2024 BTC Halving Preview: Bullish in the Long Run, But Is It Worth Trading Now?

From a supply perspective, this is undoubtedly a bullish event.

From a supply perspective, this is undoubtedly a bullish event.Original Title: The 2024 BTC Halving Preview: Bullish but is it tradeable?

Original Author: Rick Maeda

Original Compiler: 深潮 TechFlow

Abstract

On the surface, the highly anticipated halving in the Bitcoin network has historically been bullish.

However, given the frequency of halving events and a careful study of BTC's performance in the overall market context, it is difficult to make any highly certain judgments based solely on the halving event itself.

Overall, the Bitcoin halving may not be a tradeable event, but structurally it is bullish from a supply perspective. Under the right macro conditions, BTC may rise again after the halving.

Main Text

The consensus around Bitcoin halving is that it is bullish, and the general belief is that it is a tradeable event. But is that really the case? In this article, we delve into past halving events and examine the supply and macro data surrounding the upcoming 2024 halving to gain a deeper understanding of what this pre-announced event means for investors.

What is Bitcoin Halving?

Halving is a pre-programmed event in the Bitcoin network that reduces the rewards for Bitcoin miners by half (for more on what this means, see below). It is an important mechanism in Bitcoin's monetary policy that ensures only 21 million BTC will be in circulation and prevents inflation by reducing the rate at which new BTC is created.

This pre-programmed update occurs every 210,000 blocks, roughly every four years, with the next estimated date being April 20, 2024. When Bitcoin was launched in 2009, the mining reward was set at 50 BTC, and after three halvings (in 2012, 2016, and 2020), the reward will soon drop to 3.125 BTC per block.

Bitcoin uses a proof-of-work (PoW) consensus mechanism to verify and secure transactions on the blockchain. In PoW, miners compete to solve complex mathematical problems, and the first miner to solve the problem correctly gets to add the next block of transactions to the blockchain. To verify transactions and add blocks to the blockchain, the winning miner receives newly created Bitcoin as a reward, which is "halved" during the halving.

The Reality of Historical Halvings

On the surface, halvings have proven to be very bullish for BTC.

Figure 1 shows the historical price movements of BTC before and after each previous halving day, from one year prior to one year after. The red dashed line shows the volume-weighted average of past halvings, while the black line shows the current BTC path.

Figure 1: Halving is Bullish for BTC

Figure 2 presents the performance of Bitcoin around the halving in tabular form.

Figure 2: Bitcoin's Performance Around Halving

With the upcoming halving scheduled for April 20, 2024, we infer the recent price data using the latest price on April 17, 2024.

The logarithmic scale y-axis in Figure 1 indicates that halving is a bullish catalyst, but considering we only have three observations, with the first observation at just $12.80 for BTC and the third occurring in May 2020 when all risk assets surged amid Covid, any interpretation of the data should be approached with caution. Additionally, when we observe the average one-year return of BTC since mid-2011, the one-year returns after halving do not appear impressive, except for the first halving in 2012.

Here, the 2020 halving raises an interesting question about the overall performance of global markets. In Figure 3, we replicate Figure 2, using stocks, specifically the S&P 500 index, as a benchmark for risk assets:

Figure 3: S&P 500 Index Performance Before and After Halving

The one-year average rolling return for SPX is +11.42% (consistent with the BTC historical price data we have since mid-July 2011), while its one-year average performance since the Bitcoin halving has exceeded +27%, more than double the average! This highlights an important reality that popular narratives often overlook. Just as we would not conclude that "therefore, the programmatic update that halves the rewards for miners in the Bitcoin network is very bullish for the S&P 500 index," we may also not be able to draw real conclusions from Bitcoin's past performance. Otherwise, by some measures, such as a hit rate outperforming the average, one could even conclude that Bitcoin halving is more bullish for SPX than for Bitcoin itself!

