Can Bitcoin replace the US dollar? Let's popularize some basic economic knowledge

Bitcoin and the US dollar are not even in the same league, just like you can't use a sports car for hauling goods, nor can you use a truck for racing. Today, let's set aside those hype slogans about "disrupting hegemony" and explain this matter from the fundamental logic of economics.

Bitcoin and the US dollar are not even in the same league, just like you can't use a sports car for hauling goods, nor can you use a truck for racing. Today, let's set aside those hype slogans about "disrupting hegemony" and explain this matter from the fundamental logic of economics.

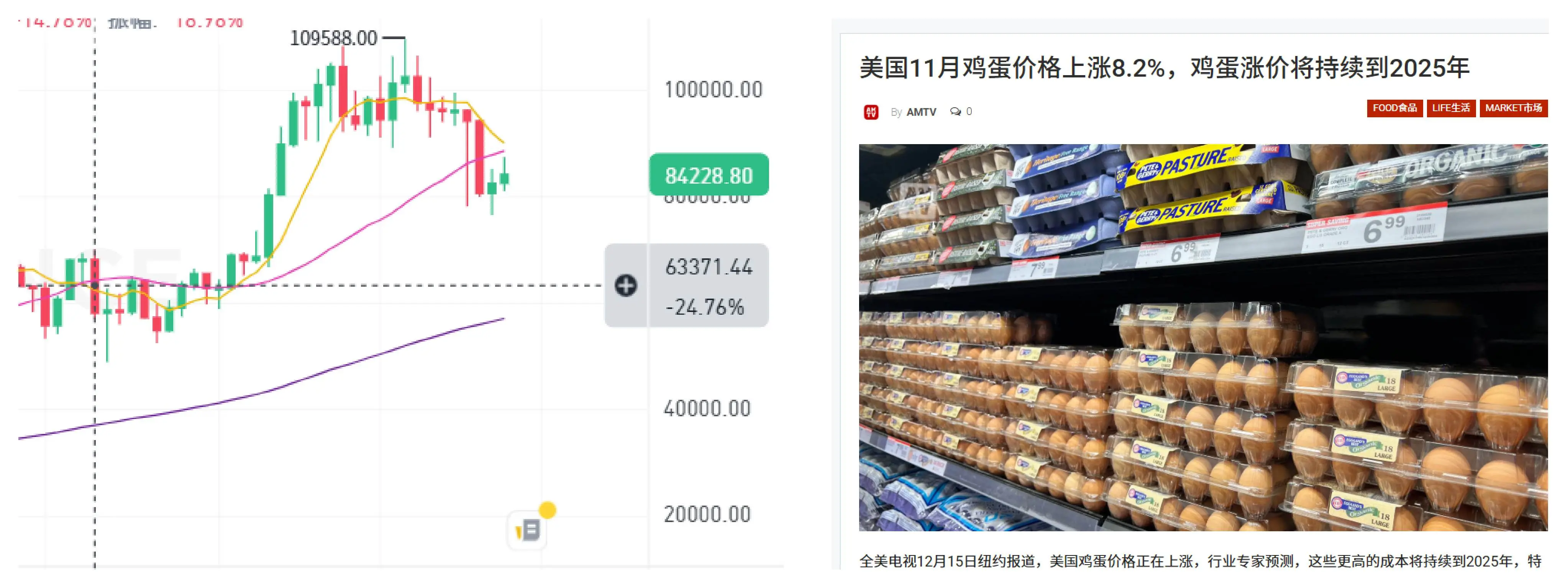

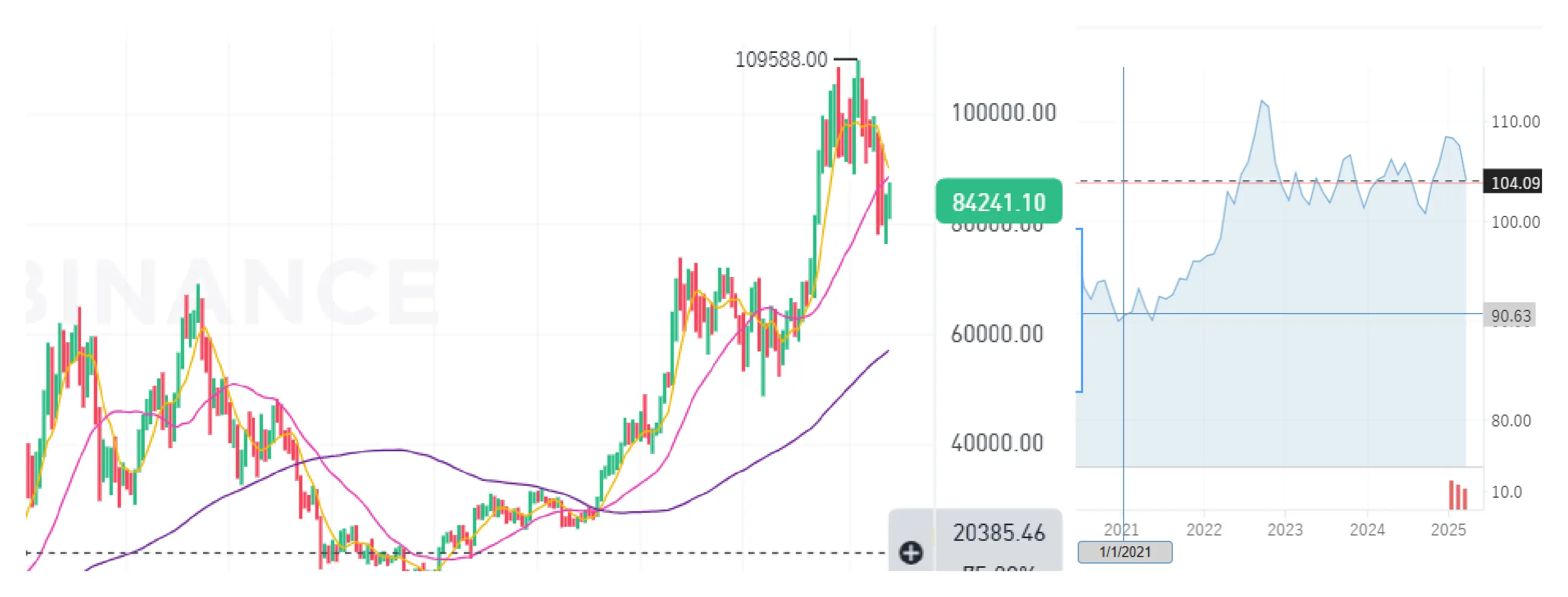

People often ask me, "Bitcoin has a total supply of 21 million coins, isn't that much more reliable than the dollar? Will it eventually replace the dollar?" Every time I hear such questions, I want to pull out my phone and show them two pictures: one is the Bitcoin price chart over the past six months, jumping from 60,000 to 110,000 and then dropping back to 80,000, and the other is a price tag showing an 8% increase in supermarket egg prices.

What does this mean? Bitcoin and the dollar are not even in the same league; it's like you can't use a sports car to haul goods, nor can you use a truck to race. Today, let's set aside those "disrupting hegemony" slogans and explain this matter from the fundamental logic of economics.

The Essence of Currency: A Continuous Division of Roles for Thousands of Years When humans first used shells as money, they probably didn't foresee the later evolution into gold, copper coins, paper money, and digital currency. However, after thousands of years of evolution, the currency system has always followed an iron law: No currency can simultaneously serve as a "safe" and a "wallet." Why did gold exit daily circulation? Because carrying gold bars to buy groceries is simply absurd. Why doesn't the dollar dare to mimic Bitcoin's fixed supply? Because the economy needs central banks to adjust the faucet to prevent droughts and floods.

