iZUMi Research: The Current State of DEX and the Future of Decentralized Trading

The DEX protocol itself, as underlying infrastructure, has good openness, and a series of products and services will emerge on top of it.

The DEX protocol itself, as underlying infrastructure, has good openness, and a series of products and services will emerge on top of it.Author: iZUMi Research

Source: Foresight News

November 8, 2022, will be another day recorded in the history of Crypto. In just three days, a generation of giants fell from grace, and the speed of the collapse exceeded everyone's expectations, severely impacting industry confidence. However, from another perspective, this may be a new turning point for the industry.

In the aftermath of FTX, every exchange is trying to prove its innocence. Binance, OKX, Bybit, Bitget, Huobi, and Gate have all proposed their own Merkle tree asset proof schemes, but in reality, these schemes still require auditing by relevant authorities and cannot guarantee complete safety. Human greed is such that, for the sake of "capital efficiency," to earn interest rate spreads and amplify their own risks, this is actually common in traditional finance: everyone wants to make money when the market is good, and everyone believes they can manage risks well and exit safely. But when a liquidity crisis strikes, the tide goes out, and no one has time to put on their clothes.

Looking back, it has been two years since DeFi Summer. During this cooling period in the industry, various DeFi protocols have slowly faded from people's view.

In a 2015 cover article, The Economist referred to blockchain as "the trust machine." This has not changed in the seven years since; cryptography is unbreakable, and the cryptoeconomic system has been validated over time. We have repeatedly tested the security of the Bitcoin and Ethereum networks. The emergence of DeFi, based on the unique protocol characteristics of blockchain, has challenged the traditional financial posture by proposing non-custodial, secure, and transparent on-chain transactions, lending, and various financial services.

When we cannot trust human nature, it is time to regain the original "trust."

As the most fundamental application on-chain, DEX has almost become a configuration at the public chain protocol level. Each different public chain will have its own leading DEX, often occupying a large portion of the market share in terms of TVL and trading volume. In terms of public chain ecology, most public chains will also support their own exclusive ecological DEX. DEX teams combine the characteristics of their respective public chains, their own team capabilities, and different judgments about the future. In this report, we analyze the largest pool on Uniswap V3, WETH-USDC 0.05%, focusing on both the Taker and Maker sides to represent the current overall state of the DEX track under different market conditions. At the same time, we conducted research on over 20 leading DEXs and DEX aggregators distributed across various ecosystems, making trend judgments about the mid-term future of the DEX track based on their operational conditions and currently announced development directions.

Observing the Current State of DEX from the Operations of Leading Exchanges

The earliest DEXs in 2017-2018 imitated traditional order book models, such as EtherDelta and DDEX, but due to on-chain transaction cost issues, it was difficult to achieve good depth and trading experience. Even with the emergence of high-performance infrastructure, the overall experience of order book-based DEXs still struggles to compete with CEXs.

At the end of 2018, Uniswap implemented an automated market maker mechanism and released Uniswap V1. The automated market maker (AMM) mechanism is more like a vending machine placed on the blockchain, with passive liquidity provision strategies adapted to the blockchain environment. The AMM mechanism, combined with liquidity mining, led to the explosive growth of on-chain finance during the DeFi Summer of 2020.

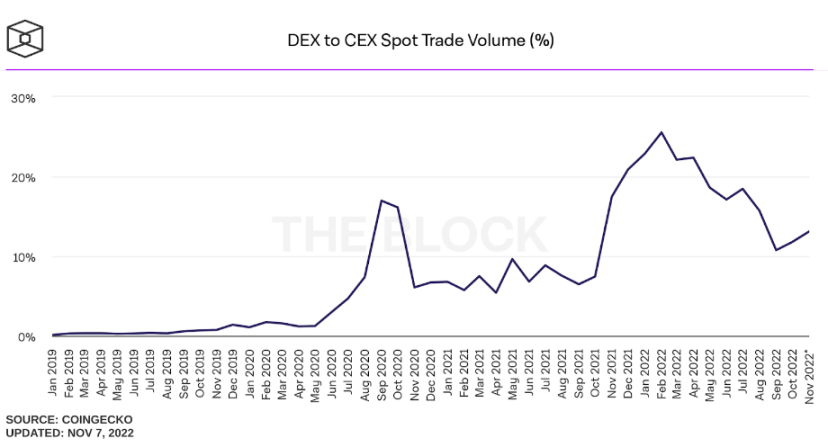

According to data from The Block, DEXs once accounted for 25% of the total trading volume across the network, currently maintaining around 15%.

