Overview of the Development of Tokenized Assets RWA in 2024

Asset tokenization is an important trend in the cryptocurrency field that can enhance liquidity, reduce transaction costs, and attract more investors.

Asset tokenization is an important trend in the cryptocurrency field that can enhance liquidity, reduce transaction costs, and attract more investors.Author: ChíPhan

Compiled by: Lynn, Mars Finance

In recent years, the tokenization of assets (or real-world assets) has become a prominent trend and area of discussion in the cryptocurrency space. Our previous research—tokenizing and securitizing real-world assets on public blockchains—highlighted the potential of tokenization to enhance liquidity across various asset classes and reduce transaction costs for alternative assets. Recent findings from leading financial firms such as JPMorgan, Bain, Citigroup, Goldman Sachs, and BNY Mellon support this view: there is a widespread consensus that asset tokenization can help increase demand and enrich markets through more liquid and standardized assets, thereby expanding interest in these financial instruments. For investment banks, this opens up additional revenue streams through new issuance services for digital assets, potentially disrupting traditional IPO underwriting market shares in the long term. Alternative asset managers may find the global liquidity of tokenized assets and the secondary market that follows to be a valuable addition to their strategic toolkit, especially for their international investments. Furthermore, for investors, as the market for tokenized assets matures in the future, the emergence of new asset classes may alter the flow of capital, impacting investment strategies and returns.

Although we are still in the exploratory phase, the community has shown significant commitment to advancing this innovative concept through substantial infrastructure development as public blockchain infrastructure continues to evolve. Thus, the dialogue has shifted from questioning the benefits of asset tokenization to discussing its experimentation and implementation methods, with the aforementioned major companies eager to explore further.

The range of tokenization approaches lies between two extremes: (1) tokenizing assets on permissionless public blockchains, and (2) tokenizing assets on private networks and ecosystems. While each approach has its own advantages and disadvantages, we can expect many projects and investments to flood in to support the further development of more synchronized financial markets.

On public chains, stablecoins (or token cash) have demonstrated a dominant product-market fit for tokenized assets. The market capitalization of stablecoins exceeds $140 billion, nearly double the total trading volume of all other crypto assets combined. Led by BlackRock ($BUIDL) and Franklin Templeton ($FOBXX), the market capitalization of tokenized treasuries has also surpassed $1.2 billion. Given the risks posed by emerging technologies, the crypto community is also addressing the growing interest in asset tokenization by advancing the infrastructure of public chains. These advancements include the introduction of new smart contract standards such as ERC-4626, ERC-7540, and ERC-404, and support for creating customized blockchains for businesses exploring asset tokenization. These are significant steps toward more seamlessly integrating tokenized assets onto public chains.

On the other hand, there are also explorations of permissioned networks, such as the Canton Network, which aims to facilitate seamless financial transactions between private blockchains. While this approach offers enterprises more control and privacy to mitigate compliance issues, it requires substantial investment and resources to keep pace with the rapid development of applications and infrastructure on public blockchains.

Looking ahead, the path to a blockchain environment filled with tokenized assets seems increasingly feasible. The growth of asset tokenization is evident, but merely digitizing assets does not fully address the inherent issues of capital markets. The true value of digital assets will depend on their functionality and ease of circulation within the broader financial market, with asset tokenization serving as a foundational initiative toward a more integrated financial system. Ongoing experimentation and innovation in this field have the potential to change the dynamics of asset liquidity and trading efficiency while presenting challenges and opportunities for achieving a more cohesive and streamlined financial ecosystem.

Key Motivations for Asset Tokenization

In the challenging conditions of the 2022 cryptocurrency bear market, asset tokenization (RWA) remains a focal point for the industry. This approach leverages the transformative capabilities of public blockchain infrastructure to foster the growth of alternative asset capital markets. By facilitating deeper liquidity and lowering transaction costs, it aims to open doors for a diverse range of global investors.