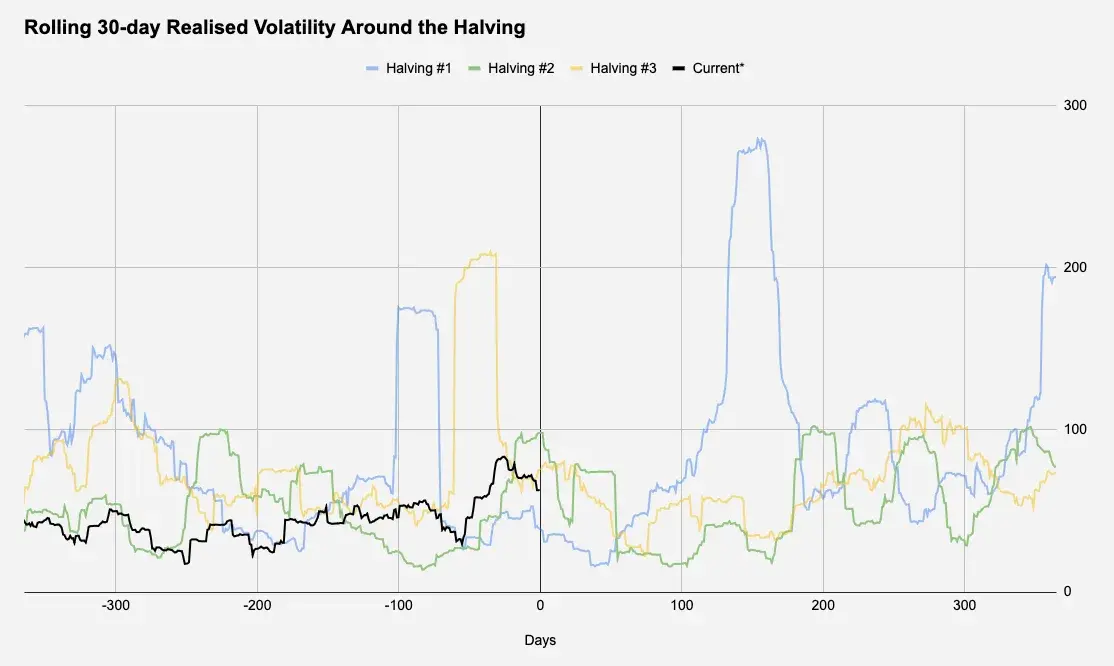

For those interested in volatility, there is no apparent relationship with the halving date or period. Figure 4 examines the realized volatility 30 days before and after the halving date:

Figure 4: BTC Volatility Shows No Pattern

2024 Halving Themes

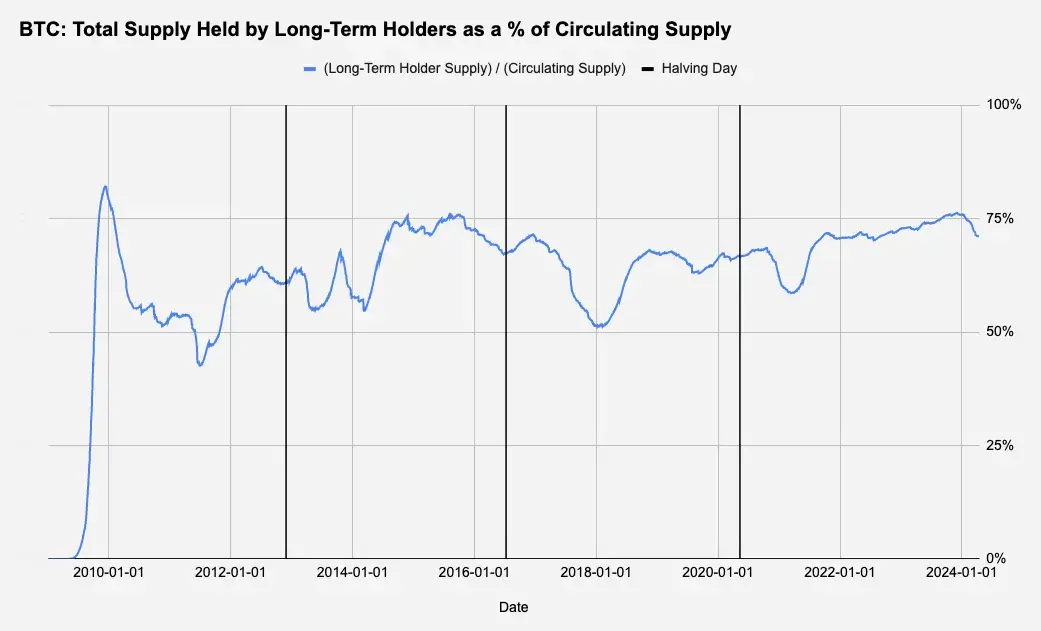

1: Long-term Holders

Here, we look at the total amount of BTC held by long-term holders, adjusted for BTC supply. Given that the circulating supply of BTC will increase before reaching the hard-coded cap of 21 million Bitcoins, we divide the amount held by long-term holders by the circulating supply at that time to see the percentage of holdings:

Figure 5: Bitcoin Held by "Long-term Holders"

Although it was less apparent in 2020, Figure 5 suggests that long-term holders may take profits before the halving, with a drop also occurring in 2024. This selling dynamic is often attributed to miners; as the halving effectively reduces income per block by 50%, miners often sell part of their reserves to upgrade their hardware for more efficient mining when rewards decrease. With only a few days until the 2024 halving, this structural selling pressure may be occurring.