Behind this is a fundamental split in the functions of money. Economists have long divided money into three roles: piggy bank (store of value), payment code (medium of exchange), and measuring unit (unit of account). Gold excels in the "piggy bank" domain, but using it as a "payment code" can be fatal—during the 2013 Cyprus financial crisis, someone actually tried to pay for surgery with gold bars, and the doctor wasted half an hour checking the purity with calipers, delaying the rescue. However, to be fair, the dollar has perfected the "payment code," but its purchasing power has shrunk by 40% over the past twenty years; storing dollars is like leaving ice cubes in the sun.

A fixed total supply and ease of storage make such items suitable as a piggy bank, referred to as a "store of value" in economics, because it can store your value without the constant concern of inflation and depreciation risks associated with fiat currency. However, due to the fixed total supply and scarcity effect, the price cannot remain unchanged; if the consensus is strong enough, it will continuously appreciate, making it unsuitable as a "payment code."

Items suitable as payment codes must have a controllable and constantly changing total supply. When the price needs to rise, the issuance must be reduced; when the price needs to fall, the issuance must be increased. This ensures stable prices for convenient daily use, and such items are called mediums of exchange. However, correspondingly, if something can be issued at will, it lacks scarcity, making it unsuitable as a medium of exchange.

Thus, Bitcoin and the dollar are two different entities in different leagues, with no competitive relationship; one does not replace the other.

The emergence of Bitcoin is essentially a blockchain technology giving rise to a "piggy bank" that is more suitable than gold. It guarantees a constant total supply through code, prevents human intervention through decentralization, and solves the carrying problem with a global ledger. However, it has a fatal flaw identical to gold—its price volatility is too high. When the Salvadoran government forcibly adopted Bitcoin as legal tender in 2021, the result was that one could buy a chicken with Bitcoin in the morning, but by the afternoon, it might no longer be affordable, creating significant barriers to transactions and pricing. Ultimately, 70% of transactions were still secretly settled in dollars. We do not deny the value of Bitcoin, but we can't help but wonder: Is there really no one in all of El Salvador who has studied basic economics?

