SignalPlus Macro Analysis (20240429): Core PCE Data Remains Elevated

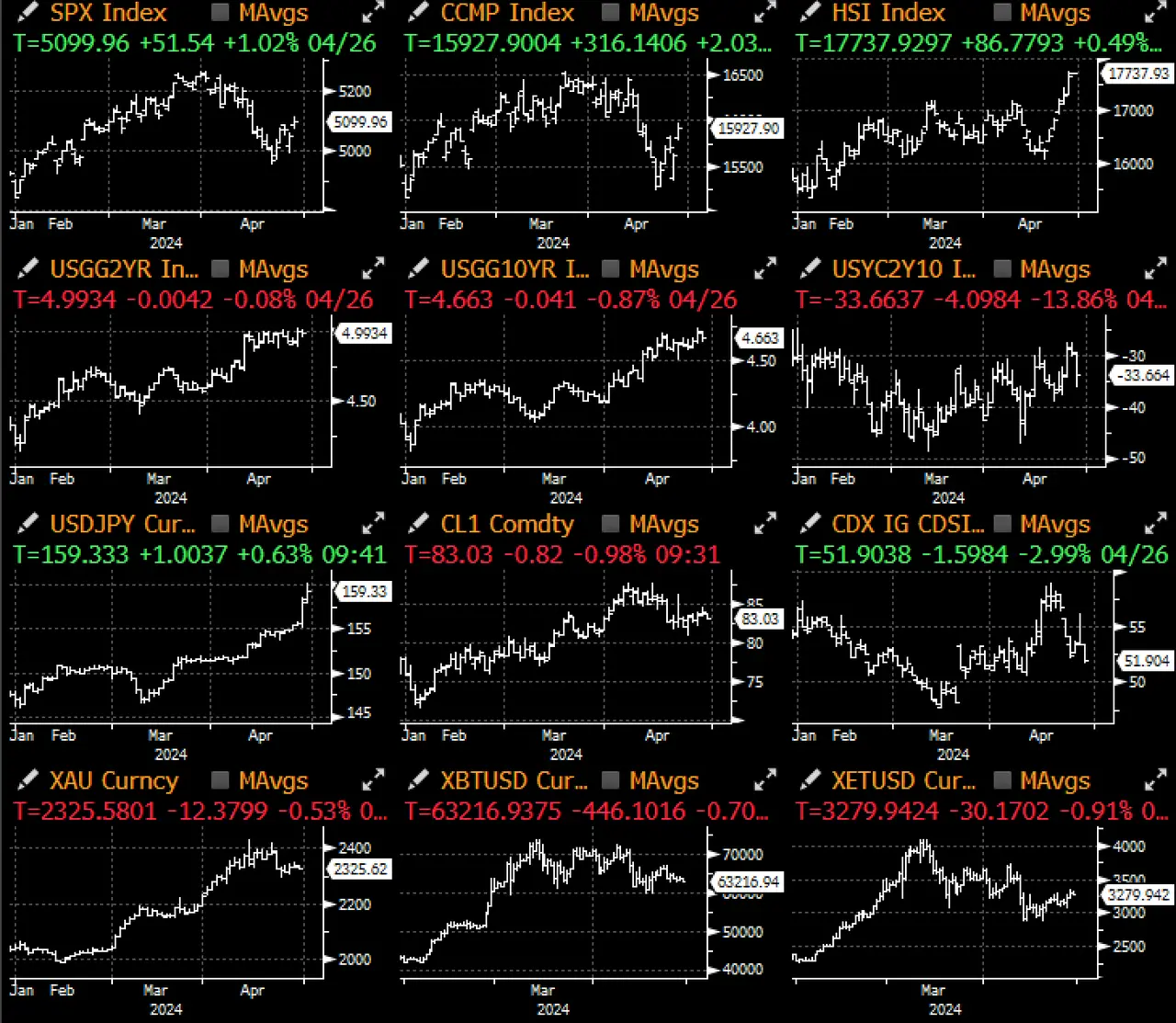

Last Friday, U.S. Treasury yields had a slight respite, and the core PCE data basically met analysts' slightly elevated expectations (overall and core month-on-month growth of 0.3%, year-on-year growth of 2.7% / 2.8%). Major ETF products did not show significant buying interest, with an outflow of $218 million last Thursday followed by another outflow of $84 million on Friday.

Last Friday, U.S. Treasury yields had a slight respite, and the core PCE data basically met analysts' slightly elevated expectations (overall and core month-on-month growth of 0.3%, year-on-year growth of 2.7% / 2.8%). Major ETF products did not show significant buying interest, with an outflow of $218 million last Thursday followed by another outflow of $84 million on Friday.

Last Friday, U.S. Treasury yields saw a slight respite, with core PCE data largely in line with analysts' elevated expectations (overall and core month-on-month growth of 0.3%, year-on-year growth of 2.7% / 2.8%). Meanwhile, core services rose by 0.39% month-on-month, up from 0.19% in February, and actual personal consumption expenditures unexpectedly increased, indicating that economic and price pressures are more stubborn than anticipated, adding further hawkish pressure ahead of this week's FOMC meeting. The University of Michigan consumer confidence index remained at 77.2; however, one-year inflation expectations rose from 2.9% in March to 3.2%, and five-to-ten-year inflation expectations increased from 2.8% to 3.0%.

However, as U.S. Treasury positions approached extreme bearishness and the PCE results were not worse than market expectations, interest rates fell across the board by about 3 basis points, while the Nasdaq index rose by 2% due to the trend in yields and strong earnings from tech stocks. On the other hand, the Japanese yen attracted more attention; relative to the hawkish Federal Reserve, the Bank of Japan continues to maintain a dovish stance, with the yen currently trading above 159, nearing a 25-year high of around 160.

The FOMC meeting will be the focus of attention this week, but the market will also be influenced by U.S. JOLTS and non-farm payroll data before and after the meeting. Additionally, CPI and Nvidia's earnings report are expected to be the biggest market movers later this month, as the chip giant seeks to reverse its worst monthly performance since October last year. Furthermore, the WSJ reported that allies of former President Trump are busy devising a secret plan to "eliminate" the independence of the Federal Reserve if he is re-elected, which is certainly difficult to achieve, but it is an interesting thought in some atypical scenarios (BTC to 200,000?).

Despite the U.S. economic data being uncooperative last week, U.S. corporate profits once again became a highlight, with strong performance so far leading to a 3.3% upward revision of Q1 2024 profits. Additionally, some companies have resumed dividends (Meta, Google), providing new growth momentum for SPX and others. Currently, other tech companies are also facing pressure to initiate dividend plans or convert some stock buybacks into cash payments, especially considering that many SPX companies have quite strong balance sheets and are fully capable of regularly distributing dividends.

In the cryptocurrency space, major ETF products have not seen significant buying interest, with $218 million flowing out last Thursday and another $84 million on Friday. Moreover, although still far above 2023 levels, the open interest in CME's BTC futures has significantly retreated from recent historical highs, with mainstream FOMO sentiment clearly slowing down, especially as the possibility of interest rate cuts diminishes. Native user interest remains focused on BTC runes/memecoins and ETH's L2 re-staking and other yield growth areas, which are relatively unfamiliar to general investors. We remain cautious about recent price movements and tend to adopt a wait-and-see attitude until the dust settles from the FOMC meeting and CPI data later in May.