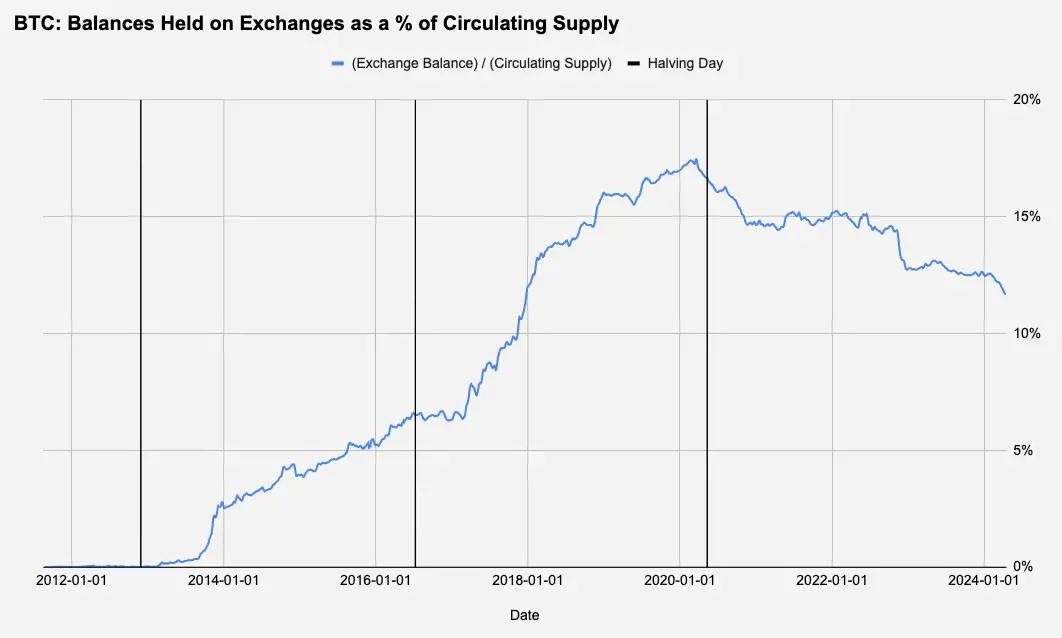

2: Exchange BTC Balances

While exchanges do not make directional bets, we still look at the reserve holdings of exchanges (and possibly their internal market makers) to see if there is any pattern around the halving date:

Figure 6: Bitcoin Held by Cryptocurrency Exchanges

Nothing interesting related to the halving can be observed from Figure 6. The only observable trend is a longer-term trend where exchange balances have experienced accumulation for about six years, with balances steadily declining as the previous bull market began.

3: Macro Context

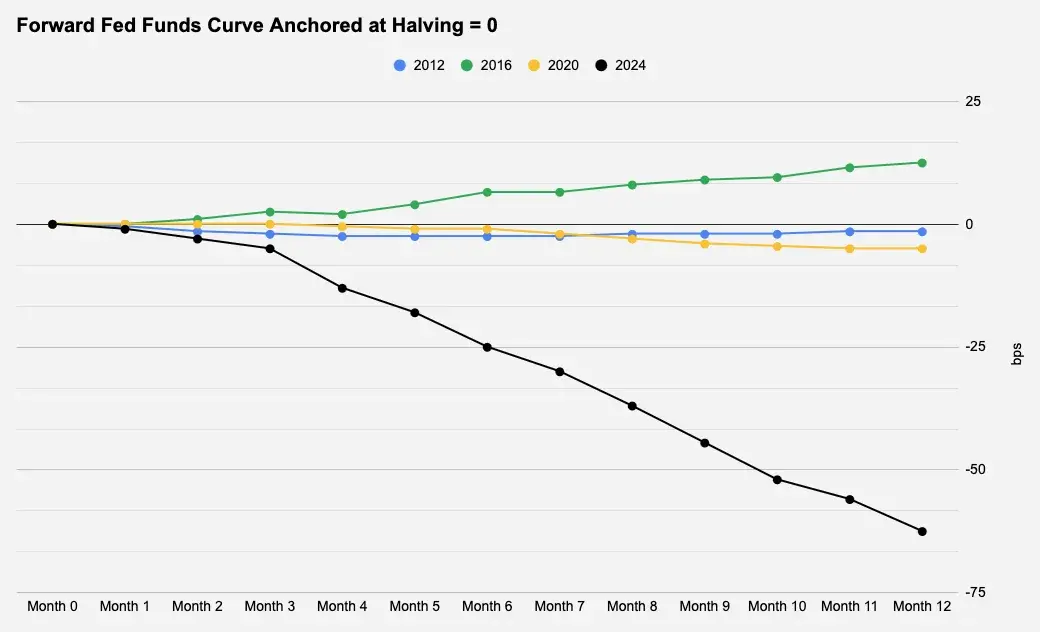

There is often debate about the relevance of macro conditions to Bitcoin, but macro cycles, particularly dollar liquidity (as a function of monetary policy/rates, risk appetite, etc.), remain a driving force for medium to long-term asset prices. With this in mind, we focus on the market pricing of the federal funds rate for the next 12 months around the halving date.

