Analyzing the Crypto Cycle: The Bull Market Begins with Institutional Capital Flowing from the Top Down, Beware of Market Reversal Caused by Excessive Euphoria

The collective always lacks foresight, and the momentum of the group hinders individual decision-making.

The collective always lacks foresight, and the momentum of the group hinders individual decision-making.Original Title: “But They Won't Trap Me”

Written by: MATTI

Translated by: ShenChao TechFlow

In hindsight, things may seem inevitable. Sometimes, the difference between inevitability and impossibility is small, perhaps just a few weeks of price action. I want to explore this difference from a hindsight perspective.

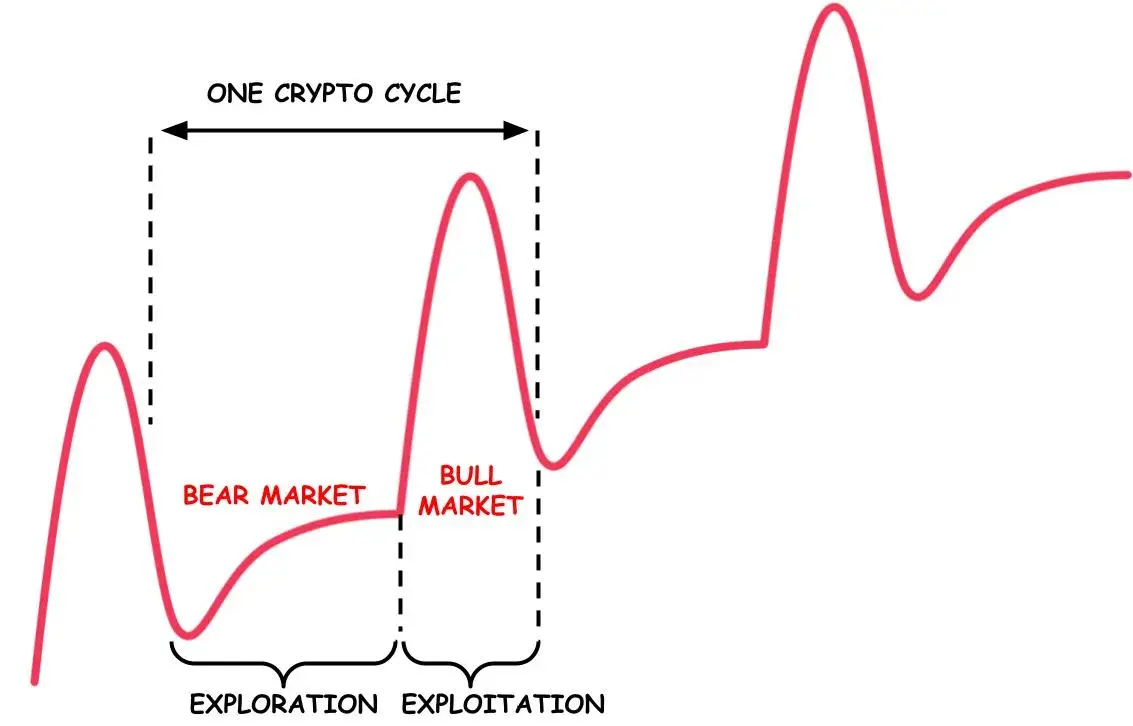

Two interacting forces formed the cryptocurrency bull market. Resources (capital) flowed from the top down, while products (ideas) flowed from the bottom up. Combining capital with the right ideas can spark innovation, or at least ignite imagination. At this point, exploration transforms into development.

I will share personal anecdotes from the past few years and then discuss the differences between the exploration and development phases of the cycle. As a conclusion, I will summarize possible future scenarios and offer personal comments.

Resources

In the cryptocurrency space, we have experienced a rapid shift from extreme fear to extreme indifference and then to high expectations. All of this occurred in about 12 months. It can be said that the collective always lacks foresight, but the momentum of the group hinders individual decision-making.

After the extreme panic at the end of 2022, most investors were reluctant to deploy capital, and some had completely given up on cryptocurrency. During the extreme indifference of the summer of 2023, many were unwilling to invest due to capital constraints, as macroeconomic momentum painted a bleak outlook.