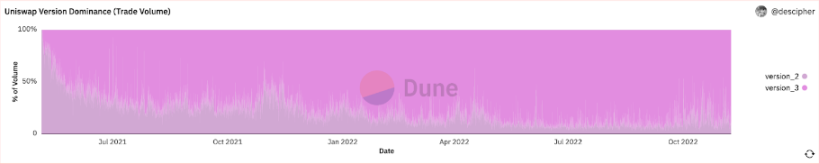

After the launch of Uniswap V3's concentrated liquidity AMM mechanism in March 2021 (where liquidity providers can choose a price range to provide liquidity instead of deploying liquidity across the entire range by default), capital efficiency improved by several dozen times compared to before. As seen in the chart below, after the launch of Uniswap V3, it began to continuously erode the market share of V2, currently averaging over 70%.

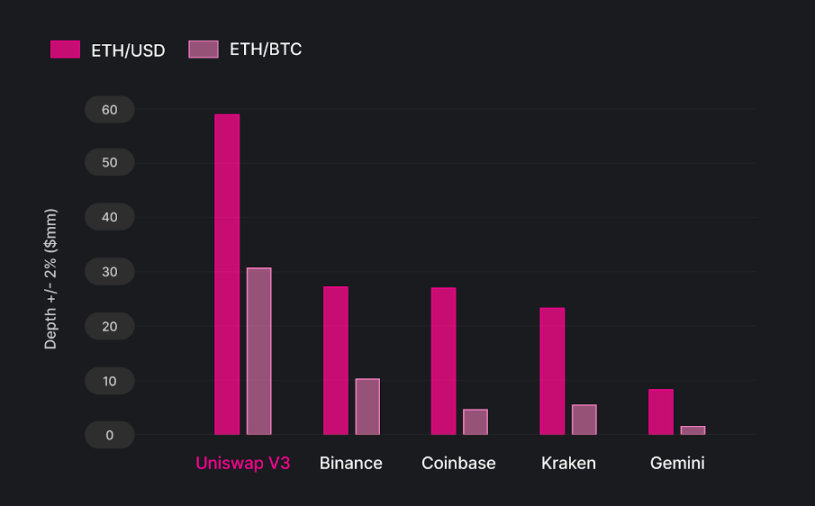

According to a research report from Uniswap in May, as the largest DEX, Uniswap once surpassed leading CEXs like Binance in terms of trading depth for mainstream coin pairs. Between June 2021 and March 2022, the depth of the ETH/USD trading pair on Uniswap for +/-2% reached twice that of Binance, demonstrating good liquidity.

So what is the current on-chain data situation for DEXs? Taking Uniswap V3 as an example, we analyze the current data status.