Figure 7: The Federal Reserve at Halving

It is clear that the upcoming 2024 halving is an outlier, with expectations for nearly three rate cuts.

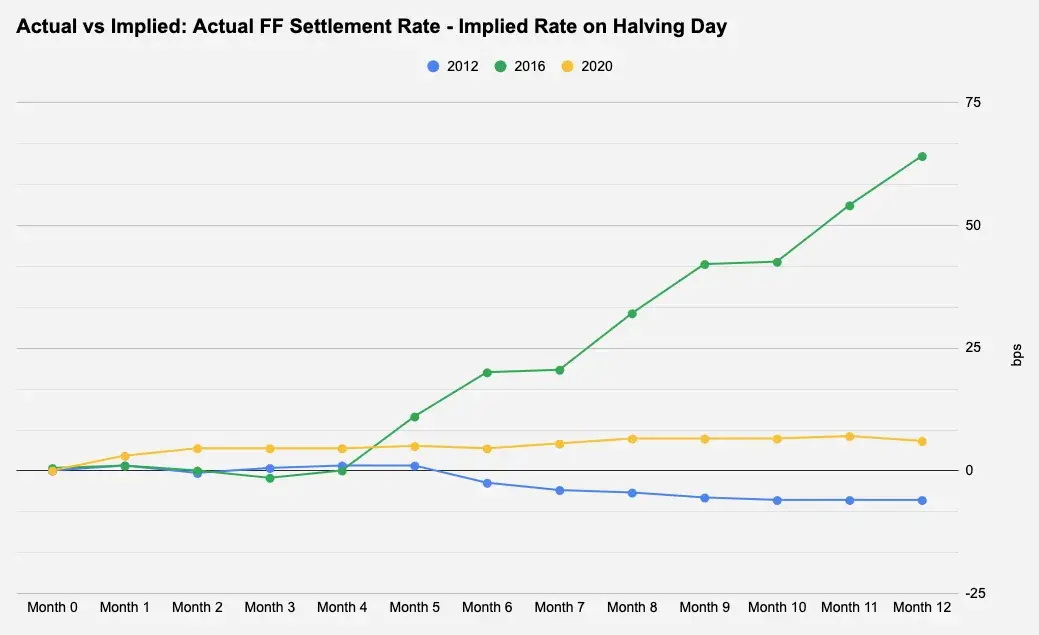

Lowering interest rates is generally bullish for risk assets, but what is often important for price movements is not the already priced-in rates but the magnitude of deviation from market expectations, whether from inflation data or statements from the Federal Reserve Chair. In Figure 8, we compare the actual settlement implied rates on each halving day with market expectations to understand how accurate the forward pricing in Figure 7 is.

Figure 8: Accuracy of Federal Reserve Expectations

The data from 2012 and 2020 is quite ordinary, with no more than a 10 basis point deviation from the initially expected range, but 2016 is worth studying because the Federal Reserve raised rates twice, which had not been priced in by the second halving. Interestingly, Figures 1 and 2 show that the 12 months following the 2016 halving was the worst performance of BTC among the three previous halvings and the only time its performance fell below the one-year average return. Therefore, with more than two rate adjustments anticipated for the next 12 months, a more significant driver for BTC post-halving may be the ongoing inflation in the U.S. or any other factors that might encourage the Federal Reserve to remain unchanged rather than cut rates.

Conclusion

We briefly explored the unique macro context of the upcoming halving, but other considerations not mentioned in this report revolve around the recent launch of spot BTC ETFs. Given that BTC has attracted all the attention recently, this is undoubtedly the most anticipated halving to date, and the general institutional introduction of BTC has brought new participants that could change the dynamics of supply, demand, and price behavior. Notably, the newly launched ETFs hold over 4.1% of the circulating supply of BTC, while MicroStrategy holds over 1%. Given that there have only been three previous halvings, drawing statistically significant conclusions from past performance to determine whether this is a tradeable event is challenging. However, structurally speaking, from a supply perspective, this is undoubtedly a bullish event.

Risk warning

Risk warning Risk warning

Risk warning