The rise and fall of the cryptocurrency market: The decline of the Friend.Tech altar

In today's daily question of what to play, who still mentions the name Friend.Tech?

In today's daily question of what to play, who still mentions the name Friend.Tech?Author: Deep Tide TechFlow

In the ups and downs of the market, some altcoins' prices have vanished without a trace.

Equally gone without a trace may also be products and businesses.

In the daily question of "What to play today," who still mentions the name Friend.Tech?

Yet a year ago, you weren't saying this: Friend.Tech was the new trend in SocialFi, the darling of Paradigm's investments, the hot topic that various research reports rushed to write about, the god of wealth liberating the KOL fan economy…

How did it become a discarded pawn that not even dogs want to play with?

Attention is not eternal. Once-popular crypto products have quietly fallen from grace.

But the crypto market has a memory; let's take a brief look back at how Friend.Tech played a good hand so poorly.

Extreme Clamor at Its Peak, Terrifying Silence After Disillusionment

Let me tell you a ghost story.

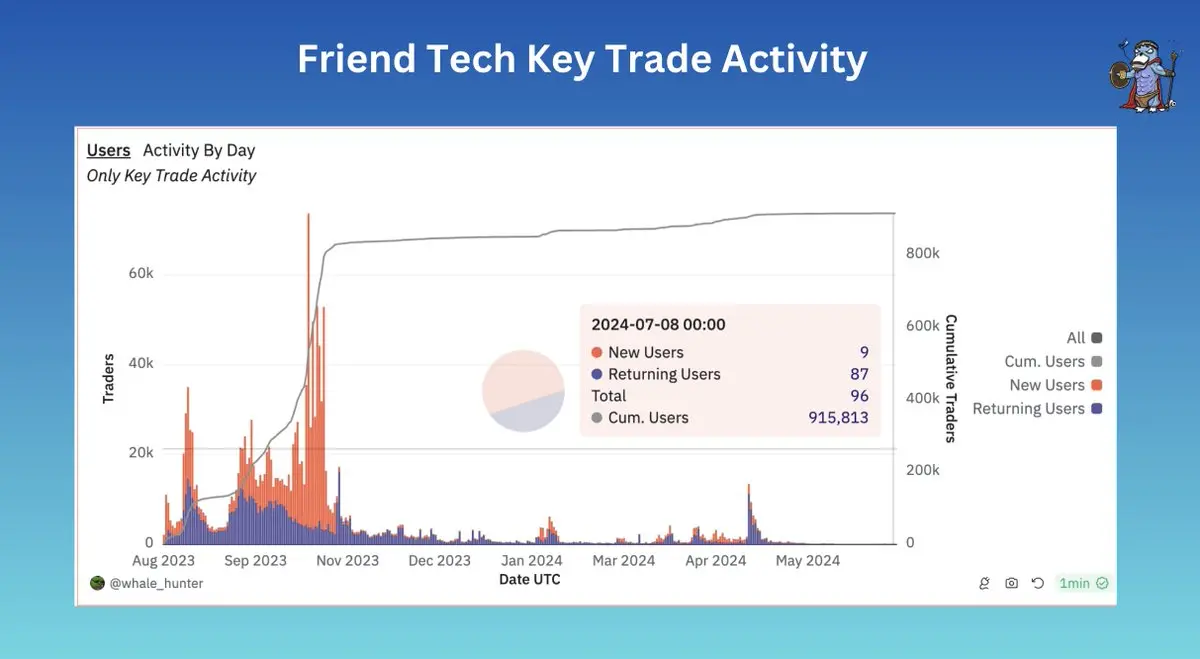

Data shows that today, Friend.Tech has fewer than 100 daily active users.

In the previous frenzy, its daily active users once exceeded 77,000, which means active users have decreased by 99.9%.

But almost a year ago, Friend.Tech rose abruptly.

In mid-August last year, Friend.Tech began to emerge, with total trading volume of shares (Key) exceeding 1 million, over 66,000 independent buyers, and 25,000 independent sellers, making it another nearly universally participated crypto product after StepN.

Within just two weeks of the launch of FT's V1 version, the platform attracted over 100,000 users and generated approximately $25 million in revenue, marking significant achievements in user adoption and financial performance.

At that time, FT's financial performance was still relatively healthy, even generating what could be called real revenue sharing, distributing about $6 million in revenue to users.

At that time, the FOMO around this product was quite simple: buying keys early could make money, quickly occupying the fan zones of celebrity KOLs became the wealth code, and FT also had a points mechanism that determined your points level based on activity, creating expectations for airdrops.

In the previously dull bear market, it indeed brought a long-awaited feast of liquidity.

The publicly available data in the crypto world is very transparent, and this hot trend naturally caught the attention of institutions in the industry. In the same month, FT also announced that it had secured seed round financing from top VC Paradigm, further pushing FOMO sentiment to a climax with the boost of airdrop expectations and capital injection.

