A panoramic interpretation of the DeFi perpetual derivatives ecosystem and its development context

With the breakthrough of the underlying performance limitations of perpetual contracts, complex on-chain derivatives strategy combinations are beginning to be adopted, and perpetual options may become a new tool recognized by traders.

With the breakthrough of the underlying performance limitations of perpetual contracts, complex on-chain derivatives strategy combinations are beginning to be adopted, and perpetual options may become a new tool recognized by traders.Written by: Zheng Jialiang, Research Director at HashKey Capital

Development Context of Perpetual Derivatives

The first phase of perpetual derivatives development is the inverse perpetual contract, which is the Bitcoin inverse perpetual contract developed by Bitmex in 2016. Traditional delivery futures have mechanisms such as settlement dates, delivery, and contract rollovers. Perpetual derivatives shine through the combination of three mechanisms: staking, funding rates, and price tracking. However, it wasn't until 2020 that many exchanges began to follow suit with perpetual derivatives.

According to BitMex's research, the returns for long positions in inverse contracts are unbalanced: in markets dominated by inverse contracts, long positions are at a greater disadvantage during price fluctuations. Later, with the introduction of stablecoins, forward contracts began to replace inverse contracts due to their more linear returns. In other words, inverse contracts exhibit convexity, similar to the gamma characteristic in options. Since Bitcoin is not normally distributed and has a drift term over time, the return ratios for long and short positions are not balanced. Forward contracts compensate for the non-linear aspects of inverse contracts.

Figure: Non-linearity of Returns in Inverse Contracts

The second phase of perpetual derivatives is on-chain perpetual contracts. During the DeFi summer of 2020, on-chain AMMs became mainstream, and perpetual derivatives were launched accordingly. This second phase can be seen as the proof of concept for perpetual derivatives, with daily trading volumes reaching hundreds of millions of dollars. Due to performance limitations, it has not yet reached the stage of large-scale usage.

Source: The Block

The third phase is marked by the launch of Layer 2, which breaks through the underlying performance limitations of perpetual contracts. With the order book becoming a viable option for projects again, and the concentrated liquidity feature of Uniswap V3 bringing in professional market makers and traders, derivatives are no longer just for speculation; complex on-chain derivative strategy combinations are beginning to be adopted.

We believe that the fourth phase of perpetual derivatives will see perpetual options become a new tool recognized by traders in 2022-23. With Paradigm discussing everlasting options and some projects launching on-chain perpetual options, more protocols will participate in this non-linear game. The fourth phase will see the market start to understand the trading opportunities and combination opportunities brought by non-linear derivatives. Perpetual options solve the dilemma of liquidity being fragmented across two-dimensional delivery options. Long-tail assets will receive more attention. Additionally, due to their high volatility, they will become favored by traders.

In the end, perpetual derivatives will coexist with other delivery derivatives, giving rise to more strategies for arbitraging across non-perpetual contracts. The market will return to a multi-product state, significantly enhancing liquidity, which will lead to the stage where optimists discuss the derivatives market being much larger than the spot market (applying the TAM estimation method). Another important feature of the fourth phase is the rise of fixed-income derivatives, marking a true entry into a more institutionalized era. Interest rate products, which have not been traded before, will be filled in.

We believe perpetual derivatives have the following functions:

- A convenient tool for directional speculation. The existing perpetual derivatives in the market prove the applicability of perpetual contracts.

- A portfolio management tool. They can be combined with spot, delivery futures, and delivery options. Professional traders can construct more types of investment portfolios. Singular combinations can be built between perpetual contracts, expiration contracts, perpetual options, and expiration options.

- A means of providing fixed income. Due to the unique way perpetual contracts maintain price stability, trading purely for fund rates will inevitably flourish among professional traders, similar to carry trades in forex. In addition to portfolios constructed by professional traders, some contracts have begun to template this combination.

- A means of providing decentralized volatility trading. Utilizing the characteristics of perpetual options to mitigate delta and theta.

- A liquidity venue for long-tail tokens.

