Presto Research: Understanding the Development History of the Japanese Cryptocurrency Market

As the origin of the two largest cryptocurrency exchange hacks in history, Japan's cryptocurrency history has been quite tumultuous.

As the origin of the two largest cryptocurrency exchange hacks in history, Japan's cryptocurrency history has been quite tumultuous.Original Title: “Presto Research: Understanding the Development History of Japan's Cryptocurrency Market”

Author: Rick Maeda, Presto Research

Compiled by: Tao Zhu, Jinse Finance

Abstract

- As the birthplace of the two largest cryptocurrency exchange hacks in history, Japan's cryptocurrency history has been tumultuous.

- This has forced regulators to intervene earlier than in other countries, providing a clear regulatory framework for the industry sooner.

- However, strict regulations, combined with high tax rates, have made Japan less competitive compared to neighboring countries like Singapore and Hong Kong.

- With sluggish sales and a lackluster domestic startup environment, Japan faces widespread challenges in developing its Web3 industry, and revitalization will require meaningful policy changes.

Introduction

Due to a lack of returns and a stagnant domestic stock market, Japanese retail investors have long been known for their interest in leveraged trading. The retail cryptocurrency trader community in Japan is famous for its influence on the volatile Turkish Lira / Japanese Yen forex trading pair, to the extent that the international financial community coined the term "Mrs. Watanabe" to represent them. When Bitcoin and other cryptocurrencies entered the retail space in the early 2010s, Japanese day traders eagerly embraced this esoteric asset class. However, investors soon faced domestic challenges, including the two most notorious exchange hacks in cryptocurrency history, coupled with Japan's relative lack of appeal from the perspective of entrepreneurs and investors, undermining the country's relevance in the Web3 space.

In this research article, we (1) introduce the history of cryptocurrency in Japan, particularly regarding various regulatory developments, (2) examine the current state of Japan, and finally (3) explore several key players in the domestic cryptocurrency industry.

History of Japan's Cryptocurrency Industry

Major events such as the hacks of Mt. Gox and Coincheck have marked Japan's cryptocurrency journey, leading to the implementation of strict regulatory measures aimed at protecting investors and ensuring the stability of the financial system. The country has continuously evolved its regulatory framework to address new challenges and opportunities in the cryptocurrency space.

Early Years: The Rise of Mt. Gox

2009:

Bitcoin, the first cryptocurrency, was launched by an unknown person or group under the pseudonym Satoshi Nakamoto. In the early years, awareness and adoption were low across all regions, and despite the creator's Japanese pseudonym, this was no different in Japan.

2011~2013:

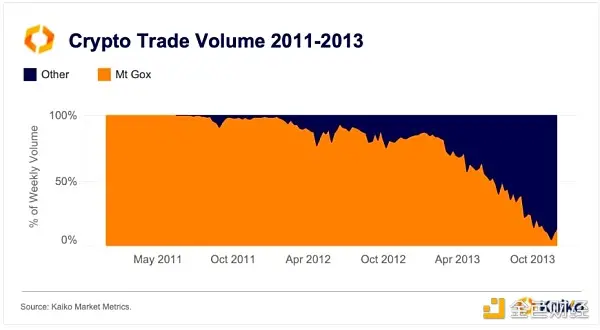

Mt. Gox, a Tokyo-based Bitcoin exchange, was the largest Bitcoin exchange in the world at the time, handling the vast majority of Bitcoin transactions at its peak. (Figure 1).

Figure 1: Global CEX trading volume as of the end of 2013.

Mt. Gox Hack and Consequences

2014:

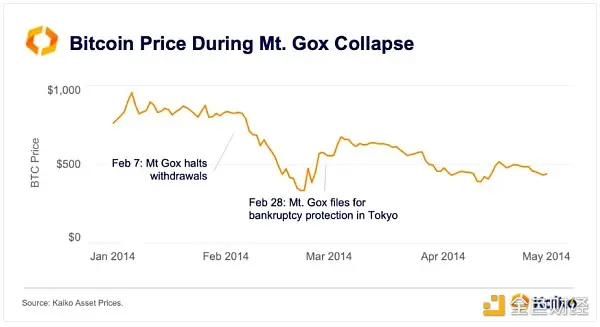

Mt. Gox suspended trading, closed its website, and filed for bankruptcy, announcing that approximately 850,000 Bitcoins were stolen due to security issues, nearly 7% of all Bitcoins worth around $450 million at the time (750,000 customer Bitcoins and 100,000 of their own Bitcoins). Investigations revealed that mismanagement and inadequate security measures led to the losses.

