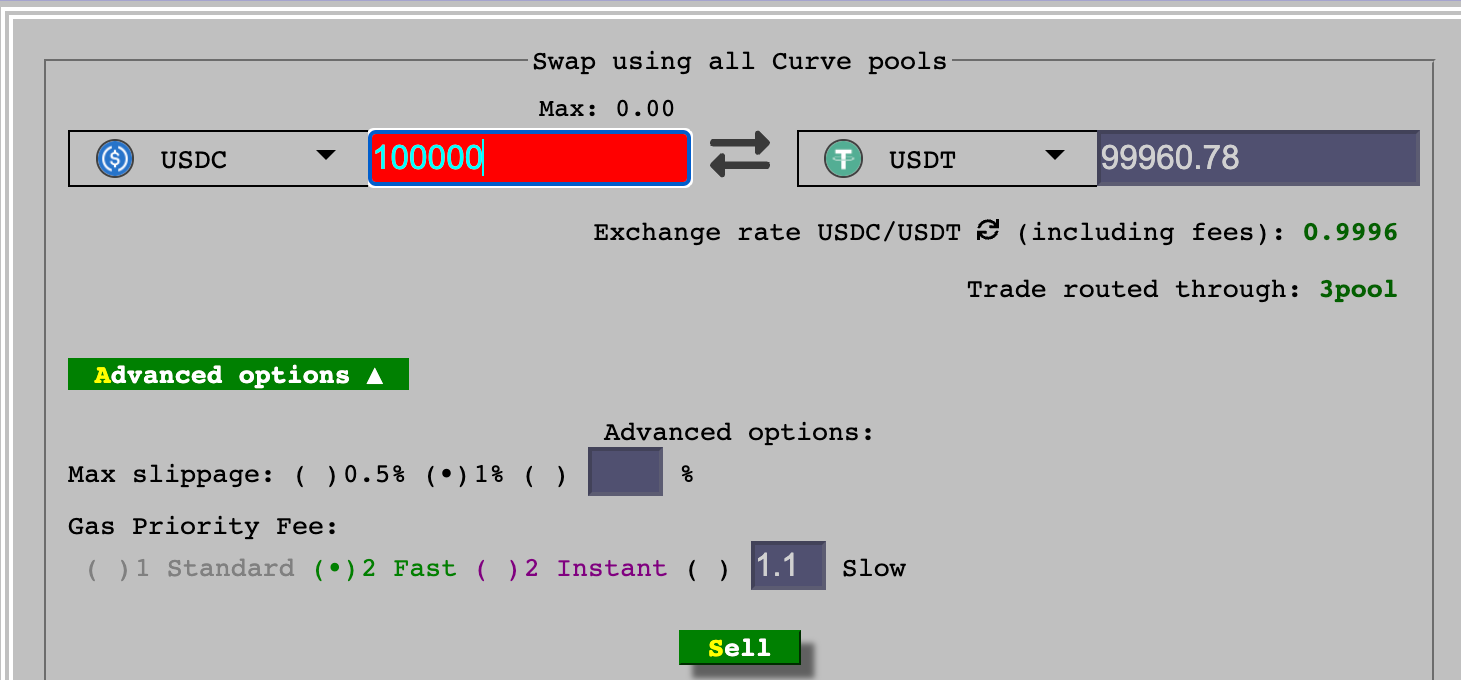

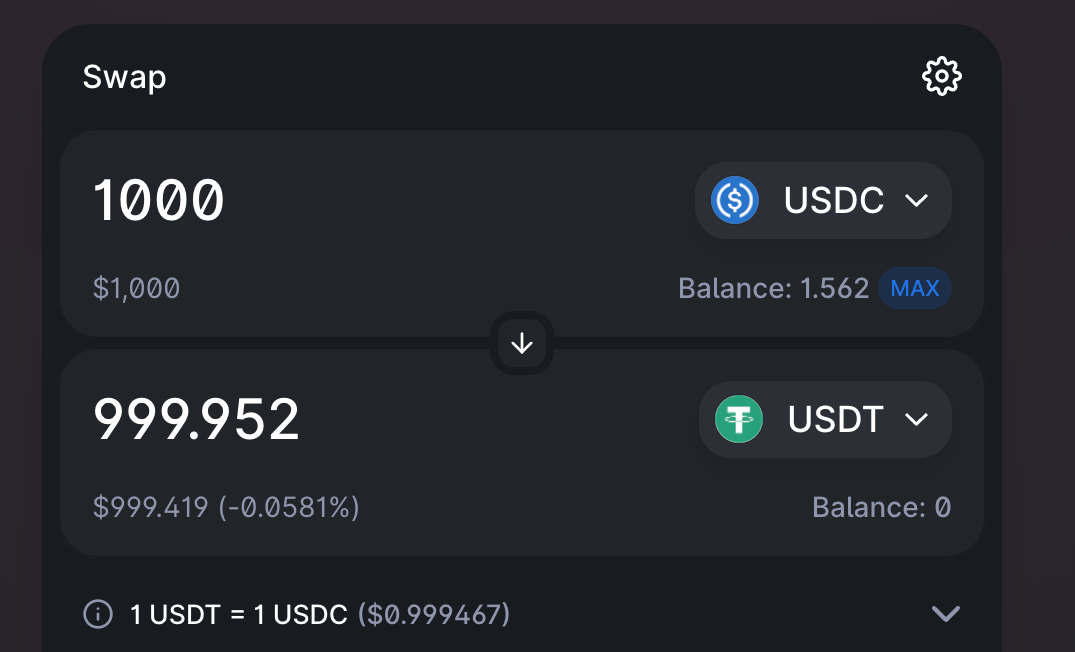

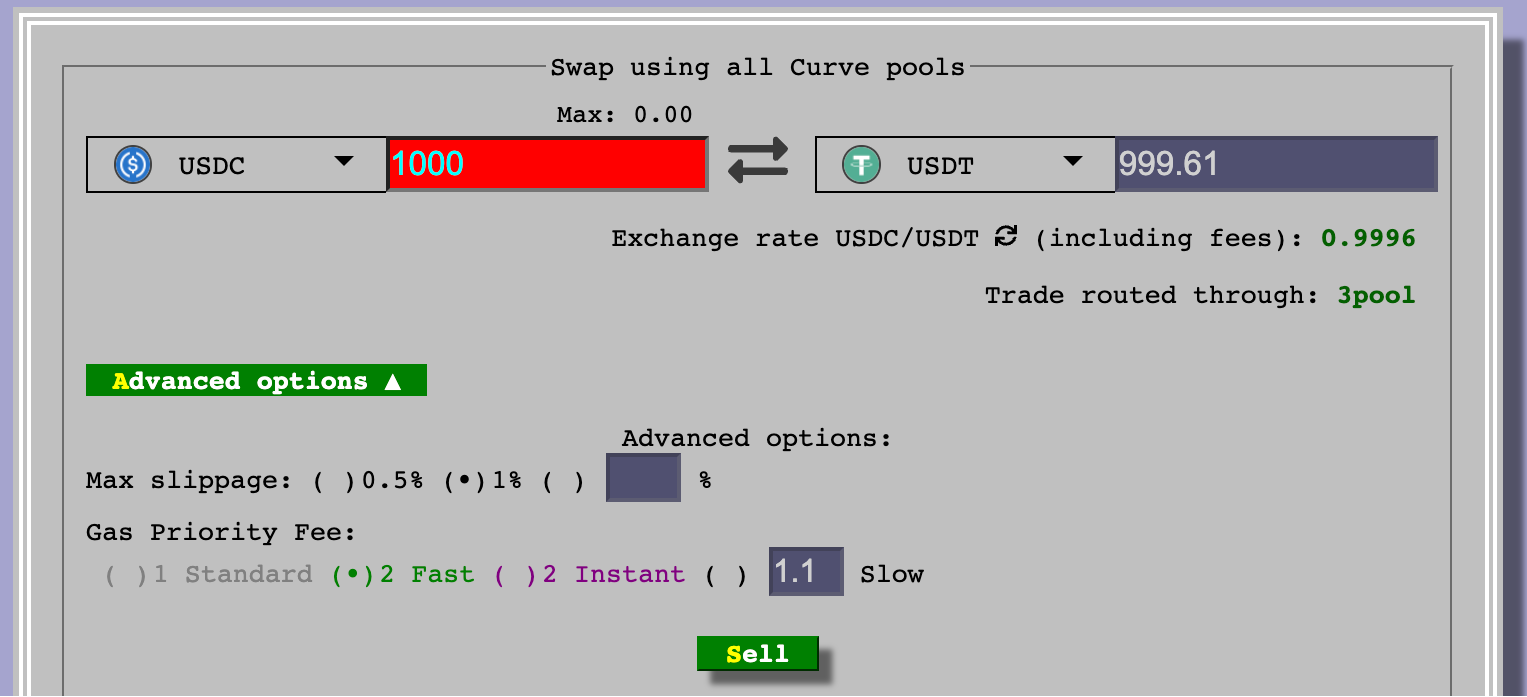

As of now (May 1, 2022), the TVL of the Curve 3-pool with USDC + USDT is $1.95B, while the TVL of the Uniswap V3 USDC/USDT trading pool is $217.43M, making the former approximately 9 times larger than the latter. If we compare the current real trading situations, taking $100,000 and $1,000 USDC/USDT trades as examples representing whale and retail single-coin trading shares:

From the screenshots above, we can see that regardless of the transaction amount, trades on Uniswap V3 achieve better results. The main reason for this difference is not due to the trading slippage caused by the AMM mechanism, but because the transaction fee for the corresponding trading pool on Uniswap V3 is 0.01%, while the transaction fee for Curve's 3Pool is 0.03%.