Dollar Hegemony: An Imperfect but Irreplaceable Payment Machine

Those claiming that dollar hegemony is about to collapse may not fully understand where the true competitiveness of the dollar lies. It is indeed depreciating, and U.S. debt is piling up, but globally, there is still no second currency that can do this: buying coffee in New York in the morning, paying for gas in Dubai at noon, and settling accounts in Bangkok at night, all using the same payment system, at the same price, with same-day settlement and fees of less than 1%. This system is backed by the SWIFT international settlement system + Federal Reserve liquidity adjustments + U.S. Navy aircraft carrier battle groups, and not even Bitcoin, let alone the euro, has managed to truly shake it after twenty years of effort.

The core competitiveness of the dollar is actually the illusion of stability. Although purchasing power has long shrunk, daily volatility is low enough to be negligible—over the past three years, Bitcoin's price increase has not been as astonishing as before, but its annualized volatility still averages over 70%, while the dollar index is only about 7%. If you ask multinational companies why they settle in dollars, the finance department will simply tell you: "Because all suppliers accept dollar quotes, and the price won't suddenly plummet tomorrow." This stability cannot be solved by technology alone; it requires central banks to adjust the money supply at any time: draining liquidity to prevent inflation during economic overheating, and injecting liquidity during crises to prevent collapses. If the U.S. were to adopt Bitcoin's fixed supply model, during the Lehman Brothers bankruptcy in 2008, ATMs across the country would have likely been smashed by crowds trying to withdraw their money.

More critically, modern fiat currency is essentially a promissory note of national credit. When you hold dollars, you are essentially holding a "debt certificate guaranteed by the U.S. government through taxes, laws, and even military force." In contrast, the value of Bitcoin is entirely based on the consensus of global users, akin to comparing company equity with bank checks in terms of payment functionality; they are not even the same species.

The Real Substitute Relationship: Bitcoin Eats Gold, Stablecoins Chew on Dollars

If we talk about substitution, the battlefield is not in one place. During the global central bank monetary easing in 2020, an interesting statistic emerged: gold ETF holdings increased by 35%, while Bitcoin holdings skyrocketed by 400%. Young people began to exchange gold bracelets for BTC wallets and ancestral gold bars for Grayscale trust shares.

Bitcoin's substitution for gold is a dimensionality reduction attack. Both are anti-inflation, but BTC doesn't require armed escorts; both are globally circulated, but BTC transfers are several orders of magnitude faster than transporting gold; both have a limited total supply, but BTC doesn't have to worry about a new gold mine suddenly being discovered in South Africa. When Bitcoin's market value surpassed one trillion dollars in 2023, the total scale of global gold ETFs barely touched 230 billion; the outcome of this "digital vs. physical" war is already clear.

The true challenger to the dollar is actually its own twin brother—stablecoins. USDT now has a daily on-chain settlement volume exceeding 30 billion dollars, faster and cheaper than JPMorgan's cross-border payment system. However, upon closer inspection of Tether's reserve composition, 80% consists of short-term U.S. Treasury bonds and cash deposits. Essentially, this is using blockchain to wrap the dollar in a layer of skin, allowing the dollar to penetrate areas that were previously hard to reach: Argentinians use USDT to combat peso depreciation, Vietnamese programmers use USDT to receive salaries from Silicon Valley, and even Russian oil merchants have started using USDT to bypass SWIFT sanctions. Ironically, dollar stablecoins are both the most successful "grave diggers" of the dollar and the best promoters of dollar hegemony.

Reality Teaches a Lesson: How Those Fantasies of Replacing the Dollar Went Bankrupt

In 2018, the Venezuelan government issued the Petro, claiming to break the dollar blockade with digital currency. Six years later, this thing can't even circulate in its own local markets—after all, no one believes that a government with a 300% inflation rate can maintain currency stability. In 2022, the Central African Republic forcibly adopted Bitcoin as legal tender, but with less than 10% internet coverage and farmers lacking even mobile phones, it ultimately had to be hastily abandoned.

In contrast, the seemingly conservative Singapore has quietly built digital currency discourse power in three steps: first, attracting compliant stablecoins like USDC and PAX to settle in regulatory sandboxes; second, integrating central bank digital currency (CBDC) with the traditional banking system; third, upgrading the cross-border payment network with blockchain. After this combination, although the Singapore dollar has not replaced the dollar, Singapore has become a hub for digital dollars.

These cases reveal a harsh truth: currency substitution is never a technical duel, but a contest of comprehensive national strength. Behind the dollar are the Federal Reserve's interest rate weapons, Wall Street's capital networks, and Hollywood's cultural exports; these soft powers are something Bitcoin lacks entirely. Conversely, when USDT's penetration in Africa exceeds that of Visa credit cards, it also indicates that the old order is showing cracks—only the wall-breaker is not Bitcoin, but stablecoins wearing the dollar's disguise.

The Answer: Bitcoin Does Not Need to Replace the Dollar

What the dollar fears most is not Bitcoin, but another fiat currency that can provide "stable payments + international settlements + bulk pricing." Bitcoin's true historical mission is to become the 2.0 version of gold in the digital age—when central banks secretly increase their BTC reserves, when wealthy individuals include BTC in family trusts, and when young people use BTC instead of real estate as marriage dowries, this quiet infiltration is far more disruptive than replacing the dollar.