An in-depth exploration of RWA assets

RWA (Real World Assets) provides advantages of eliminating intermediaries, reducing costs, and increasing transaction speed by tokenizing physical assets, and is rapidly developing in the DeFi ecosystem.

RWA (Real World Assets) provides advantages of eliminating intermediaries, reducing costs, and increasing transaction speed by tokenizing physical assets, and is rapidly developing in the DeFi ecosystem.Original Title: “Deep dive into Real World assets”

Author: Filippo Pozzi

Compilation: Baihua Blockchain

What are they?

How do they work?

What impact might they have on the financial world?

Let’s answer these and other questions through this in-depth exploration focused on RWA.

The growth of the DeFi ecosystem highlights the unique advantages offered by this decentralized infrastructure based on digital asset exchange, even prompting traditional financial entities to explore the possibility of extending these advantages to physical assets, thus giving rise to an emerging field known as RWA.

Today, we will delve into the concept of RWA (Real World Assets), focusing on the following points:

- What is RWA?

- The process of asset tokenization

- Why tokenize physical assets?

- RWA market data analysis

Let’s get started!

1. What is RWA?

Let’s immediately answer the simplest yet most important question in our study: what do we mean when we talk about Real World Assets (RWA)?

Real World Assets, or RWA, refer to tokenized assets that exist outside of the blockchain, whether they are physical, digital, or data-based assets. By tokenizing RWA, you are essentially creating a digital twin of a physical asset on the blockchain.

Thus, we can think of RWA as the digital representation of physical world assets existing on the blockchain through tokens. Simple, right?

As mentioned in the definition above, the tokenization process can be applied to various assets, such as government bonds, real estate, private credit agreements, precious materials, etc., allowing access through decentralized applications.

Having laid the groundwork for our discussion, let’s now continue to explore how these assets transform from physical goods into exchangeable tokens within the blockchain.

2. The process of asset tokenization

Asset tokenization refers to the process of recording rights to a specific asset as digital tokens that can be owned, sold, and traded on the blockchain. The created tokens represent a portion of ownership of the underlying asset.

Depending on the type of asset involved, the tokenization process may vary. Since I am not a technical expert, I will focus on purely descriptive rather than technical explanations. Generally, the process can be summarized in the following steps:

- Valuation and documentation: Determine the value of the asset through market valuation.

- Asset digitization: Create a digital representation of the asset on the blockchain, recording its ownership and relevant details.

- Token creation: Generate digital tokens representing portions of the asset, using smart contracts to manage their issuance and distribution.

- Oracle integration: Use oracles to verify and validate asset data, ensuring the integrity of information on the blockchain.

- Token issuance and trading: Issue tokens and allow them to be traded on decentralized or centralized trading platforms, facilitating market access for the asset.

These general steps outline the basic asset tokenization process, which is flexible and can adapt to the specific needs and characteristics of the assets involved. For example, in the well-known Chainlink decentralized oracle project, the concept of Proof of Reserve was introduced during the asset tokenization phase, which is a mechanism used to transparently and reliably verify whether an entity actually holds the claimed reserves of an asset. For those more interested, I have left some in-depth articles in the "Useful Links" section at the bottom of the article.

3. Why tokenize physical assets?

Tokenizing physical assets within the blockchain offers numerous significant advantages for end users. Let’s look at some of the most relevant benefits:

1) Elimination of intermediaries: One of the most notable advantages of tokenizing physical assets is the ability to conduct peer-to-peer direct transactions without intermediaries as counterparties, relying entirely on smart contracts.

2) Speed and operational continuity: With the elimination of trusted counterparties, all their "physical" requirements are also removed, making the entire process simpler, faster, and available 24/7.

3) Operational costs: Another significant benefit of avoiding interaction with physical counterparties is reflected in operational costs. Just consider the fees required at the end of a traditional home purchase transaction compared to what might be needed using decentralized smart contracts; the difference is evident.

4) Barriers to entry: In the transition to a permissionless system, we can eliminate all barriers to entry, such as nationality or the typical social backgrounds found in the "traditional" world.

5) Convenience of asset fragmentation: By converting physical assets into digital assets, we have the opportunity to split the latter into multiple identical or different parts through simple smart contracts based on user needs.

6) Security and trust: By bringing these assets onto the blockchain, we have the opportunity to interact with distributed smart contracts that are used thousands of times daily. This allows us to operate in a trustless and transparent system, eliminating the risks associated with reliance on centralized physical institutions.

4. RWA market data analysis

To complete this study, I used two sources, which we will analyze one by one: the Nifty0x Dune dashboard and the rwa.xyz website.

Let’s start with the Dune dashboard from Nifty0x:

Reference blockchains used for asset tokenization (excluding collateralized fiat currencies)

As can be expected, the reference blockchain in the field of asset tokenization is undoubtedly Ethereum, thanks to its long-demonstrated reliability and stability. Although layer two solutions are becoming increasingly popular in this field, the asset tokenization sector closely related to more "traditional" fields tends to choose blockchains that offer the highest levels of security and reliability, given the importance of the assets being managed.

Notably, after Ethereum, we find that blockchains that typically do not rank high in market capitalization within the DeFi space are rising, such as Stellar, Polygon, and Gnosis (with a particular focus on the tokenization of real estate assets).

