Stablecoins: Overview of New Regulatory Developments

Overall, whether it is setting up regulatory sandboxes for cryptocurrency companies or defining categories based on the different characteristics of stablecoins, more and more regulatory policies for stablecoins will be introduced in the future. Cross-border payments also seem to become one of the most widely used scenarios for stablecoins.

Overall, whether it is setting up regulatory sandboxes for cryptocurrency companies or defining categories based on the different characteristics of stablecoins, more and more regulatory policies for stablecoins will be introduced in the future. Cross-border payments also seem to become one of the most widely used scenarios for stablecoins.Author: WOO X Research

In recent years, the rapid development of stablecoins has attracted the attention of regulatory authorities in various countries. As a type of cryptocurrency pegged to fiat currencies or other assets, stablecoins possess the characteristic of value stability and have been widely used in areas such as cross-border payments and DeFi. Particularly in this cycle, the performance of RWA has been remarkable, with both traditional financial investment institutions (such as BlackRock) and web 3-based institutions/organizations (such as Sky, formerly Maker DAO) entering the market, leading to increasing attention from investors in this sector. A gradually forming trend of oscillating upward has emerged.

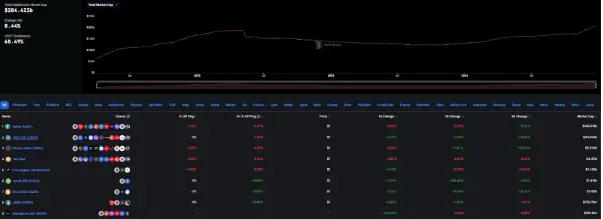

(Image source: https://defillama.com/stablecoins)

"No rules, no square," and consequently, governments and international organizations have begun to introduce policies to regulate stablecoins. This article provides a brief summary of the current regulatory dynamics.

United States (North America)

The United States is one of the main markets for stablecoin development, and its regulatory policies are quite complex. The regulatory framework for stablecoins in the U.S. is primarily implemented by multiple agencies, including the Treasury Department, the Securities and Exchange Commission (SEC), and the Commodity Futures Trading Commission (CFTC).

For certain stablecoins, the SEC may consider them to have securities attributes, requiring compliance with relevant provisions of the Securities Act. The Office of the Comptroller of the Currency (OCC), under the Treasury Department, has proposed allowing national banks and federal savings associations to provide services to stablecoin issuers, but they must comply with anti-money laundering and compliance requirements. Recently, the U.S. Congress has been discussing legislative proposals such as the "Stablecoin Transparency Act," attempting to establish a unified regulatory framework for stablecoins. After the election of Trump, known as the "crypto president," although policies have not yet been introduced, overall crypto regulation seems to be improving.

European Union (Europe)

The regulation of stablecoins in the European Union primarily relies on the Markets in Crypto-Assets Regulation (MiCA).

MiCA categorizes stablecoins into Asset-Referenced Tokens (ART) and Electronic Money Tokens (EMT). Electronic Money Tokens (EMTs) refer to tokens pegged to a single fiat currency, such as stablecoins pegged to the euro or the dollar. Asset-Referenced Tokens (ARTs) refer to tokens pegged to certain assets (such as fiat currencies, commodities, or crypto assets). MiCA establishes corresponding regulatory requirements for each category. Entities issuing stablecoins must obtain permission from EU member states and meet capital reserve, transparency disclosure, and other requirements.

Hong Kong (Asia)

On July 17, 2024, the Hong Kong Monetary Authority and the Financial Services and the Treasury Bureau jointly released a consultation summary outlining the main content of the upcoming stablecoin regulatory regime. According to this regime, companies wishing to issue or promote fiat stablecoins to the public in Hong Kong must first obtain a license from the Monetary Authority. This set of regulatory requirements includes the management of reserve assets, corporate governance, risk control, information disclosure, and measures to combat money laundering and terrorist financing.

(Image source link: https://www.hkma.gov.hk/gbchi/news-and-media/press-releases/2024/07/20240717-3/?utmsource=chatgpt.com)

In addition, the Monetary Authority has launched a "sandbox" program for stablecoin issuers to exchange views with the industry on the proposed regulatory requirements. The list of first participants was announced on July 18, 2024, including JD Coin Chain Technology (Hong Kong) Limited, Yuan Coin Innovation Technology Limited, and a consortium formed by Standard Chartered Bank (Hong Kong) Limited, Animoca Brands Limited, and Hong Kong Telecommunications Limited.

(Image source link: https://www.hkma.gov.hk/gbchi/key-functions/international-financial-centre/stablecoin-issuers/?utmsource=chatgpt.com)

Recently, on December 6, 2024, the government published the "Stablecoin Bill" in the Gazette, aiming to introduce a regulatory system for fiat stablecoin issuers in Hong Kong to improve the regulatory framework for virtual asset activities.

Singapore (Asia)

Under Singapore's Payment Services Act, stablecoins are regarded as digital payment tokens, and their issuance and circulation require the approval of the Monetary Authority of Singapore (MAS). MAS provides a regulatory sandbox for startups to test business models related to stablecoins.

Japan (Asia)

In June 2022, Japan amended the Payment Services Act (PSA) to establish a regulatory framework for the issuance and trading of stablecoins. According to the amended PSA, stablecoins fully backed by fiat currency are defined as "Electronic Payment Instruments" (EPI) and can be used to pay for goods and services. There are specific requirements for issuing entities: only three types of institutions can issue stablecoins: banks, money transfer service providers, and trust companies. Institutions wishing to engage in stablecoin-related businesses must first register as Electronic Payment Instrument Service Providers (EPISP) to obtain the necessary licenses to provide services.

Brazil (South America)

Roberto Campos Neto, President of BCB, stated in October 2024 that there are plans to regulate stablecoins and asset tokenization in 2025. In November 2024, BCB proposed a regulatory proposal suggesting a ban on users withdrawing stablecoins from centralized exchanges to self-custody wallets. However, in December, the Deputy Director of the BCB's Financial System indicated that if key issues such as transaction transparency could be improved, the central bank might lift the ban.

Conclusion

Additionally, Russia's BRICS countries are considering using cryptocurrencies as a settlement method for cross-border financing. Overall, whether it is setting up regulatory sandboxes for crypto companies or defining categories based on the different characteristics of stablecoins, more and more regulatory policies for stablecoins are expected to be introduced in the future. Cross-border payments also seem likely to become one of the most widely used scenarios for stablecoins.