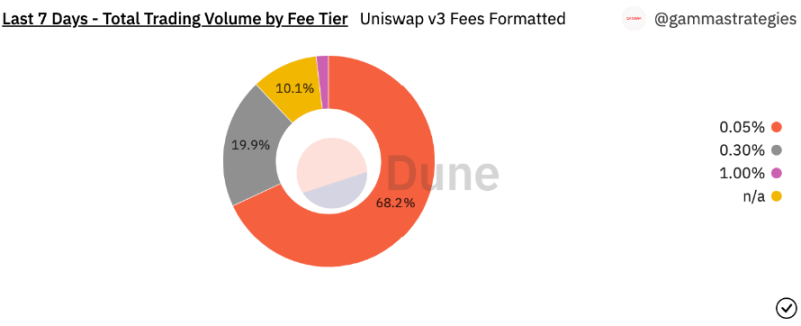

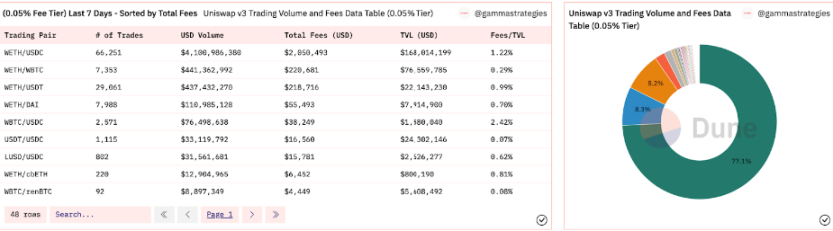

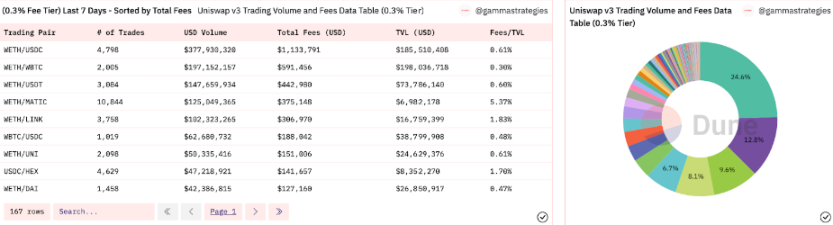

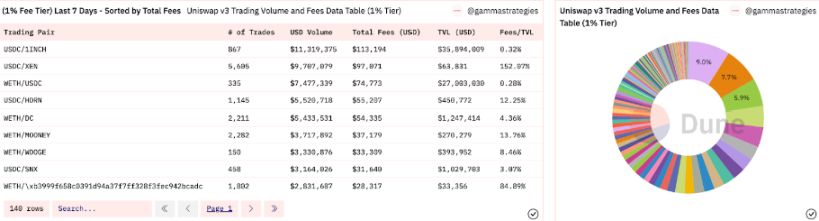

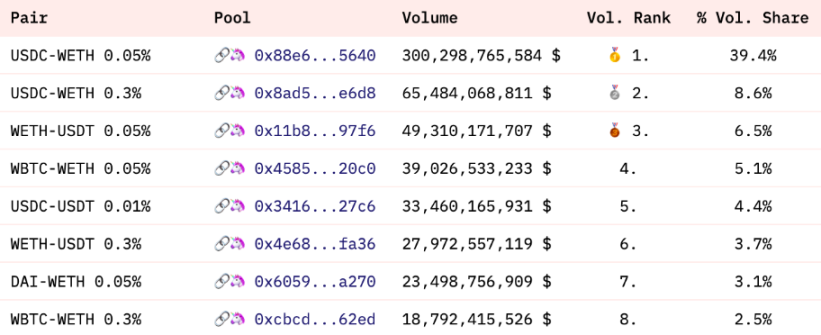

In the past seven days, Uniswap V3's total trading volume reached $7.8 billion, with the top fifteen pools accounting for $6.95 billion, a staggering 89%. In terms of fee income, the total fee income over the past seven days was $8.97 million, with the top fifteen pools accounting for $6.28 million, or 71%. This is due to the competition for trading volume among the top pools, with some liquidity providers choosing to provide liquidity in pools with lower fee percentages. For example, a significant amount of liquidity for WETH/USDC is in the 0.05% fee tier, essentially "competing" on fee rates. Meanwhile, the bottom pools mostly adopt 0.3% or even 1% fees, resulting in smaller trading volumes but a larger income share compared to their trading volume share.

Since trades on Uniswap are routed to select the lowest fees and optimal execution prices, most trades are concentrated in the 0.05% fee tier, where mainstream tokens have good liquidity. Most of this liquidity comes from the WETH/USDC 0.05% trading pool. Among the four available fee tiers, the 0.01% fee tier is relatively special, being the official liquidity pool for Dai and providing liquidity incentives through Arrakis Finance. The conditions for the other three fee tiers are as follows:

The 0.05% fee tier is primarily dominated by WETH/USDC, accounting for 77.1% of trading volume. This fee tier mainly includes stablecoin trading pairs, mainstream coins (WBTC, WETH) and stablecoin trading pairs, as well as various assets pegged to ETH/WBTC, such as the WETH/cbETH trading pair.

The 0.3% fee pool is relatively evenly distributed, mainly consisting of various mainstream tokens, as well as trading pairs for leading altcoins like Matic, Link, and Uni.

