Coinbase Report: 2025 Cryptocurrency Market Outlook

In-depth research covering the cryptocurrency field, from altcoins to ETFs, from staking to gaming, etc. The year 2025 will be a key year, and its breakthroughs and advancements are likely to help shape the long-term development trajectory of the cryptocurrency industry for decades to come.

In-depth research covering the cryptocurrency field, from altcoins to ETFs, from staking to gaming, etc. The year 2025 will be a key year, and its breakthroughs and advancements are likely to help shape the long-term development trajectory of the cryptocurrency industry for decades to come.Original Title: "2025 Crypto Market Outlook"

Author: Coinbase

Compiled by: Felix, PANews

Looking ahead to 2025, the crypto market is poised for transformative growth. With increasing institutional adoption and expanding use cases across various sectors, the maturity of this asset class continues to gain momentum. In just the past year, spot ETFs have been approved in the U.S., the tokenization of financial products has surged, stablecoins have seen significant growth, and further integration into the global payment framework has occurred.

Achieving this is no small feat. While it is easy to view these successes as the culmination of years of effort, an increasing number of people believe that this is merely the beginning of a grand journey.

Considering that just a year ago, this asset class was stumbling due to interest rate hikes, regulatory crackdowns, and an uncertain path forward, the progress in cryptocurrency is even more impressive. Despite all these challenges, cryptocurrencies have become a solid alternative asset, demonstrating their resilience.

However, from a market perspective, the upward trend in 2024 does exhibit some notable differences from previous bull market cycles. Some of these are superficial: "Web3" has been replaced by the more appropriate "onchain." Others have more profound implications: demand for fundamentals has begun to replace the influence of narrative-driven investment strategies, partly due to increased institutional participation.

Moreover, not only has Bitcoin's dominance surged, but DeFi innovations have also pushed the boundaries of blockchain—making the foundation of a new financial ecosystem within reach. Central banks and major financial institutions around the world are discussing how crypto technology can make asset issuance, trading, and record-keeping more efficient.

Looking ahead, the current crypto landscape presents many promising developments. At the forefront of disruption, we are focused on decentralized peer-to-peer exchanges, decentralized prediction markets, and AI agents equipped with crypto wallets. On the institutional side, there is immense potential in stablecoins and payments (which closely integrate crypto and fiat banking solutions), low-collateral on-chain lending (facilitated by on-chain credit scoring), and compliant on-chain capital formation.

Despite the high awareness of cryptocurrencies, the technology remains opaque to many due to its novel structure. However, technological innovations are expected to change this landscape, as more projects focus on improving user experience by abstracting blockchain complexity and enhancing smart contract functionality. Success in this area could broaden cryptocurrency accessibility for new users.

At the same time, the U.S. has laid a clearer regulatory foundation in 2024, well ahead of the November elections. This sets the stage for greater progress in 2025, potentially solidifying the position of digital assets in mainstream finance.

As the regulatory and technological landscape evolves, significant growth in the crypto ecosystem is anticipated, as broader adoption will drive the industry closer to realizing its full potential. 2025 will be a pivotal year, with breakthroughs and advancements likely to help shape the long-term trajectory of the crypto industry for decades to come.

Theme 1: 2025 Macro Roadmap

What the Fed Wants, What the Fed Needs

Trump's victory in the 2024 U.S. presidential election is the most significant catalyst for the crypto market in Q4 2024, driving Bitcoin up 4-5 standard deviations (compared to the three-month average). However, looking ahead, the response of short-term fiscal policy will not be as meaningful as the long-term direction of monetary policy, especially with the Fed's critical moments approaching. Yet, separating the two may not be so easy. The Fed is expected to continue easing monetary policy in 2025, but the pace may depend on the expansionary nature of the next set of fiscal policies. This is because tax cuts and tariffs could push inflation higher, and while overall CPI has dropped to 2.7% year-on-year, core CPI remains around 3.3%, above the Fed's target.

