SignalPlus Macro Analysis (20240419): The Federal Reserve states that there will be no interest rate cuts this year

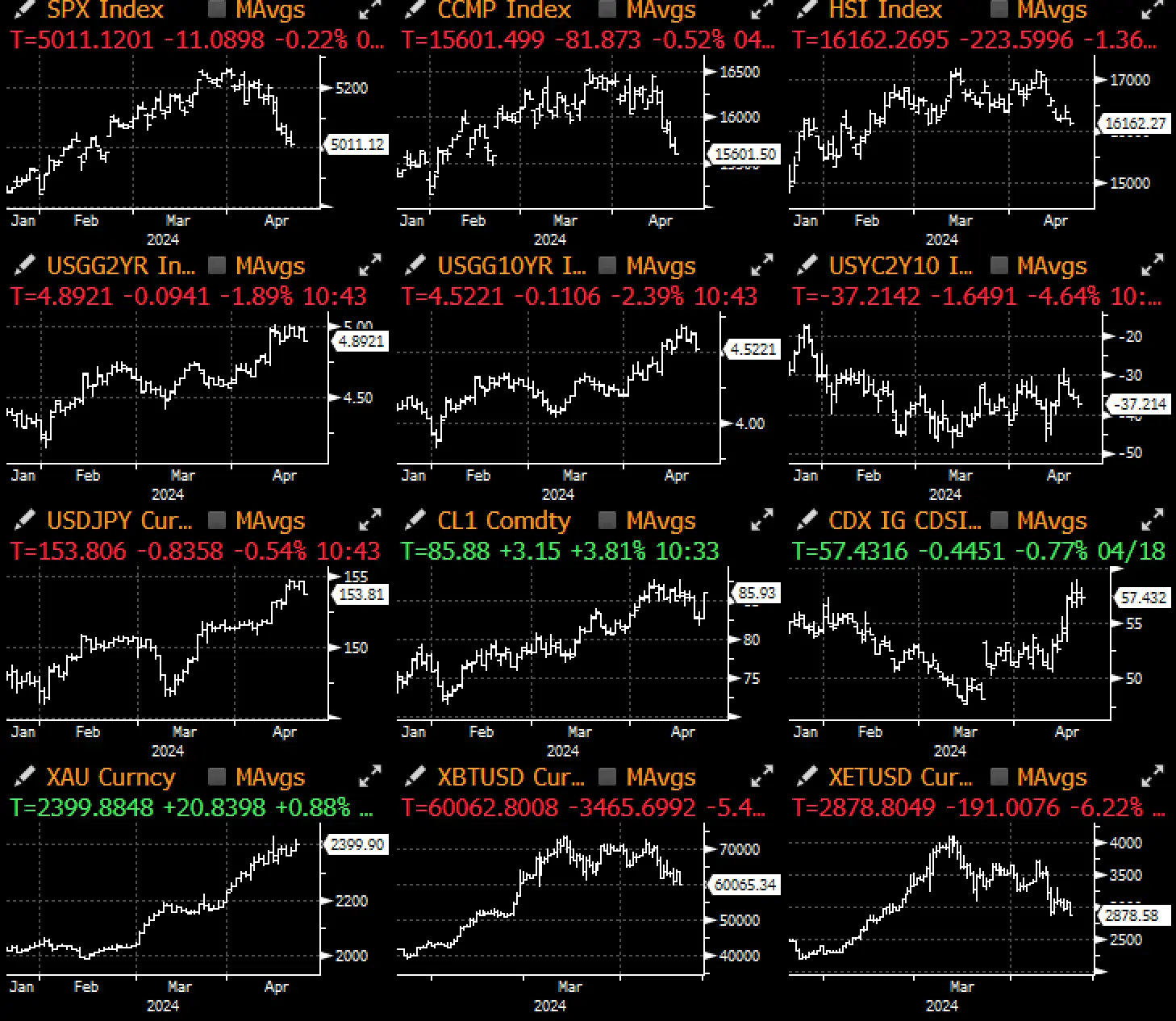

The U.S. market started off smoothly, and the geopolitical tensions and negative sentiment seem to be rapidly dissipating...

The U.S. market started off smoothly, and the geopolitical tensions and negative sentiment seem to be rapidly dissipating...

The U.S. market started off smoothly, with geopolitical tensions and negative sentiment seemingly dissipating rapidly. The initial jobless claims remained at an extremely stable level (around 210,000 for 5 out of the last 6 weeks), and the Philadelphia Fed Manufacturing Index climbed to its highest level since April 2022 (driven by new orders +12.2 and prices paid +23).