The 1% fee pool consists of longer-tail assets, with trading volumes being more dispersed.

Overall, LPs for mainstream assets are competing on fees, "involuting" into the 0.05% fee tier to vie for trading volume, attempting to exchange volume for "fee." Long-tail assets, due to their higher volatility and risks, see their relative LP costs increasing, thus opting for the 1% fee pools instead of competing in lower fee tiers.

Research on the Largest Trading Pool

According to historical data obtained from Dune, the WETH/USDC 0.05% and 0.3% pools on Ethereum account for 39.4% and 8.6% of Uniswap's total historical trading volume, respectively, with fee incomes of $150.1 million and $196.4 million, accounting for 12.4% and 16.3% of total historical fee income.

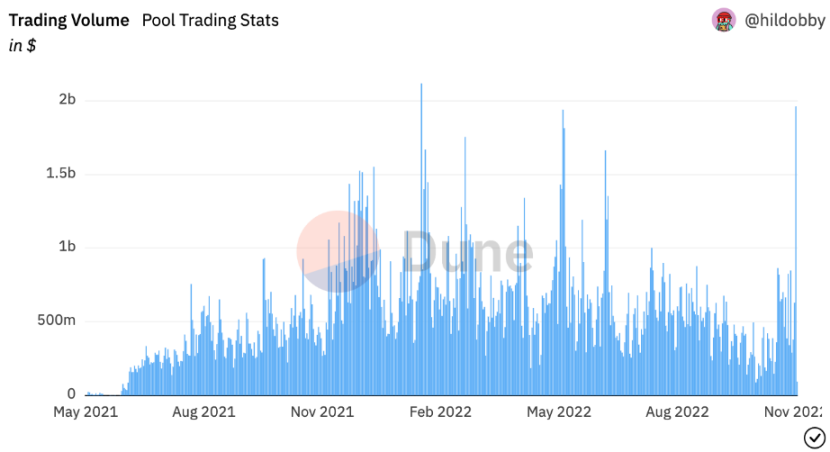

This section focuses on the Uniswap V3 WETH/USDC 0.05% trading pool, which is the largest and most active trading pool. Understanding the current status of this main trading pool can provide insights into the overall situation of Uniswap V3. The daily trading volume for this pool is as follows:

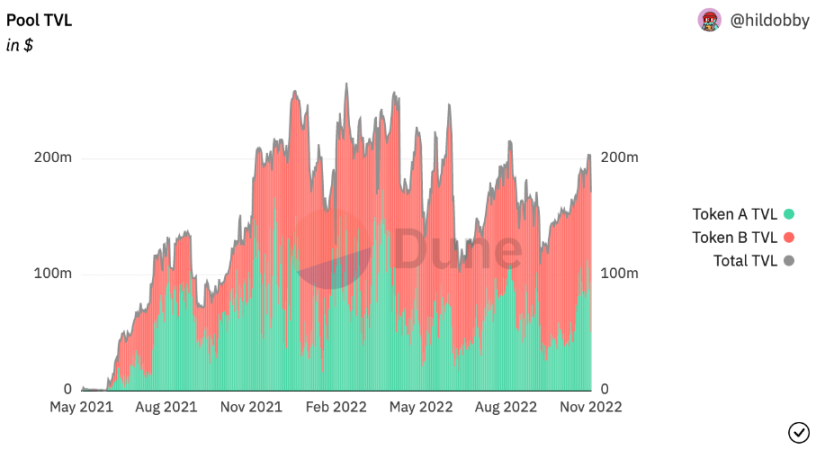

The TVL data for this pool is shown in the chart below. Recently, with frequent CEX failures, Uniswap, as an infrastructure close to the protocol layer, has gained the trust of all users. Leading DEXs will continue to maintain stable trading volumes, and with the fee income generated from trading volumes, DEXs will also have relatively stable TVL and liquidity to support trading in the ecosystem. Overall, the TVL of the Uniswap V3 WETH/USDC 0.05% pool remains relatively stable (as the chart is denominated in USD, fluctuations come from ETH price volatility), representing a high liquidity trading scenario.

