Compliance vs Decentralization: In-Depth Analysis of Hashkey Group's HSK Economic Model

This article will conduct an in-depth analysis of HSK's economic model based on a systematic evaluation standard for token economic models, taking into account the macro background. It will not only focus on superficial information such as distribution mechanisms and supply volume, but will further explore how to assess the deeper merits and demerits of a token economic model.

This article will conduct an in-depth analysis of HSK's economic model based on a systematic evaluation standard for token economic models, taking into account the macro background. It will not only focus on superficial information such as distribution mechanisms and supply volume, but will further explore how to assess the deeper merits and demerits of a token economic model.# Introduction

On November 26, 2024, Hashkey Group's token HSK was launched. As of the deadline for this article, the price of HSK has performed well, peaking at around $1.5, with a total market capitalization of $1.5 billion. Hashkey Group has attracted attention due to its compliant exchange, as compliance is a highly controversial path in the cryptocurrency industry. This has led to mixed opinions about the prospects of HSK.

To be clear, from the perspective of the token economic model, the HSK token has long-term sustainable development potential. In contrast to many "VC tokens" with short-term oriented economic model designs this year, many projects saw their token prices plummet after the TGE, while HSK "has long-term development potential," which is already a high evaluation. This article will analyze HSK's economic model in depth, combining macro background and systematic token economic model evaluation criteria, not just staying at surface information such as distribution mechanisms and supply, but further exploring how to judge the deep merits and flaws of a token's economic model.

# Macro Background Analysis: Compliance and Token Issuance

Before analyzing the token economic model, let's briefly understand HashKey's positioning in the current macro environment of the cryptocurrency market.

Exchanges play a sensitive and important role in the cryptocurrency industry chain due to their direct relation to asset security, and the issue of compliance has long been controversial in the market. On one hand, compliance can significantly enhance the credibility of exchanges, attracting a broader user base and gaining regulatory recognition; on the other hand, compliance may weaken user privacy protection and even be seen as contrary to the decentralized spirit of the cryptocurrency industry.

Historically, the development of any industry is difficult to escape the inevitable trajectory of "from barbaric growth to legal compliance." Regardless of how free or chaotic it is in the early stages, once the industry reaches a certain scale, legal compliance will become a necessary path for further development. Therefore, compliance is an inevitable trend for the maturity of the Web3 industry. As for decentralization, although it may conflict with compliance, in the long run, the two may also tend to balance in the game and achieve a symbiotic state, so the spirit of decentralization may not necessarily be weakened by compliance.

In this context, HashKey's positioning is particularly unique. As the first licensed exchange to issue a token, HashKey carries the decentralized gene of the cryptocurrency industry while actively exploring a path of compliance, and the "token issuance" and "licensing" are concrete manifestations of this balance.

Therefore, from the macro perspective of industry development, if you agree that with the expansion of the industry scale, compliance is an inevitable trend, then HashKey is undoubtedly worth paying attention to; if you believe that decentralization and compliance are irreconcilable, then Hashkey may not align with your philosophy. However, as the classic saying goes, "Opportunities always arise from divergences."

# Real Business Revenue: The Premise of a Sustainable Token Economic Model

Now we officially enter the analysis of the HSK token economic model. First, having real business revenue is the core premise of the sustainable development of a token economic model.

Real business revenue refers to income generated from users paying for the use value of the project, without relying on the sale of investment products such as tokens, NFTs, or game equipment. For example, Arweave generates revenue by providing decentralized permanent storage services, with user fees directly linked to their storage data needs. This source of income is entirely based on the service's intrinsic value rather than relying on token speculation. The funds paid by users are used for long-term data storage and network maintenance, forming a real business revenue model.

Some GameFi projects are negative examples; for instance, some blockchain games primarily generate income from the sale of NFT characters and game equipment. These projects often attract users to purchase NFTs or tokens through initial hype, but the actual gameplay and experience value are low, leading users to pay based more on speculative psychology than on the service's intrinsic value. Once market enthusiasm wanes, these projects struggle to sustain themselves.