In any case, the Fed wants to suppress inflation from current levels, which means prices need to rise but slow down from now on to help achieve its other mission—full employment. On the other hand, households have been demanding lower prices after experiencing the pain of rising costs over the past two years. However, while falling prices may be politically expedient, they could potentially fall into a vicious cycle, ultimately leading to an economic recession.

Nonetheless, thanks to declining long-term interest rates and the U.S. exceptionalism 2.0, a soft landing seems to be the current baseline. At this point, the Fed's rate cuts are merely a formality, as credit conditions have already loosened, providing a supportive backdrop for cryptocurrency performance in the next 1-2 quarters. Meanwhile, with more dollars circulating in the economy, the anticipated deficit spending of the next government (if realized) should translate into greater risk-taking (crypto purchases).

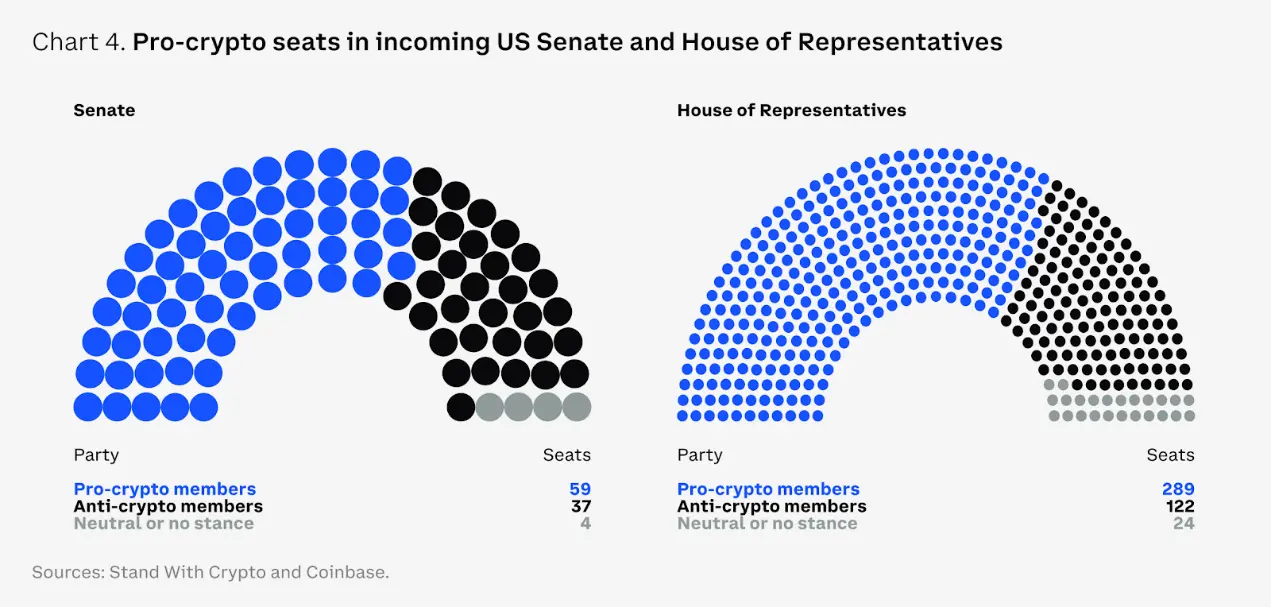

The Most Crypto-Friendly U.S. Congress Ever

After years of battling regulatory ambiguity, the next U.S. legislative session may enhance regulatory clarity for the crypto industry. This election sends a strong message to Washington that the public is dissatisfied with the current financial system and desires change. From a market perspective, bipartisan support for cryptocurrencies in both the House and Senate means that U.S. regulation may shift from "headwinds" to "tailwinds" in 2025.