Pricing of Perpetual Derivatives

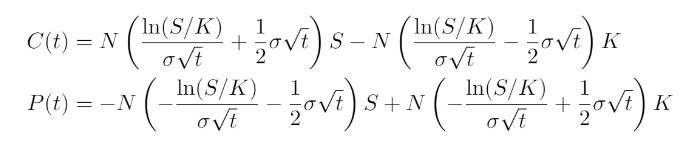

The differential form of a standard option:

S is the underlying asset, σ is the implied volatility, t is time, z is a Gaussian process, and f is the option price.

Futures can be seen as containing only the linear term:

Both futures and options can be viewed as leveraged bets on the future underlying. If boundary conditions are not included, options also contain quadratic terms (i.e., volatility) and time value. Options can be seen as containing linear terms, quadratic terms, and time terms. Futures can be viewed as an option with only the delta term, while options have additional gamma and theta terms. The logic of futures is relatively simple, with both buyers and sellers having rights and obligations. Options, due to the existence of strike prices, have a payoff function determined by the option premium; the buyer of the option has rights but no obligations, and this transfer of obligation is represented by the premium, which the seller receives while taking on the obligation to deliver at expiration.

The funding rate is the most ingenious aspect of perpetual futures contracts; all derivatives expand around their funding rates. That is, the buyer or seller of funds pays the funding rate to the other party to maintain the balance between the futures price and the underlying price (index). However, due to the increased likelihood of liquidation with highly leveraged perpetual contracts, perpetual options provide another solution: 1. They cannot be liquidated; for the option buyer, there are only rights and no obligations, and 2. They can amplify leverage without liquidation.

The main problem options need to solve is pricing, as the introduction of quadratic terms and time causes prices to exhibit convexity. The difference between the pricing of options (selling options) and the actual trading price is the source of profit in options trading.

There has been much academic discussion about perpetual options, such as the non-exercise of American call options and the analytical solutions for put options. However, the biggest barrier for users regarding options is: 1. Understanding the relationship between options and the underlying; 2. What additional benefits options provide compared to futures, allowing users to make equivalent choices between the two. Due to historical reasons and product complexity, most users start with futures.

Paradigm provides a way to express the pricing of perpetual options based on funding rates:

Deri protocol launched its perpetual options product on August 11, utilizing Paradigm's option pricing model and introducing another expression for the perpetual model:

And C(t) and P(t) are represented by the general BS model

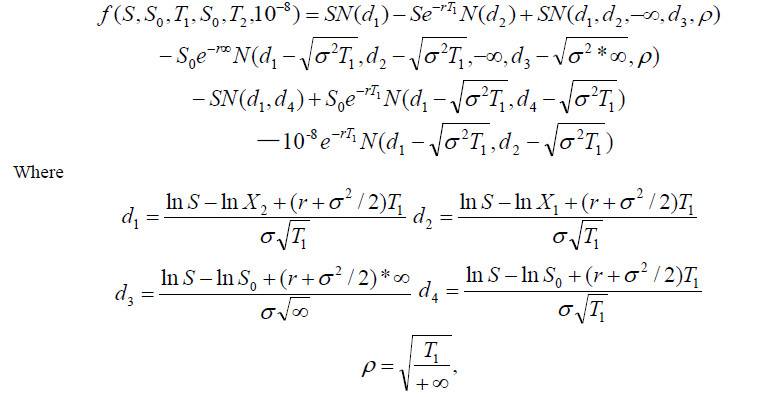

The on-chain perpetual options protocol Shield protocol has taken a step further by deriving the analytical solution for perpetual options:

The analytical solution of Shield Protocol is based on dynamic hedging verification with three years of historical data and empirical research on over-the-counter option pricing theory.

The implementation of the perpetual option pricing formula lays a foundational role for the entire perpetual product, allowing option sellers to calculate their risk exposure, which means traditional option seller strategies can be realized. The option pricing model proposed by Black, Scholes, and Merton in 1973 remains the most important method for option pricing today, with analytical solutions being the jewels of pricing, although most option pricing formulas still rely on numerical solutions due to the high computational difficulty of analytical solutions.

