Grayscale April Market Report: Macro Storm Approaches, Yet Crypto Market Surprisingly Bullish?

Under the premise of a stable overall macro market environment, cryptocurrency prices are expected to welcome new upward space in the second half of 2024.

Under the premise of a stable overall macro market environment, cryptocurrency prices are expected to welcome new upward space in the second half of 2024.Original Title: April 2024

Author: Grayscale

Compiled by: BitpushNews Yanan

- Affected by the tightening macroeconomic environment, the cryptocurrency market experienced a certain degree of correction in April. Notably, due to the robust growth of the U.S. economy and persistently high inflation levels, the probability of the Federal Reserve cutting interest rates this year has significantly decreased, which undoubtedly puts some downward pressure on the cryptocurrency market.

- However, from the overall development trend of the crypto industry, the market outlook remains optimistic. The Bitcoin halving event, the increasing activity in the Ethereum ecosystem, and the potential positive progress in U.S. stablecoin legislation all demonstrate the strong growth momentum within the industry.

- The Grayscale research team believes that, provided the overall macro market environment remains stable, cryptocurrency prices are expected to welcome new upward space in the second half of 2024.

After experiencing seven consecutive months of growth, Bitcoin's price encountered a 15% decline in April 2024, which also led to a downward trend in the entire cryptocurrency market. Despite a series of positive fundamental news in April—such as the Bitcoin halving and significant progress in stablecoin legislation in the U.S.—these positive factors did not fully offset the market pressure brought about by the tightening macroeconomic environment.

After considering risk-adjusted factors (i.e., incorporating the volatility of each asset into the assessment), we found that the return rates of Bitcoin and Ethereum are at a moderate level compared to traditional assets (as shown in Figure 1). In April, gold and oil prices showed an upward trend, partly due to the escalation of tensions in the Middle East. However, at the same time, most other mainstream asset classes exhibited a downward trend.

Figure 1: Macro tightening drags down the performance of various assets in April

The core reason for this market weakness seems to lie in the strong performance of nominal U.S. economic growth, which makes the prospect of interest rate cuts by the Federal Reserve appear bleak. At the beginning of April, the U.S. Department of Labor released a report indicating that employment increased by about 300,000 in March, with an average monthly growth of about 275,000 in the first quarter. Subsequent reports showed that the "core" Consumer Price Index (CPI) had an annualized growth rate exceeding 4% for the third consecutive month. With the release of a series of strong economic data, statements from Federal Reserve officials in public settings seemed to suggest that the possibility of rate cuts was gradually diminishing.

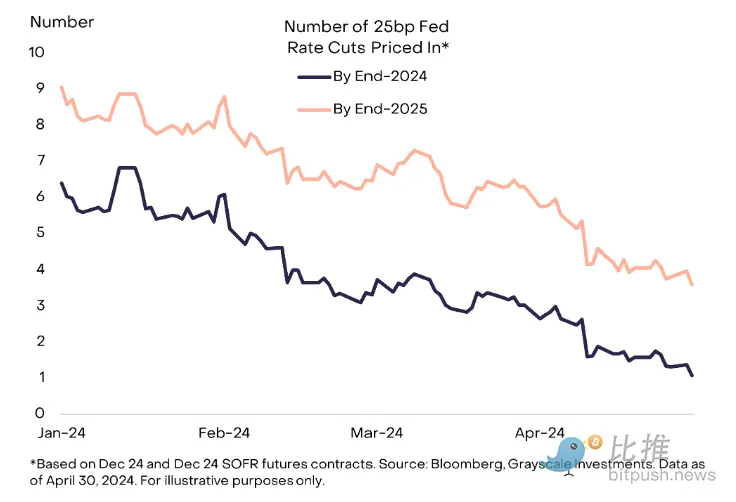

At the end of March, the market generally expected that the Federal Reserve would cut rates three times by the end of 2024, with each cut being 25 basis points. However, by the end of April, this expectation had been significantly reduced to only one rate cut, also by 25 basis points (see Figure 2). This change reflects the market's re-evaluation of the Federal Reserve's future monetary policy.

