Staking, Restaking and LRTfi: Composable Capital Efficiency and Neutrality

The combinable capital efficiency has driven the development of Staking and Restaking at both primary and secondary levels, while tokens like LST have enabled the deep application of staking yields in DeFi.

The combinable capital efficiency has driven the development of Staking and Restaking at both primary and secondary levels, while tokens like LST have enabled the deep application of staking yields in DeFi.Author: LongHash Ventures

Translator: Baihua Blockchain

Key points of this article:

- Composable capital efficiency and staking as the crypto-native benchmark interest rate

- Staking, Restaking, and LRTfi

- Addressing centralization and externality issues in Staking and Restaking

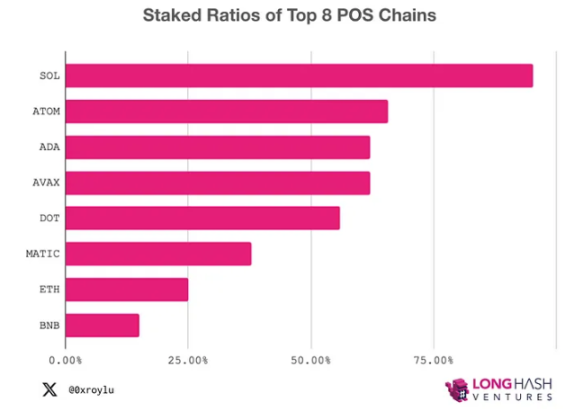

In our research, the main layers of Ethereum, Solana, and Polygon are maturing, while the staking mechanisms of Bitcoin and Cosmos are also evolving. In Ethereum, there are two potential outcomes: if Ethereum's value is maintained, it may lead to an oligopoly, with top participants holding nearly 33% of the share but not exceeding that ratio; or, if Ethereum's value is not maintained, it may result in the establishment of LST (Layer 2 networks). In Cosmos, the ICS (Inter-Chain Standard) is in its early stages, while Solana's staking rate has reached 90%.

The secondary layer of restaking has sparked a competition for high yields, with capital flowing into projects with the highest returns, particularly into LRT (Layer 2 Staking Tokens) pools. As the first Layer 2 network to adopt a staking mechanism, Blast and Manta have made waves globally, instantly attracting over $1 billion in total locked value. However, in a scenario of ample supply and strong demand, the expected returns from AVS (Automated Vault Strategies) and restaking Layer 2 networks remain unclear. Additionally, the restaking mechanisms in Bitcoin, Cosmos, and Solana are still in their early stages.

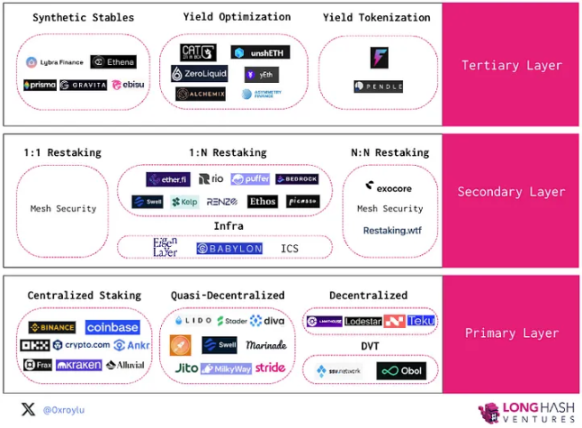

At the third layer, synthetic stablecoins, yield optimization, and yield tokenization are aimed at increasing innovative diversity. At this layer, capital efficiency and risk surpass composability. The key success factor at this level is achieving the broadest composability with the least risk.

1. Composable Capital Efficiency and Staking as the Crypto-Native Benchmark Interest Rate

Composability is a hallmark of Web3, characterized by frictionless, low minimum requirements, and self-custody. In contrast, in traditional finance, yield stacking faces high friction. For example, borrowing against government bonds incurs multiple friction points, such as third-party custodians, case-by-case assessments of LTV ratios, and high minimum requirements to prove the labor costs involved, to name a few.

The emergence of LST (Layer 2 stablecoins) unlocks the composability between consensus layer yields and execution layer DeFi activities. This composability made the DeFi summer of 2020 possible. Time flies, and three years later, composability now feels so natural that it is almost taken for granted. We have become accustomed to frictionless yield stacking to enhance capital efficiency. For instance, we expect to stack yields by minting LP Tokens for staking (superliquid staking) or minting LST to deposit LP positions.

Self-custody, low minimum requirements, and frictionlessness—these features are unique to Web3 and highlight the potential for broader efficiency improvements in financial markets. Imagine if you could tokenize your stock holdings and use them to participate in an LP on a stock trading platform. Imagine if you could tokenize your real estate equity and easily use it for restaking yields. Through LSTfi, we can glimpse what composability means for traditional finance.