Major Perpetual Derivative Projects

Industry Map

dYdX

dYdX was founded in 2017 and offers cryptocurrency derivatives products including: perpetual contracts, spot and leveraged trading, lending, etc. dYdX's perpetual contracts use USDC as collateral and can cross-margin, meaning multiple contracts can use the same collateral. The funding rate for perpetual contracts is settled every hour, and dYdX's funding rate also considers the interest rate spread from two direct lending weights; its funding rate formula is:

Funding Rate = (Premium Component / 8) + Interest Rate Component

dYdX's perpetual contracts are built on Starkware's zk-rollup. zk-rollup completes customer transactions off-chain and sends the transaction results on-chain; rollup is responsible for packaging transactions, while zk provides zero-knowledge proofs to verify that deposits into layer 2 are valid. The interaction process is as follows:

- From Ethereum to Layer 2: dYdX monitors relevant Ethereum transactions, such as deposits, forced withdrawals, and forced trades. Once such transactions are received on Ethereum, related operations like adding funds will occur on the second layer.

- From Layer 2 to Ethereum: After executing a batch of transactions off-chain, the proof of their validity is generated and verified by the STARK validators on-chain. Once the STARK validators approve the state transition, the state transition takes effect, such as deposits or withdrawals from the second layer that change the user's Ethereum balance.

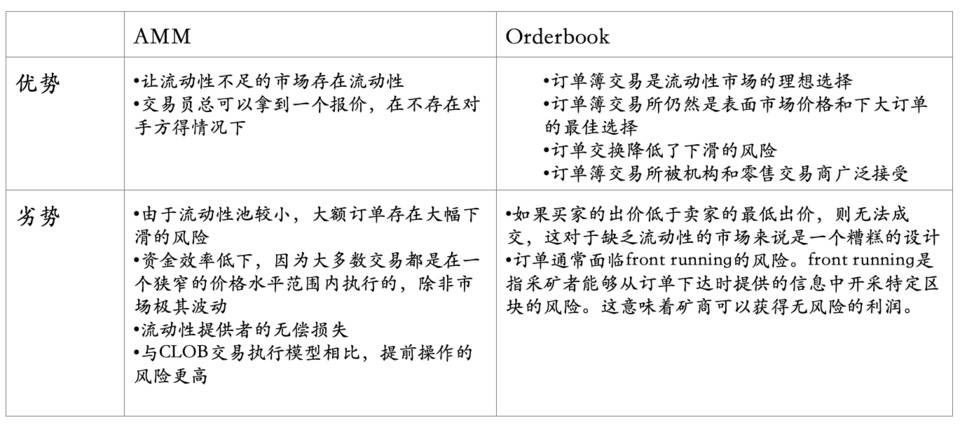

dYdX uses an order book system, which can provide limit orders, making it more suitable for derivatives. The perpetual derivatives protocol Injective compared the two mechanisms of order books and AMMs.

The advantage of the order book system is that it can provide many complex order types but still relies on market makers; for example, dYdX uses market makers like Wintermute, so the order book and market makers essentially form a system. In addition to professional market makers, general liquidity providers can add USDC to liquidity pools, allowing professional market makers to utilize this portion of USDC, distinguishing liquidity from market making, further facilitating participation from users with capital but no trading ability.

dYdX is very similar to traditional trading markets, with the biggest innovation being its API, which can provide a level similar to centralized exchanges, effectively removing the blockchain logic, leaving only what is applicable to market makers. For example, 1.25 ETH is simply 1.25, rather than the basic wei representation. From Wintermute's feedback, cross-margining is very friendly to market makers, saving a lot of capital.

