BeWater Research: Returning to Growth Drivers, How Can VC Coins Break Free from the Narrative Trap?

VC coins are collapsing, but it won't just be VC coins that are collapsing.

VC coins are collapsing, but it won't just be VC coins that are collapsing.Author: Loki, BeWater Venture Studio

TL;DR

- The essence of "VC coin collapse" is the excessive investment and irrational valuation in the primary market during this cycle, allowing VCs and projects that should have been eliminated to survive, raise funds, and appear in the secondary market at unreasonable valuations.

- In the absence of external cash inflows, the degree of internal competition in the crypto market is rising sharply, forming a pyramid-like class structure where profits at each level come from the exploitation of the levels below, draining liquidity from the market. This process exacerbates distrust among the next level, leading to increasing internal competition, and besides VCs, there are many higher tiers within the pyramid.

- In the era of intense internal competition, the mortality rate of projects and tokens will significantly increase. The top-down "technological determinism," "background determinism," and "narrativism" will increasingly shift from sufficient conditions to necessary conditions. The only thing the market believes in is real growth: real user growth, real revenue growth, and real adoption growth.

I. It's not just VC coins that are in crisis, but the entire crypto market

VCs and "VC coins" have become scapegoats in the era of intense internal competition. While many believe that VC coins are the culprits of this round of "non-interconnected bull market," this is not the case. A quick comparison reveals that not only VC coins but also fully circulating altcoins, meme coins, and even ETH have significantly underperformed BTC and have been continuously declining. Moreover, most tokens during the DeFi Summer had an initial circulation rate of less than 5%, indicating that mere token circulation cannot explain the ongoing collapse of Alts.

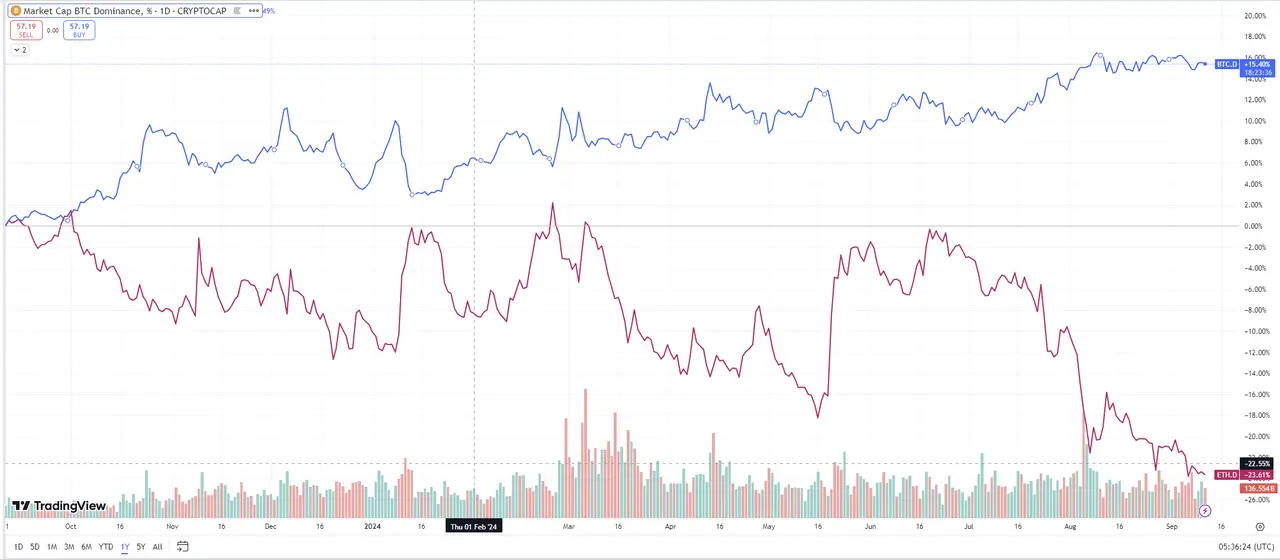

From a macro perspective, the certainty of a "four-year bull market" is no longer sustainable. Since Q2 2024, the market has entered an unusually low liquidity state. On one hand, the peak of BTC's market share lags behind the peak of BTC's price. In previous cycles, the peak of BTC's market share typically corresponded to the bottom of the market cycle, but this bull market's new highs in BTC have not led to a widespread rise in altcoins, including ETH. This also proves one point: it's not just VC coins that are in crisis, but all tokens or the entire crypto market.