A new discussion point is the possibility of establishing strategic Bitcoin reserves. Following the Bitcoin Nashville conference, Senator Cynthia Lummis (WY) not only introduced a Bitcoin bill in July 2024 but also proposed a Pennsylvania Bitcoin Strategic Reserve Act. If passed, the latter would allow the state treasurer to invest up to 10% of the general fund in Bitcoin or other crypto-based instruments. Michigan and Wisconsin have already held cryptocurrencies or crypto ETFs in their pension funds, with Florida following suit. However, creating strategic Bitcoin reserves may face challenges, such as legal restrictions on the amount of Bitcoin the Fed can hold on its balance sheet.

Meanwhile, the U.S. is not the only jurisdiction preparing to make regulatory progress. The growing global demand for crypto is also changing the competitive landscape of regulation internationally. The EU's crypto asset regulation market (or MiCA) is being implemented in phases, providing a clear framework for the industry. Many G20 countries and major financial centers such as the UK, UAE, Hong Kong, and Singapore are also actively developing rules to adapt to digital assets, creating a more favorable environment for innovation and growth.

Crypto ETF 2.0

The approval of spot Bitcoin and Ethereum exchange-traded products and funds (ETPs and ETFs) in the U.S. marks a watershed moment for the crypto economy, with net inflows of $30.7 billion since their inception (approximately 11 months). This far exceeds the $4.8 billion attracted by SPDR Gold Shares ETF (GLD) in its first year after launching in October 2004 (adjusted for inflation). According to Bloomberg, this places these tools in the top 0.1% of approximately 5,500 new ETFs launched in the past 30 years.

ETFs have reshaped the market dynamics of BTC and ETH by establishing new demand anchors, pushing Bitcoin's dominance from 52% at the beginning of the year to 62% in November 2024. According to the latest 13-F filings, almost all types of institutions are now holders of these products, including endowments, pension funds, hedge funds, investment advisors, and family offices. Meanwhile, the introduction of U.S. regulatory options on these products (in November 2024) may strengthen risk management and enhance the cost-effectiveness of these assets.

Looking ahead, the industry is focused on issuers potentially expanding the range of exchange-traded products to include other tokens such as XRP, SOL, LTC, and HBAR, although potential approvals may only have a positive impact on a limited asset group in the short term. However, what is more noteworthy is what might happen if the U.S. SEC allows staking ETFs or removes the authorization for cash rather than physical creation and redemption of ETF shares. The latter authorization introduces settlement delays between when authorized participants (APs) receive buy or sell orders and when issuers can create or redeem corresponding shares. This delay, in turn, causes a misalignment between the ETF share price on the screen and the actual net asset value (NAV).

Introducing physical creation and redemption could not only improve price consistency between share prices and asset net values but also help narrow the price spread of ETF shares. In other words, participants (APs) would not need to quote cash prices above the trading price of Bitcoin, thereby reducing costs and increasing efficiency. The current cash-based model also brings other implications related to the ongoing buying and selling of BTC and ETH, such as increased price volatility and triggering taxable events, which do not apply to physical trading.

Stablecoins, the "Killer App" of Cryptocurrency

In 2024, stablecoins experienced significant growth, with total market capitalization increasing by 48% to $193 billion (as of December 1). Some market analysts believe that based on the current trajectory, the industry could grow to nearly $3 trillion within the next five years. While this may seem high, considering this valuation is comparable to the current size of the entire cryptocurrency market, it only represents about 14% of the $21 trillion total supply of U.S. M2.

The next wave of true adoption for cryptocurrencies may come from stablecoins and payments, which can explain the surge of interest in this area over the past 18 months. Compared to traditional methods, they facilitate faster and cheaper transactions, prompting more payment companies to expand their stablecoin infrastructure, thereby increasing the utilization of digital payments and remittances. In fact, we may soon see major use cases for stablecoins that go beyond transactions to global capital flows and commerce. However, beyond broader financial applications, the ability of stablecoins to address the U.S. debt burden has also garnered political interest.