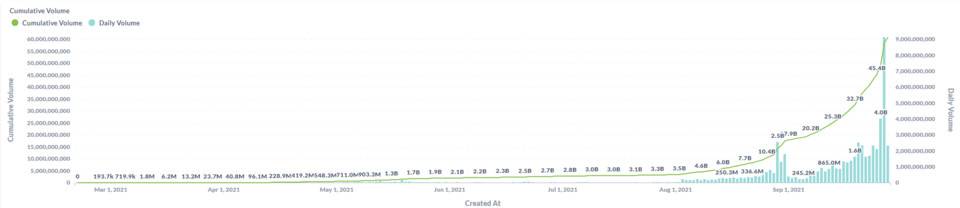

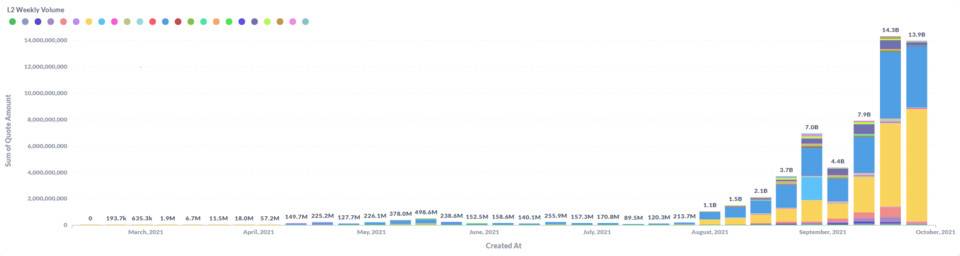

After dYdX launched Layer 2, trading volumes surged.

Daily trading volumes can reach $7 billion, but with the market downturn, it has also come down; the three largest trading pairs are BTC/ETH/SOL/COMP, etc.

Layer 2 Engine

dYdX uses the StarkEX engine, which is a trading engine developed by Starkware specifically for Layer 2 networks, launched in June 2020, supporting many use cases such as spot trading, perpetual contract trading, and NFT trading. Starkware can support both on-chain data (ZK-Rollup) and off-chain data (Validium) modes.

Source: Starkware

Users' funds are transferred to StarkEX's contracts for decentralized self-custody, allowing them to trade on dYdX. The off-chain components of StarkEX manage all trading orders and send state updates to the on-chain components after execution.

Transactions and state changes are verified by StarkEX's validators, and SHARP is a tool that packages various statements to generate proofs. Currently, the Stark engine supports several protocols, including dYdX, DeversiFi, Immutable, and Sorare.

Perpetual Protocol

Perpetual was once the largest on-chain perpetual futures market by trading volume (currently second). The V1 version of Perpetual uses a vAMM type trading pool, which is an extended type of AMM. Based on trading volume statistics, Perpetual, dYdX, and Futureswap are the top three in perpetual derivatives.

vAMM adopts the calculation method of AMM but does not use AMM's liquidation method. The K value can be adjusted; the larger the K value, the lower the slippage, and the K value must match the off-market. vAMM can utilize nearly infinite liquidity, so according to the constant product formula k=x*y, it almost does not produce trading slippage. All liquidity-poor AMM pools face issues of insufficient liquidity and excessive trading slippage. The actual liquidation in vAMM occurs at the base of Perpetual, where the insurance fund takes on the role of liquidity provider. Perpetual's v1 uses xDai as a Layer 2 solution.

The insurance fund bears the counterparty risk of vAMM (for example, when there is consistent long and consistent short). If the business does not continue to develop steadily, the growth of the insurance fund should not be sustainable. Large negative fluctuations can offset weeks of growth in the insurance fund.

In the new V2 version, Perpetual utilizes Uniswap V3's liquidity, introducing counterparties and reducing liquidity risk. The V2 version has made many other design improvements and will be divided into four steps: V2.1: Utilizing V3's concentrated liquidity for market making based on Arbitrium; V2.2: Launching a market order system and PERP staking; V2.3: A multi-collateral system beyond USDC; V2.4: A permissionless private market. In version V2.2, it will become a limit order system like dYdX. Offchain Lab believes Arbitrium can package 4,200 transactions per second, which is 300 times higher than the Ethereum mainnet.

Perp's V2 chooses Arbitrium, partly because Uniswap V3 also chose Arbitrium, as V3's liquidity pools are built on it. V3's concentrated liquidity results in smaller slippage, which is a significant advancement over Perp v1's vAMM. Additionally, compared to Optimism, Arbitrium is fully EVM compatible, allowing Uniswap to launch directly without any modifications, influencing many non-project choices. The difference between fully compatible and partially compatible lies here. At the end of May, nearly 100% of the Uniswap community voted in favor of V3 launching on Arbitrium. Many projects have begun to support Arbitrium, with over 70 projects, including Aave, Band, Hop, imToken, MakerDAO, and WBTC, choosing Arbitrum.

Perpetual Swap DerivaDEX

DerivaDEX's main product is the perpetual swap contract, which is an on-chain version similar to Bitmex.