Figure 2: BTC dropped over 40% three days after Mt. Gox halted withdrawals.

Regulatory Developments and Early Regulation

2015:

- The Financial Action Task Force (FATF), an intergovernmental policy-making body, issued guidelines recommending that countries regulate virtual currency transactions to combat money laundering and terrorist financing.

- The Japanese government began drafting legislation aimed at regulating exchanges to protect consumers and ensure financial stability.

2016:

- The Japanese Cabinet and Diet passed amendments to the Payment Services Act (PSA) and the Financial Instruments and Exchange Act (FIEA). These amendments recognized virtual currencies ($BTC, $ETH, $XRP, $LTC, and $BCH) as a means of payment and imposed regulatory requirements on cryptocurrency exchanges, laying the groundwork for comprehensive cryptocurrency regulations.

- The Financial Services Agency (FSA) was tasked with preparing for the implementation of these regulations, focusing on exchange registration requirements, cybersecurity measures, and anti-money laundering (AML) protocols.

Coincheck Hack and Strengthened Regulation

2017:

- The amended Payment Services Act came into effect in April, requiring cryptocurrency exchanges to register with the FSA and comply with AML and know your customer (KYC) regulations. It also classified Bitcoin as a prepaid payment instrument.

- Bitcoin and cryptocurrencies became very popular in Japan, with many merchants, including Japan's largest electronics retailer Bic Camera, beginning to accept Bitcoin as a payment method.

- The National Tax Agency (NTA) classified cryptocurrency income as "miscellaneous income," making it taxable.

2018:

- One of Japan's largest cryptocurrency exchanges, Coincheck, was hacked, resulting in approximately 523 million NEM ($XEM) tokens being stolen, worth about $530 million at the time. Coincheck ultimately refunded customers in full. This hack remains one of the largest cryptocurrency heists in history and prompted the FSA to implement stricter regulatory measures. Reports indicated that the exchange stored $XEM in a hot wallet rather than a multi-signature wallet. In Figure 3, the chart below shows that $VIEW dropped over 76% in the two months following the hack. The first quarter of 2018 marked a brutal start to the bear market, but even when we eliminate the bear market impact by plotting $XEM/$BTC on the top chart, the currency pair still fell by over 61%.

Figure 3: Price trends surrounding the Coincheck hack.

- Zaif, a smaller exchange, was hacked, resulting in a loss of approximately $60 million.

- The Japan Virtual Currency Exchange Association (JVCEA) is a government-approved self-regulatory organization aimed at raising industry standards and is responsible for approving tokens for listing on exchanges.

- The FSA issued business improvement orders to several cryptocurrency exchanges and conducted on-site inspections to ensure compliance with new regulations.

- The FSA limited the leverage for cryptocurrency margin trading to four times the deposit amount, aiming to curb speculative trading and protect investors.

Margin Trading Regulations and Ongoing Developments

2019:

- Coincheck has now complied with the new regulations and resumed operations.

- The Japanese Cabinet approved new regulations limiting the leverage for cryptocurrency margin trading to 2-4 times the initial deposit.

- The amended Financial Instruments and Exchange Act (FIEA) and Payment Services Act (PSA) came into effect, further tightening regulations on cryptocurrency exchanges and security token offerings (STOs).

2020:

- The FSA reduced the maximum leverage for margin trading to 2 times.

- Further amendments to the PSA and FIEA were implemented, focusing on enhancing user protection and market integrity.

2021:

- Japan continued to develop its regulatory framework, focusing on strengthening investor protection, cybersecurity, and anti-money laundering measures.