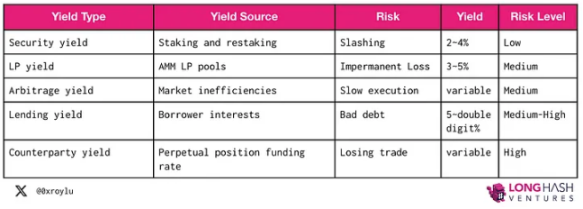

Fundamentally, there are five types of yield sources in the crypto space, and they are stackable, in other words, composable. An IOUToken from one yield source can be used as an input token for another yield source.

Of course, risk and return go hand in hand. Among these five basic yields, staking yields are the safest. Since Ethereum began staking, only 226 out of 959,000 node operators have been penalized. On the other hand, while sovereign bonds are often touted as the lowest-risk investment, there have been recent bond defaults in Italy, Spain, Portugal, Ireland, and Greece (not to mention the continuous defaults of Venezuela and Ecuador). Even the gold standard U.S. bonds "defaulted" when they abandoned the gold standard in the 1930s to print money without restriction to repay debts. Sovereign bond defaults relate to a country's ability to repay its debts. Its risk level is more akin to the risk of "substitute yields" rather than "staking yields." Sovereign bond yields are based on expectations of future debt repayment, while staking yields are related to current network usage levels.

For this reason, we believe that staking is the benchmark interest rate in the crypto space.

Above staking is the capital efficiency engine driving the yield stacking rocket. We are beginning to see some innovations, such as L2 networks with staking guarantees like Blast and Manta, cross-domain restaking similar to Picasso and Babylon, and LST loops like Gravita.

The composability characteristics of LST will drive further innovation in yield stacking design.

2. Staking, Restaking, and LSTfi/LRTfi

Staking is the cornerstone of security for POS chains and serves as the risk-free benchmark interest rate in Web3.

Justin Drake attributes ETH to two purposes: economic security and economic bandwidth. By combining with various DeFi and restaking activities, LST and LRT allow the same ETH to participate in both purposes simultaneously.

In terms of economic security, PoS chains must protect decentralization and neutrality to mitigate potential collusion. Designing protocols in game theory to maintain decentralization and neutrality is a balancing act. We will soon return to this tension.

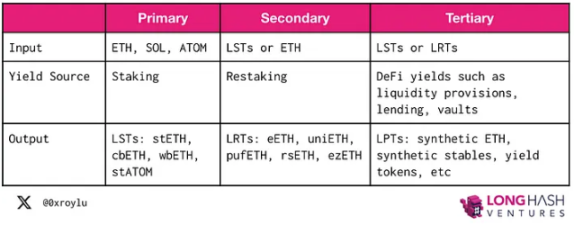

First, let’s use Ethereum as an example of a PoS chain to understand this stacking process. The main layer allows users to stake their ETH and earn LSTs like stETH, cbETH, wbETH, and rETH. In the secondary layer, LST or ETH can be restaked to provide security for other staking services and earn LRTs like eETH, uniETH, and pufETH. Then, the third layer combines LST and LRT with various DeFi activities for yield stacking.

To understand the incentive mechanisms driving adoption, we answer three questions:

- Which strategy combination can generate the highest yield? This involves capital efficiency.

- Which output token can achieve the deepest liquidity and participate in the broadest DeFi activities? This involves composability.

- Which strategy is the safest yield source? This involves risk mitigation.

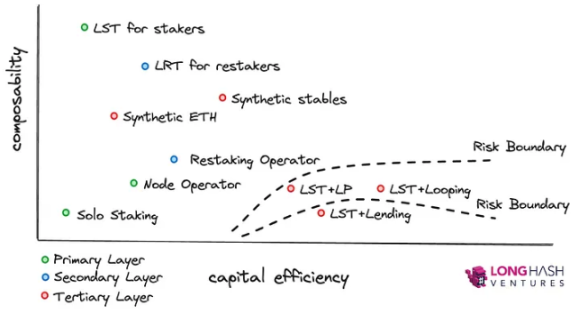

Thus, composability and capital efficiency are the primary drivers of adoption, while risk serves as a boundary condition limiting the choice set.

3. Main Layer - Staking

In the main layer, validators deposit native tokens, such as ETH, ATOM, and SOL, to secure the PoS network and earn transaction fees as rewards.

Since staking is the lowest-risk yield generation form in the crypto space, over time, we expect Ethereum (with a staking rate of 23%) to catch up with Solana (with a staking rate of 90%) and Atom (with a staking rate of 70%), representing a market expansion of hundreds of billions to trillions.

Staking can be categorized into three types: centralized, quasi-decentralized, and decentralized. Centralized and quasi-decentralized staking trade off convenience and composability for custodial transactions. Decentralized staking, or independent staking, is the safest for protocols but is difficult to maintain and lacks composability. In theory, self-custody nodes could also issue LSTs, but due to a lack of composability, no rational thinker would purchase them.