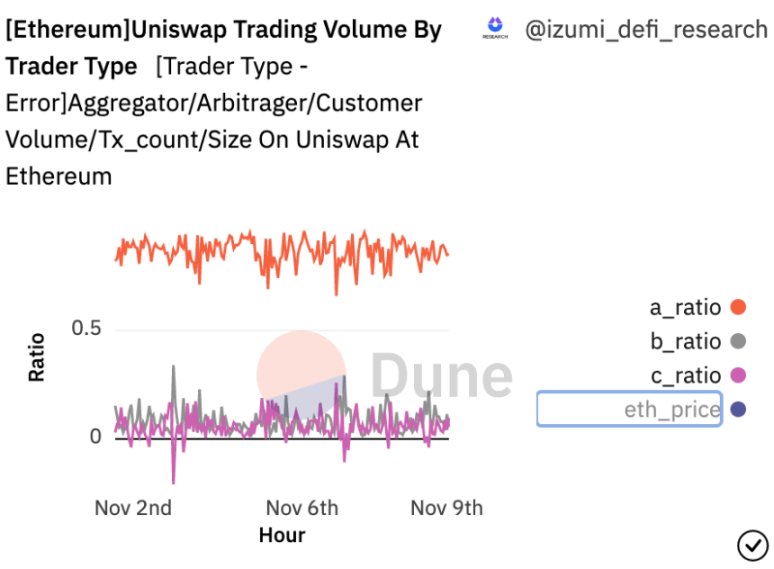

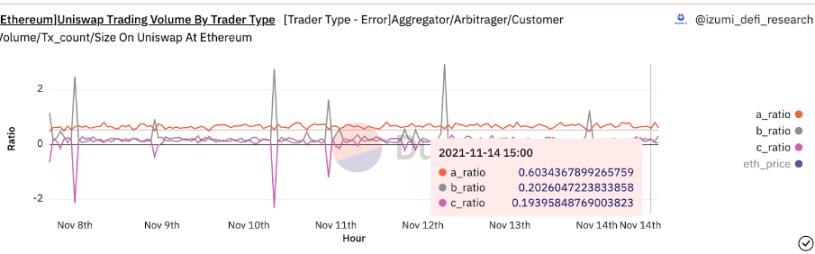

On-chain data can distinguish between bot addresses and real user addresses. Due to the latency of on-chain transactions, price discovery generally occurs on CEXs, followed by arbitrage among various bots to equalize DEX prices. There are also various trading bots on-chain. The proportion of real users is an important indicator of on-chain trading activity. Currently, in this market environment, the proportion of bot trading volume in this pool exceeds 85%.

Data from 360 days ago shows that the proportion of bot trading volume was around 60%. It can be seen that this data is indeed related to market conditions; in a bear market environment, overall trading volume declines, accompanied by a significant drop in the proportion of real users on-chain.

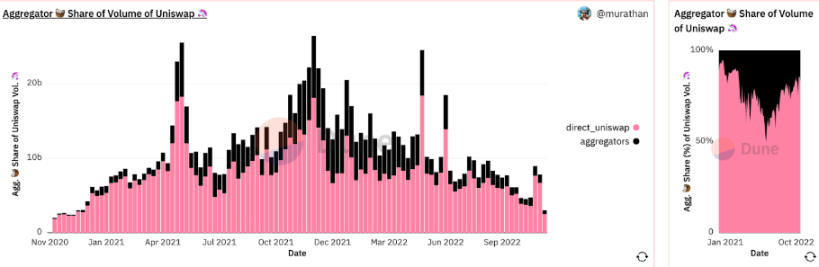

From the perspective of trading aggregators, the proportion of aggregators significantly increases during bullish markets and then declines. The main reason is that in poor market conditions, most trading volume comes from arbitrage and quantitative bots, which interact directly with Uniswap pools and generally do not operate through aggregators.

From the Taker side, the overall on-chain situation is relatively pessimistic. In the industry winter, as overall trading volume and TVL shrink, the number of real users on-chain has plummeted, and the main trading volume has returned to leading platforms. In terms of token trading pairs, the proportion of mainstream token trading has rebounded, while long-tail assets are in a "frozen period."