- The FSA established a new regulatory body to oversee cryptocurrency trading operators and ensure compliance with evolving regulations.

- The FSA required the JVCEA to implement self-regulatory rules regarding information sharing during trading periods under the "cryptocurrency travel rule."

Recent Developments

2022:

- The FSA introduced additional guidelines for exchanges holding digital assets, emphasizing the necessity of strong internal controls and risk management practices.

- The JVCEA introduced the travel rule in its self-regulatory rules, while the Cabinet Secretariat amended the Act on Prevention of Transfer of Criminal Proceeds (APTCP) to enforce the rule.

- The Japanese Tax Commission amended tax laws to exempt token issuers from corporate tax on unrealized cryptocurrency gains.

- Japan explored the possibility of issuing a central bank digital currency (CBDC), with the Bank of Japan conducting experiments and research.

- The House of Councillors passed a bill regulating stablecoins, monitoring money laundering, and combating money laundering activities.

- The Liberal Democratic Party's Digital Society Promotion Headquarters released the "NFT White Paper: NFT Strategy for Japan's Web 3.0 Era," reflecting policy recommendations for the development and protection of NFTs.

- The Ministry of Economy, Trade and Industry (METI) established a Web3 Policy Office to create a supportive business environment for Web3-related industries.

- The FSA continued to lift the ban on foreign-issued stablecoins.

2023:

- The FSA continued to refine its regulatory approach, focusing on emerging trends such as DeFi and non-fungible tokens (NFTs).

- The FSA initiated a public consultation on a draft order to amend the APTCP enforcement order, clarifying the applicability of the travel rule to Japanese virtual asset service providers (VASPs).

- Japanese Prime Minister Fumio Kishida emphasized that Web3 is a pillar of economic reform, describing it as "a new form of capitalism" and highlighting its potential to drive growth by addressing social issues.

2024:

- The JVCEA plans to streamline the listing process for digital currencies, aiming to simplify the approval process for existing tokens in the market.

- The lengthy pre-screening process for certain digital assets by authorized exchanges is expected to be eliminated.

- The Cabinet approved a bill that may allow venture capital firms' investment tools to directly hold digital assets.

Japan's Efforts to Adopt Web3

Japan's weaknesses in Web3 adoption stem from regulatory constraints, particularly regarding exchange listings and taxation. Exchange listings are subject to strict regulation by the FSA, and local CEXs lack major tokens, failing to provide stablecoin liquidity (Figure 4).

Figure 4: Limited products on local CEXs. Note: We focus on USDT pairs from Binance and ByBit, as neither offers USD against fiat currency. For ByBit, $SHIB and $BONK are offered in blocks of 1000 units ($1000BONK and $SHIB1000).

Apart from Bitbank, which has a slightly higher token issuance volume among Japanese exchanges, this reinforces the dominance of major exchanges in Japan (Figure 5):

Figure 5: Market share of trading volume for the top 2 assets on Japanese and international top centralized exchanges. Duration: 2024 to present.

Meanwhile, cryptocurrency gains are classified as miscellaneous income and are therefore taxed at personal income tax rates plus local taxes, with a maximum rate of 55% (Figure 6).

Figure 6: Japan imposes excessively high capital gains tax on cryptocurrencies.

Before institutional interest emerged, the trading volume in yen once exceeded that of the dollar, but the aforementioned challenges have made the situation challenging.

Figure 7: Market share of yen in global fiat currency trading volume.

The yen's absolute dominance (which once accounted for over 60% of all fiat currency trading volume) was short-lived and gradually became irrelevant during the COVID-19 pandemic (Figure 7). However, over time, the total share of Asian fiat currency trading volume has remained stable, with trading volume shifting from yen to won (Figure 8).

Figure 8: Yen trading volume relative to other currencies' market share.

Notably, when we adjust the trading volume of yen and dollars to historical highs before November 2021, yen trading volume shows a stronger recovery in this cycle (Figure 9).

Figure 9: Yen and dollar trading volume adjusted to the previous high point of November 2021 = 100.