As of November 30, 2024, the stablecoin market has completed nearly $27.1 trillion in transactions, almost three times the $9.3 trillion recorded in the same 11 months of 2023. This includes a significant amount of peer-to-peer (P2P) transfers and cross-border business-to-business (B2B) payments. Businesses and individuals are increasingly utilizing stablecoins like USDC to meet regulatory requirements and integrate extensively with payment platforms such as Visa and Stripe. Stripe acquired stablecoin infrastructure company Bridge for $1.1 billion in October 2024, marking the largest deal in the crypto industry to date.

Tokenization Revolution

According to data from rwa.xyz, tokenization continued to make significant strides in 2024, with the tokenization of real-world assets (RWA) growing from $8.4 billion at the end of 2023 to $13.5 billion by December 1, 2024 (excluding stablecoins), an increase of over 60%. Multiple analysts predict that within the next five years, the industry could grow to at least $2 trillion and potentially up to $30 trillion—an increase of nearly 50 times. Asset management firms and traditional financial institutions like BlackRock and Franklin Templeton are increasingly embracing the tokenization of government securities and other traditional assets on permissioned and public blockchains, enabling near-instant cross-border settlements and 24/7 trading.

Institutions are attempting to use such tokenized assets as collateral for other financial transactions (e.g., those involving derivatives), which can simplify operations (e.g., margin calls) and reduce risks. Additionally, the RWA trend is expanding beyond assets like U.S. Treasuries and money market funds, gaining traction in private credit, commodities, corporate bonds, real estate, and insurance. Ultimately, tokenization could simplify the construction and investment processes of entire portfolios by bringing them on-chain, although this may take several years.

Of course, these efforts face a range of unique challenges, including liquidity fragmentation across multiple chains and ongoing regulatory hurdles—though significant progress has been made in both areas. Tokenization is expected to be a gradual and ongoing process; however, the recognition of its advantages is clear. This period is an optimal time for experimentation, ensuring that businesses remain at the forefront of technological advancements.

DeFi Renaissance

DeFi is dead. Long live DeFi. DeFi suffered significant blows in the last cycle as some applications used token incentives to guide liquidity, offering unsustainable yields. However, a more sustainable financial system has emerged, combining real-world use cases with transparent governance structures.

The shift in the U.S. regulatory landscape could revive the prospects for DeFi. This may include establishing a framework for managing stablecoins and pathways for traditional institutional investors to participate in DeFi, especially as the synergy between off-chain and on-chain capital markets becomes increasingly evident. In fact, DEXs currently account for about 14% of CEX trading volume, up from 8% in January 2023. In the face of a more favorable regulatory environment, even decentralized applications (dApps) sharing protocol revenues with token holders are becoming more likely.

Moreover, the role of cryptocurrencies in disrupting financial services has also been recognized by key figures. In October 2024, Fed Governor Christopher Waller discussed how DeFi could largely complement centralized finance (CeFi), arguing that distributed ledger technology (DLT) could make record-keeping in CeFi faster and more efficient, while smart contracts could enhance CeFi's capabilities. He also noted that stablecoins could be beneficial for payments and serve as "safe assets" on trading platforms, although they would need reserves to mitigate risks such as runs and illicit financing. All of this suggests that DeFi may soon expand beyond the crypto user base and begin to engage more with traditional finance (TradFi).

Theme 2: Disruption Paradigm

Telegram Trading Bots: The Hidden Profit Center of Cryptocurrency

After stablecoins and native L1 transaction fees, Telegram trading bots became the most profitable area in 2024, even surpassing major DeFi protocols like Aave and MakerDAO (now Sky) in terms of net protocol revenue. This is largely a result of increased trading and memecoin activity. In fact, meme tokens have been the best-performing crypto sector in 2024 (measured by total market cap), with trading activity in meme tokens (on Solana DEXs) soaring throughout Q4 2024.