With the market rallying at the end of 2023, driven by the tone of ETFs and top-down narratives like Solana, the market soared. When talking to many fellow investors in 2023, almost no one expressed optimism. Among those with resources, very few were actually deploying them.

In the cryptocurrency space, whether in liquid funds or venture capital, many investors were caught off guard by the sudden bullish market, at least expecting another six months of winter. The prospect of a gold bull market seemed to happen overnight, leaving investors confused.

Those with liquid funds were scrambling to buy tokens they should have purchased a year ago, while venture capitalists with resources were chasing the hottest stories—mainly L2 and AI projects. We can judge this by observing the following aspects:

Oversubscription

KOL/angel round only

Intense price competition

Shares quickly sold out

Those who felt over-allocated in December 2022 felt under-allocated by March 2024. The capital inflow into liquidity funds accelerated at the end of 2023, followed by venture funds (a few still with disposable resources) raising more capital demands.

Based on my personal experience raising venture capital crypto funds from mid-2023 to now, it is almost impossible to find LPs willing to allocate positively. In terms of fund-of-funds (FoF), most funds are struggling to raise capital, delaying capital deployment each quarter, while a few resource-rich funds opted for larger companies.

In the summer of 2023, one partner from a large FoF expressed their frustration over every $500,000 check. Another FoF privately revealed that they had communicated with about 100 cryptocurrency venture capital funds that raised funds in 2023 (I can't even name that many), but allocated to none. This is not just a cryptocurrency phenomenon, as venture capital overall has become dry across various sectors.

However, for cryptocurrency, there is an additional micro crisis—FTX—on top of the overall macro collapse. Shortly before the FTX collapse, I spoke with a U.S. FoF that stated they had committed tens of millions of dollars to cryptocurrency managers, but the FoF itself wouldn't start fundraising until the end of 2022. I have yet to hear of their actual successful fundraising. When cryptocurrency funds came, many LPs found themselves unable to fulfill their capital commitments.

The FTX situation also delayed new capital entering the cryptocurrency space, causing many smaller and larger family offices and funds eager for cryptocurrency investments to lose interest. Few investors could truly think independently, which is why we have both euphoria and disenchantment.

However, comparing the cryptocurrency winters of 2018 and 2022/23, the result is that traditional finance has greatly increased its confidence in cryptocurrency. In fact, before FTX, I had spoken with almost everyone in traditional finance, and those who had not ventured into or were only marginally involved in cryptocurrency believed that cryptocurrency would stay. That was absolutely not the case in 2018.

In summary, from my limited personal experience, venture capital and liquidity allocators have been marginalized by the rapid changes in sentiment. This means that a funnel has been created around existing narratives, and the market is accelerating.

The bull market catalyst is the flow of funds into ETFs and liquid cryptocurrency funds, repricing the secondary market (which is already happening). In the primary market, I expect resources flowing into cryptocurrency venture capital to increase in the second half of 2024, but mainly in 2025, thus driving an already competitive primary market.

Ideas

Due to the collapse of Luna and the FTX crash, the bear market quickly turned into a cleansing, with sellers rapidly offloading, while those still in the game remained shocked. If they were to allocate assets, they would feel uneasy. The influx of founders decreased, as many turned their attention to the AI craze.

The narrative reset came quickly. The disillusionment phase of cryptocurrency helped explore new ideas and select the best ones for development when the narrative shifted to euphoria. The exploration phase laid the groundwork for the later imitation race. Exploration is about searching for the legendary "innovation trigger."

Throughout 2023, trading flows were the most diverse, as there was no particularly strong narrative. There were some clusters, such as intent, ZK, rollup/second layer, ordinals, etc., along with some other aspects, mainly in infrastructure.

Founders were effectively forced to think for a while before exciting venture capitalists. At this point, both founders and investors were eager to explore. This is when cryptocurrency is at its most creatively vibrant. Marginal improvements on hot topics do not yield significant results, as there are not enough hot topics during the bear market, and excitement does not last long in a bear market.

As the market soared at the end of 2023, the search for the "innovation trigger" ended—the cards had been played. I believe that the "Overton window" of this bull market has opened. However, this does not mean that the best-performing companies have emerged and can be invested in.

