Please answer 2018: That era of chaos and strange forces

"I don't understand bull markets, but I know bear markets very well." — A small investor who entered at the peak in 2018 said.

"I don't understand bull markets, but I know bear markets very well." — A small investor who entered at the peak in 2018 said.Author: Hippy, Foresight Research

0. Preface

Recently, many old friends have talked to me about "dreaming back to 2018," and many veteran investors have started writing "Survival Guide for Bear Markets." More new friends who entered the market during this bull run are eager to know what the market will be like. Seeing the eager eyes of these new friends reminds me of myself in 2018, listening to veteran investors bragging, filled with confidence about the future market, yet unaware that a long three-year bear market awaited me.

Of course, writing this article does not mean we predict that the future market is about to enter a bear market; we are simply reminiscing about what the cryptocurrency market was like in 2018 and thinking together about how participants in the cryptocurrency market can "Live long and prosper" through the ups and downs of the cycle.

1. Market Overview ------ An Era of Chaos and Confusion

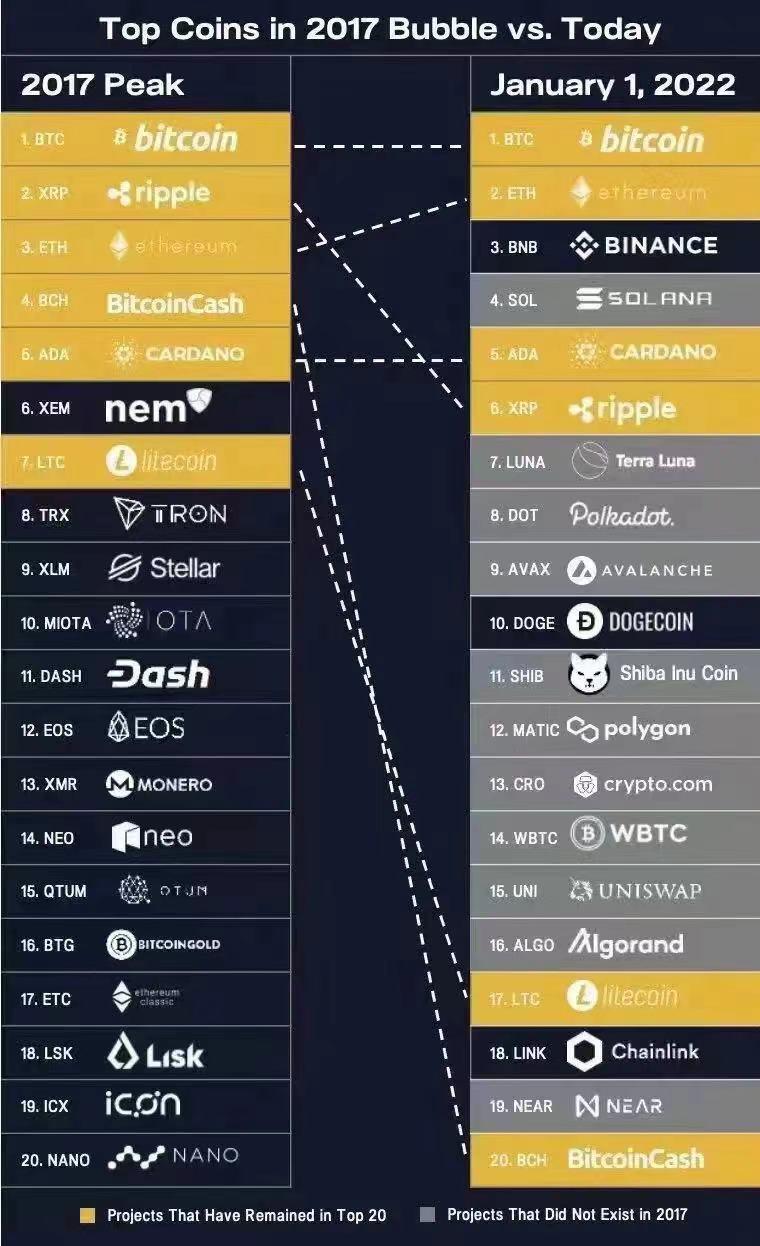

The peak of the secondary market occurred in January 2018, with the total market capitalization of the cryptocurrency market exceeding $800 billion, about one-third of the ATH in 2021. At that time, the market was flooded with altcoins, and Bitcoin's market share reached a low of 33.39% on the day of the market cap peak, still immersed in the bubble of the ICO wealth creation myth. Looking back at the top 20 cryptocurrencies by market capitalization at that time, they were all various public chain tokens and Bitcoin replicas, while now only six cryptocurrencies remain on the list, with eleven new ones emerging.

