Is MicroStrategy's model a scam?

More than 80% of people believe this is a scam...

More than 80% of people believe this is a scam...Author: Crypto_Painter

Cold Knowledge: Michael Saylor's MicroStrategy was one of the companies that suffered the most significant market value shrinkage and losses during the 2000 internet crisis, and his personal wealth also experienced a massive drawdown during that bubble burst.

Now, MicroStrategy's main business is an online AI and data analysis platform, and its official website still reflects the traditional internet B2B enterprise level; apart from the company's substantial holdings of BTC, in my personal view, there is hardly any product or technology that can support MicroStrategy's current market value of over $20 billion…

So we can roughly understand MicroStrategy's stock as a corporate "ETF" based on BTC prices.

Even so, if we calculate the value of the BTC it holds at the current price of $63,000, these BTC are worth only $15.89 billion, while its stock market value exceeds $20 billion.

At the same time, MicroStrategy reportedly still has 2,000 employees. I am curious, if the company's value comes from BTC, where do the expenses for these employees come from? After all, MicroStrategy's self-operated business seems to be losing money.

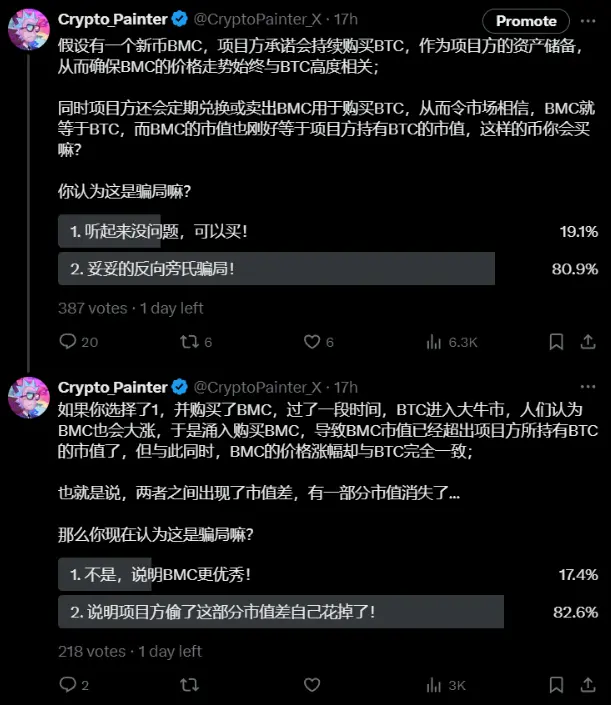

This leads us to a "new type of Ponzi scheme" that has been widely circulated online, known as the "reverse Ponzi scheme."

A traditional Ponzi scheme relies on a large number of new users entering the market to pay a small number of old users' returns, thus forming a pyramid scheme structure; the "reverse Ponzi scheme," on the other hand, acts as both new and old users, attracting external investments or loans to inflate the overall capital market value. This is a structure similar to the "standing stick method," which is a "left foot stepping on the right foot, spiraling upwards" internal circulation model.