Source: Tradingview

This is not hard to understand. On one hand, BTC halving reduces supply, driving the supply-demand curve upward until a new balance is reached. However, after multiple halvings, the marginal effect of BTC's inflation rate continues to weaken, and a larger base limits the multiplicative space. The price increase driven by BTC ETFs overlaps with the halving cycle in time, giving us the illusion of a bull market, and this bull market may not have existed from the start. On the other hand, since BTC's inception, the global economic cycle has generally been in an upward or stable phase, so the so-called "cycle" resembles a series of small cycles within a trend line, but this trend is also changing.

II. The "VC Coin Effect" is just the prologue to the era of intense internal competition

From an industry perspective, the consequences of over-investment and mispricing are becoming evident. In 2021, we proposed the "VC Happiness Index", calculated by dividing the current cycle's cryptocurrency market cap growth by the total financing amount of the previous cycle's blockchain industry. The logic behind this index is simple: the purpose of VC investment is to generate profits, so their investments need to be realized through the market cap growth of the next cycle. The higher this index, the greater the probability that VCs will earn high returns.

This can form a cycle theory similar to the Merrill Lynch clock. The speculative nature of cryptocurrency market cap is largely driven by external factors. If there is little investment for a period, the next cycle can easily create a wealth effect, forging a bull market, which in turn brings FOMO sentiment and financing convenience, leading to over-investment. Over-investment makes it impossible for the next cycle to realize profits, creating a bear market, which then leads to insufficient investment, repeating the cycle of bull and bear markets.

Source: CBinsights, public data

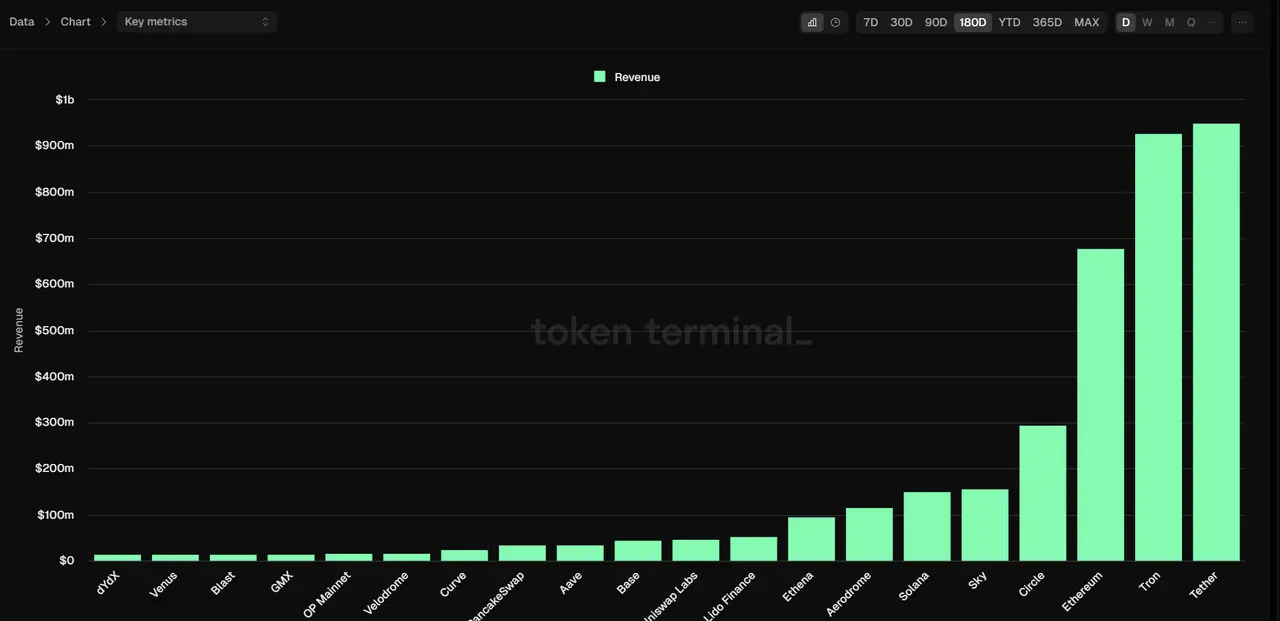

The years 2020-2021 were the happiest times for VCs in the post-ICO era. Normal VCs made money in 2021-2022, leading them to multiply their financing scales. Thus, we saw total financing exceeding $30 billion in 2021-2022, with projects valued at hundreds of millions or even billions of dollars emerging one after another. However, to this day, only thirty crypto projects have annual protocol revenues exceeding $30 million.