Public Chains/Protocols

First, there was a reshuffling in the public chain/protocol market. The market from 2017 to 2018 mainly stayed in the infrastructure development stage, with public chains and protocol layers being the focus of market attention, with sharding, DAG, BFT, and various Proof of Bullshit emerging endlessly. Each public chain attempted to solve the "impossible triangle" of "efficiency, security, and decentralization" using various methods.

Overview of Public Chains in the First Half of 2018

In such a market environment, primary market investors would typically start with consensus standards and end with TPS. Today, they study how directed acyclic graphs solve asynchronous problems, and tomorrow they ponder how Byzantine generals achieve peer-to-peer communication. However, most public chains were still in the early development stage, with very few projects launching their mainnets. Primary investments could only start from the angel stage, but no one knew if they could be realized. This market environment gave rise to a large number of pseudo-technical projects, where a white paper and a few advisors could start fundraising, and project due diligence could only look at technical solutions without any data or developed products to verify. Everyone was looking for the next generation of public chains beyond BTC and ETH; in 2018, someone told me it was called EOS.

(Foresight Ventures remains optimistic about the Cosmos ecosystem and various new public chains)

In addition to general-purpose public chain solutions, many projects chose to take a different path, adopting vertical solutions aimed at specific application scenarios, such as public chains for IoT, storage, and privacy use, as well as protocols targeting data, security, transactions, and more. Most projects remained before launching their mainnets, or even in the early development stage, with only a small portion actually being completed. The lack of infrastructure led to a shrinkage in application layer demand, with few uses beyond transfer payments, clearing settlements, and using ETH smart contracts for ICO token issuance. As for scenarios like traceability, identity verification, and distributed computing, they were even harder to solve.

Overview of Protocols in the First Half of 2018

Of course, among these projects, there are still many teams that have endured the trials of the bear market and are still developing and working. Ultimately, they have settled into the blue-chip giants we see today, as well as the basic components we commonly use.

Chain Reform

After the wealth creation effect of ICOs spread across the country, many traditional industry companies sought to solve their industry or internal problems through blockchain technology, leading to a rapid rise in the trend of "chain reform." Among them are many insightful individuals eager to engage in the technological revolution, as well as opportunists looking to profit from the hype. The chain reform trend spanned various sectors, including P2P, mobile, e-commerce, traceability, AR/VR, SaaS, gaming, etc. It seemed that blockchain could solve all the pain points that could not be addressed online or offline, but for most projects, the ultimate problem solved was actually just one— the financial issues of the project parties.

Trading Mining

After a slight decline in market sentiment, most investors began to consider investing in projects that could generate cash flow, with exchanges becoming the preferred choice. The "trading mining" exchanges led by Fcoin emerged. To achieve a cold start for the exchange, Fcoin issued FT tokens based on users' trading volumes to incentivize trading. At that time, the yield was only around 30-40% annualized, but users who had never experienced yield farming flocked in. As the hype soared, the FT token skyrocketed a hundredfold in a few weeks, only to crash rapidly due to flaws in the mining mechanism design. However, this innovative model was carried forward, and many exchanges began to use "trading mining" as a selling point for platform token fundraising. Like internet companies, exchanges competed on long-term product and operational capabilities, as well as the discovery and capture of quality assets. Most of the following exchanges were short-lived, with only a small portion surviving.