(Note: The Overton window is a theory about the range of policies that are acceptable to the majority of people in politics over a period of time.)

Uniswap may be one of the most replicated products from the last cycle, but the second most replicated product, the progenitor of DeFi 2.0, OlympusDAO, only emerged a few months after the DeFi summer. There is still room for innovation, but it must be done by leveraging existing narratives.

The most promising narratives we see today are:

Cryptocurrency AI/agents

Re-staking

Second layer

ZK

Infrastructure

DeSci

SocialFi/Web3 social

These are quite uncertain categories, more like vague identifiers of what people are building. Many products may be combinations of two or more of the above categories. The winners will be those who master traditional tools for user acquisition: yield and leverage. "Digital up" is always the best user experience.

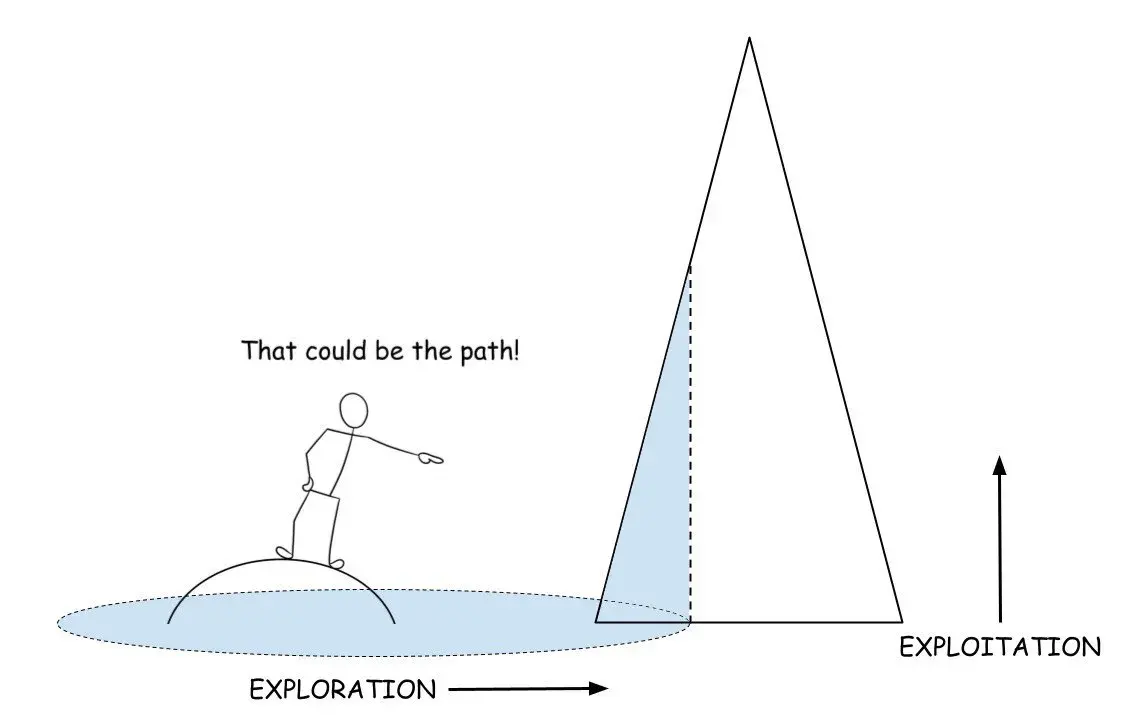

Exploration vs. Exploitation

Let’s briefly discuss the game theory of exploration/exploitation. The cryptocurrency cycle has two behaviors. One is that people are forced to come up with seemingly new things, and the other is that people exploit these new things through exaggerated narratives.

