HashKey Hao Kai: Analyzing the Reasons and Impacts of the Price Difference Between Grayscale GBTC and Bitcoin

Allowing redemptions may be the most direct and effective way to fix the GBTC discount, but Grayscale is trying to address it by converting to an ETF.

Allowing redemptions may be the most direct and effective way to fix the GBTC discount, but Grayscale is trying to address it by converting to an ETF.This article is from HashKey Research, author: Hao Kai, reviewer: Zou Chuanwei.

Recently, Grayscale CEO Michael Sonnenshein stated that converting to an ETF could resolve many issues with the Grayscale Bitcoin Trust. He mentioned that by converting the Bitcoin Trust into an ETF, the disconnection between the price of GBTC and the Bitcoin (BTC) it holds could be rectified. From the perspective of the built-in arbitrage mechanism of ETFs, any discount or premium of the stock relative to the ETF's net asset value will be offset.

From this statement, we can see: first, there is a price difference between GBTC and BTC, and this difference has become very apparent; second, Grayscale believes that a change is necessary; third, converting the Bitcoin Trust to an ETF is a feasible solution. In the cryptocurrency space, the Grayscale Bitcoin Trust is the largest and most well-known Bitcoin investment product, thus requiring in-depth research into the price of GBTC.

Why is there a price difference between GBTC and Bitcoin?

The operational mechanism of the Grayscale Bitcoin Trust has been detailed in "The Design and Impact of Bitcoin Financial Products" (2021, Issue 4, No. 101). Qualified investors give BTC or USD (to purchase BTC) to Grayscale and receive a corresponding amount of GBTC (approximately 1000 shares of GBTC for each BTC). After waiting for six months, qualified investors can sell GBTC on the secondary market, but they cannot redeem their BTC or USD from Grayscale using GBTC.

The price difference between GBTC and BTC is mainly the result of the interplay of arbitrage mechanisms and market sentiment. The product structure of the Grayscale Bitcoin Trust is one-way, with BTC flowing in but not being redeemable. Therefore, the arbitrage mechanism of the Grayscale Bitcoin Trust is not smooth, which is the fundamental reason for the price difference between GBTC and BTC. Qualified investors can obtain GBTC directly from Grayscale, while ordinary investors can only purchase it on the secondary market, making market sentiment an important factor. The cryptocurrency market is an emerging market, and ordinary investors typically lack professional investment knowledge and experience. Additionally, the price volatility of cryptocurrencies can easily lead to emotions of greed or fear among investors, significantly impacting the price of GBTC. For example, if ordinary investors suddenly increase their purchases while the amount of GBTC sold by qualified investors is limited, GBTC will experience a significant premium in the secondary market. Conversely, if ordinary investors suddenly decrease, it means fewer investors are buying GBTC on the secondary market, leading to a discount.

When did the price difference start to appear?

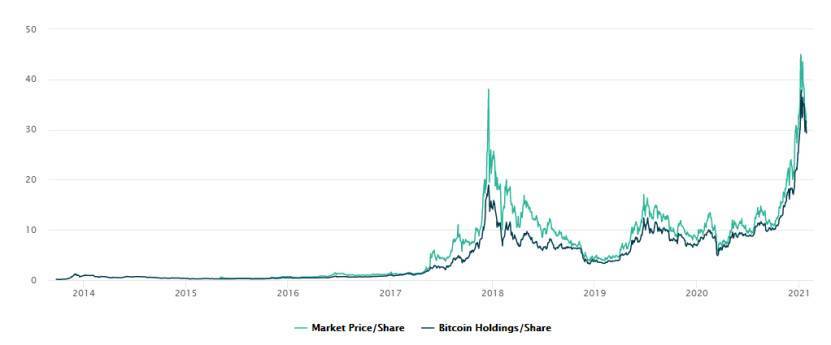

As shown in the figure below, due to the separation of the primary and secondary markets, GBTC has long existed at a premium, meaning the price of GBTC is higher than its corresponding BTC price.

Figure 1: Market Value of Grayscale Bitcoin Trust Shares vs. Actual Value of Bitcoin

When GBTC is at a premium, rational investors should buy BTC directly instead of purchasing GBTC at a higher price on the secondary market. So why are there still many investors willing to buy GBTC on the secondary market when it is at a premium?

First, GBTC is a compliant product, which is relatively rare in the cryptocurrency space. Buying and holding GBTC can avoid regulatory uncertainties and tax uncertainties. If investors want a regulated BTC trading product, GBTC is a very suitable choice. However, Grayscale only targets qualified investors, with a minimum investment amount of $50,000, which is a high barrier for ordinary investors. Therefore, ordinary investors can only settle for purchasing the regulated compliant product GBTC on the secondary market.