Number of users holding tokenized assets

As the chart clearly shows, the total number of users has steadily increased, peaking at around 60 million active users. Particularly interesting is the significant growth in new users starting again between 2022 and 2023 after a period of contraction, indicating a resurgence of interest in this field, further suggesting the increasing adoption and acceptance of technologies and platforms related to asset tokenization and decentralized finance.

Now let’s turn to the analysis of the data from the rwa.xyz report. Through the rwa.xyz website, we have the opportunity to explore a wealth of data related to the world of RWA in a highly technical and pragmatic manner. Although the interface may not be very intuitive at first, using the site remains an extremely useful tool for monitoring key data in this field.

Value of RWA

As the value approaches historical highs, exceeding $160 billion, the category of tokenized fiat currencies through stablecoins like USDT and USDC stands out in the RWA field, highlighting the critical importance of fiat currency tokenization in the decentralized finance ecosystem. Due to their ease of tokenization and high utility, stablecoins play a crucial role in facilitating fast and efficient transactions on the blockchain.

Value of RWA (excluding collateralized fiat currencies)

To gain a clearer understanding, the website allows us to exclude the category of collateralized fiat currencies from the chart for a more detailed analysis of the market situation of different subcategories.

After excluding the category of collateralized stablecoins, we find ourselves facing a very interesting situation. Although the previous chart indicated that the value of RWA was approaching the historical highs of 2022, after excluding stablecoins, there are clear signs of unprecedented expansion in other subcategories.

Notably, the private credit category shows an almost exponential growth trend, with a value approaching $8 billion, positioning this category as the second most important in the RWA field.

Next, the chart clearly indicates that government bonds are also experiencing a strong growth period in the real asset market, with a value approaching $2 billion. This category reflects an increasing interest in tokenizing government debt securities, leveraging the potential of blockchain to improve the accessibility and liquidity of these assets.

Additionally, the commodities category has also become another important area for tokenizing physical assets, primarily focusing on tokenizing gold through PaxGold. This choice reflects an interest in making traditionally illiquid physical assets liquid, allowing investors to participate in the gold market in a more flexible and decentralized manner.

These data highlight the evolving landscape of the physical asset tokenization industry, with multiple asset categories benefiting from the technological innovations provided by blockchain and smart contracts.

Now let’s analyze each subcategory, excluding stablecoins, as I believe they are a separate category within RWA, and I have decided to write a dedicated in-depth article on them in the coming weeks.

5. Focus Analysis of the Private Credit Market

Now, let’s focus on the RWA market data in the private credit sector. As previously emphasized by the data, this category seems to be the most important after collateralized stablecoins.

According to data from rwa.xyz, as of the end of 2022, the undisputed market leader in the private credit sector is the Figure.com platform.

Figure.com is a U.S.-based online lending platform that leverages blockchain technology to provide various financial services, including personal loans, mortgage refinancing, home equity lines of credit, and equity release services. Through their website, loans can be obtained using physical collateral, which is assessed through an economic evaluation process developed by the platform. It is important to note that, strictly speaking, this is not a true Real World Asset (RWA) project, as there is no tokenization of physical assets. However, blockchain technology is used to make the lending process faster, cheaper, and safer.

In terms of transaction volume processed, the second place is a protocol that I find even more interesting: Centrifuge. I will not go into detail about the specifics of each project in this article to avoid excessive discussion, but I will publish more related information in the coming weeks.

For completeness, here are the main protocols displayed according to the data: Maple, Goldfinch, Clearpool, TrueFi, Credix, HomeCoin, Florence Finance, and Ribbon Lend.

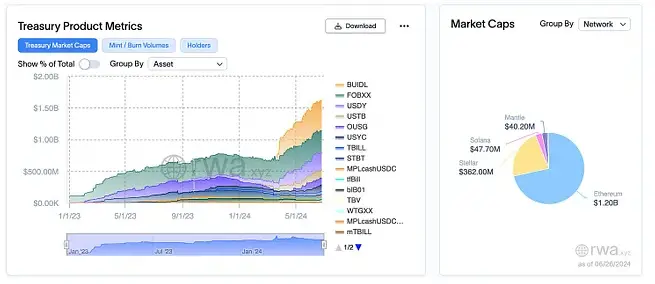

Focus on U.S. Treasury Bonds

Now let’s turn to the category of tokenized U.S. bonds.

As we can see from the chart, this category has experienced explosive growth recently, possibly due to rising interest rates making these instruments more attractive, leading to a market capitalization exceeding $1.5 billion. Clearly, these numbers are still very small compared to traditional finance, but it is noteworthy that the use of these products is increasing, with participants like Blackstone leading the rankings with their "BlackRock USD Institutional Digital Liquidity Fund" product, highlighting the growing interest in this category of RWA, which undoubtedly deserves special attention.

Focus on Commodities

The last category we studied involves commodities.

As we can observe from the data in this field, Paxos' PAXG product represents the tokenization of gold, while Tether's XAUT also represents the tokenization of gold, and they are almost the only examples of tokenization in the commodities sector, indicating that there is currently relatively low interest in other commodities in the market.

That’s all for today. If you have any questions, please feel free to ask in the comments section.