Traditional institutions entering Bitcoin, what is the appropriate position size?

Best strategy: Allocate 3% to 5% of total investment to Bitcoin.

Best strategy: Allocate 3% to 5% of total investment to Bitcoin.Written by: Crypto Research

Compiled by: Luffy, Foresight News

In the fast-evolving world of investments, diversification has always been a key strategy for reducing risk and enhancing returns. With the emergence of cryptocurrencies, particularly Bitcoin, investors have found a new asset class to add to their portfolios. This article delves into the impact of incorporating Bitcoin into a traditional 60/40 stock and bond portfolio.

Through a detailed analysis of various digital metrics, we explore how different levels of Bitcoin allocation affect the overall performance, risk, and return of the portfolio. From gradually increasing positions to significant allocations, we reveal the nuanced relationship between risk and return in the context of Bitcoin investment.

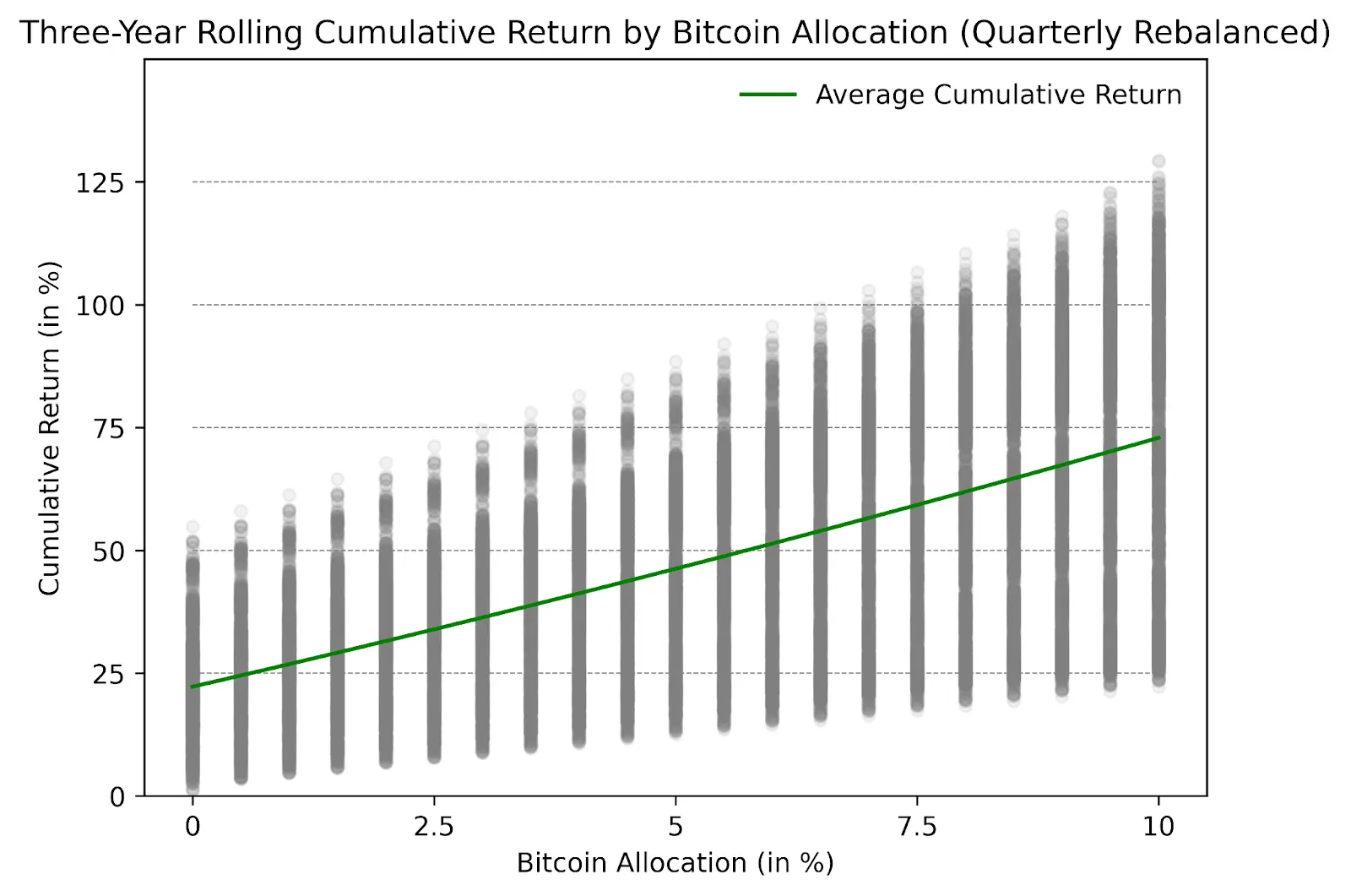

The first column on the left side of the chart below represents the scenario when no Bitcoin is allocated in the portfolio, while the subsequent columns show what happens when Bitcoin holdings are gradually increased (up to 10%). These lines do not represent changes over time but simply indicate how much Bitcoin you hold. Notably, historical data shows that the more Bitcoin you allocate, the higher the return rate.

Figure 1: Three-Year Rolling Cumulative Returns of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