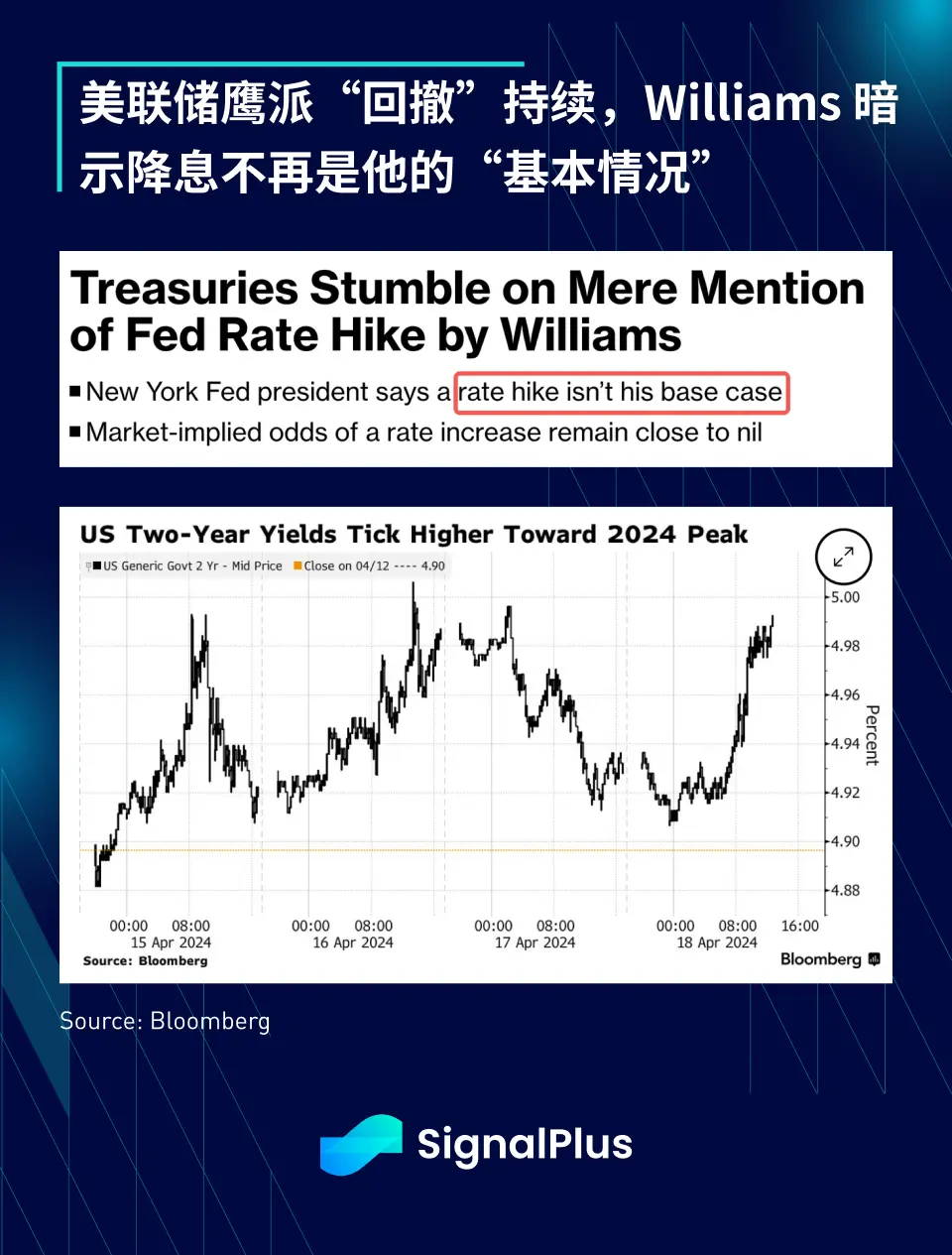

However, just after gaining a foothold for a day, U.S. Treasuries were hit hard again as New York Fed President Williams hinted that rate cuts were no longer his "baseline scenario," stating that rates are in a "good place" and "I don't feel there's an urgency for rate cuts." Yields jumped across the board by 5-6 basis points, with the 2-year yield approaching this year's high of around 5% again.

