SignalPlus Macro Analysis (20240916): 50 is the New 25

For most of last week, the market performed steadily, but by Friday, the market's expectation of a 50 basis point rate cut in September suddenly soared from around 15% to about 50%, with almost no clear news to explain this change. Economic data was generally in line with expectations and was not a factor, while the Federal Reserve remained in a blackout period, leading market participants to speculate that this repricing may have been triggered by comments from former Fed officials and journalists.

First, there was Timiraos from The Wall Street Journal, who quoted Powell's former senior advisor Jon Faust as saying, "leaning slightly towards starting with 50 basis points," and he believes "there's a good chance the FOMC will do this." Additionally, he mentioned that the Fed could use "a lot of verbal explanations to alleviate… making a large rate cut not a cause for concern," to manage investors' worries about a larger rate cut. If the Fed instead chooses to cut rates by 25 basis points first, it could raise "awkward questions."

Next, the Financial Times published an article stating that the Fed faces a very difficult choice between a 25 or 50 basis point rate cut in September. Finally, former New York Fed President Dudley made a stronger comment, stating, "I think there are strong reasons to support a 50 basis point cut, regardless of whether they do it," adding that given the current federal funds rate is nearly 200 basis points above the neutral rate, "the question is: why not start cutting rates now?"

Due to the repricing of rates, the U.S. Treasury yield curve continued its bull steepening trend, with the 2/10 spread rising by 4.5 basis points, making the curve the steepest it has been in two years, and returning to positive territory after a long inversion (since 2021).

We have discussed multiple times the "policy shift" of the Fed officially turning towards a dovish stance, which is clearly reflected in the continued steepening of the yield curve and the correlation between bonds and stocks returning to negative territory.

Over the past year, stocks and bonds have moved almost in sync, with both asset classes reflecting the market's one-way bet on Fed policy. However, since the "flash crash" in August, the market has begun to focus again on economic trajectories rather than just Fed stimulus measures, causing the movements of these two asset classes to return to a risk diversification mode.