Like any innovative concept, asset tokenization has faced skepticism and reasonable concerns. However, the fundamental argument for asset tokenization—centered on democratizing investment opportunities and streamlining capital flow efficiency—remains compelling.

The unparalleled success of securities is largely attributed to their high liquidity and low transaction costs. Recognizing this, we believe that enhancing the appeal of alternative asset classes depends on optimizing the same attributes (transaction fees and liquidity).

Existing financial structures, including sub-funds and master funds, provide channels for accessing alternative assets but come at a cost. They shift the operational burden from managers to distributors, increasing investor fees without offering the scalability, automation, or simplicity required for a digital, low-touch experience. In contrast, tokenization promises a more scalable and efficient process, thereby reducing management fees and ultimately benefiting end investors.

Reducing Transaction Costs

Tokenization is a key innovation for reducing the intermediary fees and administrative burdens inherent in traditional asset management. By adopting public blockchain ledgers and smart contract applications, tokenization can facilitate direct transactions between parties, bypassing intermediaries. This should encourage more trading activity and enrich the liquidity of asset classes.

Enhancing Liquidity of Traditional Illiquid Assets

Low transaction costs also encourage market makers (or liquidity providers) to engage in order books, thereby increasing the liquidity of alternative asset classes. Furthermore, tokenization harnesses the power of public ledgers to simplify transactions and introduce transparency, particularly for cross-border transactions. This approach has the potential to transform traditional illiquid assets (such as real estate or artwork) into more liquid investments, thereby expanding the market and investor base (even with stringent KYC and KYB processes). According to a recent report from JPMorgan Onyx Digital Assets, asset tokenization on the blockchain can streamline operations for alternative asset managers, reducing the complexity and costs associated with legal processes and capital management. This efficiency not only makes investment products more competitive but also allows managers to focus on strategic decision-making rather than administrative duties.

The same publication also noted that tokenization fundamentally changes asset management through data standardization, workflow collaboration, and process automation. These advancements can not only alleviate costs associated with manual reconciliation but also pave the way for investor-friendly innovations such as automated capital calls and automatic ownership transfers.

Another report from Citigroup, "Bringing Traditional Assets into the Digital Network: Exploring Tokenization in Private Markets," delves into how traditional assets can be integrated into digital infrastructure. The report reveals the potential of tokenization to enhance accessibility and efficiency in private markets.

Citigroup, Wellington Management, and WisdomTree have practically demonstrated these concepts using the Avalanche Evergreen subnet "Spruce." The Spruce subnet is a dedicated blockchain with features tailored for institutional use. Features of the Spruce subnet include multi-tier permissions, Ethereum Virtual Machine (EVM) compatibility, and extensive customizability.

This proof of concept showcased the tokenization of traditional assets (a private equity fund issued by Wellington Management) and their introduction into the digital network. ABN AMRO participated as an investor, WisdomTree represented the wealth management platform, and Citigroup acted as the issuer's agent on Spruce. These experiments and studies indicate that through tokenization, the market will undergo a significant transformation toward a more streamlined, efficient, and accessible direction. They reveal the potential of blockchain to overcome traditional barriers, opening up new possibilities for asset management and investment.

Citigroup's exploration of asset tokenization has yielded positive results, marking the entry of traditional markets into a new era:

"Tokenization unlocks the value of traditional markets for new use cases and digital distribution channels while achieving higher automation, more standardized data tracks, and even improved overall operating models, such as those driven by digital identity and smart contracts. These are significant advantages compared to traditional models."

"Combined with segmentation, greater transparency, and liquidity in secondary trading, this capability can open up asset classes that have previously been inaccessible to a broader range of investors, such as private assets."

"We expect tokenization to soon begin driving tangible utility through its supported new use cases. The programmability offered by digital tokens makes traditionally unfeasible models possible, such as automated rule-based asset allocation. Making private assets easier to trade and faster to settle may also facilitate their use in automated model portfolios."