Death Spiral

After the secondary market reached its peak, the primary market "prospered" for half a year through various bizarre hot topics. By August 2018, the most thrilling part of the bear market arrived—the ETH death spiral. Due to the previous bull market, many projects had raised funds using ETH, resulting in project parties and primary investment institutions holding a large amount of ETH that had not been liquidated. When ETH began to decline, investors started to sell, and project parties also reduced their holdings. As the anchor of the altcoin market, ETH's decline triggered a market-wide downturn. Project parties, investors, and traders began to reduce their holdings of various altcoins, initiating the death spiral. ETH plummeted from $400 to $200, halving in value, and after two months of sideways movement, it fell to $89, marking the complete death of the primary market. Most investors experienced a 50-80% drawdown in their original accumulation from the previous bull market, and the glory of ICOs had long vanished.

STO, EOS/Tron dApp, and Others

During the two months of sideways movement in the market, the primary market also attempted some small activities: first, there was the compliant ST (Security Token) and STO (Security Token Offering), which is essentially a form of asset tokenization. This is the process from asset-backed security to asset-backed token. It has assets or cash flow as value support, but it is essentially another form of ICO that aligns with regulatory requirements. Given the market downturn at that time, the issuance demand in the primary market had begun to shrink, so the concept of STO ultimately did not gain traction.

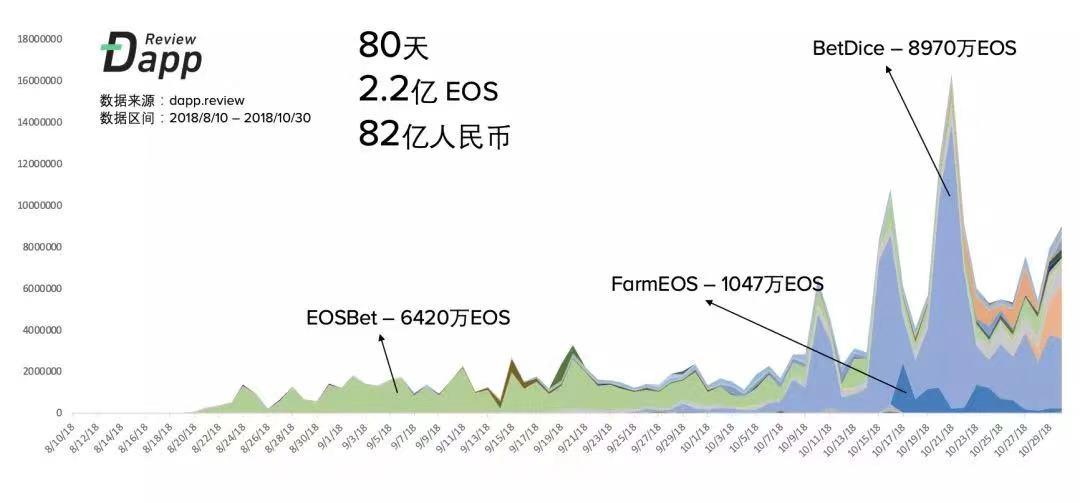

Secondly, there was the explosion of EOS dApps, with a large number of gaming and gambling projects appearing on the EOS chain. The EOS dApp represented by BetDice generated a turnover of 8.2 billion RMB in just two months and attracted hundreds of thousands of users. Decentralized exchanges, wallets, mining bots, and other related services built on EOS rapidly developed, leading to a speculative frenzy over EOS RAM. This was the first time an application-driven ecosystem ignited the entire public chain ecosystem. However, projects on EOS were primarily gambling-oriented, with gambling dApps accounting for 90% of total trading volume, and their user lifecycles generally remained under one month. The competition for existing funds led to the rapid collapse of the EOS application ecosystem. Later, Tron copied EOS's model in an attempt to continue its glory, but within weeks, its user data and activity also saw a dramatic decline.

After Bitcoin maintained a sideways movement around $6,000 for three months, it quickly plummeted to $3,000 in November. The primary market then entered a phase where there was nothing left to speculate on, and the most despairing moment was about to arrive.