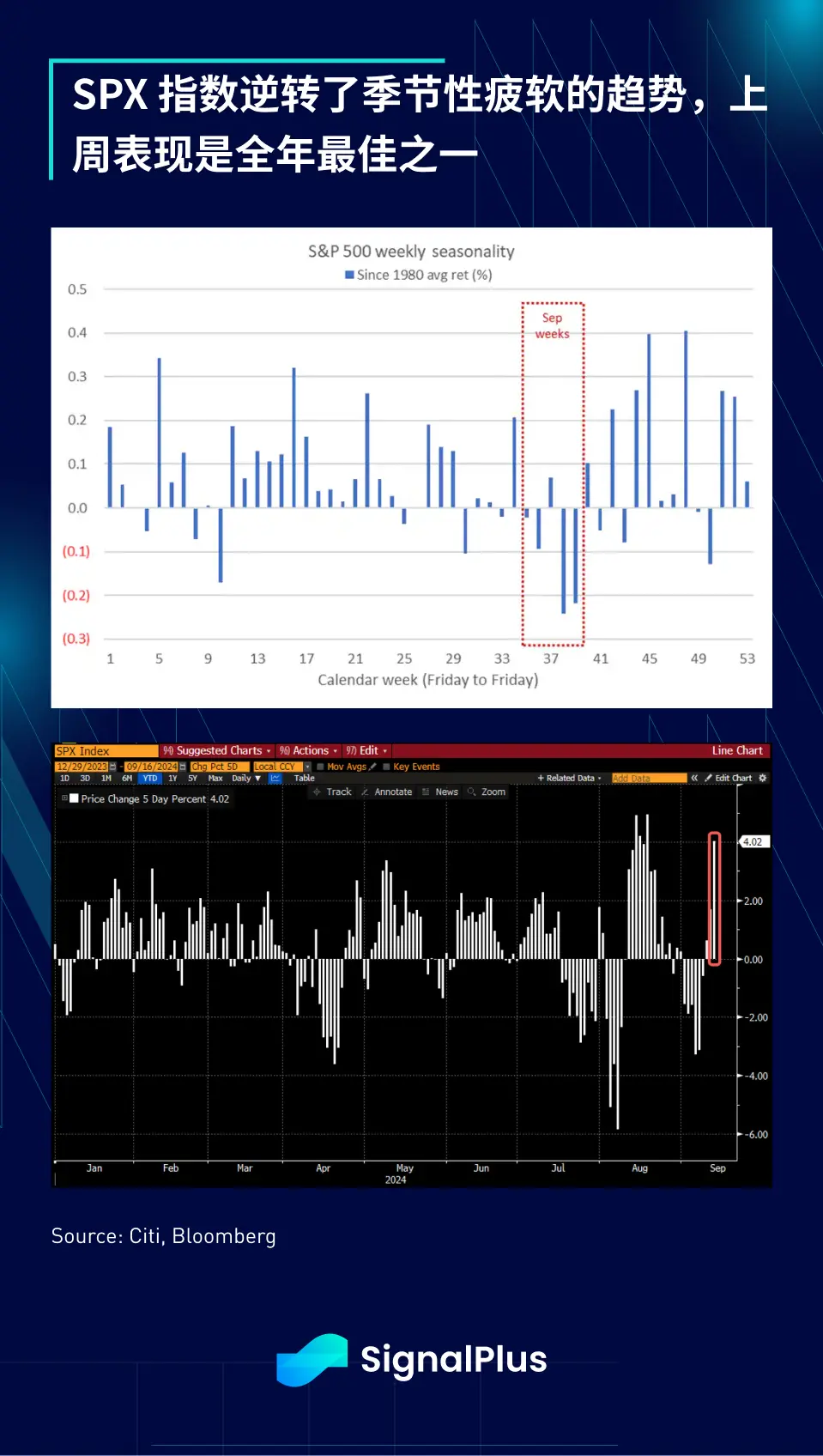

As U.S. interest rates become the market's focus again, the forex market has also reacted, with the U.S. Dollar Index (DXY) and USDJPY both fluctuating in sync with yields, hovering around key technical levels of 100 and 140, respectively. On the other hand, the U.S. stock market has at least temporarily reversed the trend of seasonal weakness, with the SPX performing as one of the best of the year last week.

Part of the strong rebound may be due to fund managers chasing yields, as a report from JPMorgan indicated that $55 billion flowed out of equity mutual funds in August, the worst since 2022. In the important end of September, will this situation see a significant reversal regardless of whether a 50 basis point cut occurs?

In the cryptocurrency space, as macro sentiment continues to dominate price movements, there has been a lack of other significant developments on-chain. The correlation between BTC and SPX has risen to near historical highs. With market sentiment temporarily improving, BTC prices have rebounded to the $58-60k range, and BTC ETFs saw inflows of $263 million last Friday, even as ETH ETF outflows temporarily halted. Meanwhile, as traders continue to prefer selling covered call options for income, implied volatility has decreased.

However, despite the temporary relief, medium-term resistance and challenges remain. ETH continues to face difficulties, with ETH/BTC having fallen to a five-year low, and there is currently no end in sight.

In news, Coinbase announced the launch of its own wrapped BTC (cbBTC), and SWIFT announced plans for tokenized asset transfer infrastructure, raising concerns about the increasing centralization of digital assets. However, as traditional finance (TradFi) continues to gain influence in the cryptocurrency space, this trend may persist.

This week will be filled with central bank activities, including meetings from the Federal Reserve, Norway, Japan, the UK, Brazil, South Africa, Thailand, Taiwan, and Indonesia. In terms of economic data, China's credit supply and retail data will be closely watched to understand the ongoing economic slowdown, while Tuesday's U.S. retail sales data should be the most important data before the FOMC meeting, potentially influencing the final decision on a 25 or 50 basis point rate cut.

Good luck to everyone, and the SignalPlus team looks forward to further discussions with you at this week's Token 2049 event!

Risk warning Risk warning

Risk warning Risk warning