With a new product model, solid user data, and backing from top VCs… In the last cycle, when everyone was not yet debating high FDV and low liquidity, and had not seen VCs as adversaries, possessing these elements, Friend.Tech indeed held a good hand.

But you and I both know that the key-selling model of FT has some flaws and monotony; once there are no more new entrants, its inherent flaws will quickly lead to a loss of popularity.

It was clear to everyone, and the FT team certainly understood this better, so holding a good hand, the urgent task was to improve the product, operations, and manage economic expectations to extend FT's lifespan and vitality.

Yet this good hand was played poorly.

Operations Fierce as a Tiger, Product Dull as a Fool

If we rewind time, you'll find that FT's decline has long been traceable in the details at different points in time.

In an extreme summary, it could be said — operations fierce as a tiger, product dull as a fool.

Don't misunderstand; this is not to say that FT's product has no merits. On the contrary, it has traffic and liquidity attraction capabilities that previous products lacked; it's just that compared to the overly aggressive operational maneuvers and directional choices, the product itself seems to have stagnated.

The initial traces of this overexertion were mentioned in our article “Two-Level Reversal, Friend.Tech Agreed to Let You Be Friends with Clones”** last year:**

FT initially strongly resisted users playing other similar clones and publicly stated that playing other clones would not earn FT points; this arbitrariness and narrow-mindedness faced community resistance, and the founder, fearing a loss of users, immediately issued a public apology, a rapid reversal that was quite unexpected, marking a public relations disaster.

It's very likely that the FT team themselves hadn't figured out how to operate and handle competition at that time. For a phenomenal product, entering a battle unprepared seems a bit makeshift, revealing deeper issues.

Another fierce operation was the overly aggressive PUA in the V2 version.

By the end of April this year, after a long silence, Friend.Tech announced the release of the FRIEND token and the new V2 version on the 29th, reigniting community enthusiasm.

However, the release of the token and version was delayed until May 3rd; a slight delay was still within the acceptable range for the users; what truly irked them was the rules and experience of claiming the FRIEND airdrop:

Users not only had to follow at least 10 users on FriendTech but also had to join 1 club to claim the airdrop tokens; clearly, the club's design aimed to encourage users to engage more with the V2 version, promoting activity and providing users with new things to play with.

However, the forced binding of joining first and then claiming tokens was already displeasing, and on the day of claiming tokens, many users reported difficulties in the claiming process, with tokens being delayed, and due to insufficient liquidity pool for FRIEND, it began to plummet in the secondary market, with many people not having claimed their tokens, and the airdrop value halving.

My tokens have plummeted; how can I be in the mood to listen to your PUA again?

Some netizens joked: "The only update we got after 8 months is 'club,' and everyone just uses it to claim airdrops."

The misalignment of incentives and product functions began to erode users' confidence in FT.

But just when it seemed like things couldn't get worse, the FT team then made matters worse by having co-founder Racer publicly state that "they hope to migrate the product out of the Base network," pointing out that the product was being marginalized and isolated within the Base ecosystem.

Drawing a line with the public chain they were backed by and publicly complaining is clearly a dangerous game; the market voted with its feet, and FT once again faced a double decline in users and price.

Even more surprisingly, by June, FT announced that it would soon launch its proprietary chain, Friendchain, transforming from an application layer to an infrastructure layer.

But will the market buy into this transformation?

Compared to the overly aggressive operational maneuvers and directional choices, FT's product seems not to have changed much from a year ago, with a simple, even rudimentary interface, no standalone app, and the old Ponzi game routine…

With a dull product, compounded by various internal and external troubles, it is only reasonable for a phenomenal product to fall from grace.

In contrast, other social products like Farcaster have introduced many other meme coins, FRAME, FAR, POINTS, with waves of popularity coming one after another; compared to them, FT has indeed fallen behind.

Is Ponzi a Pass for Ponzi Players?

Perhaps, FT should never have sat on a pedestal.

Relying on an improved Ponzi model can drive higher, but the flaws of the aircraft cannot be ignored.

Ponzi is indeed a pass for Ponzi players, but it does not guarantee that they can continue walking down that path. FT ignited the market last year due to various factors coming together, with inevitability within the coincidence, but this inevitability cannot be fully replicated.

Chasing profits leads to a rush, while the absence of profits leads to a swift decline; the reasoning is simple, but FT's process has been drawn out.

Ultimately, products like FT in the SocialFi space have not found true product-market fit, appearing more like short-term speculative products rather than fulfilling real demand, compounded by operational missteps, leading to an expected outcome.

But if all phenomenal crypto products are merely historical phenomena, the best crypto products still remain speculative.

Risk warning Risk warning

Risk warning Risk warning

Popular articles