2. Market Participants ------ To Persist or to Leave

Exchanges

Exchanges are among the participants in the cryptocurrency industry with the best cash flow and are also the ones that survive the longest in bear markets. As channels for asset issuance and circulation, exchanges occupy the upstream of the entire industry chain. However, in a bear market, assets do not create wealth effects, spot trading volume has severely shrunk, and users' trading habits have shifted from buying coins to trading contracts, leading to the emergence of many contract trading exchanges.

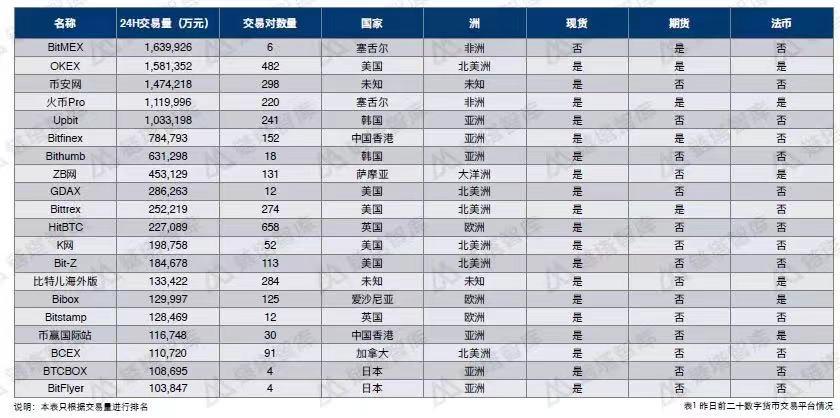

Trading Volume Rankings of Exchanges in April 2018

The above chart shows the trading volume rankings of exchanges in April 2018. It can be seen that BitMEX, which focuses on contract trading, ranked first, followed by the three major domestic exchanges and regional exchanges overseas. BitMEX and OKEX were among the first to launch contract trading features and were the choices for most people to engage in contract trading at that time. In the second half of 2018, most exchanges began developing contract trading businesses. Huobi launched its contract trading section, Huobi DM, at the end of 2018, and Binance began its USDT perpetual contract business after acquiring JEX in September 2019. In terms of spot trading, Binance pioneered the Launchpad concept in the first half of 2019, and subsequently, major exchanges began to launch their own IEO replicas, leading to a wave of IEO activity independent of the broader market.

During the years 2018-2019, leading exchanges largely maintained their original positions, with Binance gradually rising to the top through innovative operational methods and management models. For smaller exchanges, some were able to maintain existing customers to continue generating revenue, while others gradually ceased operations in a shrinking market.

Project Parties

Before discussing the situation of project parties, let's first look at the financing situation of projects during the bull market. The following chart shows the public fundraising data of the top ten projects before 2017. It can be seen that the valuations and fundraising amounts of projects at that time were substantial, with large projects raising amounts typically between tens of millions to hundreds of millions of dollars. By the first half of 2018, a valuation of $100 million had become standard for early-stage white paper projects. Therefore, for project parties raising funds during the bull market, most projects did not face funding issues.

Top Ten Digital Asset Crowdfunding Projects by Fundraising Amount in 2017

Here, we categorize project parties into three types: those that have raised funds and issued tokens, those that have raised funds but not issued tokens, and those that have not raised funds.

For projects that have raised funds, those that issued tokens in the first half of 2018 generally did not need to consider market cap management and maintenance issues, as a large amount of capital was still entering the market. There were numerous projects that cashed out at the peak, represented by EOS. Blockone can be considered a master of cash management, selling raised funds for cash and U.S. Treasury bonds at the market peak, successfully avoiding the bear market. Some project parties did not sell, and after experiencing the ETH death spiral in August, their funds significantly shrank. Some teams chose to abandon price maintenance and focus on development, while more project parties opted to completely give up and let things fall apart. Project parties that failed to issue tokens in the first half of the year began to delay or abandon token issuance, commonly referred to as "running away." For project parties that had not yet raised funds, most changed their project direction, with some choosing to leave the blockchain industry and return to traditional markets, while others transitioned to industry blockchain, providing some To G services.