Since Bitcoin is viewed as an alternative currency system that competes with the U.S. dollar to some extent, the rise in real interest rates over the past month may have supported the value of the dollar to some degree. At the same time, this change in interest rates has also had a direct impact on Bitcoin's price.

Figure 2: The market currently believes that the number of Federal Reserve rate cuts will be relatively few

Although the market currently generally believes that the number of Federal Reserve rate cuts will be relatively few (as shown in Chart 2), last month's news revealed some important macro trends that could support Bitcoin's demand over a longer period.

Specifically, media reports indicated that if Trump successfully wins re-election, his second administration may implement a series of policy measures, including attempts to undermine the independence of the Federal Reserve (Wall Street Journal), deliberately devalue the dollar (Politico), and impose penalties on countries seeking to conduct more bilateral trade in non-dollar currencies (Bloomberg). These potential policy directions undoubtedly increase the uncertainty surrounding the dollar's outlook and may impact alternative currency systems like Bitcoin.

We have previously discussed the importance of these macro policy issues in detail, especially in the context of the upcoming elections, where these issues are particularly significant. Although the current campaign is still in its early stages, the latest related reports have highlighted that the election could bring considerable uncertainty to the medium-term outlook for the dollar. This uncertainty, in turn, may affect the medium-term trend of cryptocurrencies like Bitcoin.

Despite the macro market environment becoming more challenging, the cryptocurrency market in April still saw many positive factors. Among them, the most notable was Bitcoin's successful halving operation on April 20. This halving reduced the Bitcoin network's new coin issuance rate from approximately 900 coins per day to about 450 coins per day.

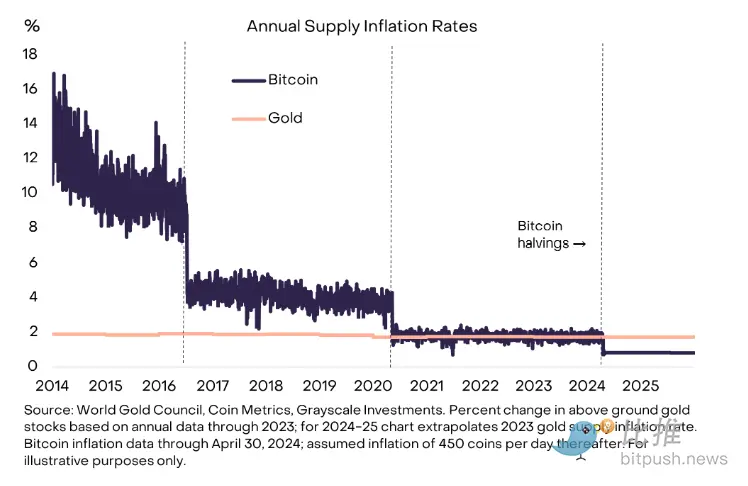

After the halving, the inflation rate of the Bitcoin network—i.e., the annualized rate of new coin issuance relative to existing supply—dropped from about 1.7% to approximately 0.8%. Notably, prior to the Bitcoin halving, its inflation rate was roughly on par with the supply inflation rate of gold; however, now, Bitcoin's inflation rate has significantly decreased (as shown in Figure 3). When calculated in U.S. dollars based on the current Bitcoin market price, the reduction in Bitcoin's daily issuance effectively means that its annual supply growth has decreased by about $10 billion.