Telegram bots are a chat-based interface for trading these tokens. Hosted wallets are created directly in the chat window and can be funded and managed through buttons and text commands. As of December 1, 2024, bot users primarily focused on Solana tokens (87%), followed by Ethereum (8%), and then Base (4%).

Like most trading interfaces, Telegram bots earn a percentage fee from each transaction, up to 1% of the transaction amount. However, due to the volatility of the underlying assets they trade, users may not be deterred by high fees. As of December 1, the highest-earning bot, Photon, has charged a cumulative $210 million year-to-date, close to the $227 million of Solana's largest memecoin launcher, Pump. Other major bots, such as Trojan and BONKbot, also generated substantial profits of $105 million and $99 million, respectively. In contrast, Aave's protocol revenue for the entire year of 2024, after fees, was $74 million.

The appeal of these applications lies in their ease of use in DEX trading, especially for tokens not yet listed on exchanges. Many bots also offer additional features, such as "sniping" tokens at launch and integrated price alerts. The trading experience on Telegram is quite appealing to users, with nearly 50% of Trojan users retained for four days or longer (only 29% of users stop using it after one day), bringing in a high average revenue of $188 per user. While the increasing competition among Telegram trading bots may eventually lower trading fees, by 2025, Telegram bots (along with other core interfaces discussed below) will remain major profit centers.

Prediction Markets: Betting

Prediction markets may be one of the biggest winners of the 2024 U.S. elections, as platforms like Polymarket outperformed polling data, predicting campaign outcomes more accurately than the final results. This is a broader victory for crypto technology, as blockchain-based prediction markets demonstrate significant advantages over traditional polling data and showcase the technology's potential differentiated use cases. Prediction markets not only illustrate the transparency, speed, and global access provided by crypto technology, but their blockchain foundation also allows for decentralized dispute resolution and outcome-based automatic payment settlements.

While many believe the relevance of these dapps may fade after the elections, their utility has expanded into other areas such as sports and entertainment. In finance, they have proven to be more accurate sentiment indicators compared to traditional surveys released alongside economic data like inflation and non-farm payrolls, which may continue to play a role and remain relevant after the elections.

Games

Games have long been a core theme in the crypto space due to the transformative potential of on-chain assets and markets. However, attracting a loyal user base for crypto games (a hallmark of most traditional successful games) has been a challenge, as many crypto game users are profit-driven and may not play for entertainment. Additionally, many crypto games are browser-based, often limiting their audience to cryptocurrency enthusiasts rather than the broader gaming population.

However, compared to the previous cycle, crypto-integrated games have made significant progress. At the heart of this trend is a shift from the early crypto punk ethos of "fully owning your game on-chain" to selectively placing assets on-chain, unlocking new features without compromising gameplay itself. In fact, many prominent game developers now view blockchain technology more as a convenient tool rather than a marketing gimmick.

The first-person shooter and battle royale game "Off the Grid" exemplifies this trend. At launch, the game's core blockchain component (Avalanche subnet) was still in the testnet phase, yet it became the top free game on Epic Games. Its core appeal lies in its unique gameplay mechanics rather than its blockchain tokens or item trading market. Crucially, this game has also paved the way for crypto-integrated games to expand their distribution channels for broader market appeal, being available on Xbox, PlayStation, and PC (via the Epic Games store).

Mobile devices are also an important distribution channel for crypto games, including native apps and embedded applications (such as Telegram mini-games). Many mobile games also selectively integrate blockchain components, with most activities actually running on centralized servers. Generally, these games can be played without setting up any external wallets, reducing the entry barrier and allowing those unfamiliar with crypto to engage with these games.

The lines between crypto and traditional gaming may continue to blur. Upcoming mainstream "crypto games" may combine with crypto technology rather than focus solely on it, emphasizing polished gameplay and distribution rather than game-earning mechanics. That said, while this may lead to broader adoption of cryptocurrencies as a technology, it remains unclear how this will directly translate into demand for liquid tokens. In-game currencies are likely to remain isolated across different games.