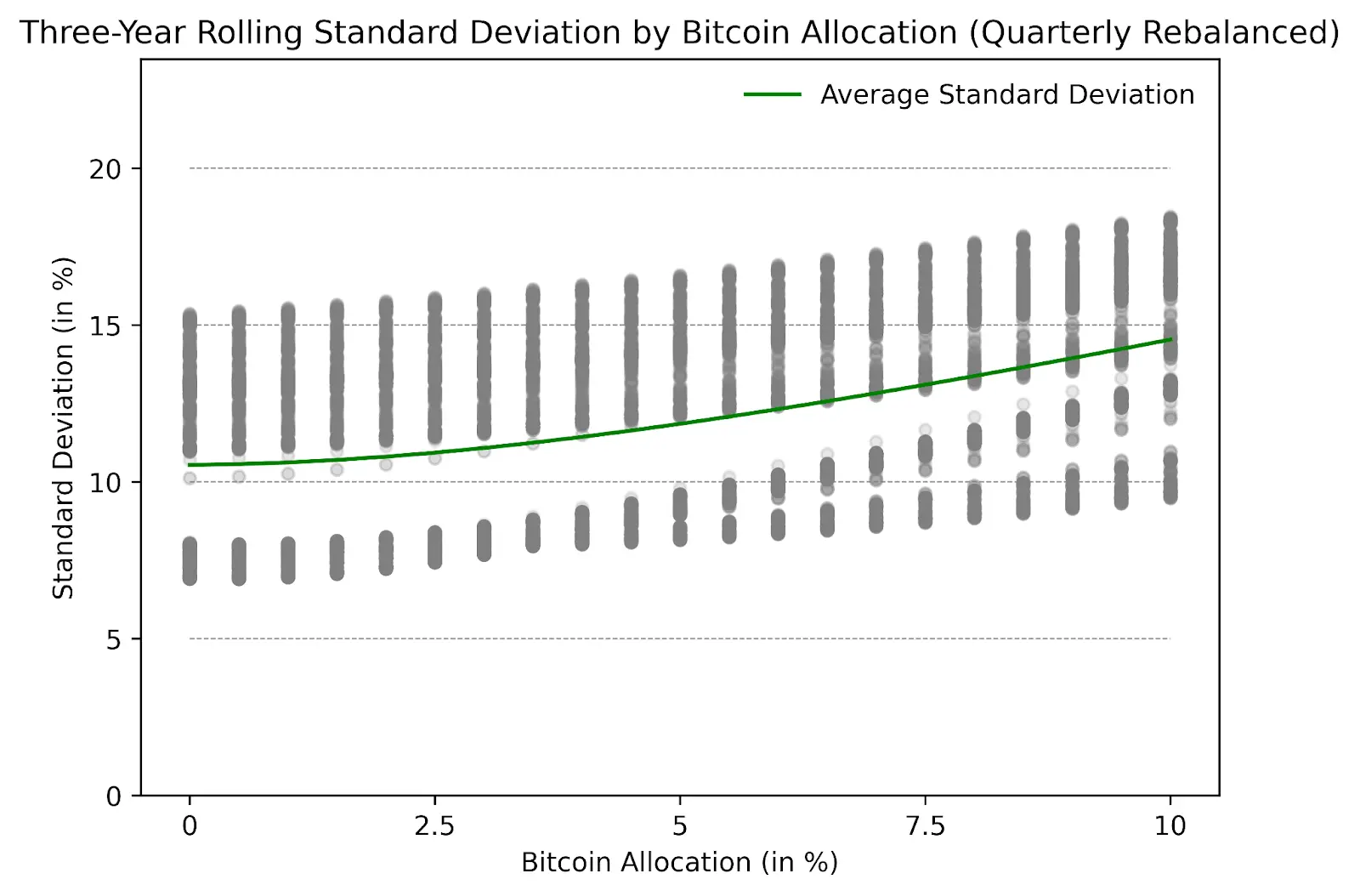

While adding Bitcoin to a 60/40 stock and bond portfolio increases cumulative returns, there is a caveat: it may also increase uncertainty and risk. Figure 2 illustrates the change in volatility after allocating Bitcoin. Although risk increases, it does not do so in a linear fashion. Instead, the line has a curvature. This means that if you only add a small amount of Bitcoin, say between 0.5% and 2%, it won't significantly increase your investment risk. However, as you add more Bitcoin, things quickly become unpredictable.

Figure 2: Three-Year Rolling Standard Deviation of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

Figure 2: Three-Year Rolling Standard Deviation of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

In Figure 3, we combine the information from Figure 1 to examine the Sharpe ratio of the portfolio. The shape of the graph is quite interesting: it rises rapidly at first and then levels off as you invest more Bitcoin. The chart indicates that adding some Bitcoin to your investment typically means you will receive higher returns to compensate for the risk you are taking on. However, there is no free lunch: once you start adding more Bitcoin, particularly around 5% of the total investment, the increase in risk becomes more pronounced than the benefits. Therefore, allocating a small amount of Bitcoin may be beneficial, but beyond a certain point, the cost of allocating more Bitcoin is a significant increase in risk. Based on historical returns and mean-variance optimization, the optimal allocation of Bitcoin to the portfolio is between 3% and 5%.

Figure 3: Three-Year Rolling Sharpe Ratio of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

Figure 3: Three-Year Rolling Sharpe Ratio of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