Figure 3: Bitcoin's inflation rate is lower than gold's

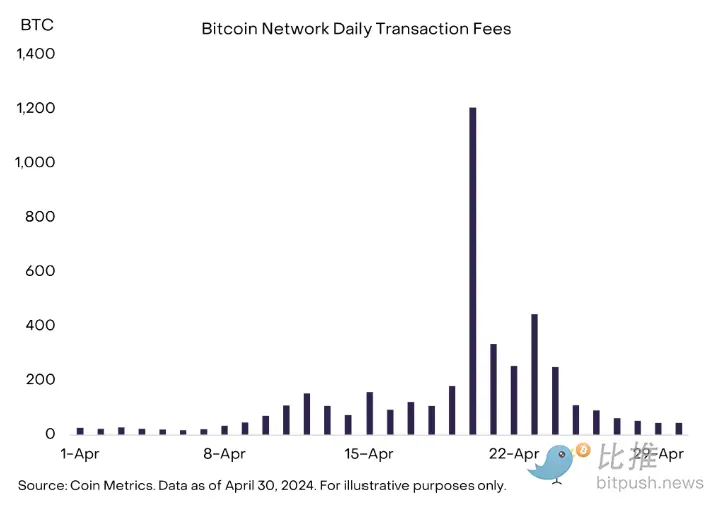

On the day of the halving, Bitcoin transaction fees saw a significant increase, primarily due to the emergence of Runes. Runes are a new type of fungible token standard on the Bitcoin network, created by the same developer who launched Ordinals. According to data, transaction fees collected by miners on the day of the halving reached approximately 1,200 BTC, a substantial increase compared to the previous daily average of 70 BTC. In the following days, daily transaction fees remained between 250 and 450 BTC until a downward trend was observed at the end of the month (as shown in Figure 4). However, the high transaction fees have made small transactions on the Bitcoin network prohibitively expensive, which may undermine Bitcoin's property as a medium of exchange (for example, the average transaction fee on the day of the halving was $124). Although the outlook remains uncertain, we initially predict that Bitcoin transaction fees will rise in the medium term to ensure miners' income. At the same time, we also need to seek broader scaling solutions to make Bitcoin payments more cost-effective and network usage more convenient.

Figure 4: Bitcoin transaction fees soared before and after the halving

In April, Ethereum's performance once again lagged behind Bitcoin, possibly due to the significantly reduced probability of Ethereum spot ETF approval in the U.S. According to data from the decentralized prediction platform Polymarket, as of the end of May, the probability of Ethereum spot ETF receiving regulatory approval in the U.S. has plummeted to 12%, down from 21% at the end of March and 75% at the beginning of January.

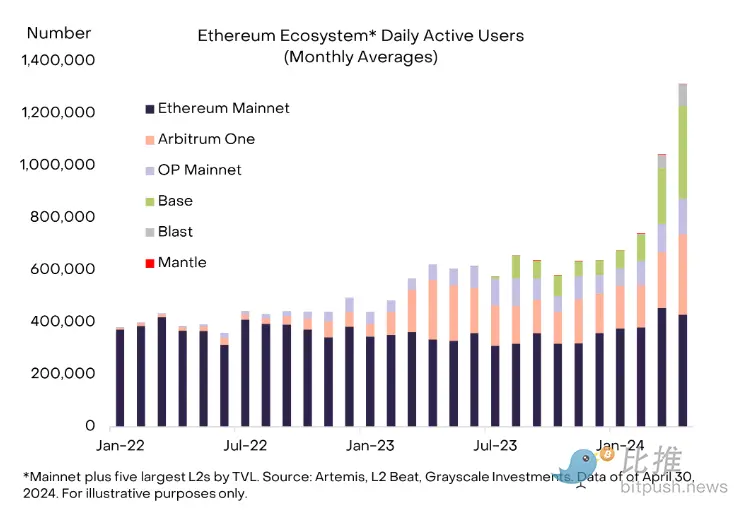

However, it is worth noting that on-chain activity within the Ethereum ecosystem has not been adversely affected; rather, it has shown continuous growth. In particular, in April, thanks to the momentum from Base and Arbitrum, the number of daily active users in the Ethereum ecosystem surged to 1.3 million (see Figure 5).

Despite the recent disappointing return rates, we remain optimistic about Ethereum. We believe that as the trend of tokenization continues to develop, Ethereum is likely to benefit from it.

Figure 5: The Ethereum ecosystem continues to grow

This month, there were several exciting pieces of news in the stablecoin sector. On April 17, Senators Lummis and Gillibrand jointly proposed a bipartisan bill aimed at establishing a clear legislative framework for stablecoins. The proposal is comprehensive, requiring stablecoin issuers to hold one-to-one reserves to ensure the stability of stablecoin value, and it also includes consumer protection measures, such as involving the Federal Deposit Insurance Corporation (FDIC) in case of failures. Notably, the proposal explicitly calls for a complete ban on algorithmic stablecoins.