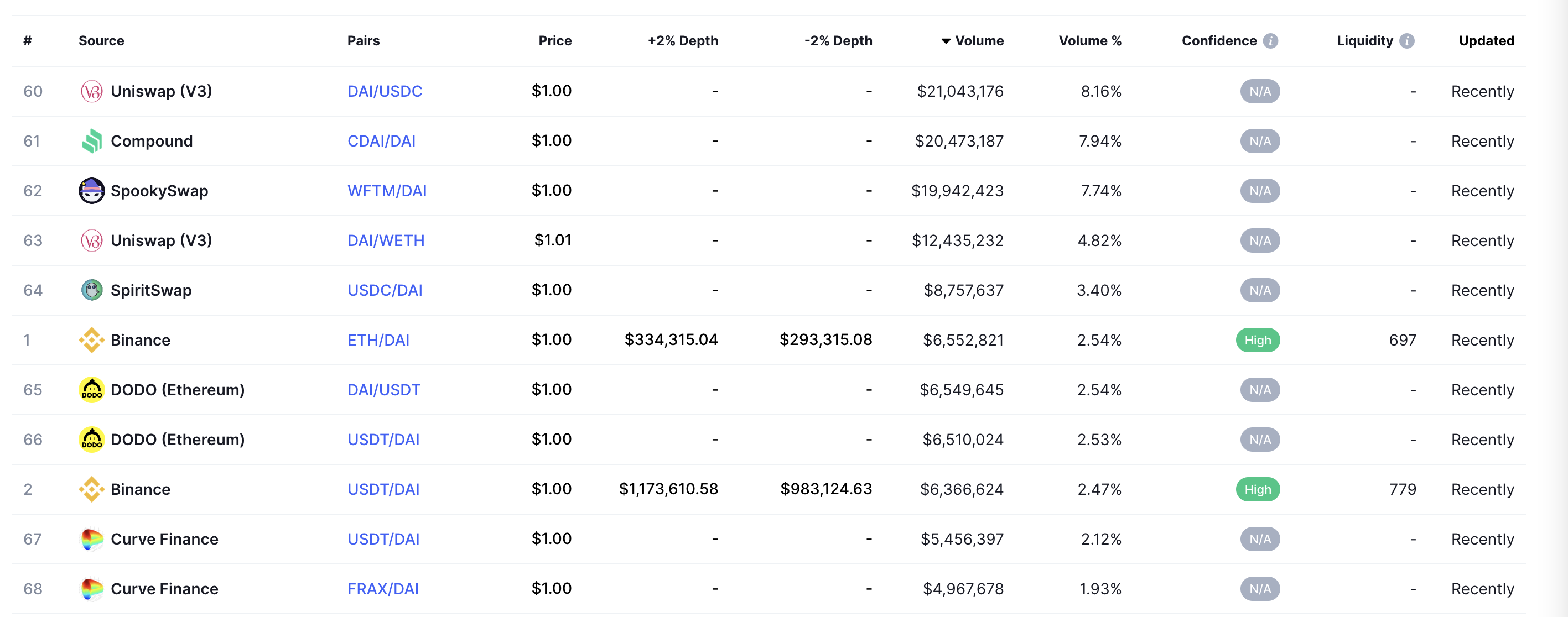

For MakerDAO's $DAI, which is most negatively impacted by the 4Pool proposal, Uniswap V3 has already captured its largest trading volume, and the trading volume of DAI against dollar stablecoins on Curve accounts for only a small portion (less than 5%). At the same time, DAI's trading pairs with other mainstream coins also provide ample trading depth, ensuring DAI's liquidity and supporting its use cases in the overall on-chain liquidity market.

(DAI trading pairs based on 24-hour trading volume and corresponding trading platform rankings)

Considering MakerDAO's own PSM mechanism, which supports a 1:1 exchange of DAI and USDC, as MakerDAO co-founder @RuneKek stated, MakerDAO is currently not very concerned about the impact of 4Pool on its 3Pool liquidity.

Supplement: @MonetSupply posted a proposal on Twitter on April 29 regarding MakerDAO's participation in the Curve War: MakerDAO is planning to initiate another 4pool proposal consisting of DAI- USDC- USDP - GUSD. This could become a strong competitor to the 4Pool initiated by Terra. In Proposal B, Maker plans to issue a wrapped staking token for CRV, mkrCRV, and lock the obtained CRV tokens to obtain veCRV, thus directly entering the Curve War.

Capital Efficiency: Uniswap V3 > Curve