So why is real business revenue the premise for the sustainable development of a token economic model? There are two main reasons:

First, the profit sources of any cryptocurrency project mainly fall into two categories: one is based on real business revenue, and the other is through market manipulation, such as attracting FOMO sentiment users to buy in and then cashing out. If a project lacks real business revenue and can only rely on the latter, this model is often unsustainable.

Second, a truly excellent token economic model must design certain mechanisms to organically combine with the project's real business revenue. This combination can use various mechanisms to return the project's earnings to token holders, thereby enhancing the long-term value of the token. This issue may sound simple, but it is actually quite complex, and related content is discussed in detail in "The Incentive Misalignment Problem in the Cryptocurrency Market and Evaluation Criteria for Sustainable Token Economic Models."

It is important to emphasize that HSK is not merely the platform token of the HashKey exchange but the core token covering the entire HashKey Group ecosystem. This positioning gives it broader and deeper application scenarios and empowerment mechanisms.

The main sources of business revenue for HashKey Group include the following aspects:

- Revenue from HashKey Exchange and HashKey Global exchanges: Compared to top-tier exchanges, their daily trading volume is generally one to two orders of magnitude lower, but this is still quite considerable compared to most on-chain projects.

- HashKey Capital: As an important investment institution in the blockchain field, HashKey Capital manages a fund size of up to $1 billion and has invested in over 600 blockchain projects.

- HashKey Cloud: Focused on providing professional, stable, and secure blockchain services to global clients, its node verification services cover over 80 mainstream public chains, managing assets totaling 1.2 million ETH.

Additionally, HashKey Group plans to launch the EVM L2 public chain—HashKey Chain. This layout is quite similar to Coinbase's "exchange + L2 public chain + other services" business structure, adding more possibilities to its ecosystem.

In summary, if we compare HashKey Group with other Web3 projects horizontally, its business revenue performance can be ranked at the "next tier" level. However, considering that most projects have little to no real revenue, this performance is already quite impressive. This also fully demonstrates that HSK has good business revenue, providing a solid foundation for the sustainable development potential of its token economic model. Next, we will specifically analyze its economic model's design and performance.

# Token Economic Model Analysis

If we divide the token economic model into two parts: basic information and in-depth research, then almost all articles about economic models currently only stay at the introduction of basic information. While this part is important, attempting to judge whether a token economic model is healthy or has long-term development potential based solely on basic information is clearly insufficient. To truly see its value, we must delve into the specific mechanisms of the token economic model.

Basic Information

|------|-------------------------------------------| | Overview | Hashkey Group's Group Token | | Total Supply | 1B | | Issued on Public Chain | Ethereum (ERC-20) | | Other Notes | Fair distribution based on incentives to ecosystem users and contributors, not to be sold through private or public sales to raise funds |

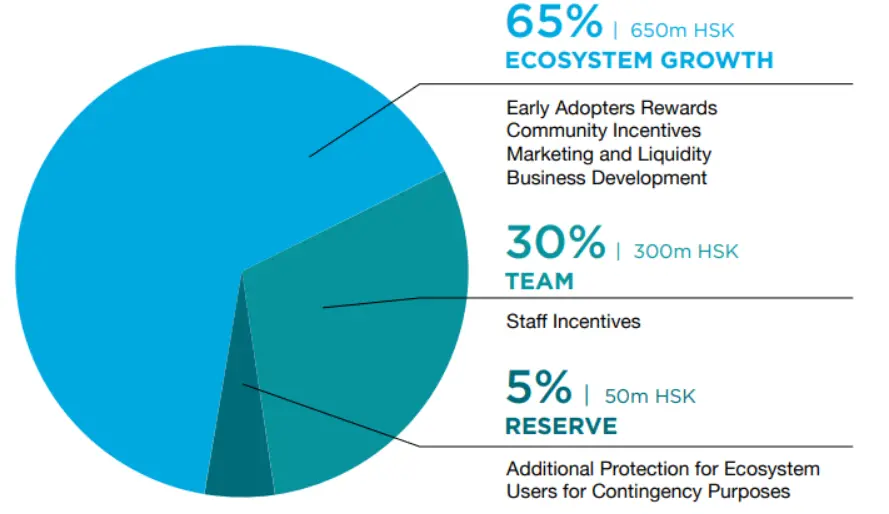

The distribution mechanism is as follows

The basic mechanism of the HSK token economy is overall quite reasonable; we won't spend too much space on this, but two points need to be noted:

- The 30% team incentive ratio is relatively high, which may raise some market concerns, especially in the absence of clear lock-up and release rules. However, considering that the team portion starts after 3 months and is unlocked over 36 months, this release mechanism somewhat mitigates the team's selling pressure and prevents the team from being inactive, aligning the team's goals with the project's objectives.