Institutional Investors

The primary market in 2017 was mainly dominated by individual participants, while in early 2018, a large number of token funds and traditional VC firms began to enter the scene. The quality of these institutions varied, with some coming from traditional finance and internet sectors as professional investors, while others were early cryptocurrency players and large holders with original accumulations. The following chart lists some well-known domestic investment institutions at that time, while overseas there were A16Z, Pantera, Hashed, Kenetic, and others. Comparing this with the current list of investment institutions, it can be seen that most domestic institutions have exited the historical stage, and the reshuffling of primary market participants has been quite thorough.

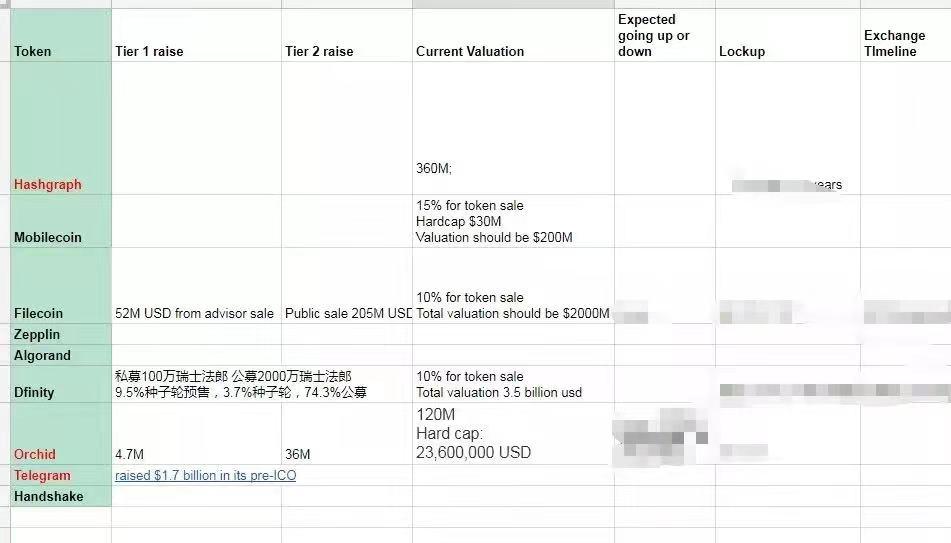

The iteration of institutions was not very apparent in the first half of 2018. Everyone had basically made a fortune in the previous wave, and as long as they could get allocations, they could make money. Fundraising, exiting, and cashing out were not issues. However, as the market declined, many projects experienced price drops, zero valuations, or even failed to issue tokens. A large number of institutions without investment capabilities faced situations where they could not exit from the projects they had previously invested in, leading to a wave of rights protection in the primary market. Many SAFT agreements were resold in the secondary market, including notable projects like Filecoin, Algorand, and Dfinity, which later surged a hundredfold or more. Institutions that still had faith in the market and investment capabilities began to transition. In addition to seeking funds from project parties, some funds started to find ways to create cash flow, making secondary asset management and quantitative trading popular choices.

SAFTs Resold by the End of 2018

Media, Communities, and Other Service Institutions

For service institutions, the downturn in the primary market was devastating. Market hotspots cooled, fundraising shrank, and project parties went silent, leading to a rapid decline in demand for media promotion and public relations. Service institutions lost their main clients and sources of income. As the wealth levels of all market participants declined, the interpersonal networks and resource relationships accumulated in the past gradually lost their effectiveness. The original investment communities began to run away and dissolve, and investment exchange communities gradually transformed into contract trading groups. Service institutions without cash flow and income began to exit the historical stage.

3. Investment Logic ------ Transition from Speculative Paths to Research Paths

I started learning about the cryptocurrency market in early 2018. Before entering this industry, I worked in securities research, firmly believing in fundamental analysis and dismissing technical analysis. When I began to invest in the primary market, I started by examining the principles of projects, assessing their technical solutions, consensus mechanisms, token models, release rules, and team quality. Although I did not come from a technical background, I still read a large number of papers, white papers, and technical articles, deeply studying commonly used solutions and filled with anticipation for the blockchain world.