Source: Token Terminal

The prosperity of 2020-2021 allowed some funds that should have gone bankrupt or should go bankrupt in the future to survive and obtain funds that they should not have raised. This money then allowed some projects that should not exist to continue to exist in 2021-2022, even raising unreasonable amounts of money at unreasonable valuations, ultimately leading to these projects appearing in the secondary market at unreasonable valuations in 2023-2024.

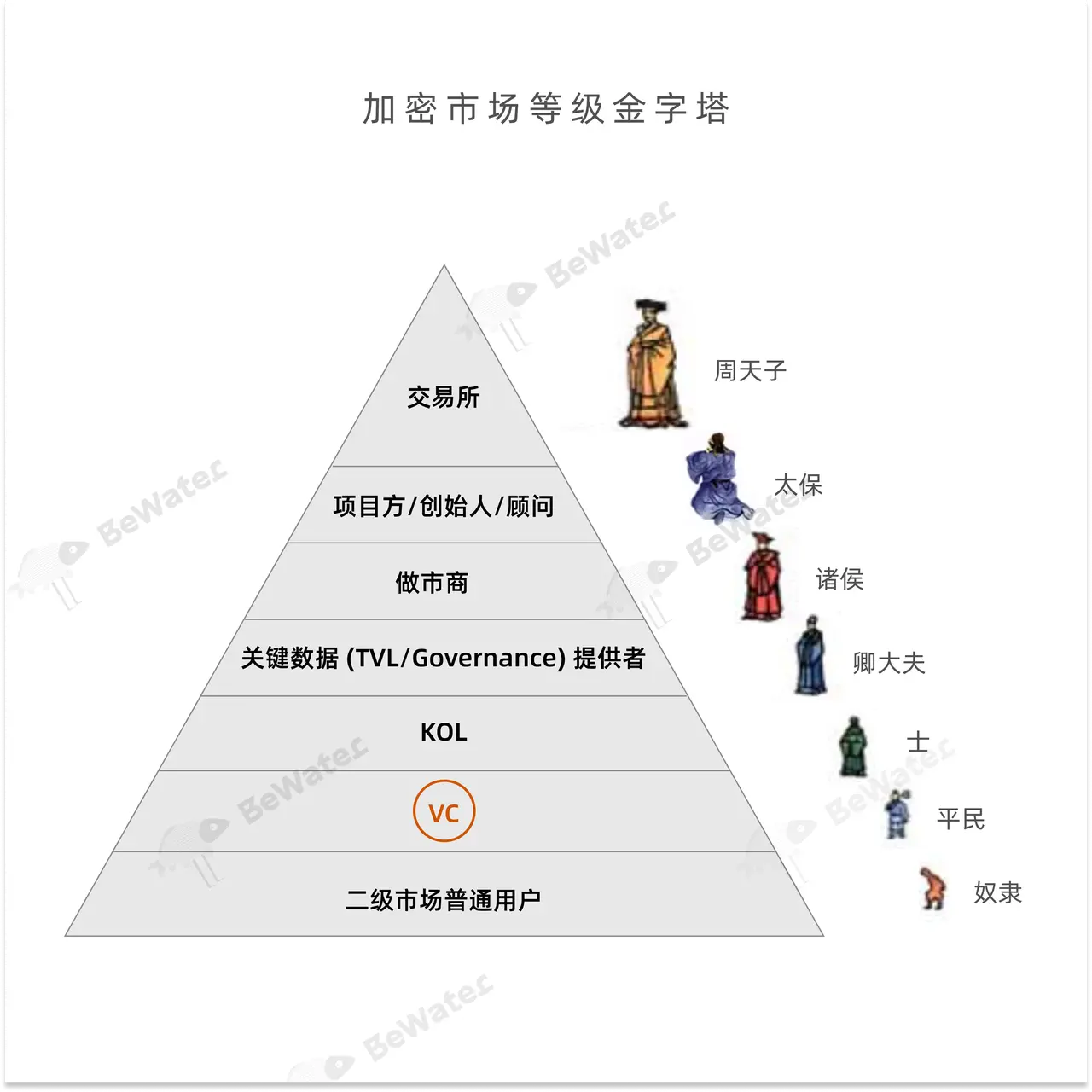

Up to this point, it seems that VCs are the culprits of the market downturn, but things are rapidly changing. This large-scale (-3, -3) is like a black hole, pulling more and more participants into it, while VCs, due to contractual and vesting restrictions, are actually the disadvantaged party in this mass exodus game. In terms of "easier access to low-cost, high liquidity," VCs can only rank at the sixth level.

In the absence of external cash flow (global protocol revenue or new funds entering the market), profits at each level come from the exploitation of the levels below, draining liquidity from the market. This process exacerbates distrust among the next level, leading to increasing internal competition.

III. Growth, Growth, Growth!

In the era of intense internal competition, the mortality rate of projects and tokens will significantly increase. The top-down "technological determinism," "background determinism," and "narrativism" will increasingly shift from sufficient conditions to necessary conditions, with the core driving factor switching to "real growth," real user growth, real revenue growth, and real adoption growth.

(1) Organic Growth: A qualified CMO's salary should not be lower than that of a CTO

Currently, there are two common misconceptions in the market:

Technology or product is more important than the market. The essence of all protocols or projects is a business, and the essence of business is profit. Therefore, everything can be simplified into two steps: (1) create a product; (2) sell the product. For most crypto projects, (1) corresponds to technology and product, while (2) corresponds to the market. Sufficient liquidity means supply cannot meet demand, and any product can find suitable buyers. However, in the era of intense internal competition, liquidity is severely lacking, and projects face only growth or death.