Decentralized Real World

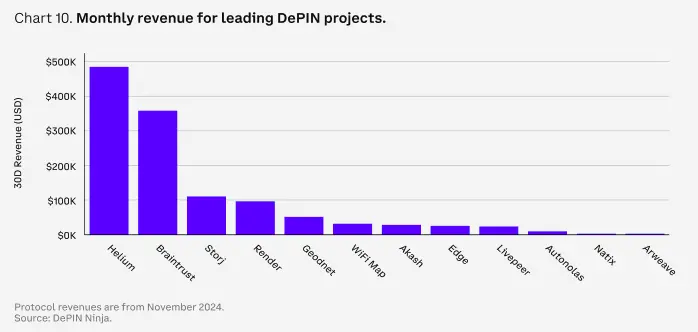

Decentralized Physical Infrastructure Networks (DePIN) have the potential to change the allocation of "real-world" resources by guiding the creation of resource networks. In other words, DePIN can theoretically overcome the initial economies of scale typically associated with such projects. DePIN projects range from computing power to cellular towers to energy, creating a more resilient and cost-effective way to integrate these resources.

A typical example is Helium, which distributes tokens to individuals providing local cellular hotspots. By issuing tokens to hotspot providers, Helium has been able to launch coverage maps in major urban areas in the U.S., Europe, and Asia without the overhead of building and distributing cellular towers or incurring significant upfront costs. Instead, early adopters are motivated by early exposure and equity in the network through tokens.

The long-term revenue and sustainability of these networks should be assessed on a case-by-case basis. DePIN is not a panacea for resource allocation, as industry pain points can vary significantly. For example, pursuing decentralized strategies may not be suitable for a particular industry, or it may only address a small portion of the issues within that industry. There may be wide variations in network adoption, token utility, and revenue generated in this space—all of which may relate to the underlying industry they target rather than the underlying technology network they use.

AI, Real Value

Artificial Intelligence (AI) has been a focal point for both traditional and crypto market investors. However, the impact of AI on cryptocurrencies is multifaceted, with narratives frequently shifting. In the early stages, blockchain technology aimed to address issues related to the authenticity of AI-generated content and user data sources (i.e., tracking data authenticity). AI-driven intent-based architectures were also seen as potential improvements to the crypto user experience. Later, the focus shifted to decentralized training and computing networks for AI models, as well as crypto-driven data generation and collection. Recently, attention has turned to autonomous AI agents capable of controlling crypto wallets and communicating via social media.

The overall impact of AI on cryptocurrencies remains unclear, as evidenced by the rapid cycling of various narratives. However, this uncertainty does not diminish the potential transformative effects AI may bring to cryptocurrencies, as AI technology continues to achieve new breakthroughs. Non-technical users are also finding it increasingly easier to use AI applications, further accelerating the development of creative use cases.

The biggest question is how to translate these shifts into enduring value accumulation for tokens versus company equity. For instance, many AI agents operate on traditional technology, with short-term "value accumulation" (i.e., market attention) flowing to memecoins rather than any underlying infrastructure. While tokens associated with infrastructure layers have also seen price increases, their usage growth often lags behind concurrent price surges. The speed of price increases relative to network metrics reflects a lack of strong consensus among investors on how to capture AI growth within cryptocurrencies.

Theme 3: Blockchain Metagame

Multi-Chain Future or Zero-Sum Game?

A major theme returning from the last bull market cycle is the popularity of L1 networks. Newer networks are increasingly competing on lowering transaction costs, redesigned execution environments, and minimizing latency. Even as high-quality block space remains scarce, the L1 space has expanded to the point of now having an oversupply of general block space.

Additional block space itself does not necessarily hold more value. However, a vibrant protocol ecosystem, coupled with an active community and dynamic crypto assets, can still allow certain blockchains to command additional fees. For example, Ethereum remains the center of high-value DeFi activity, even though its mainnet execution capacity has not improved since 2021.