Alongside legislative progress, payment giant Stripe also announced a significant move. The company will allow its customers to use USDC stablecoin for payments on networks such as Ethereum, Solana, and Polygon. For these rapidly developing projects, Stripe's decision is undoubtedly a positive signal.

In 2024, the stablecoin market has seen significant growth, with its total market capitalization rapidly rising from $130 billion in January to $160 billion now, an increase of 23%.

It is worth mentioning that since the beginning of 2023, Tether (USDT) has maintained a strong position in the stablecoin market. According to data in Figure 6, Tether currently accounts for 69% of the total market capitalization of stablecoins, representing an overwhelming advantage. However, despite Tether further expanding its market leadership in 2023, other stablecoins are also actively competing, presenting a diversified competitive landscape.

USDC, issued by U.S. Circle, has shown strong growth momentum in 2024. Statistical data shows that its market capitalization has increased by 36% so far, significantly higher than Tether's 20% growth during the same period.

Figure 6: Stablecoin market capitalization continues to grow

Both Bitcoin and Ethereum outperformed the FTSE Grayscale Cryptocurrency Industry Index in April. This index covers 243 tokens (or "altcoins") across five cryptocurrency sub-markets (Figure 7). The best-performing cryptocurrency sub-market in April was the currency sector (mainly due to Bitcoin's relatively stable price), while the worst-performing was the consumer and culture sector. The weakness in this sector also reflects the pullback adjustment trend of meme coins after their strong rise in March.

Figure 7: All five cryptocurrency sub-markets performed weakly in April

In most cases, the market's correction clearly reflects a broad decline in market sentiment. However, upon deeper analysis, we find that certain specific thematic trends still deserve close attention. For example, after adjusting for risk, the investment return rates of some decentralized exchange (DEX) tokens remain low. Another noteworthy example is Worldcoin (WLD), which experienced a price drop of up to 45% in April. Although the WLD team announced that they are building an Ethereum-based L2 network and actively exploring collaboration opportunities with OpenAI, these positive news did not effectively boost the coin's price. More concerning is that the WLD team plans to further increase token supply through new private sales, which may exert additional downward pressure on the price.

Other projects also have good news worth noting: Toncoin (TON) has recently performed well, successfully surpassing Cardano (ADA) to become the seventh-largest asset in the cryptocurrency space. The project further announced deep integration with the messaging tool Telegram and launched a series of community and developer incentive measures, which undoubtedly adds more appeal.

Additionally, over the past 30 days, the market's attention has also been drawn to SocialFi—decentralized social media applications. Notably, the FriendTech platform innovatively provides creators with an opportunity to monetize from online communities. On FriendTech, users can trade "keys" linked to Twitter accounts to access exclusive chat rooms. According to data from the analytics firm Kaito, FriendTech's popularity peaked in September 2023.

At the end of March, we judged that Bitcoin was entering the "fifth inning" of the current bull market cycle. If we borrow the metaphor of a baseball game, we may now have progressed to the "seventh inning": Bitcoin's valuation has receded, and the inflow of funds brought by Bitcoin spot ETFs has slowed. At the same time, indicators reflecting speculative traders' positioning (such as perpetual futures funding rates) have also declined. Given the shift in expectations regarding the Federal Reserve's monetary policy, the current pause in the upward trend seems reasonable—after all, the rise in real interest rates poses a fundamental disadvantage for Bitcoin.

However, from a broad macroeconomic perspective, the outlook still seems optimistic: the U.S. economy is on track for a soft landing, Federal Reserve officials are signaling the possibility of future rate cuts, and the results of the November elections are unlikely to trigger stricter fiscal policies. Furthermore, indicators used to measure Bitcoin's valuation, such as the MVRV ratio, are currently far below previous cyclical peaks (see Figure 8). As long as the macroeconomic outlook remains stable, we believe that Bitcoin prices and the total market capitalization of cryptocurrencies are still expected to continue rising this year.

Figure 8: Bitcoin valuation shows below previous peaks