Later, when I truly immersed myself in the market, I found that fundamental analysis was basically ineffective in an inefficient market. Without data support, there were only concepts and theories. In such a situation, how could one make investment judgments by retreating to the next best option? I attempted to organize the following logic from limited data and due diligence information:

• Technical Solutions: Project progress, technical heat, technical feasibility;

• Market Heat: Number of media reports, roadshow situations, community data, search indices;

• Economic Models: Token distribution plans, token functions, token unlocking situations, fundraising and valuations;

• Team Situation: Background of the founding team, background of the advisory team, background of the investment team;

However, in the actual operation of most investment funds, this investment system gradually transformed into two main points—tokens and teams. Investing became exceptionally simple; when investing in projects, only two aspects were considered: first, when the token would be listed, what the initial release ratio would be, and whether the unlocking time was reasonable; second, who the advisors were, who was investing, and who was backing the project. Thus, primary market investment turned into a thorough following behavior, with a list of institutional participants firmly in mind. Essentially, if a leading investment institution invested, others would inevitably follow suit. As the primary market continued to shrink, the above logic ultimately devolved into a market-making logic. Incubation, market-making, and market cap management became the last means of harvesting the existing market.

As the market slowly recovered over the two years and various data statistical tools emerged, fundamental analysis finally found its place in the cryptocurrency world. During the DeFi Summer of 2020, through the exploration of on-chain data, trading data, business models, and project mechanisms, research-driven investors finally made money for the first time. The cryptocurrency market gradually transitioned from inefficiency to efficiency, and the holy grail of investment no longer bowed to market makers but leaned towards those who genuinely worked hard to research and build.

4. What Have We Gained?

By sorting through the investment hotspots, market participants, and investment logic of the bear market, and comparing them with the current market situation, we can easily draw the following conclusions:

1. Market volatility is enormous, and both investment targets and market participants have undergone significant reshuffling. The industry's beta is high, but how to maintain beta profits through the bear market is challenging, requiring strong investment capabilities and foresight in market trends. Over 90% of those without capability were eliminated during the bear market, and over 90% of unreliable projects were discarded by the market. Only the essence of the industry remains after the storm.

2. The market is improving and becoming more efficient. With the global recognition of cryptocurrencies and blockchain technology, a large number of professional investment institutions and capable industry builders have continuously entered the cryptocurrency industry over the past few years. Fraudulent projects are becoming fewer, while teams that get things done are increasing, leading to significant changes in industry participants and fundamentals.

3. The market rewards long-termists and those who work hard to build. One must have firm faith; persistence leads to victory. 2018 was just the beginning of the bear market, and the most painful stages were actually in 2019 and 2020, when the entire market was in a semi-dead state. When market participants could no longer expand their businesses from any angle, their faith in blockchain would collapse. I believe everyone still in the industry at that time repeatedly asked themselves these questions: Is Bitcoin a tulip bubble? Will the bull market return? Most people's hopes faded away in waiting. However, during this period, there were always some long-termists who continued to work on projects, continued to invest, and supported projects. They dared to invest their time or money into things they believed in, and among these people, some became leading institutions, while others became blue-chip projects, with the market rewarding them with a hundredfold or thousandfold return.

5.

Finally, let me share a little story with everyone: On April 19, 2019, my colleagues and I had a meeting with a guy whose WeChat profile picture was a curly-haired kid. He told me they were going to create a contract trading exchange, and after listening, I felt it was no different from BitMEX's model. So I asked him several questions related to the issues BitMEX encountered, but he couldn't answer them well. I checked their website for trading data and found there were only a few trades per day. Coupled with the cold market conditions, we were not planning to make more investments in the primary market, so we quickly passed on the project. Later, I saw him again during a live stream of a hearing in the U.S., and his name tag read "Mr. Bankman-Fried."

In the end, I hope everyone can survive in future market cycles; plant seeds in the bear market and reap rewards in the bull market.

Data Sources:

Huobi Research Institute "Global Blockchain Industry Panorama and Trend Report (First Half of 2018)"

Chain Tower Think Tank "2018 Digital Currency Exchange Research Report"

DappReview "80 Days, 8 Billion: The Underlying Currents in the Winter—The EOS dApp Ecosystem Explosion You Don't Know About"