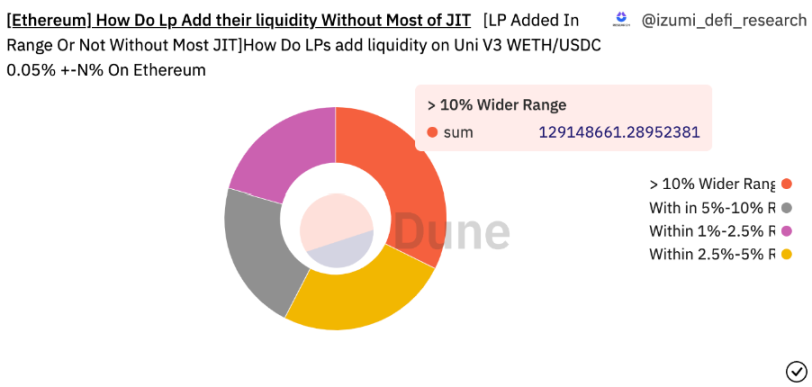

From the LP side, the Uniswap V3 WETH/USDC 0.05% pool sees most liquidity providers adding LP within a range of 10%.

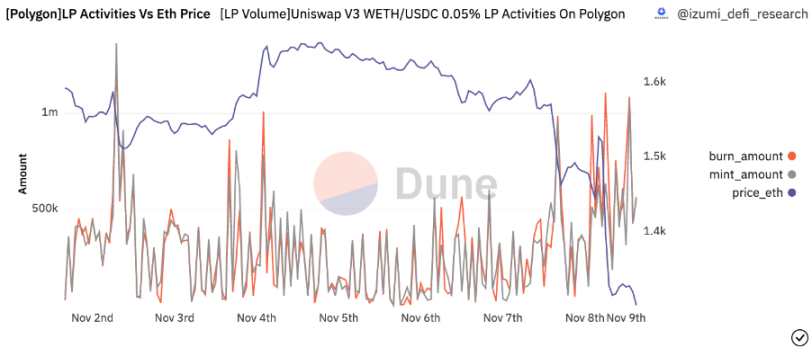

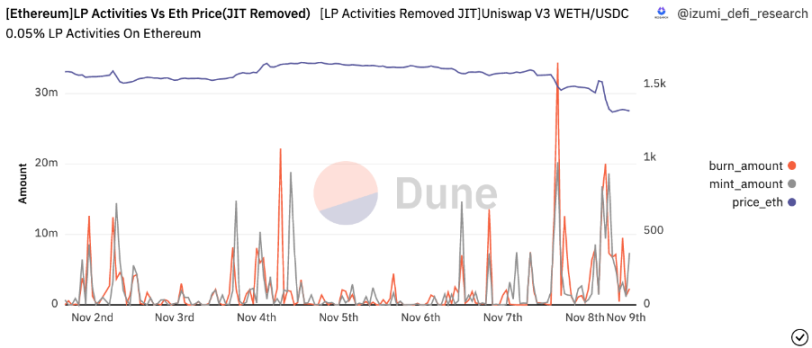

At the same time, liquidity providers in this pool adjust their positions relatively infrequently. Comparing the activity of LPs on Polygon (above) and Ethereum (below), it is evident that adjustments on Polygon are more frequent.

The above chart shows the LP activity for the Uniswap V3 WETH/USDC 0.05% pool on Polygon, where Mint and Burn represent the dollar amounts added and removed from LP. When viewed alongside the deep blue Ethereum price curve, it is clear that LPs on Ethereum are less sensitive to price fluctuations compared to liquidity providers on Polygon.

Overall, in a highly volatile market, trading volume and active real users on Uniswap V3 have decreased, but liquidity providers remain active, and DEX maintains good liquidity. Additionally, due to factors like JIT liquidity (short-term liquidity supporting large trades), overall trading liquidity is actually better.

However, in terms of overall user experience, Uniswap V3 still has too much room for improvement, such as issues with MEV attacks, slippage, uncertain trading execution results, and user experience problems like not supporting limit orders and complex wallet management. These issues may not necessarily be solved by the underlying DEX. Traditional financial markets also have a second-layer structure: users do not trade directly on NASDAQ but through brokers, who are the distribution channels for traffic and funds.