A crucial metric for comparing DEXs is the capital efficiency of their liquidity funds: Volume/TVL. Here, we compare the capital efficiency of dollar stablecoin trading on Uniswap V3 with that on the Curve platform. The 7-day volume/TVL for Uniswap V3 dollar stablecoin trading pairs is 1.15, while Curve's is only 0.06. Therefore, for dollar stablecoins, Uniswap V3 has 19 times the capital efficiency of Curve. This means that LPs can capture more trading fees through Uniswap V3.

Currently, more funds choose to provide liquidity on the Curve platform mainly due to the liquidity mining rewards offered by Curve and Convex, with corresponding APRs for UST and Frax trading pairs reaching 9.54% and 5.95%, respectively. In contrast, the estimated annualized yield for dollar stablecoin trading pairs like USDC/USDT on Uniswap V3 based on 7-day trading volume is 1.5%. Although the corresponding APR for the 3 Pool on Curve is only 1.26%, as a liquidity provider, obtaining low-risk liquidity mining incentives for dollar stablecoins through the Curve ecosystem is a better investment choice.

However, if we consider adding a liquidity mining incentive model based on Uniswap V3, could this gap be bridged or even surpassed?

iZUMi's LiquidBox --- The Curve Killer in the Uniswap V3 Ecosystem

In Uniswap V3's concentrated liquidity mechanism, users can customize the value range for providing liquidity, making each user's liquidity unique. As a result, the LP Token provided by Uniswap V3 has transformed into an NFT model, breaking the traditional model of distributing liquidity mining rewards based on the quantity of ERC-20 LP Tokens pledged by users.