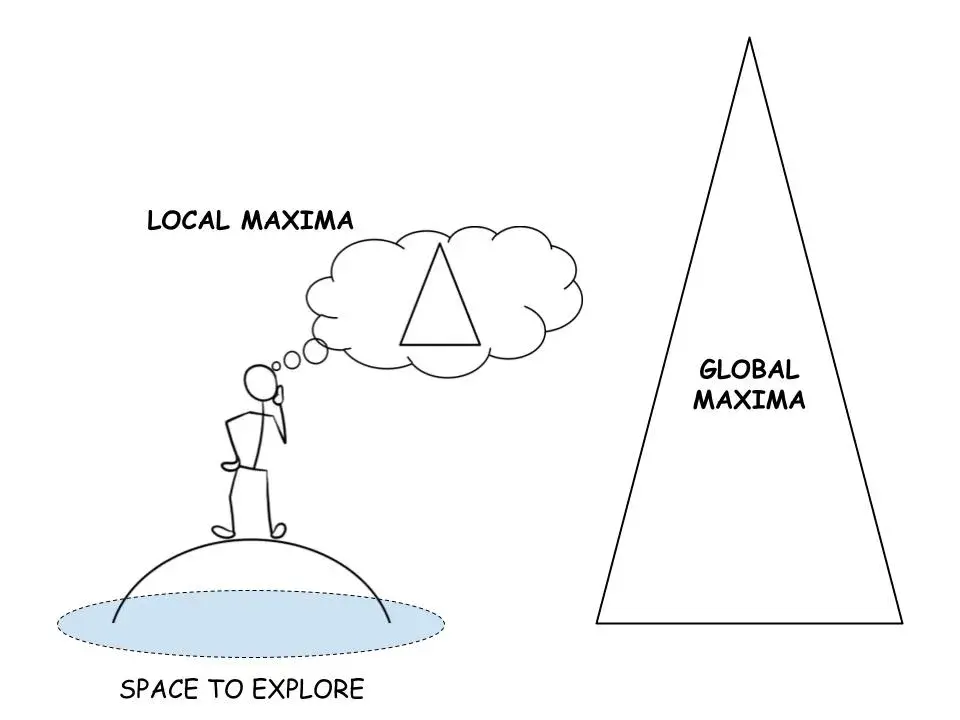

In a bear market, we fall into a local maximum. With the old narratives having collapsed and unable to support the market further, founders are forced to explore, while investors reluctantly follow. The "innovation trigger" is the foothill of the new global maximum. This becomes the target for exploration, around which new narratives can be built.

As previous ideas become dead ends, founders return to the starting point, expanding the exploration space. The longer prices continue to fall or stagnate, the greater the motivation to abandon the safety of old narratives and explore larger potential novelty areas.

At some point, explorers will set their sights on the foothills that may become the new global maximum. Typically, the formation of the foothills is a function of novelty and price recovery. While this may be more of a correlation than a causation—it is enough to begin the climb and form an overall narrative.