Source: DerivaDEX

DerivaDEX uses an order book and has designed an insurance fund similar to Perpetual Protocol to protect against certain losses (such as when counterparty losses exceed their collateral). There is no special solution for liquidation; it relies on the insurance fund to resolve this, which is another mechanism created by Bitmex's perpetual contracts.

In DerivaDEX, the funding rate game can also become a trading strategy: for example, continuously constructing a long spot and short futures position, when the funding rate is favorable, a fixed funding rate can be earned (in an ideal situation).

Source: DerivaDEX

Perpetual Options Shield Protocol

Shield Protocol is an on-chain perpetual derivatives protocol whose economic logic is based on non-cooperative game theory. Its first version product is an on-chain perpetual options product, followed by the development of perpetual contract products, over-the-counter options, and structured products. It features non-collateralization, transparency, no intermediary fees, trustlessness, and ease of use. The logical structure of the perpetual options product is similar to that of perpetual futures, where the option price's payoff is determined by price changes, funding fees, and trading fees:

Payoff= (No. Of Contracts*Price Change) - Funding Fee - Trading Fee

Compared to futures, options do not have the concept of liquidation. The maximum daily loss is just the funding rate. Its liquidity is supported by both private and public pools. The core innovation of Shield lies in the analytical solution of the pricing formula for perpetual options, resembling the BS model, as previously mentioned.

The main issue with options at the market fit level is that due to their complexity, they are not very suitable for retail investors; the T-shaped quote board is the biggest barrier. The largest options exchange, Deribit, has relatively low trading volume, and the options field is more suited for professional traders. Shield addresses this concern by: 1. Introducing a broker role to help users understand options and provide trading/investment advice. The entire process occurs on-chain, and brokers can earn commissions, similar to traditional finance, where commissions come from the trading fees of referred users. 2. Transforming traditional delivery options into perpetual options, allowing users to only execute at-the-money calls, significantly lowering the barriers and risks for users.

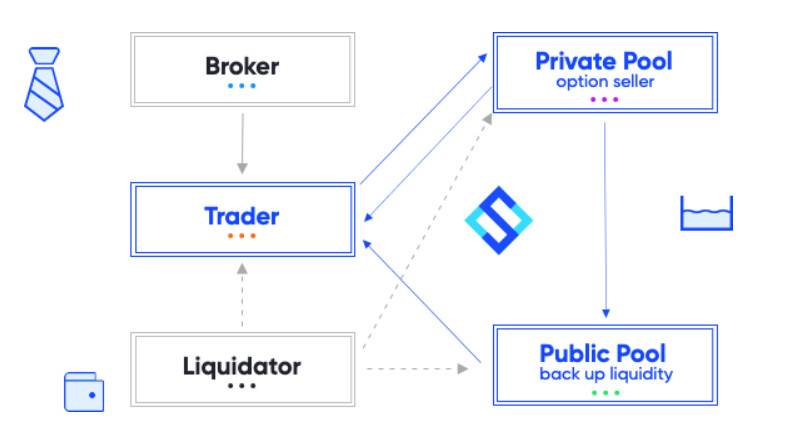

Shield features a public pool and private pool system. The private pool serves professional traders who can transfer risks through external hedging. The public pool has a lower threshold, suitable for retail investors and risk-averse participants. At T=0, the private pool acts as the seller of the options, with traders being the sellers of the options; all trades are peer-to-pool, with liquidity coming from the pool. The allocation of new orders is determined by random numbers, one being the block hash and the other the block time. Orders are randomly matched to the private pool. Providers of the private pool earn trading fees based on SLD (governance token), with higher fee income for the private pool. Liquidators earn rewards by providing liquidation services. The five roles in Shield maintain the stability of the protocol through non-cooperative games.

The explicit utility of perpetual options allows investors to avoid the hassle of rolling over; as holders of options, they face no liquidation risk. The long-term holding of options incurs time value, meaning there is daily time decay, while perpetual options do not require time value payment, only the funding fee. The implicit utility of perpetual options provides a derivative that can speculate on volatility. When combining perpetual futures and perpetual options, removing the linear terms and time value (assuming the funding fee is controllable), the resulting product is a pure volatility instrument, providing significant space for non-directional speculation. Furthermore, it enriches the product mix, reflecting true composability. Perpetual options can be combined with delivery options to form various strategies, but the current pricing mechanism for perpetual options is still relatively complex, making it difficult to calculate various greeks' risk exposures.