Institutionally, Japan is a country rich in content intellectual property, with companies like Sega and Kodansha, making it a preferred location for NFT and game-driven projects. Theoretically, these companies bring attention, users, research capabilities, and capital— the issue is that these areas perform in any country, and this has been touted as Japan's bull market for years.

Politically, there are recent concerns that the ruling party's push for deregulation may fail in the House of Representatives elections in April 2024, giving momentum to the opposition Constitutional Democratic Party. However, given the Liberal Democratic Party's continued majority in both houses of Congress and the increasing international and domestic competition for Web3 adoption, we believe these developments are not currently concerning.

Cryptocurrencies face many resistances, but simply put, many issues are cultural, making them unquantifiable and lacking simple solutions. For a globalized city with very low English proficiency, an inherent lack of entrepreneurial spirit, and stable jobs in local large companies still viewed as the pinnacle of employment for graduates, the corporate caution alongside the nature of cryptocurrency's "fast action" makes it hard to envision Japan's adoption rate catching up to its Asian neighbors anytime soon.

Key Players in Japan's Cryptocurrency Market

i) CEXs

As discussed in the previous section, Japanese centralized exchanges have struggled to compete in product offerings compared to their international counterparts, and high capital gains taxes make cryptocurrency trading unattractive. These challenges are reflected in the trading volumes of domestic exchanges, which, despite the observed differences outside of cryptocurrency exchanges, also lag behind foreign competitors in UI/UX.

Japan has 29 registered cryptocurrency asset trading service providers with the FSA, and we explore the current situation through charts.

BitFlyer is the largest exchange by trading volume and has maintained its dominance in recent years.

Figure 10: Market share of trading volume for Japanese CEXs.

However, compared to top international exchanges, domestic exchanges in Japan are almost non-competitive in trading volume. Since the pandemic, Binance has left Japanese exchanges behind.

Figure 11: Total spot trading volume of Japanese exchanges versus Binance.

When comparing the depth of the spot BTC order books of exchanges, this difference can also be observed.

Figure 12: 1% depth of spot BTC order books of Japanese exchanges versus Binance.

ii) Investment Groups:

SBI Digital

SBI Holdings (TYO: 8473) is a Tokyo-based financial services group founded in 1999. The company was initially part of the SoftBank Group and became independent in 2000. SBI Holdings operates in multiple sectors, including financial services, asset management, and biotechnology. The company is known for combining technology with traditional financial services to drive innovation and growth.

SBI provides a range of traditional financial and crypto services through its subsidiary B2C2, including custody solutions and market making.

iii) Protocols / Projects

Astar Network

Astar Network is a decentralized application (dApp) platform built on the Polkadot ecosystem and is one of Japan's leading crypto projects (although it is well-known that its headquarters is not in Japan but in Singapore). It was founded by Sota Watanabe, a prominent figure in Japan's blockchain space. Astar aims to provide developers with a scalable, interoperable, and decentralized network to deploy their applications. The network supports multiple virtual machines, including the Ethereum Virtual Machine (EVM) and WebAssembly (WASM), allowing developers to write smart contracts in various programming languages.

Astar is significant in Japan as it represents one of the country's leading blockchain projects, showcasing the growing interest and investment in blockchain technology from Japan's tech community. However, perhaps representing Japan's interest in Web3, activity on Astar is still in its infancy: Figure 13 shows the TVL (in USD) of the chain, while Figure 14 shows the growth of its native token's TVL.

Figure 13: Astar TVL compared to large blockchains in USD.

Figure 14: Astar TVL compared to Solana TVL, measured in its native tokens ($ASTR and $SOL), re-benchmarked to 01Jan23=100.

Conclusion

Despite leading in retail adoption, a combination of factors such as regulatory scrutiny following exchange hacks, high taxes, limited token offerings by exchanges, and cultural resistance have left Japan far behind other Asian countries in the Web3 space. The current government under the Liberal Democratic Party led by Kishida has a long-term vision, but progress is slow. The activities of local exchanges reflect this struggle, and it is hard to see what catalyst could change the tide for Japan.