Nonetheless, investors are attracted to the potential differentiated ecosystems on these new networks, even as the bar for differentiation is rising. High-performance chains like Sui, Aptos, and Sei are vying for market share against Solana.

Historically, DEX trading has been the largest driver of on-chain fees, requiring strong user logins, wallets, interfaces, and capital—creating a cycle of increasing activity and liquidity. This concentration of activity often leads to a winner-takes-all scenario across different chains. However, the future may still be multi-chain, as different blockchain architectures offer unique advantages to meet various needs. While application chains and L2 solutions can provide tailored optimizations and lower costs for specific use cases, a multi-chain ecosystem allows for specialization while still benefiting from broader network effects and innovation across the blockchain space.

Upgrading L2s

Despite the exponential growth in the scalability of L2s, debates surrounding Ethereum's rollup-centric roadmap continue. Criticisms include the "extraction" of L1 activity by L2s, as well as their fragmented liquidity and user experience. In particular, L2s are seen as the source of declining Ethereum network fees and the fading narrative of "ultrasound money." New focal points in the L2 debate are also emerging, including decentralized trade-offs, potential fragmentation of virtual machine environments (EVM), and more.

Nevertheless, from the perspective of increasing block space and lowering costs, L2s have achieved some success. The introduction of blob transactions in the March 2024 Ethereum Dencun (Deneb+Cancun) upgrade reduced average L2 costs by over 90% and increased activity on Ethereum L2s tenfold. Additionally, multiple execution environments and architectures can experiment within ETH-based environments, which is a long-term advantage of the L2-centric approach.

However, this roadmap also has some drawbacks in the short term. Cross-rollup interoperability and general user experience have become more challenging to navigate, especially for newcomers who may not fully understand the differences between ETH across different L2s or how to bridge between them. In fact, while bridging speed and costs have improved, the need for users to first interact with cross-chain bridges diminishes the overall on-chain experience.

While this is a real issue, the community is seeking many different solutions, such as superchain interoperability in the Optimism ecosystem, real-time proofs and super transactions in zkRollups, resource-lock-based solutions, sequencer networks, and more. Many of these challenges are being addressed at the infrastructure and network layers, and improvements may take time to reflect in the user interface.

Meanwhile, the growing Bitcoin L2 ecosystem is harder to navigate due to the lack of unified security standards and roadmaps. In contrast, Solana's "network expansion" is often more targeted at specific applications and may be less disruptive to current user workflows. Overall, L2s are being implemented across most major crypto ecosystems, although they vary widely in form.

Everyone Has a Chain

The convenience of deploying custom networks is increasing, prompting more applications and companies to build chains where they have more control. Mainstream DeFi protocols like Aave and Sky have clear goals of listing blockchain launches in their long-term roadmaps, and the Uniswap team has also announced plans for a DeFi-focused L2 chain. Even more traditional companies are getting involved. Sony has announced a new chain called Soneium.

As the blockchain infrastructure stack matures and becomes increasingly commoditized, owning block space is seen as more attractive—especially for regulated entities or applications with specific use cases. The technology stack enabling this is also changing. In previous cycles, application-centric chains primarily leveraged Cosmos or Polkadot Substrate SDKs. Additionally, the evolving RaaS industry, represented by companies like Caldera and Conduit, is driving more projects to launch L2s. These platforms facilitate easy integration with other services through their marketplaces. Similarly, Avalanche subnets may see increased adoption due to their managed blockchain service AvaCloud, which simplifies the launch of custom subnets.

The growth of modular chains may correspondingly impact the demand for Ethereum blob space and other data availability solutions (such as Celestia, EigenDA, or Avail). Since early November, the usage of Ethereum blobs has reached saturation (three blobs per block), growing over 50% since mid-September. Demand does not seem to be slowing, as existing L2s (like Base) continue to expand throughput, and new L2s are launching on the mainnet, although the upcoming Pectra upgrade in Q1 2025 may increase the target number of blobs from three to six.