Perpetual Templates and Composability - Ribbon and OPYN

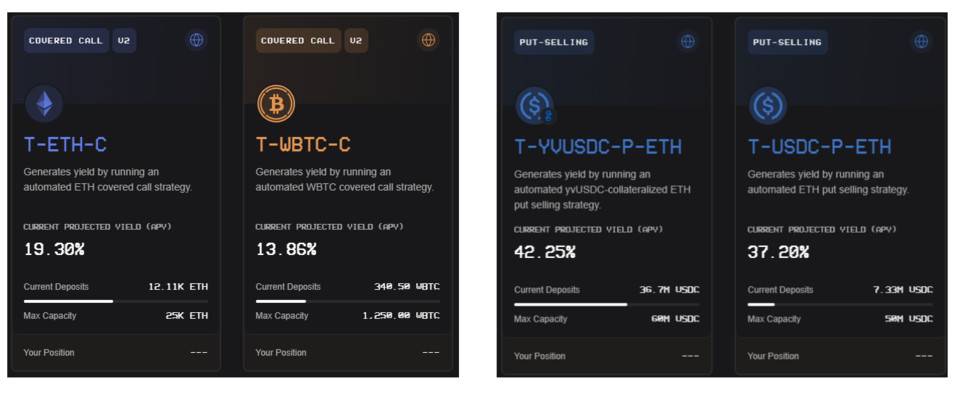

The stories of Ribbon and OPYN illustrate an interesting phenomenon: the creativity of complex products often relies on extremely simple front-ends to achieve scalability, reflecting the advantages of DeFi composability. Ribbon Finance utilizes the perpetual options templates provided by OPYN to create a fund pool similar to fixed-term savings, supported by put selling and covered call strategies, offering users a collection product akin to fixed income.

Ribbon effectively establishes a strategy aggregation yield front-end for OPYN, helping users execute a fixed weekly selling options strategy, similar to a derivative of perpetual options. The implementation principle is that the Theta Vault (the fund pool on Ribbon) uses 90% of investors' deposited funds to mint covered calls on OPYN and sells them to market makers; the option parameters are determined by the Theta Vault, so users do not need to consider them, typically opting for out-of-the-money options to earn premiums, with the downside being that if the underlying price rises to the strike price within a unit period, users will incur losses.

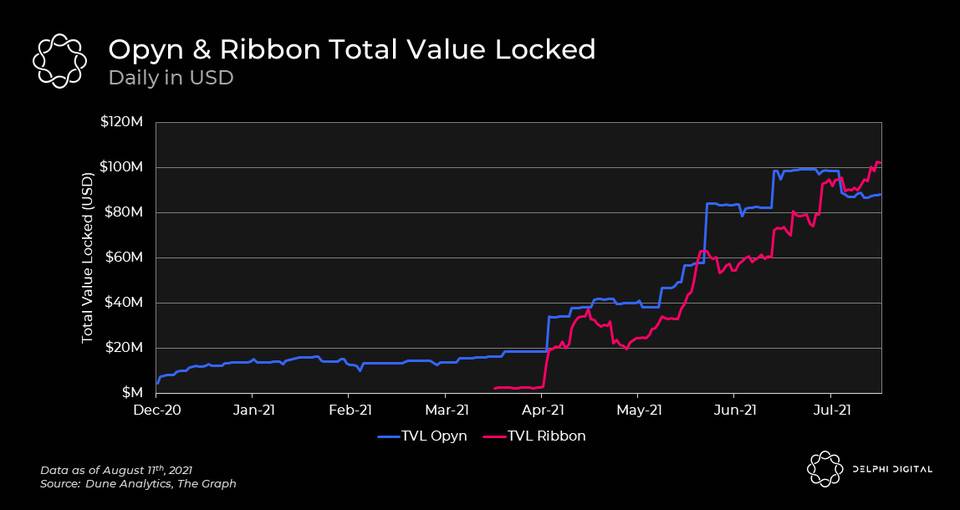

It is worth mentioning OPYN, which is increasingly moving towards the underlying, especially with practical tools like call options, liquidation bots, option liquidity pools, and perpetual options vault templates, which are used by Ribbon and have significantly increased OPYN's TVL. Essentially, the recent growth in OPYN's TVL has been driven entirely by Ribbon.