Data growth equals growth. Undeniably, task platforms/community tools/operational activities are playing an increasingly significant role, but neither the marketing team nor marketing agencies should overly rely on them and become mere transporters of tools.

Achieving community and social media growth through task platforms, packaging and wholesale KOL retweets of repetitive information, accumulating 1000+ GM/GN messages in Discord, incentivizing Airdrop Hunters to open 1000 accounts, attracting large holders with 8% fixed returns, ultimately resulting in a community size of 500,000, daily exposure of 1 million, 200,000 effective accounts, and $1 billion TVL appearing in financing decks and exchange listing decision meetings… This is clearly not "real growth." "Real growth" should be highly integrated with product strategy, aligned with operational routes, and maintain a high retention rate even after excluding unsustainable factors (such as lotteries, short-term incentives, points).

A truly excellent CMO should spend 70% of their time on strategic observation and thinking, 20% on planning, and 10% on execution to achieve 100%+ results.

(2) The first step in KOL collaboration is one-on-one communication with the CEO

The role of KOLs is underestimated and mismatched, primarily due to incorrect pathways. On one hand, recent KOL or KOL rounds have almost become pejorative terms due to some KOLs or matrix accounts promoting indiscriminately and without any bottom line, leading to a "fear of KOLs." However, there are still many high-quality KOLs in the market. The 80/20 rule also applies to market growth, where 80% of the influence is provided by 20% of the people. Moreover, these KOLs often possess multiple attributes, offering not only market and brand-level insights but also product and strategic advice, resource networks, and some KOLs can invest at levels comparable to small and medium-sized VCs. While these KOLs contribute their value, they also bear the blame for "harvesting retail investors" and often lose more money, moving from the first level to the 1.5 level, then to KOL rounds, and finally to the secondary market.

This is a typical case of "adverse selection." The lower the quality of the KOL, the stronger their motivation to participate in promotions or KOL rounds, while the worse the project, the better the conditions offered, even to the point of being packaged for sale. For founders, are you really willing to believe that a KOL willing to take on any promotional task can bring growth to your project?