Here, DEX is like NASDAQ and other exchanges, while aggregators are like brokers, serving as channels to solve user experience issues. In the latter part, we track the current status and future plans of 20 DEXs and aggregators from the perspectives of products, narratives, and planning to study the development trends of DEXs.

What Does the Future Hold? A Look at the Future Landscape of the Trading Track from 20 Innovative DEXs/Aggregators

In the first part, we studied the overall situation of the leading DEX - Uniswap V3 on Ethereum from a data perspective. These data only represent a part of the present and past of DEXs. To see the future direction of DEX evolution, we have compiled the recent product and market developments of 20 DEXs. From their product design and narratives, we observe the following trends:

1. The Emergence of Multi-Chain Ecosystem CL-AMM DEXs and the Professionalization of Market Making

Recently, we have seen several other public chain ecosystems, in addition to Uniswap V3, emerging with similar products, such as Ref Finance V2 in the Near ecosystem and Arctic in the Aurora ecosystem, both supported by iZUMi Finance. Other examples include Traderjoe V2 and Quickswap V3, which draw on iZUMi's DL-AMM design, as well as MoveX in the Sui ecosystem and Duality in the Cosmos ecosystem. Whether it is the technical upgrades of old DEXs to the original liquidity deployment methods or new DEXs, they all adopt a concentrated liquidity model, allowing liquidity providers to provide liquidity within custom price ranges. Additionally, there are technical providers like Algebra that help DEXs achieve upgrades (Quickswap V3 is implemented with underlying technology provided by Algebra).

From the market-making situation of Uniswap V3 and recent discussions on Twitter involving Friktion Labs and Uniswap Labs, as well as iZUMi Research's previous analysis of on-chain LPs, Why shouldn't you be the liquidity providers on Uniswap V3 for now? | by iZUMi Finance | Medium

Although the openness and disorderly permissiveness of DEXs allow ordinary people to participate in liquidity provision businesses that were traditionally only accessible to professional market makers, achieving "everyone is a market maker," liquidity mining is also a new way of distributing rights. The all-range liquidity operation of Uniswap V2 is simple and easier to combine with liquidity mining and other DeFi modules. However, in reality, most liquidity providers are losing money overall. The emergence of concentrated liquidity in Uniswap V3 has made liquidity provision more complex and professionalized. With the recent emergence of many DEXs featuring concentrated liquidity designs across multiple ecosystems, considering the unique on-chain environment (including transaction confirmation delays, MEV, fee mechanisms, slippage, etc.), as well as the mathematical calculations and characteristics of the AMM model being completely different from traditional order books, we can expect more market-making teams focusing on providing professional liquidity services in concentrated liquidity DEXs in the future.

Currently, major professional market makers are concentrated on major coin types, while long-tail coins, due to the complexity of adjusting positions and difficulties in incentivizing liquidity providers, generally still adopt the V2 all-range liquidity combined with liquidity mining approach. In the future, considering the high efficiency of concentrated liquidity and the demand for on-chain native trading (such as GameFi, which inherently requires on-chain trading scenarios), concentrated liquidity service solutions around long-tail coins will gradually mature. iZUMi Finance has positioned itself as a liquidity service platform from the beginning, launching the LiquidBox incentive tool for concentrated liquidity, combining various strategies with different liquidity ranges to allow project parties to achieve better on-chain liquidity with less intervention and lower costs.

2. Clear 2C Trend, Pursuing Traffic, and Upgrading User Experience

Leading DEXs are focusing on enhancing traffic, including improving user experience on mobile and web platforms to achieve traffic exposure. Among them, after acquiring the NFT aggregation market Genie, Uniswap integrated Sudoswap to upgrade its web app. DoDo is promoting large-scale landing applications while marketing in both Web3 and traditional traffic channels, achieving gasless trading and limit order functions to capture more users. Additionally, Sushiswap has implemented gasless limit trading, and DEXs in the Solana ecosystem and multi-chain wallets like Chainge are emphasizing mobile platforms.

