SignalPlus Macro Analysis Special Edition: Cliff Dive

Last Friday's weak non-farm payroll data triggered a major earthquake in macro assets, with asset prices experiencing severe fluctuations of multiple standard deviations after the data was released. Cryptocurrency prices plummeted, with BTC dropping 20% last week, nearly erasing the gains since the ETF announcement in January.

Last Friday's weak non-farm payroll data triggered a major earthquake in macro assets, with asset prices experiencing severe fluctuations of multiple standard deviations after the data was released. Cryptocurrency prices plummeted, with BTC dropping 20% last week, nearly erasing the gains since the ETF announcement in January.

Last Friday's weak non-farm payroll data triggered a seismic event in macro assets. Following the data release, asset prices experienced severe fluctuations of multiple standard deviations, and the aftershocks continued into the new week.

The non-farm payrolls increased by 114,000, one of the weakest figures since the pandemic, and the numbers for the previous two months were also revised down. Average hourly wage growth slowed to a month-on-month increase of 0.2% and a year-on-year increase of 3.6%. The unemployment rate unexpectedly rose to 4.25%, with the unrounded figure already close to triggering the "Sahm recession indicator" threshold (4.28%). The market reacted harshly, with risk assets facing severe blows across the board.

In addition to the non-farm payroll report, last week's economic data was also relatively weak. The U.S. manufacturing index experienced its largest contraction in eight months (-1.7 points to 46.8), primarily due to a decrease in orders and production as well as a decline in employment. Comments from some industries seem to indicate that an economic slowdown is occurring (source: Bloomberg):

"The economy appears to be slowing significantly, with a notable increase in sales calls from new suppliers, and our own order backlog is also decreasing." --- Machinery

"Demand remains weak in the second half of the year, with ample supply chain pipelines and inventory reducing the need for overtime. Geopolitical issues between China and Taiwan, as well as the upcoming elections in November, remain focal points." --- Transportation Equipment

"Sales volumes are decreasing, customer orders are below expectations, and consumers seem to be starting to cut back on spending." --- Food, Beverage, and Tobacco Products

"Unfortunately, our business order levels are experiencing the sharpest decline in a year." --- Metal Products

"Business is slowing down, and we are taking cost measures." --- Electrical Equipment and Appliances

"Some typically stable markets are now showing signs of weakness." --- Non-Metallic Mineral Products

"Rising financing costs are suppressing residential investment demand, which has reduced our demand for parts and inventory." --- Wood Products

The market fell into a selling frenzy of multiple standard deviations. Technology stocks dropped 2.5% on the day, chip stocks have plummeted over 20% since July, the 2-year U.S. Treasury yield fell sharply by 26 basis points to 3.87%, the VIX soared to nearly 30, and the dollar against the yen plummeted to 145, almost completely reversing its gains for the year.