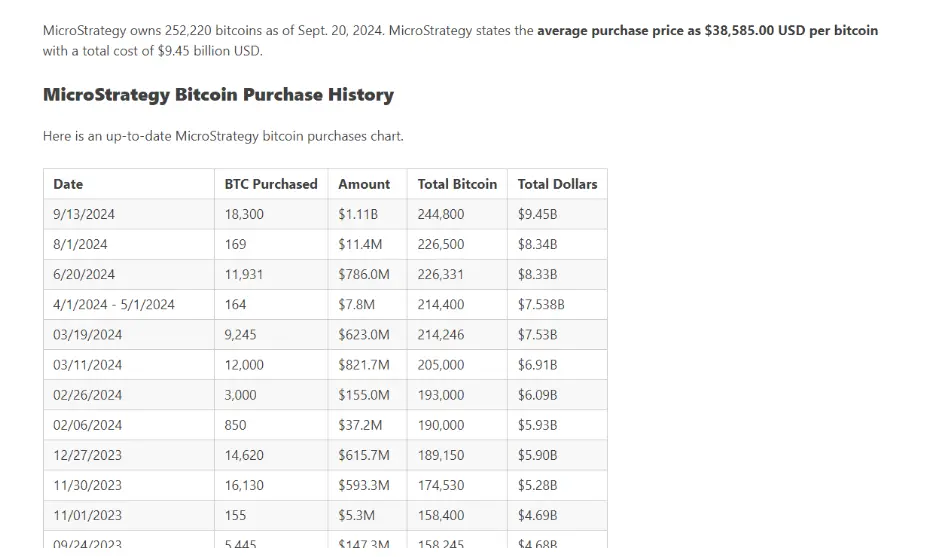

Now, let's see if MicroStrategy's behavior aligns with this. Firstly, since 2020, MicroStrategy has been continuously purchasing BTC, with the most recent purchase occurring on September 13, currently holding 252,220 BTC at an average price of about $38,585.

The funds used to purchase BTC do not come from company deposits but are raised from the market through a method similar to convertible bonds, where borrowers can obtain shares of MicroStrategy at an equivalent amount or negotiated price.

In simple terms, MicroStrategy sold its own stock to buy BTC with the money obtained, and because it purchased BTC, the company's stock price has increasingly maintained a high correlation with BTC prices since 2020, especially in the past six months, where the price trends have almost completely aligned.

From the perspective of investors or borrowers, this is equivalent to buying a substitute for BTC and enjoying the returns. Therefore, if there is a risk, it only resides in the price fluctuations of BTC, and the entire process is entirely legal. But is that really the case?

I initiated a poll yesterday in an analogous manner, and the results were as follows:

Over 80% of people believe this is a scam…

Thus, I am also pondering how this behavior of incorporating a large amount of BTC into the company's balance sheet will ultimately play out.

The first question is: the gap between inflow of funds and asset valuation.

Assuming MicroStrategy raised $2 billion from the market to purchase BTC, and after the purchase, both the company's stock price and BTC saw an increase, then in fact, the returns behind MicroStrategy have effectively doubled. This means that if one only holds BTC or only holds MicroStrategy stock, the price increase can only yield a 1:1 return, while MicroStrategy can gain two returns from the price increase of both the coin and the stock, i.e., a 1:2 return.

From the perspective of investors or borrowers, it indeed equals buying BTC spot and enjoying the returns, but for MicroStrategy, the coin is in its hands, and the stock price is still rising, so the speed of increase in paper wealth is twice that of the former. Not to mention, there are operational possibilities behind lending and mortgaging stocks.

The second question: BTC cannot be issued, but stocks can…

As long as MicroStrategy continues to purchase BTC to ensure the market believes that its stock price will always follow BTC, even when the stock price is slightly lower than BTC, there will be a large amount of arbitrage capital entering to correct this short-term negative premium. The specific operation is to short BTC while going long on the stock, and once the price difference is restored, one can close the position for profit (though I believe this operation is actually very difficult to execute).

However, this can explain why MicroStrategy's stock price is highly consistent with BTC prices.

Returning to MicroStrategy's stock, does it have a total issuance limit? Can MicroStrategy split its stock or issue more in the future?

If the answer is yes, then there is a clear arbitrage opportunity here; using an asset that superficially seems equivalent to BTC to exchange for real BTC. Even if BTC crashes in the future or the stock falls, investors will sell stocks when they exit with losses, but MicroStrategy doesn't necessarily have to sell BTC, right?

If BTC's price falls below $38,500, is it possible for the stock price to show a significant negative premium relative to BTC? That is, investors or borrowers may suffer losses far exceeding those caused by BTC's decline?

I haven't thought this through completely, but logically analyzing, MicroStrategy's model may not be a strict Ponzi scheme; rather, it is more of a means to transfer risk to borrowers or investors.

For Michael Saylor, if BTC continues to rise, he will eventually become the richest person in the world. If BTC bears and crashes below $38,500, he will still be the individual or entity holding the most BTC in the world, aside from Satoshi Nakamoto. In any case, he wins.

Unless he is willing to sell BTC to buy back stocks to stabilize the price difference when the stock price shows a negative premium, leading to further declines in both BTC and stocks, otherwise, theoretically, he can keep playing this model indefinitely.

Do you think it's possible?

Risk warning Risk warning

Risk warning Risk warning