This transformation of the LP Token model makes traditional liquidity mining models unfeasible on Uniswap V3, while liquidity mining incentives are the primary means by which the Curve ecosystem can offer higher liquidity incentives compared to Uniswap V3. To address this issue, iZUMi Finance launched the LiquidBox platform based on Uniswap V3, allowing users to participate in liquidity mining activities by pledging Uniswap V3 LP NFTs to earn token rewards.

Based on different project parties' varying needs for price volatility, and in conjunction with the characteristics of Uniswap V3 LP NFTs, iZUMi has launched three different types of programmable liquidity mining models on the LiquidBox platform to serve different liquidity needs. Among them, the "Fixed-range" model for fixed price ranges effectively addresses the liquidity mining needs for stable assets.

The fixed price range liquidity mining model is suitable for stablecoins or assets with low price volatility, allowing project parties and platforms to customize target liquidity market-making ranges. Users can arrange specified price ranges to inject liquidity on Uniswap V3 and stake the obtained Uniswap V3 NFTs on the iZUMi platform. Subsequently, liquidity providers will earn rewards in iZi platform tokens while also receiving Uniswap V3 trading fee income.

This model not only meets the demand for concentrated liquidity for stable assets but also allows Uniswap V3 to directly compete with Curve's CFMM algorithm + CRV token incentive model with the support of iZUMi's liquidity mining. Additionally, original Uniswap V3 liquidity providers can also earn extra liquidity mining rewards beyond trading fees.

iZUMi supports liquidity mining for the USDC/USDT trading pairs on Uniswap V3 across Ethereum, Polygon, and Arbitrum. In the Uniswap V3@Polygon USDC/USDT trading pair, 87% of the $4.7M liquidity funds are participating in iZUMi liquidity mining ($4.1M). Similarly, in the Uniswap V3@Arbitrum USDC/USDT liquidity funds, the $13.3M TVL on the iZUMi platform accounts for 95% of the total fund pool ($13.95M).

Such a high participation rate in TVL liquidity mining has proven its attractiveness to stable asset holders and significantly enhanced the liquidity funds and trading depth of the corresponding trading pairs.

Comparing the current approximately 9.5% APR yield provided by Curve + Convex with the 1.5% yield for liquidity providers based on trading fees on Uniswap V3, if we add an 8% APR liquidity mining yield for liquidity funds through iZUMi Finance, half of which is provided by iZi platform token mining and the other half being the project party's corresponding liquidity funding cost: only 4%.

This represents a significant improvement in both cost and efficiency compared to liquidity funds obtained through traditional AMM ERC-20 LP token liquidity mining incentives, as well as the liquidity funds obtained through competing for governance rights for Curve ecosystem incentives analyzed earlier. Project parties can obtain better on-chain liquidity at a lower funding cost, providing users with a better trading experience and meeting the goals of algorithmic stablecoin project parties like Terra and Frax to accumulate their token use cases. Therefore, for such stable asset project parties, conducting liquidity mining incentive activities through the iZUMi LiquidBox platform and migrating liquidity to the concentrated liquidity range on Uniswap V3 may be a more cost-effective and efficient choice.

Conclusion

Although UST and Luna have not yet fully proven the reliability of their value support, the 4Pool proposal initiated by Terra can be considered the most exciting event in the DeFi industry in April. Its impact on the Curve War situation and the uncertainty of the final outcome of 4Pool highlight the high innovation and risk inherent in the DeFi industry. Through this research report, we hope to help everyone understand the financial costs that external participants in the Curve War, whose main goal is to promote the liquidity of their project tokens, need to bear at different levels of the ecosystem.

Additionally, through the analysis of the trading limitations of dollar stablecoins on Uniswap V3, we hope everyone recognizes that Uniswap V3 has become a superior trading platform compared to Curve. With the support of LP NFT liquidity mining functions provided by iZUMi Finance, Uniswap V3 now possesses all the necessary conditions to comprehensively surpass Curve. Once the core value function of the Curve platform -- stable asset trading -- is surpassed by competitors, the value support of its ecosystem projects will rapidly collapse. Once this perspective becomes mainstream market recognition, the foreseeable conclusion of the Curve War may not be far away.