In terms of trading user experience, they are approaching CEX levels of professionalism. Uniswap, Pancakeswap, and others have recently introduced price charts to free users from the hassle of using additional K-line tools. iZUMi Finance will soon launch iZiSwap Pro, which, in conjunction with DL-AMM, combines AMM and limit order features to bring the front end closer to CEX, creating a decentralized Binance.

On the Maker side, most all-range liquidity DEXs offer a Zap feature for one-click liquidity exchange. Furthermore, at the recent hackathon in San Francisco, a team guided by the iZUMi team achieved third place with a one-click LP generation solution for Uniswap V3. iZiSwap provides one-stop liquidity services for project parties through the V3 liquidity incentive tool Liquid Box and accompanying market-making strategies.

3. Hybrid AMM + RFQ + LOB

While AMM adapts to the complex on-chain environment, it also brings many issues, such as uncertain trading results, slippage, and susceptibility to various forms of MEV attacks. To reduce the impact of MEV, there are numerous solutions and attempts from the network layer to the protocol layer, but none are completely effective.

Limit orders can avoid these issues with AMM. Aggregators/DEXs like 1inch, DoDo, and Sushiswap have introduced limit order functions, and Pancakeswap has implemented limit orders through Gelato. iZUMi Finance's iZiSwap is designed to be compatible with both AMM and limit orders through DL-AMM.

However, traditional limit orders face issues with front-running trades. Currently, most aggregators adopt centralized limit order solutions, which still encounter such problems. iZUMi's DL-AMM directly implements an on-chain order book and does not significantly increase gas costs compared to general AMMs, making it the best solution available.

Additionally, Binance's latest offerings like Hashflow, 0x's Matcha, and several projects in the primary market all adopt RFQ mechanisms, where users submit trading requests, and the platform provides quotes off-chain through oracles or market makers, followed by on-chain atomic swaps, eliminating slippage and providing trading certainty. However, such mechanisms cannot achieve price discovery, as the price discovery mechanism relies entirely on oracles and other price inputs; essentially, GMX also belongs to this type.

4. Financial Products Based on DEX, Liquidity Bundled and Sold by Trading Platforms

In the previous section on DeFi on-chain funds, our research team also mentioned this trend. At that time, the case was Umami Finance obtaining yields through GLP and hedging the exposure of GLP's volatile asset portion through Mycelium (formerly Tracer DAO), providing users with a 20% annualized return in USD terms. Ultimately, this product was closed due to Mycelium's poor performance during price volatility.

Concentrated liquidity, represented by Uniswap V3, is a very flexible type of asset that can simulate the effects of other derivatives. For example, by deploying liquidity in a price range at the current price and holding an equivalent amount of spot assets, one can simulate a call option. Moreover, the dual-currency wealth management products offered by traditional CEXs, which employ low-buy and high-sell strategies, essentially use certain market-making strategies to provide users with returns. DEX's LP tokens can fully realize similar products and provide equivalent levels of returns. These products essentially deploy users' funds according to specific strategies on concentrated liquidity DEXs, earning fee income, and finally settling according to agreed rules, satisfying specific user needs while achieving growth in DEX liquidity, which is a win-win strategy. iZUMi Finance is currently experimenting in this area and will soon launch related wealth management products.

What Will the Future of DEX Look Like?

This is a question we continue to ponder. DEX protocols themselves, as underlying infrastructure, possess good openness, and a series of products and services will emerge based on DEX protocols like Uniswap and iZUMi Finance's iZiSwap. The trends mentioned in this section also indicate that a dual-layer architecture of aggregators + DEXs will achieve distribution of traffic and liquidity on the C-end; at the same time, the front-end experience will approach that of CEXs, while the back-end will provide professional one-stop liquidity services and accompanying financial derivatives. In this supply chain, there will be many opportunities at various stages, which can take the form of products or services.

Any centralized entity will carry the risk of single points of failure. As BitMEX founder Arthur Hayes mentioned in his latest article "Speechless":

"Centralized exchanges will always face these issues of mistrust on behalf of their customers; FTX was not the first high-profile exchange to fail, and it won't be the last."

The asset transparency, security, and non-custodial nature provided by DEXs, combined with their open and composable characteristics, will prove their reliability as centralized institutions continue to rise and fall.

Risk warning

Risk warning Risk warning

Risk warning