- Although there is a 5% reserve as a risk buffer, in extreme cases, this portion of funds may still be insufficient to cope with greater market pressures.

Next, we will focus on analyzing the in-depth mechanism design of the HSK token and its long-term development potential.

In-Depth Research

Not only must there be real revenue, but it must also be distributed to token holders

Let’s start with the most important point: the core mechanism of the HSK token economic model is that Hashkey Group will regularly buy back HSK tokens and burn 20% of the total profits.

Image source: HSK Token White Paper

This is a great design and is the core mechanism that gives HSK tokens long-term development potential. To simply understand it as "a mechanism that ties the issuance of tokens to the company's actual operating conditions" would be somewhat superficial. As we mentioned earlier, "a truly good sustainable token economic model must organically combine with business revenue." What does this specifically mean? Let’s analyze it further.

First, it should be noted that the buyback and burn mechanism of HSK is essentially a way to indirectly distribute business revenue to token holders. This is very intuitive: when HashKey uses profits to buy back HSK, the circulating supply in the market decreases, while the total market capitalization (circulating supply × token price) remains unchanged, and the reduction in circulating supply will naturally drive up the token price. In other words, this is equivalent to HashKey indirectly returning part of its business revenue to token holders in the form of an increase in token price.

To achieve this mechanism, two key elements must be met: first, the project itself must have real business revenue; second, there must be a mechanism designed to distribute business revenue to token holders. Only when both are present can a token economic model with long-term investment value be constructed.