Overview of Tokenization Verticals and Key Developments

As mentioned earlier, the scope of tokenization lies between two extremes:

(1) Tokenizing traditional assets on permissionless public blockchains, leveraging the infrastructure, applications, and liquidity resources available on public blockchains.

(2) Tokenizing assets on private permissioned blockchains within controlled systems.

Tokenizing Assets on Permissionless Public Blockchains

At first glance, stablecoins may seem unrelated to "real-world assets." However, from a financial and accounting perspective, cash is one of the most fundamental assets. Therefore, it is reasonable to include stablecoins (representing $140 billion tokenized on public blockchains) in the discussion of tokenization innovations.

The Stablecoin Wars: Battling for Volume

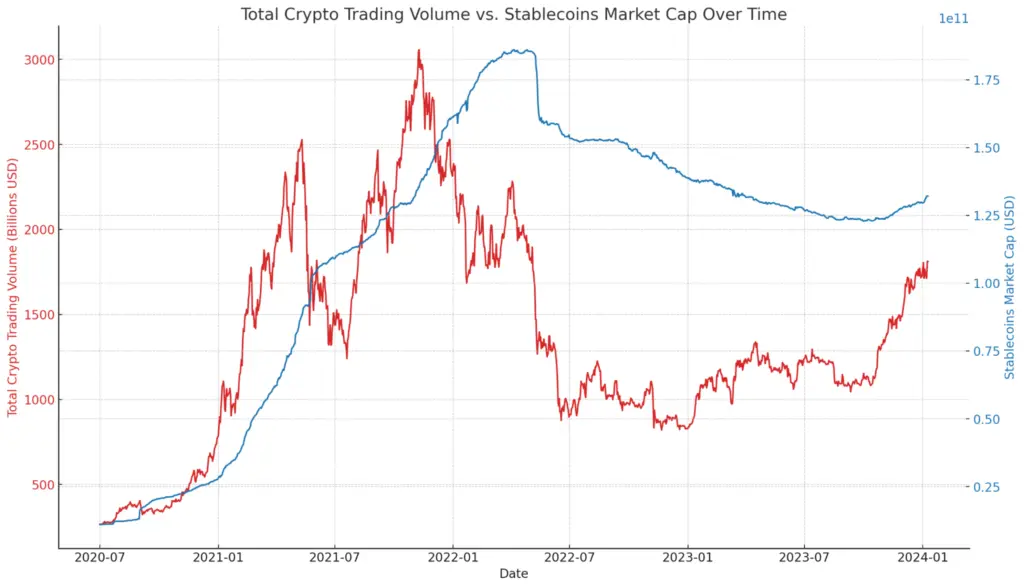

Despite a market capitalization lower than the peak during the 2021 bull market, stablecoin trading volumes have shown resilience and signs of recovery over the past six months, reflecting positive sentiment across the cryptocurrency market. However, trading volumes remain below peak levels.

A notable aspect of this resilience is the moderate positive correlation between the total trading volume of cryptocurrencies and the total market capitalization of stablecoins, with a correlation coefficient of about 0.50. This suggests that as the market capitalization of stablecoins grows, the overall trading volume of cryptocurrencies also increases, although this relationship is not entirely linear.

It is worth noting that the trading volume of stablecoins has surpassed the total of all other crypto assets combined, including major players like Bitcoin and Ethereum. This underscores the critical role stablecoins play in providing liquidity and stability in a turbulent cryptocurrency market.

Recent developments have witnessed significant breakthroughs in the stablecoin space. PayPal's launch of PYUSD marks an important milestone, making it the first publicly traded company to introduce a global stablecoin product. This ERC-20 token is backed by highly liquid assets, promising ease of redemption and widespread use, leveraging PayPal's vast user base for rapid adoption. Within eight months of its launch, PYUSD's market capitalization has exceeded $150 million, peaking at $270 million in the first two months of 2024.

Similarly, Hong Kong-based First Digital Labs, supported by Binance, has also made waves with its yield-bearing stablecoin FDUSD. FDUSD achieved a market capitalization of over $2.4 billion in just a few months, quickly ranking among the top five digital assets by trading volume, highlighting the vibrancy and competitiveness of the stablecoin market.

These developments indicate that the stablecoin market is thriving and will play an increasingly important role in the cryptocurrency ecosystem. As the market continues to mature, the entry of established financial institutions and the introduction of innovative products like yield-bearing stablecoins will further shape the future of digital asset trading.

Beyond Stablecoins: A Broader RWA Ecosystem

With the emergence of tokenized yield assets, the financial sector is undergoing a transformative wave, integrating traditional finance with the transparency and efficiency of blockchain. By tokenizing assets such as private credit or alternative investments like real estate, issuers can represent fractional ownership of these assets as digital tokens on a blockchain network. These tokens entitle holders to share in the underlying asset's income, which may include rental income, interest payments, or other forms of revenue. Using smart contracts can automatically distribute income to token holders, ensuring a transparent and efficient process. Over the past two years, many yield asset projects have successfully launched.

Franklin Templeton launched the first registered mutual fund in the U.S. on a public blockchain, allowing investors to directly purchase shares through the BENJI token. This approach marks a leap in combining mutual funds with blockchain technology, providing a seamless and efficient investment process.

Centrifuge stands out by creating a transparent market for lending real-world assets without traditional intermediaries. By tokenizing assets such as mortgages and invoices, Centrifuge enhances liquidity and provides a new avenue for crypto-backed lending, showcasing the versatility of DeFi applications.

Ondo Finance showcases a unique combination of tokenization strategies, from providing on-chain exposure to traditional ETFs to facilitating the trading of tokenized stocks. Their efforts to bridge the gap between traditional securities and blockchain reflect the growing intersection between DeFi and traditional finance.

Maple Finance targets a niche market for institutional and accredited investors, offering customized on-chain lending opportunities. They focus on high-quality loan pools, indicating that the scope of blockchain applications is continually expanding to meet the complex needs of seasoned investors.

These platforms highlight the critical shift toward a more inclusive, efficient, and integrated financial ecosystem. Tokenized yield assets represent an emerging field that can redefine investment models, providing new opportunities for growth and diversification in the digital age.

The journey of real-world asset (RWA) tokenization is paved by the efforts of numerous protocols, such as Goldfinch, Tokeny, Securitize, and Polymath.

Ongoing Development of the Infrastructure Layer

- Technological Advances in Ethereum: The Ethereum network has made significant progress with the introduction of ERC-4626, a tokenized vault standard that simplifies and standardizes the technical parameters of yield vaults. This standard streamlines integration work and enhances interoperability. Additionally, the proposed ERC-7540 expands these capabilities, providing asynchronous deposit and redemption features to accommodate more complex use cases.

- Collaboration Initiatives on Avalanche: On the Avalanche platform, JPMorgan's Onyx team is leading proof-of-concept efforts to explore asset tokenization beyond its main platform, leveraging interoperability protocols and the Avalanche Evergreen subnet to enhance connectivity. Furthermore, Avalanche has facilitated collaboration among other leading financial institutions through the Spruce Evergreen subnet, which aims to conduct institutional testing of on-chain finance. These subnets can be customized according to institutional needs, combining the innovations of public networks with the security and specificity required by enterprise applications.

- Polygon Chain Development Kit (CDK): This multifunctional modular framework is designed to support the development and deployment of Ethereum-compatible blockchain networks. It serves as the cornerstone for building scalable and interoperable blockchain solutions within the Polygon ecosystem, including Layer 2 solutions and sovereign Ethereum chains. With the Polygon SDK, developers can create platforms that make tokenized assets more accessible, liquid, and synchronized in the growing digital economy.

- Chainlink Cross-Chain Interoperability Protocol (CCIP): This protocol facilitates communication and interoperability between different blockchain networks, securely transmitting data and value using Chainlink's decentralized oracle network. This functionality aids in executing tokenization. CCIP enhances this process by ensuring that tokens representing RWAs can be easily managed, traded, and securely transferred across multiple blockchain platforms. This not only expands the accessibility and liquidity of such assets but also significantly enhances their utility across various applications, particularly in the decentralized finance (DeFi) space.