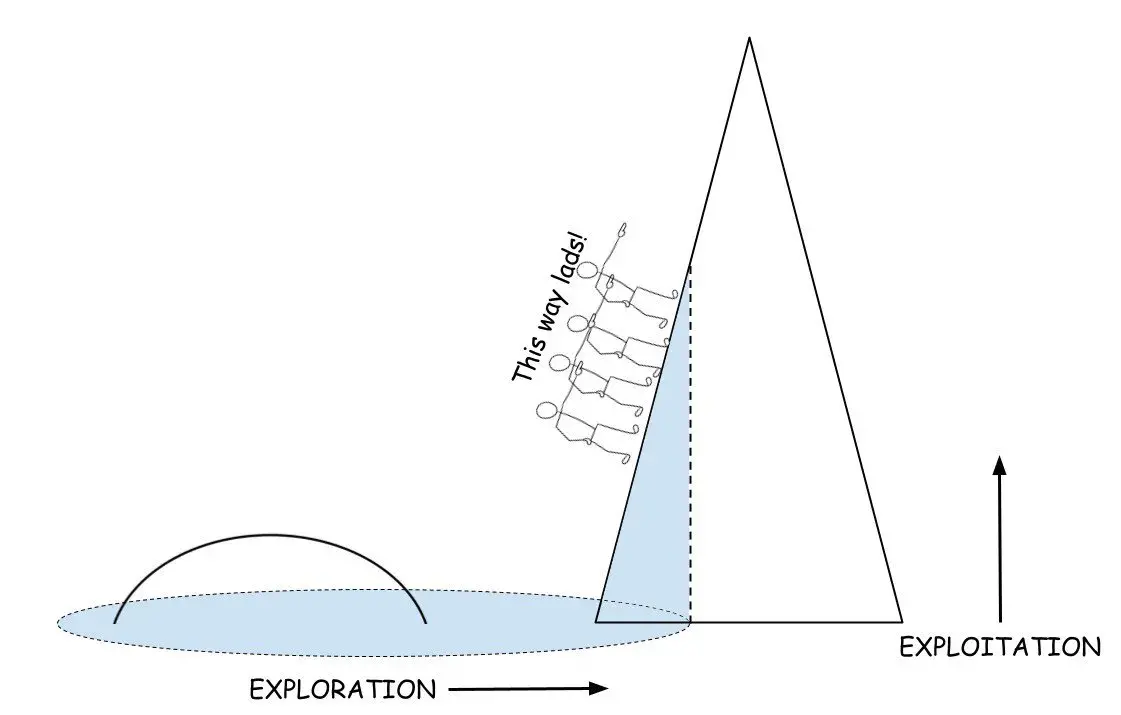

The ascent signifies the end of the exploration phase, as we establish a base camp and begin to exploit market momentum. At this point, the reflective relationship between novelty and price behavior begins to push the global maximum higher. Price becomes a leading indicator of adoption.

As of March 2024, we seem to have found the foothills, with everyone scrambling to climb new peaks, as they appear to offer better returns than further exploration.

What's Next?

The exploration phase has ended, and considering that most investors are passive, they will not waste time exploring but will double down, as they must make up for lost ground. Each round of financing begins to receive oversubscription, indicating that investors are in full exploitation mode.

2024 will resemble 2020 and 2016, mostly an internally driven year. The active retail base participating in cryptocurrency is already higher than in 2020, meaning we are starting from a higher baseline. Although there has been little innovation over the past two years, we are leveraging resources.

Developers focus on resources, while explorers focus on ideas. There is a subtle distinction between being an investor and "doing investment business" (investors vs. allocators).

Development strategies are also a function of scale. Most funds with abundant resources only engage in development, as innovation or exploration does not require as much capital as competing on the development axis. There is far more dumb money than outsiders believe and insiders admit.

Given that during any frenzy, a large amount of capital is seeking scarce genius, many will compromise to achieve their deployment goals. Or as ++Hobart and Huber++ put it: "While genius is scarce, the demand for credulousness is always met through a plethora of fraud." People's expectations are inflated, founders are incentivized to engage in resource wars, and the yields of exotic varieties are subsidized.

As the VC fundraising machine has begun to operate, top-down capital flows will gradually increase. Early internal rounds of competition mean that before retail floods in, insider and institutional funds will support the market. Moreover, retail is not a homogeneous group but a variety of adoption waves throughout the cycle.

Those who were most fearful are transforming into fearless bulls. But this is just the other side of insecurity. Remember, insecurity is the mother of greed, and there is a lot of insecurity in the market today.

The fact is that there has not been much innovation in cryptocurrency over the past two years, making it difficult to view this bull market as an independent phenomenon from the last one. Thematically, it seems to be a continuation of the last cycle, but on a larger scale, as yield arbitrage becomes more profitable and the doors for institutions open with the advent of ETFs.

For an uncontrolled frenzy, imaginative triggers are more effective than innovation triggers. Reflexivity is released again, and most people in the space are supporting kayfabe. The role of credit has yet to play out in this cycle.

(Note: The term "kayfabe" has evolved into a kind of jargon used to maintain this "reality" in the direct or indirect presence of the public.)

A few months ago, I wrote in an investor letter:

Every round of the cryptocurrency cycle tends to be destroyed by its excessive fundamentals. The 2017 cycle was destroyed by an obsession with ICOs, and the 2021 cycle was destroyed by the excessive leverage of the DeFi narrative; each frenzy's fundamental principle is a mimetic struggle for immediate wealth.

**This rise began with the top-down flow of institutional capital. There are no truly shiny new things. The foundation for the impending potential frenzy is the inflow of institutional funds (and ** credit ?) and the price trends themselves. Will this cycle be destroyed by exposure to excessive institutional exposure? Let’s wait and see.