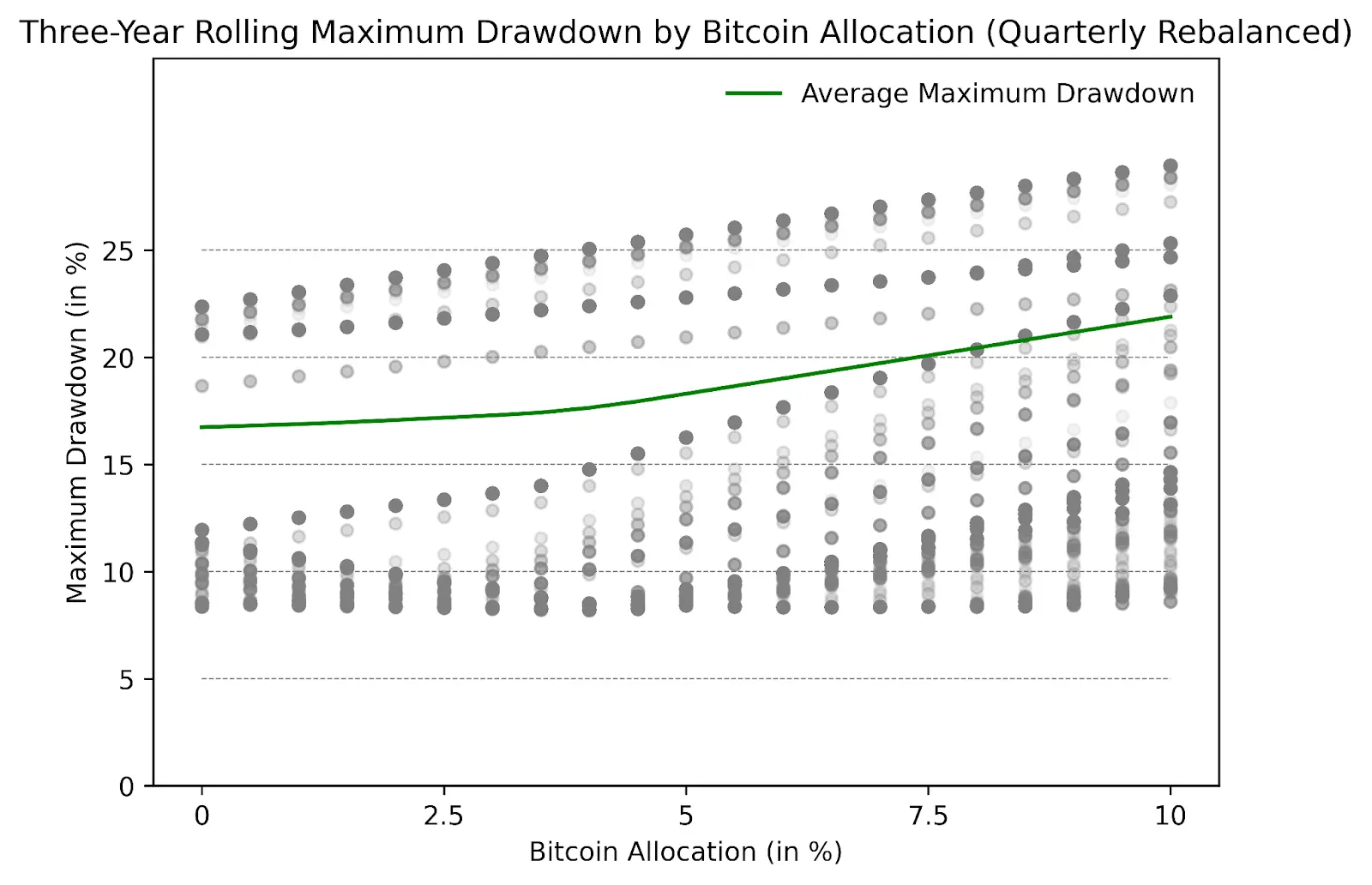

Figure 4 shows how different amounts of Bitcoin affect the "maximum drawdown" of the investment value. Similar to the Sharpe ratio, the green line on the chart indicates that allocating a small amount of Bitcoin (e.g., 0.5% to 4.5%) in a 60/40 stock and bond portfolio does not significantly impact the maximum drawdown over three years. If the allocation exceeds 5%, the impact on maximum drawdown begins to increase substantially. For risk-averse institutional investors, keeping Bitcoin holdings at 5% or below of the total investment may be the best choice from a risk-adjusted and maximum drawdown perspective.

Figure 4: Three-Year Rolling Maximum Drawdown of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

Figure 4: Three-Year Rolling Maximum Drawdown of Bitcoin Allocation (Quarterly Rebalanced), Source: Cointelegraph Research

In conclusion, exploring Bitcoin as part of a diversified portfolio reveals the delicate balance between risk and return. The results presented through various data emphasize the potential for enhancing cumulative returns by strategically increasing Bitcoin holdings, accompanied by an increase in volatility. Based on historical data and mean-variance optimization, the best strategy is to allocate 3% to 5% of the total investment to Bitcoin.

Exceeding this threshold makes the risk-return trade-off unfavorable, highlighting the importance of cautious and informed decision-making when incorporating Bitcoin into investment strategies.