Second, the recent heat in the entire cryptocurrency market has attracted many new investors. They lack professional knowledge of cryptocurrencies and find it difficult to identify malicious fraudulent projects. Choosing GBTC can avoid this issue, and they do not need to deal with technical issues such as cryptocurrency wallets and private keys.

Third, secondary market investors hold an optimistic view of GBTC's price trend. They believe that the price of GBTC will continue to rise, and the premium will remain, allowing them to profit from the premium when they sell in the future. Additionally, GBTC has a relatively large trading volume and sufficient liquidity, leading investors to feel that selling in the future will not be difficult.

Why has it turned into a discount?

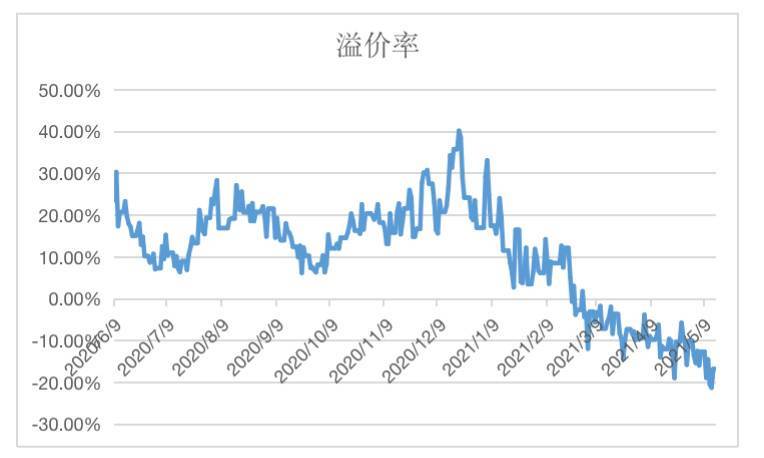

Since the price difference between GBTC and BTC has long existed, why has Grayscale only recently indicated a desire to make changes? This is because GBTC has long maintained a premium, but since around February of this year, GBTC has been at a discount (negative premium) for several consecutive months, even exceeding -20% at one point, as shown in the figure below. This situation has never occurred during the operation of GBTC.

Figure 2: Premium Rate of GBTC Over the Past Year

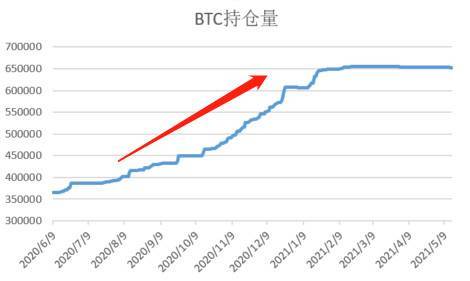

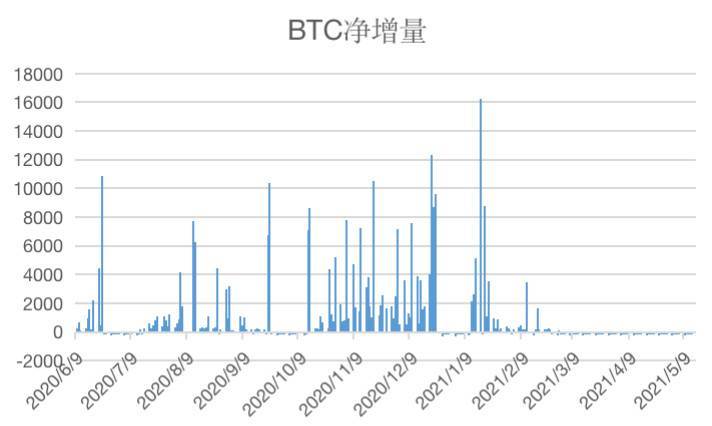

From the following two figures, it can be seen that the number of Bitcoins held by Grayscale surged in 2020, with inflows exceeding the Bitcoin mining output during the same period. This was particularly evident from August to December, with many days seeing a net increase of over 5000 BTC. Since GBTC has a lock-up period of 6 months, this means that starting from February 2021, a large amount of GBTC would continuously unlock and flow into the secondary market. However, the number of investors in the secondary market did not increase correspondingly, resulting in supply far exceeding demand, thus shifting from a premium to a discount.

Figure 3: Number of BTC Held by Grayscale Over the Past Year

Figure 4: Daily Net Increase of BTC Held by Grayscale Over the Past Year

At the same time, the price of BTC has increased significantly over the past year. As shown in the figure below, during the period when GBTC was at a discount (the red box), the price of BTC was at least above $30,000, while the price when purchased 6 months ago (the blue box) was around $10,000. This means that for qualified investors who purchased GBTC from Grayscale, even with a 20% discount, they are still making significant profits in fiat currency terms. Therefore, this level of discount does not affect their decision to sell GBTC.