In a sense, KOLs are also customers. On one hand, if you can't convince even 10-20 KOLs of your plan, how can the market believe it? On the other hand, if founders are not familiar with key KOLs, how can they be familiar with the entire track? Thus, the solution is simple: KOL lists, agencies, or intermediaries can only play a supporting role. Founders or team members must have at least one one-on-one communication with each important KOL.

(3) Prioritize protocol revenue as the highest growth metric

One major illusion the crypto market presents is that issuing tokens is easy, assetization is easy, and exiting is easy, leading to the neglect of a fact: the growth of asset stimulation (including token/NFT/points issuance, task platforms, incentive testnets, etc.) is always one-time, while true sustainable growth comes from sustainable revenue generated by a sustainable business model.

The first step to sustainability is having a reliable source of income. Objectively speaking, crypto has not achieved large-scale adoption, which also means limited protocol revenue. Generally, protocol revenue has two sources: the first is external sources, such as Tether earning income through RWA and stablecoin interest margins. The second is internal sources, such as public chains earning gas fees, exchanges earning transaction fees, and on-chain and secondary market transactions being objectively present. The second step to sustainability is ensuring the protocol has the potential to achieve surplus. Protocol revenue is similar to a company's main business revenue, but main business revenue does not mean profit. There is a saying that if a protocol relies on issuing tokens to sustain itself, then its token issuance is meaningless. The logic here is that issuing tokens is an act of "external blood transfusion." We can rely on transfusions to operate once or for a period, but it cannot be permanent. After many years of development, we can see that many protocols have achieved this, such as some exchange platform tokens maintaining net deflation, and some blue-chip public chains/DeFi protocols having revenues exceeding token inflation.

The third step to sustainability is to build effective governance mechanisms and economic model designs. Even if the first two steps are achieved, we may still encounter issues, such as some protocols spending tens of millions of dollars annually on operational expenses, some protocols lacking long-term incentives for teams to continue building after token release, and unfair token distribution. These issues require the joint efforts of multiple stakeholders, including core teams, investors, and communities, to resolve.

(4) 90% of projects have not established a true economic model

Most "VC" coins face the issue of mismatched token circulation growth and business performance. For example, within the 6 months to 2 years after launch, teams/foundations/investors/developer incentives/users who started holding tokens begin to unlock, most notably OP and ARB, which still have a circulation rate of around 30%. The peak of ecological development occurs before the token cycle. New competitors face even more severe problems, as a large number of ToC/ToB incentives ultimately do not result in any retention. A true economic model must meet the following conditions:

Can earn or potentially earn sustainable protocol revenue. For example, many protocols have achieved or may truly achieve sustainability, such as: (1) Curve protocol's distributable revenue has exceeded inflation output. (2) MakerDAO's annual net protocol revenue exceeds $50 million, and the formal implementation of Endgame begins this quarter. (3) Uniswap introduced front-end fees, which, despite initial skepticism, has now earned Uniswap tens of millions of dollars in revenue.

Token cycles match project growth cycles. Increasing the initial circulation rate of tokens reduces long-term inflation rates, minimizes market cap misestimation caused by "virtual circulation rates," extends/delays token unlocking cycles, and establishes transparent and deterministic profit distribution/buyback mechanisms. These are shallow yet effective solutions.

View incentives as investment behavior rather than consumption behavior. Many projects (especially large infra of public chains) have launched large-scale ToC incentives recently, leading to the emergence of an airdrop industry. However, this type of incentive is essentially a consumption behavior: users contribute transactions, and public chains pay incentives. The problem is that this is a one-time action, and most users will not retain. In contrast, incentivizing developers is an investment behavior. With ecological projects, user transaction needs can be met, leading to transactions, and once the project is supported, it can implement secondary incentives. This investment behavior is sustainable.

Address the class solidification issue of chip structure. As pointed out in the previous chapter, current market participants have formed a clear seven-layer structure, and the differences in chips at each level are becoming increasingly pronounced. This process inevitably creates space for malfeasance, such as distributing low-cost or free chips in opaque ways. When all these behaviors accumulate, it leads to an infinite reduction in the weighted average chip cost, resulting in market valuation inversion and exacerbating internal competition. The end of class solidification has only two paths: reform or revolution. Diluting chip costs without limits is unsustainable; in fact, users have already voted with their feet, choosing inscriptions and MEME.

Risk warning Risk warning

Risk warning Risk warning