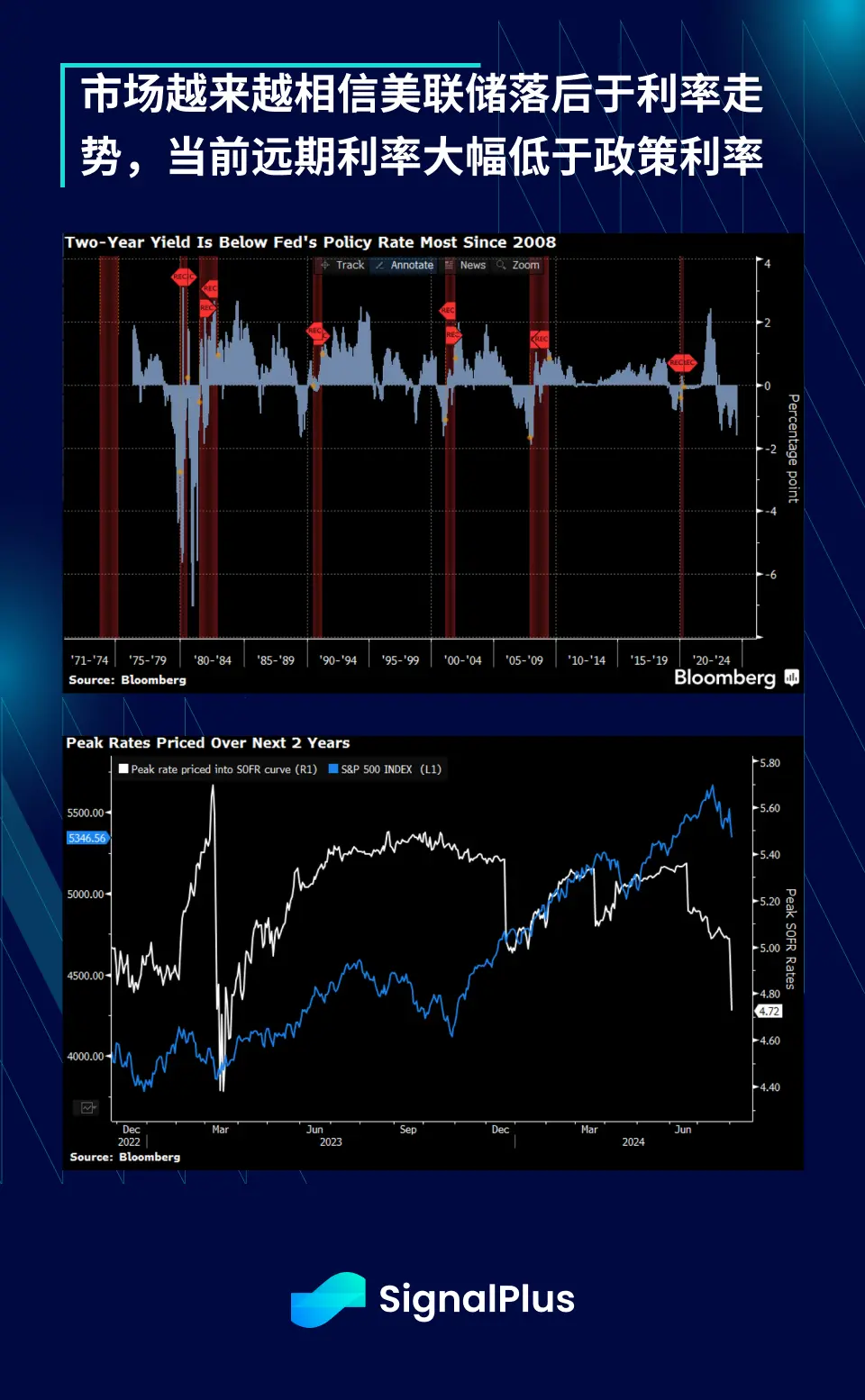

Bond traders and the federal funds futures market quickly lowered their expectations for future interest rates. JPM and Citi expect a 50 basis point rate cut in September and November, followed by a 25 basis point cut in December, totaling five complete cuts by the end of the year. The inversion of the 2-year yield relative to the policy rate has reached the most severe level since the global financial crisis, with the market believing that the Federal Reserve is significantly behind the curve, though we do not necessarily agree with this view and instead believe that the interest rate trend is somewhat overreacting.

Some readers may remember the market's obsession with using the yield curve inversion as a recession signal, but as we mentioned before, this is not a very useful signal in itself. We have experienced over 500 days of inversion without any recession occurring. However, what is more concerning is that when the market "acknowledges" that the economy is beginning to slow down and starts to significantly price in rate cuts and buy bonds in the short term, the curve immediately shows a dangerous steepening after the inversion, which is the current situation.

This partly explains why the market reaction is so severe compared to past instances of data falling short of expectations and bond rebounds.

Similar to other asset classes, cryptocurrency prices plummeted, with BTC dropping 20% last week, nearly erasing the gains since the ETF announcement in January. ETH fell to the $2000 range, and altcoins also dropped 30% to 50% over the past week.

We can certainly attribute the price drop to weak ETF inflows (especially for ETH), but cryptocurrencies ultimately demonstrate that they truly represent a "leveraged Nasdaq index," with prices merely "catching up" to the declines in tech stocks since early July. Additionally, when prices fell below the $3000 mark, large funds' profit and loss protection and risk stop-loss measures led to over $1 billion in ETH sell-offs.

Predictions for cryptocurrency trends are essentially predictions for the performance of U.S. growth stocks, which in turn extend to predictions about whether a recession is imminent, specifically whether a total of 4.5 rate cuts by the end of the year is reasonable. Although the U.S. growth trajectory is slowing, we do not yet see any actual "hard" data approaching recession, and we believe it would be unwise for the Federal Reserve to react to the drastic changes in market sentiment, as this would only backfire in terms of boosting market confidence.

After all, weren't we discussing "no landing" (i.e., growth) just a few months ago? Furthermore, with the U.S. elections approaching and the Atlanta Fed's GDPNow still predicting a GDP growth of 1.8-2% for the third quarter, can the Federal Reserve really cut rates by 100 basis points under political cover?

The main damage has already been done, and the Federal Reserve has an opportunity to calm the market at the upcoming important Jackson Hole meeting, avoiding sounding the alarm for a crisis.

Wishing everyone well during this difficult time.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles