SignalPlus Macro Analysis (20240508): ETF funds have seen net outflows for three consecutive weeks

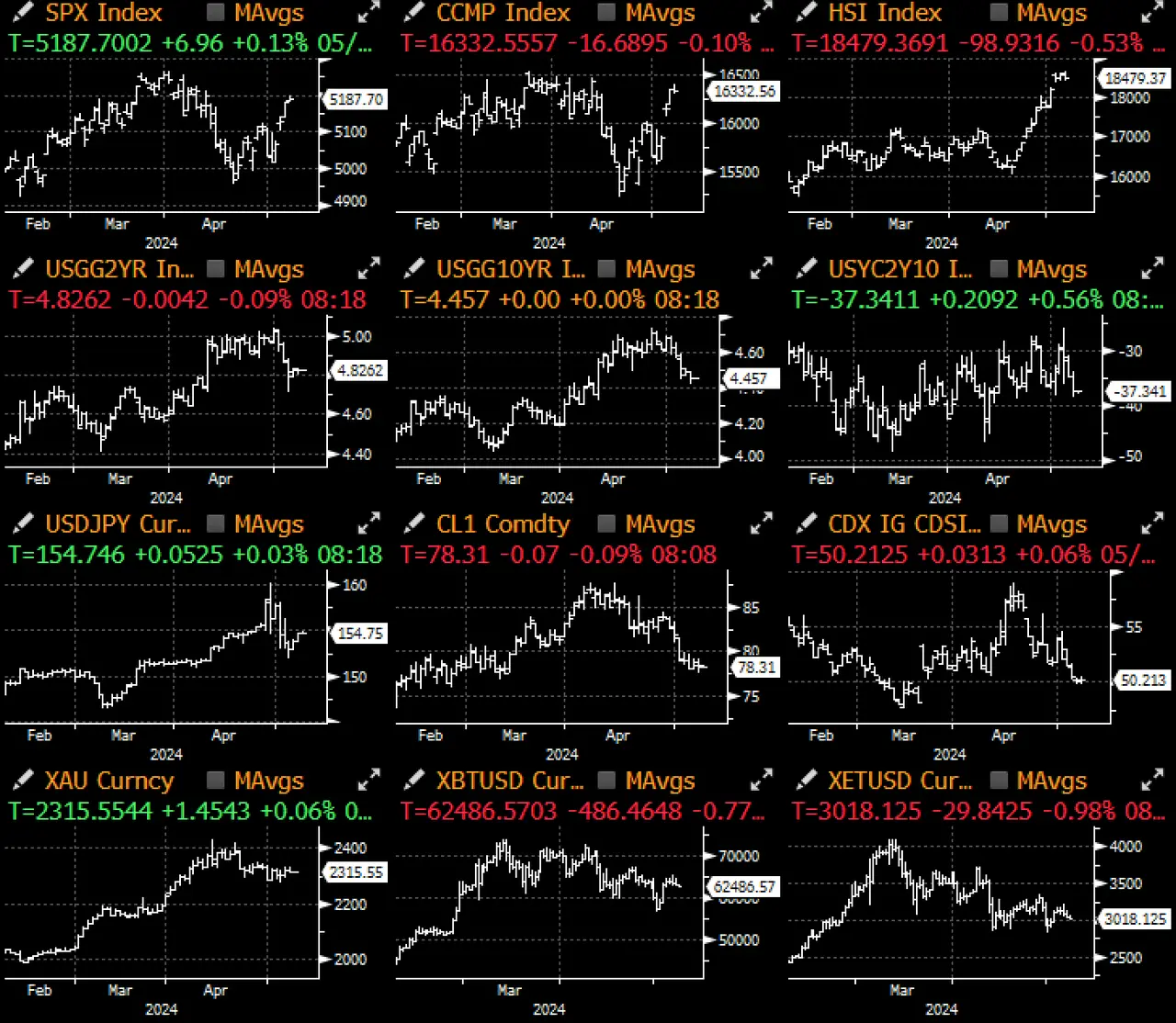

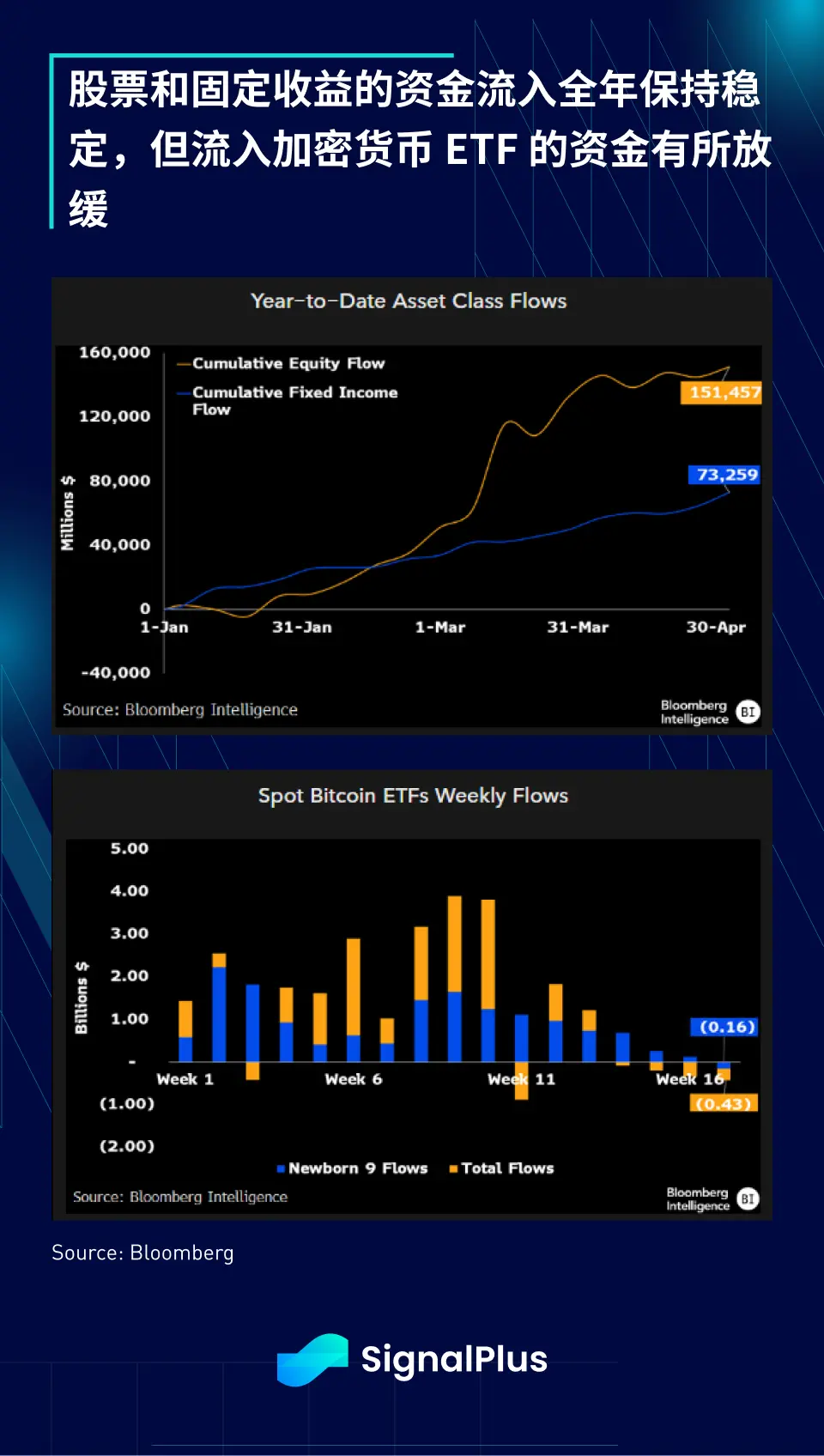

Macro assets experienced another calm trading day, with prices remaining largely stable. Several Federal Reserve officials spoke, revealing differing viewpoints. ETFs saw outflows for three consecutive weeks, with Greyscale experiencing a significant outflow of $459 million.

Macro assets experienced another calm trading day, with prices remaining largely stable. Several Federal Reserve officials spoke, revealing differing viewpoints. ETFs saw outflows for three consecutive weeks, with Greyscale experiencing a significant outflow of $459 million.

Macro assets experienced another calm trading day, with prices remaining largely stable. Several Federal Reserve officials spoke, revealing differing views. New York Fed's Williams (moderately dovish) echoed Powell's sentiment, stating that the Fed's interest rate policy will be determined by "overall data, not just CPI or employment data." He also reiterated that "we will eventually lower rates," but that monetary policy is currently in a "very good position," and that the labor market is achieving "better balance" following the release of non-farm payroll data. On the other hand, Minneapolis Fed's Kashkari (hawkish) indicated that rates may need to remain at current levels for a "prolonged period," and that "we may need to stay put for longer than expected until we know what effect monetary policy is having." He also sought to keep the option of rate hikes open, stating, "I think the threshold for (the Fed) to raise rates is quite high, but not infinite. When we say 'well, we need to do more,' there is always a line, and that line is inflation stubbornly remaining around 3%."

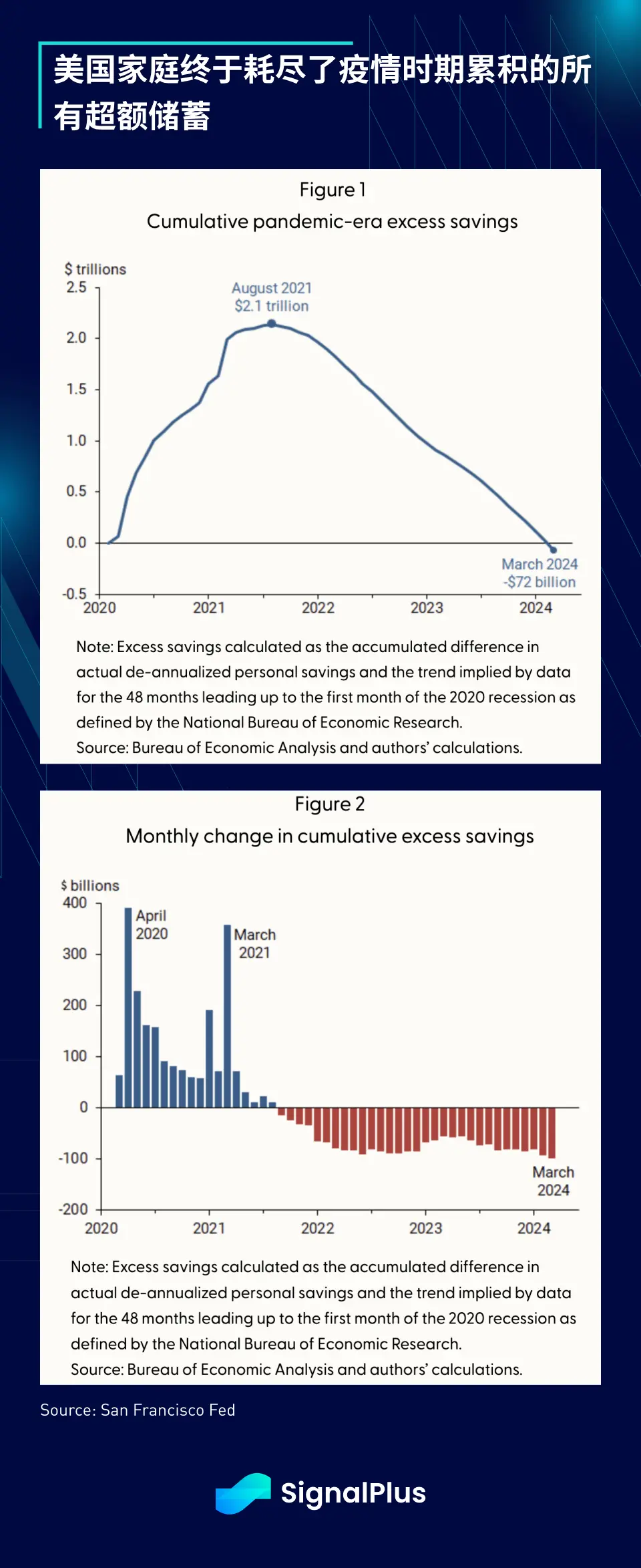

In terms of data, comments released by the San Francisco Fed over the weekend noted that the excess savings accumulated during the pandemic have been depleted, dropping from a peak of $21 trillion in August 2021 to -$72 billion in March of this year. Directly quoting the Fed's comments: "As long as they can support their consumption habits through sustained employment or wage growth… and higher debt, it is unlikely that the depletion of excess savings will lead to a significant reduction in spending by American households." While this may indeed be the case currently, this phenomenon, combined with higher interest rates and a slowing job market, will certainly prompt macro observers to start paying attention to more signs of economic slowdown.

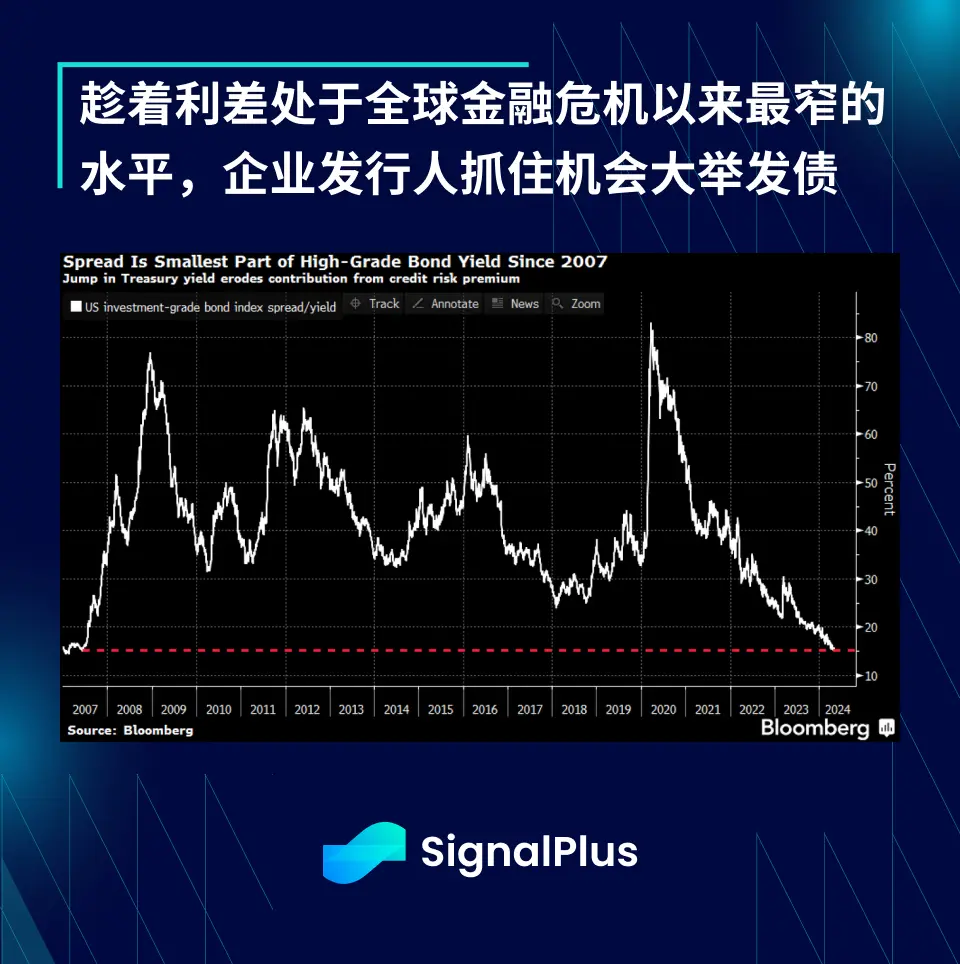

There isn't much to note regarding asset prices, but companies are taking advantage of the current period of low activity to launch another round of bond issuance. On Tuesday, up to 14 companies announced bond offerings, with over $34 billion in new bonds priced in just the past two days, far exceeding previous expectations. And although corporate bond spreads are at their narrowest levels since 2007, demand remains quite strong, with oversubscription exceeding 4.4 times.

In terms of fund flows, despite currently high valuations, inflows into equities and fixed income remain steady this year, with no signs of stopping. In the cryptocurrency space, ETFs have seen outflows for three consecutive weeks, with Greyscale experiencing a significant outflow of $459 million (IBIT data has not yet been updated), causing BTC prices to drop by 2-3% in New York's late trading.

On a positive note, according to the FTX restructuring plan, "98% of FTX creditors will receive at least 118% of their claims within 60 days after the plan takes effect," while "other creditors will receive 100% of their claims, with billions of dollars in compensation to account for the time value of their investments." After liquidating all assets, FTX is expected to have up to $16.3 billion in cash available for distribution, far exceeding the total amount owed to creditors of $11 billion. Ironically, this could become the largest single liquidity 'off-ramp' event in cryptocurrency history. Will creditors reinvest these recovered funds into cryptocurrencies, or will they return to traditional assets? It's truly an interesting time.