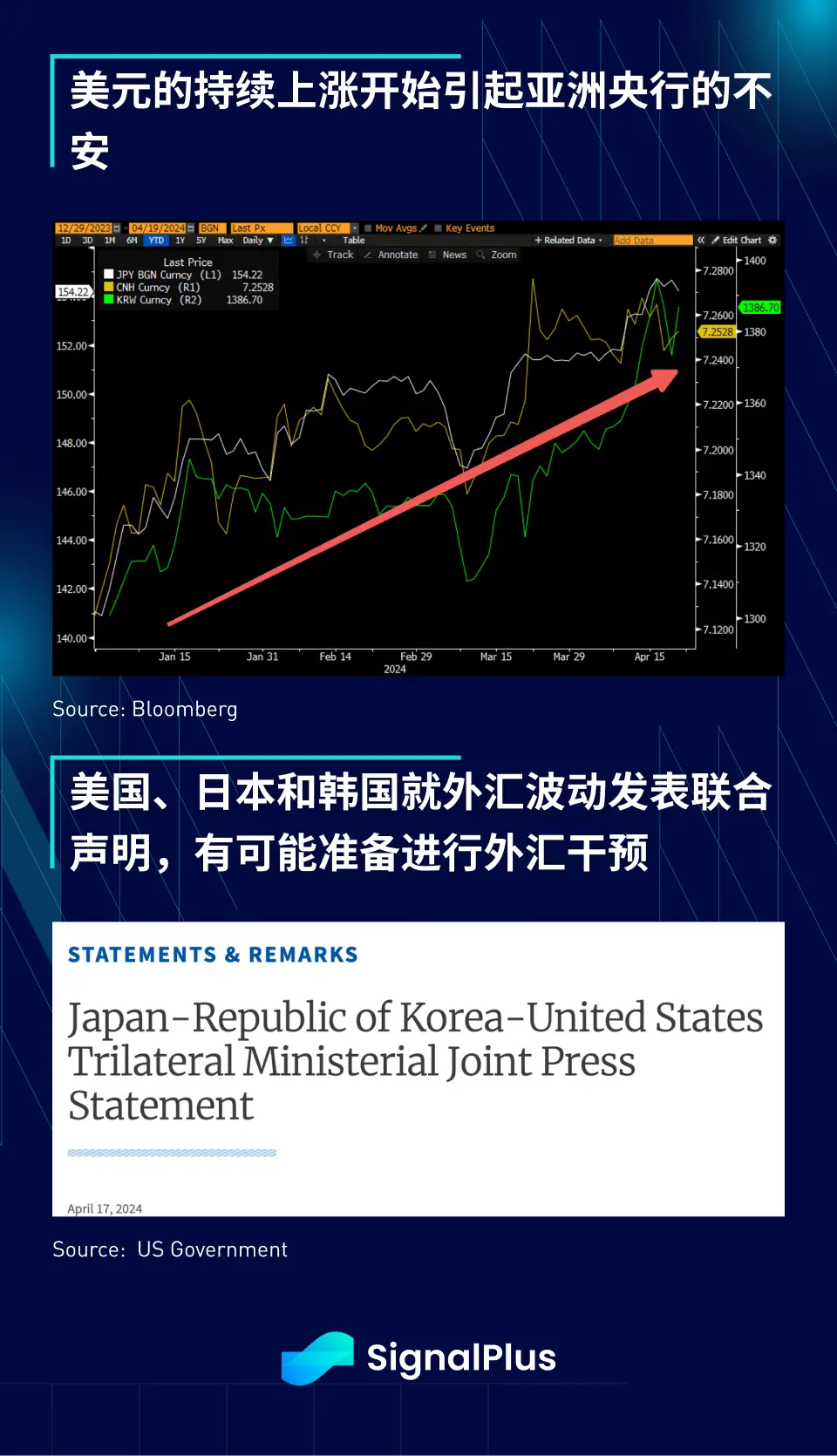

The significant rise in U.S. Treasury yields and the U.S. dollar index prompted a joint statement from U.S. Treasury Secretary Yellen, Japanese Finance Minister Suzuki, and South Korean Finance Minister Choi Sang-mok, stating that the three countries will "continue to closely consult on developments in the foreign exchange market, in line with existing G-20 commitments," while acknowledging concerns over the recent sharp depreciation of the yen and won. This indicates that if the trend continues, central banks in the Asian region may intervene in the foreign exchange market. Reuters later reported further news, with Japanese Finance Minister Suzuki stating that "the G7's confirmation of its commitment to prevent excessive fluctuations in exchange rates that could negatively impact the economy" is significant, suggesting that the trading risks brought by the news will return for a while.

Speaking of news-related risks, reports of Israel attacking Iran led to a rapid decline in all asset classes during the closing hours (SPX futures <5000, Nikkei index futures -3%, BTC dropping from 63,500 to below 60,000). As the war risk premium continues to escalate, risk sentiment may remain subdued as we head into the weekend. The inflow into BTC ETFs was also disappointing again, with IBIT only seeing an inflow of $37 million, while GBTC experienced an outflow of $90 million.

For the past 1.5 weeks, we have repeatedly mentioned reducing risk and protecting profits, as geopolitical conflicts do not seem to be resolved anytime soon. Additionally, macro data is unlikely to show any dovish easing before next Friday's PCE data release, meaning that caution is essential in trading over the next few days.

Risk warning Risk warning

Risk warning Risk warning