Source: Delphidigital

The underlying of OPYN: Perpetual Vault Templates. It uses a complete set of perpetual options templates, allowing anyone to construct the options they need (with any strike price and expiration date), saving the effort of bootstrapping from the ground up, and representing any strategy in the form of oTokens (tokens representing options in OPYN). It can accommodate a vast array of option strategies, with the front-facing vault allowing for the construction of products tailored to customer needs (such as fixed income).

Observing the Development of Options through Perpetual Derivatives

The development of options in ancient and modern times can be traced back to the Middle East and the tulip bubble era, appearing as a form of contractual agreement. For example, buyers pay sellers a deposit of 3.5%-10%, and if the tulip price is below the contract price at expiration, the seller can waive the obligation to buy. Modern options, both theoretically and practically, originated in the United States, with commodity options stemming from agriculture and livestock, while financial options (represented by stock options) initially followed a decentralized model, primarily being over-the-counter options. The year 1973 marked a turning point in the development of the options market, when the Chicago Board Options Exchange invited the Nansen Company to complete the "Nansen Report." In the same year, Fisher Black, Myron Sholes, and Robert Merton published two papers proposing similar conclusions regarding option pricing models, later known as the BSM option pricing model.

The 1974 SEC report extensively cited the contents of the "Nansen Report," with four key conclusions: 1. On-exchange options help reduce volatility in on-exchange spot markets, 2. On-exchange options enhance spot liquidity, 3. On-exchange options do not siphon off liquidity, 4. On-exchange options allow investors to maturely face complex markets. In 1985, the four major regulatory agencies in the U.S. released the "Study on the Economic Impact of Futures and Options Trading," commonly known as the four-party report, which put the development of options on a formal track.

The history of options development is long, resulting from the interplay of markets, theory, traders, and regulation. In the context of crypto options, we find that the theory remains largely unchanged, market demand exists, traders are not very mature, and regulation holds a very negative attitude, reflecting characteristics similar to the early stock options market before 1973. The early development of derivatives generally had a heavy speculative flavor, until investors began to mature, at which point the tool attributes gradually re-emerged. The significance of options differs markedly for institutions and individuals. Therefore, the positioning of developing the crypto options market warrants careful consideration.

Why We Are Optimistic About Perpetual Derivatives at This Time:

- Performance Improvement: The launch of Layer 2 seems to have resolved performance issues, and more importantly, it provides an opportunity for derivatives to launch new versions. The AMM model on the underlying chain is beginning to transition to order books. With the emergence of Uniswap V3, the previously forgotten order book solution has returned, and AMMs will coexist with order books.

- Diverse Playstyles: Perpetuals are a great direction; the characteristic of many retail investors in crypto makes them uncomfortable with expiration derivatives. Perpetual derivatives have been proven by the market to be combinable into interesting yield products.

- Rising Interest in Options: The interest in options is increasing, and options are well-suited for the emergence of professional market makers, who are now commonplace in Layer 2. The pricing and timing of perpetual and everlasting options have begun to form a trend, which is an important factor driving professional traders into the market.

- Potential Trading and Non-Trading Factors: As long as the overall market trading volume rises, the adoption of perpetual derivatives will be very rapid. Currently, some other factors have provided incremental growth for DeFi derivatives.

Risks of Perpetual Derivatives:

- The high leverage of derivatives can attract customers but also puts pressure on the protocol.

- For the designers of its pools, liquidity providers may face losses or be unwilling to participate actively.

- The choice of collateral is a double-edged sword.

- Whether derivatives can handle high throughput has yet to be verified.

- The closer an order book system is to centralization, the closer it is to competing with centralized exchanges. Previously, user engagement was stimulated through mining/staking mechanisms, but now it is the competition of actual products.

Risk warning

Risk warning Risk warning

Risk warning