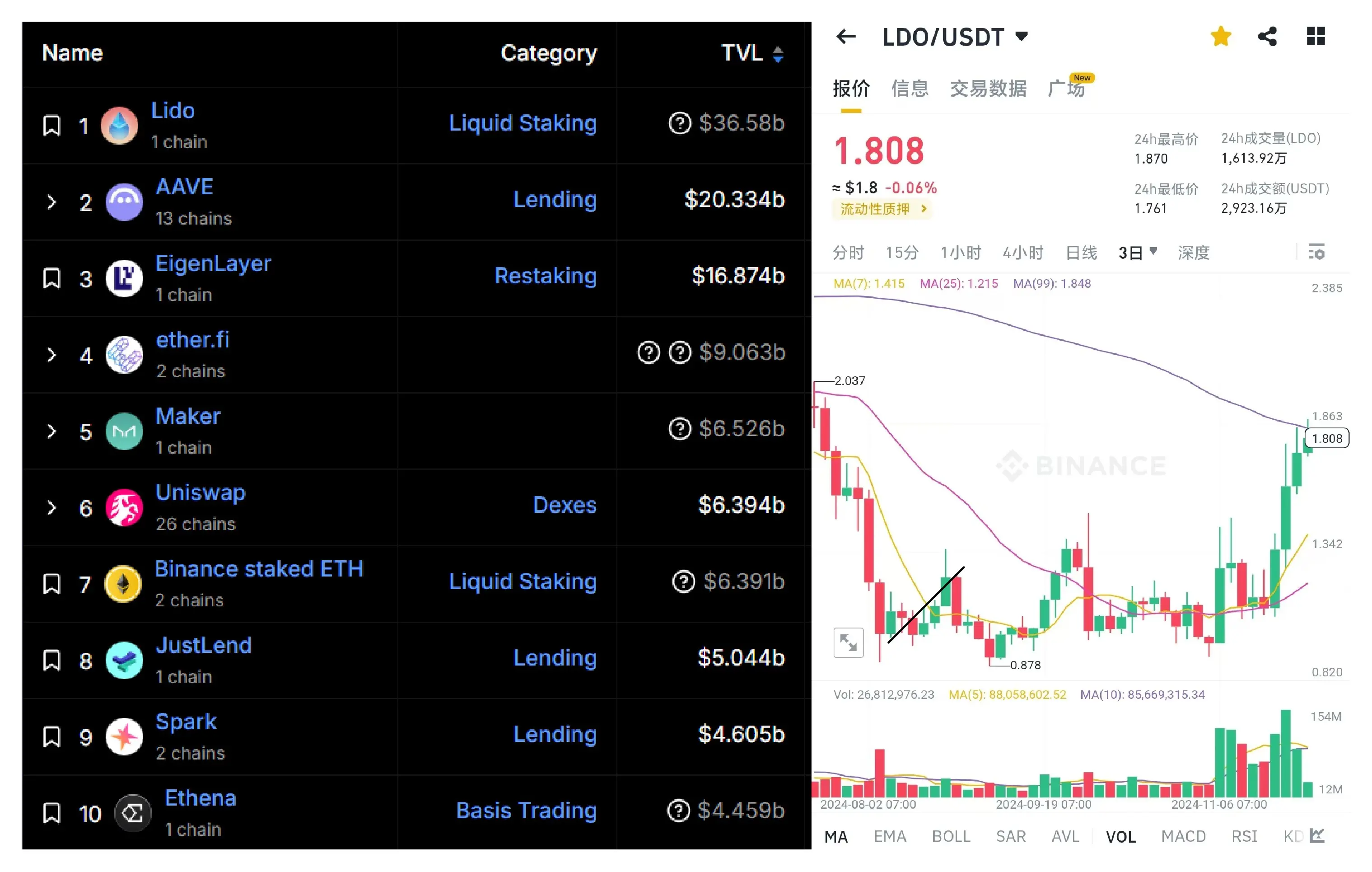

Why do we say this? Because even high-quality projects with real business revenue may not necessarily have a token economic model that is attractive for long-term investment. For example, Lido, a leading project in the DeFi space, provides services for Ethereum staking by aggregating liquidity, and its business revenue is among the best in the entire Web3 field. However, the problem is that Lido's token LDO does not have a mechanism designed to distribute business revenue to token holders. Regardless of how substantial Lido's revenue is, LDO holders cannot benefit from it. This directly leads to LDO's price fluctuating within a certain range for a long time, lacking strong performance.

A similar case is Uniswap's token UNI, which also lacks a profit-sharing mechanism in its economic model, resulting in less impressive price performance. However, Uniswap has now proposed to incorporate a profit-sharing mechanism into its token economics to improve the situation.

Lido's price is not correlated with project revenue

UNI and LDO belong to the category of "having revenue but not sharing," while another category is "sharing but having no revenue."

There are many projects in this category, where token prices often experience a brief surge before plummeting. The characteristic of these projects is that they lack business revenue and often preset a portion of tokens in the token economic model to reward holders. It should be noted that these preset rewards are merely speculative and not real profits derived from business revenue. This type of economic model is a typical short-term pump-and-dump project, often lacking long-term investment potential. Due to space limitations, we will not elaborate here; detailed analysis can be found in "The Incentive Misalignment Problem in the Cryptocurrency Market and Evaluation Criteria for Sustainable Token Economic Models."

Typical project SyncusDAO's K-line chart

Therefore, a token economic model with long-term potential must meet the requirement of distributing a portion of profits to token holders, and this distribution must be made with real business revenue. A representative of such projects is Curve, whose economic model design has long been regarded as a classic in the Web3 industry. Recently, the price of CRV has been quite strong, fundamentally because as one of the leaders in Ethereum DeFi, Curve's revenue has increased with the recent rise in on-chain trading volume, and users have long-term confidence in Curve due to its profit-sharing mechanism. From this perspective, the profit-sharing mechanism of HSK is essentially similar to that of CRV.