Tokenizing Assets on Customized Permissioned Blockchains

On the other hand, strategies for tokenizing assets on customized permissioned blockchains have also gained attention.

For example, the Canton Network (a public permissioned blockchain) successfully demonstrated its ability to facilitate atomic transactions (delivery versus payment, or DvP) across enterprises using a Global Synchronizer powered by composable smart contracts. Each participating institution has its own Canton node to access applications on each permissioned blockchain and connect to the Global Synchronizer to facilitate atomic transactions across various Canton blockchain networks.

While this approach maintains the privacy and control required by regulators, it necessitates a certain level of development investment to keep pace with the evolving application layers and sources of liquidity on public chains. Therefore, it will be interesting to observe whether these enterprise blockchains can interact and synchronize with public chains to drive market progress more rapidly.

In cases where enterprises have clearer requirements for control and privacy, they can also use Avalanche's technology stack (developer tools) to create their own customized private blockchains (dedicated subnets). However, tokenized assets on these chains need to be transferred to other subnets via the Teleporter Bridge.

In the aforementioned tokenization report, Citigroup also emphasized the ongoing development of transaction-level privacy technologies, such as zero-knowledge proofs (ZK) and fully homomorphic encryption (FHE), which will further help protect the privacy of financial transactions containing confidential or proprietary information.

Asset Tokenization—The First Step Toward More Synchronized Financial Markets

A statement in the pilot report from the Canton Network succinctly summarizes the current state of digital assets:

"Asset tokenization is on the rise, but presenting assets in new digital forms is insufficient to address the deep-rooted industry challenges in capital markets. The true value of digitally native assets lies in their utility and liquidity in financial markets. Asset tokenization is the first step; it is a driver for achieving more synchronized financial markets. But as we move beyond the first phase of digital issuance, financial institutions and their clients are asking, what comes next?"

When tokenized assets are locked on balance sheets or opportunities are limited in illiquid or poorly connected secondary markets, their value is constrained. The next building block will help create a composable system where different tokenized assets existing on various ledgers (including public and private ledgers) can be exchanged, swapped, or transferred to other ledgers with minimal execution risk.

The initiatives of these major blockchain ecosystems highlight the collaborative efforts driving the tokenization of alternative assets. By developing an infrastructure layer tailored to institutional application needs and raising interoperability and efficiency standards, the blockchain community is laying the groundwork for a more accessible and efficient digital asset space.

Tokenizing assets onto blockchains is now a solved problem, as evidenced by the market capitalization of stablecoins and yield assets (treasury bills) and the on-chain availability of other alternative asset classes. Additionally, dozens or even hundreds of projects are quietly advancing, exploring the incorporation of various assets into blockchains.

Tokenization products for treasuries have gradually gained acceptance. Chart: rwa.xyz

The next challenge is to increase demand for these tokenized assets, which will involve enhancing their liquidity and utility, educating a broader range of investors, while balancing the benefits of lower transaction costs with any slightly higher and unknown technological risks inherent in new technologies.

While tokenizing assets on permissionless public blockchains can leverage the growing liquidity on-chain, the trustless nature of these blockchains may subject the ever-growing tech stack and applications to stringent regulatory scrutiny. On the other hand, tokenizing assets on private networks and ecosystems, while providing the necessary customization and configuration to meet evolving regulatory requirements, may be at a disadvantage compared to permissionless public methods, particularly in developing application layers to attract users and investors.

As these technologies continue to evolve, the collaborative efforts of blockchain ecosystems, financial institutions, and dedicated protocols will fundamentally transform asset management and trading. This shift could reshape the investment and financial landscape into a system characterized by robustness, improved capital flow efficiency, and greater transparency, offering a broader range of on-chain and off-chain financial instruments.