Theme 4: User Experience

User Experience Improvements

A simple user experience is one of the most important drivers of mass adoption. While cryptocurrencies have traditionally focused on deep technology, the current emphasis is rapidly shifting towards simplifying user experience. In particular, the entire industry is pushing to abstract the technical aspects of cryptocurrencies into the background of applications. Many recent technological breakthroughs have made this shift possible, such as adopting account abstraction to simplify onboarding and using session keys to reduce signature friction.

The adoption of these technologies will make the security components of crypto wallets (such as mnemonic phrases and recovery keys) invisible to most end users—similar to the seamless security experience of today's internet (e.g., https, OAuth, and keys). Trends in key login and in-app wallet integration are expected to become more prevalent in 2025. Early signs include key login for Coinbase Smart Wallet and Google-integrated login for Tiplink and Sui Wallet.

The abstraction of cross-chain architecture may continue to pose the biggest challenge to the crypto experience in the short term. While cross-chain abstraction remains a focus of research at the network and infrastructure level (e.g., ERC-7683), it is still far from front-end applications. Improvements in this area require enhancements at the smart contract application level and wallet level. Protocol upgrades are necessary for unifying liquidity, while wallet improvements are essential for providing users with a clearer experience. The latter will ultimately be more important for expanding adoption, although current research efforts and industry debates are focused on the former.

Owning Interfaces

The most critical shift in the crypto user experience will come from efforts to "own" user relationships through better interfaces. This will happen in two ways. First, as mentioned above, improvements to independent wallet experiences. Onboarding processes are becoming increasingly streamlined to meet user needs. Direct integration of applications (such as trading and lending) within wallets may also lock users into a familiar ecosystem.

At the same time, applications are increasingly competing for user relationships by abstracting blockchain technology components into the background through wallet integration. This includes trading tools, games, on-chain social applications, and membership applications that automatically provide wallets for users registered through familiar methods like Google or Apple OAuth. After logging in, on-chain transactions are funded by the payer, with costs ultimately borne by the application owner. This creates a unique dynamic where each user's revenue needs to align with the costs of their on-chain operations. While the latter cost continues to decrease as blockchains scale, it also forces crypto applications to consider which data components to submit on-chain.

Overall, attracting and retaining users in the crypto space will be highly competitive. As indicated by the average revenue per user (ARPU) of Telegram trading bots, many retail crypto traders tend to be relatively price insensitive compared to existing TradFi entities. In the coming year, it is expected that building user relationships will also become a focus of protocols beyond the trading space.

Decentralized Identity

As regulatory transparency increases and more assets are tokenized off-chain, simplifying KYC and anti-money laundering (AML) processes is becoming increasingly important. For example, certain assets may only be available to qualified investors located in specific regions, making identity verification and authentication a core pillar of long-term on-chain experiences.

This has two key components. The first is the creation of on-chain identities themselves. Ethereum Name Service (ENS) provides a standard for resolving human-readable ".eth" names to one or more wallets across chains. This change is now present in networks like Basenames and Solana Name Service. With major traditional payment providers like PayPal and Venmo now supporting ENS address resolution, the adoption of these core on-chain identity services has accelerated.

The second core component is building attributes for on-chain identities. This includes confirming KYC verifications and other jurisdictional data that protocols can subsequently view to ensure compliance. At the heart of this technology is the Ethereum attestation service, a flexible service that allows entities to assign attributes to other wallets. These attributes are not limited to KYC; they can be freely extended to meet the needs of verifiers. For instance, Coinbase's on-chain verification utilizes this service to confirm that a wallet is associated with a user who has a Coinbase trading account and is located in certain jurisdictions. Some new licensed lending markets for real-world assets on Base will control usage through these verifications.