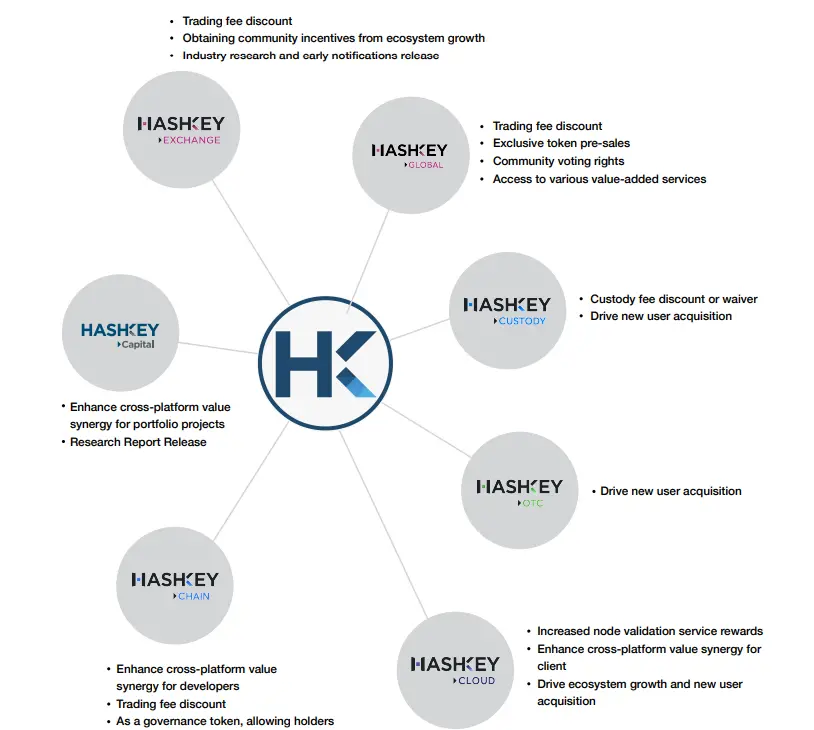

HSK's Token Empowerment

An excellent token economic model must have a clear token empowerment mechanism, which is key to closely integrating the token with ecosystem value. Token empowerment means providing actual benefits or functions to holders, such as participating in governance, enjoying discounts, or unlocking special services, thereby significantly enhancing the intrinsic value and market attractiveness of the token.

Exchange platform tokens inherently possess the potential for token empowerment, as exchanges themselves hold advantages in liquidity, trading fees, and project listing resources, which can be used to incentivize users through the use of platform tokens. For example, users holding platform tokens can receive trading fee discounts, participate in new project token sales (such as Launchpad), or earn additional rewards through staking. These empowerment mechanisms not only expand the application scenarios of the token but also enhance user stickiness, promoting a virtuous cycle within the ecosystem.

For instance, BNB's market value multiplied several hundred times after its launch, and apart from Binance's rapid development, it also benefited from successive Launchpool activities that created wealth, providing strong empowerment support for BNB. As HSK also has similar platform token attributes, it naturally possesses promising development potential.

Another important empowerment scenario is that HSK will be used as gas and transaction fees for the EVM L2 public chain Hashkey Chain released by Hashkey Global. The gas and fees of public chains are undoubtedly an excellent deflationary measure, but more deeply, they will also give the token a "soft landing" attribute through an "underdamped mechanism," preventing sharp price declines. (The "underdamped mechanism" of tokens is discussed in detail in "The Incentive Misalignment Problem in the Cryptocurrency Market and Evaluation Criteria for Sustainable Token Economic Models.")

In addition to being a platform token, HSK has diversified application scenarios across different business segments of Hashkey Group, providing ample empowerment potential.

# Conclusion

In summary, the economic model design of the HSK token is quite good in the current cryptocurrency market, not only supported by real business revenue but also returning income to token holders through mechanisms such as buybacks and burns. Additionally, it achieves multi-scenario and multi-functional coverage in its empowerment mechanisms, giving the HSK token long-term development potential.

Of course, the perfection of the economic model is only one important component of a project's success; ultimately, HSK's future depends on the prospects of the compliance track. If you agree that as Web3 gradually matures, legal compliance is an inevitable trend and believe that this trend is a key step in bridging the cryptocurrency industry with traditional finance and achieving a broader user base, then HSK is undoubtedly a quality asset worth paying attention to. Conversely, if you firmly believe that Web3 should always adhere to the core spirit of decentralization and non-regulation, and that compliance will hinder industry development, then HSK does not align with your investment logic.

The market always gives birth to opportunities amid divergences; whether HSK is worth holding long-term depends not only on the continued development of HashKey Group itself but also on users' expectations for the future path of Web3.