Figure 5: Price Trend of BTC

Moreover, the premium rate of GBTC is also correlated with the price of BTC. When the price of BTC rises, market sentiment becomes overly optimistic, leading to an increase in GBTC's premium; conversely, when the price of BTC falls, market sentiment becomes cautious, resulting in a decrease in GBTC's premium. Recently, the trend in the cryptocurrency market has weakened, which has also somewhat reduced the demand for GBTC among secondary market investors.

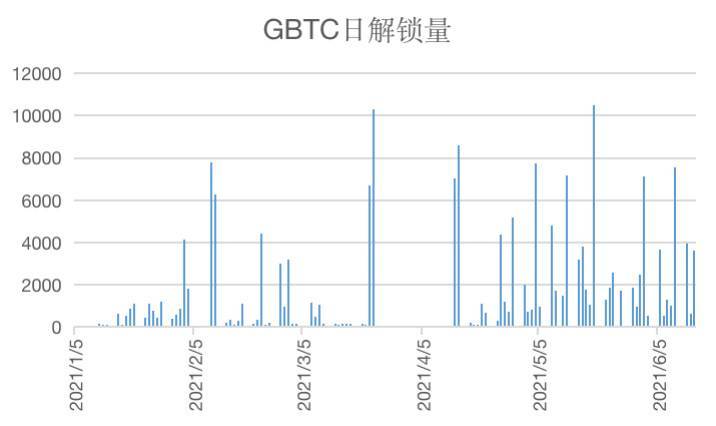

The figure below shows the daily unlocking amount of GBTC. It can be seen that there will continue to be a large amount of GBTC unlocking in May and June, which will help stabilize the price of GBTC in the secondary market, and GBTC may continue to maintain a discount.

Figure 6: Daily Unlocking Amount of GBTC

What impact will the discount have?

The product characteristics of the Grayscale Bitcoin Trust determine that the amount of BTC it accumulates will continue to increase, currently exceeding 650,000. The Grayscale Bitcoin Trust essentially acts as a forced lock-up, reducing the selling pressure of BTC and gradually becoming a powerful bullish force in the cryptocurrency market. During bullish cycles, Grayscale's purchases of BTC often spark discussions and enthusiasm. However, everything has two sides; if GBTC cannot reverse the discount situation for an extended period, Grayscale's influence may backfire and affect investor confidence.

According to data released by Grayscale, most of its clients are institutions. Institutional investors pay attention to controlling risk exposure and are more likely to engage in arbitrage through Grayscale. They buy GBTC while simultaneously shorting BTC (such as through CME's BTC futures). When GBTC unlocks, they can sell it on the secondary market and profit from the premium. If GBTC shifts from a premium to a discount, these institutional clients will stop buying GBTC. It is worth noting that if these institutions borrow BTC first and then engage in arbitrage through Grayscale, the discount will directly lead to their losses.

Since GBTC cannot be directly redeemed, the price anchoring between GBTC and BTC is not entirely solid and may require a certain consensus to maintain. However, a sustained discount may affect this consensus, meaning that the extent of GBTC's discount may continue to widen. At the same time, the discount of GBTC may also directly impact the BTC trading market.

How to respond to the GBTC discount?

As mentioned earlier, the lack of a smooth arbitrage mechanism is the fundamental reason for the price difference. Therefore, when Grayscale wants to address the discount issue, allowing redemptions is the most effective method, as arbitrageurs will quickly narrow the price difference between GBTC and BTC. Allowing redemptions will have a certain impact on Grayscale. First, the Grayscale Bitcoin Trust charges a 2% management fee annually, and after allowing redemptions, this management fee income is likely to decrease. Second, if the Grayscale Bitcoin Trust does not have sufficient reserves, it may not be able to fulfill redemptions (though this scenario is very unlikely).

Grayscale is already working on solving the discount issue. In March 2021, Grayscale's parent company, Digital Currency Group, announced it would purchase $250 million of GBTC, but this did not reverse the discount situation. Recently, Grayscale indicated that converting to an ETF could resolve many issues with the Grayscale Bitcoin Trust. U.S. regulators have not approved related ETF applications due to concerns that the cryptocurrency market is not transparent enough and is prone to manipulation, aiming to protect investors.

Currently, several new BTC products have emerged in the market. MicroStrategy issued convertible debt and used the raised funds to purchase BTC. MicroStrategy provides a low-risk product that captures BTC value. Canada has successively launched three Bitcoin ETFs. These BTC investment products are more reasonable, as investors do not need to lock up their assets and do not bear the risk of BTC price declines during the lock-up period. At the same time, secondary market investors no longer need to purchase products with price differences.