1) Issuing Collateral

In ordinary independent staking, validators create two pairs of keys, one as the validator key and one as the withdrawal key, and then send 32 ETH to the Ethereum 1.0 deposit smart contract. The base fee is burned, and transaction tips are sent to the validators. Only 8 validators per period, or 1,800 validators per day, can be activated.

Staking pools like Rocket Pool, Diva, and Swell allow independent node operators to support pools composed of stakers' deposits. From the operator's perspective, the lower the collateral, the higher the capital efficiency, as they can earn a portion of the commission from the deposited ETH. Essentially, lowering collateral requirements can provide greater leverage.

- Rocket Pool: 8 ETH collateral

- Stader: 4 ETH collateral

- Puffer: 1 ETH collateral

It is estimated that node operators can earn up to 6-7% ETH rewards and up to 7.39% staking pool token rewards.

On Polygon, validators need to obtain permission. Validators must apply to join the validator set, and can only join when an approved validator unbinds. On Solana, validators can join without permission, and the Solana Foundation provides optional clusters for validators. Solana also officially tracks the number of minority validators holding more than 33% of staked SOL.

In centralized exchange (CEX) staking, the mechanism for issuing collateral is opaque. Retail stakers can provide all the collateral, while centralized node operators can pass on all potential penalties to retail stakers. However, stakers also automatically benefit from the smoothing effect, which usually yields higher returns than independent staking.

2) Earning Rewards

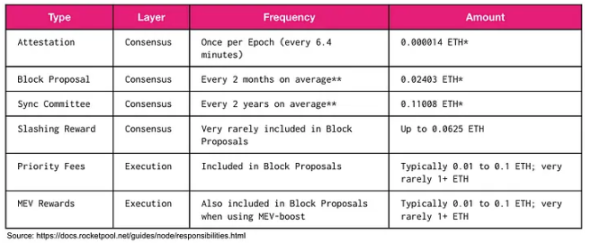

Every 2 to 3 days, the Ethereum beacon chain settles validators and distributes rewards. In addition to the consensus layer, validators can also earn execution layer rewards through priority fees and MEV. Protocols like Jito in Solana leverage MEV to enhance the yields of their LSTs.

MEV increases the redistribution of MEV from block producers to validators, who can then distribute the rewards to stakers. Ultimately, MEV burn may be implemented to return value to ETH holders. Essentially, the redistribution of MEV revolves around the philosophical issue of fairness. However, currently, MEV can be used to increase staking rewards.

Validator rewards are typically volatile. Due to the inherent randomness of validator selection, rewards may be uneven. In Ethereum, deterministic randomness is used to select the next validator, involving the hash and seed of the previous block.

To this end, Rocket Pool offers a smoothing pool based on an opt-in model. The smoothing pool accumulates rewards for validators that opt in. As a rule of thumb, if the number of small pools of validators is less than the number of nodes in the smoothing pool, it is more likely to earn greater rewards from the smoothing pool. For projects like Lido, the smoothing function has been embedded in the smart contract.

In centralized exchanges (CEX), smoothing is done automatically, and stakers can expect stable returns over time.

3) Penalties

Penalties are very rare events. Since Ethereum staking began, only 226 out of 959,000 node operators have been penalized.

Validators may be penalized when they 1) fail to produce a block, or 2) fail to produce attestations within the expected time. The penalty amounts are small. Typically, validators can regain rewards within a few hours equal to their offline time. On the other hand, penalty punishments are more severe.

Penalties occur when one of the following three conditions is met: 1) double signing: signing two different beacon blocks for the same time slot; 2) signature wrapping: signing an attestation around another attestation; 3) double signing: signing two different attestations for the same target. Validators will include evidence of misconduct in one block, socialize with the validator set, and begin penalties after all validators sign that evidence.

In penalty events, the following consequences may occur:

- Initial penalty: 1/32 of the effective balance is slashed

- Correlation penalty: if multiple violations occur in a short time, it may slash up to the effective balance amount. Secondary penalties can prevent collusion.

- Exit: Validators will enter withdrawal status for 8,192 periods (36 days)

DVT (Distributed Validator Technology) aims to reduce penalty risks and enhance the security of staking pools by protecting validators from the risk of failing to produce blocks or attestations. DVT employs distributed key generation (DKG), multiparty computation (MPC), and threshold signature schemes (TSS) on a redundant set of validators.

SSV (Socialized Secure Validation), as part of the DVT network, is a fully open, decentralized, and open-source public good currently being experimented with for protocols like Lido. Obol utilizes Charon as a non-custodial middleware responsible for communication between validator clients and consensus clients. Diva uses its own DVT implementation to support its LST in a permissionless manner, allowing anyone to run a node. Puffer's Secure-Signer is a remote signing tool funded by the Ethereum Foundation, designed to prevent punishable misconduct using Intel SGX. Puffer's Secure-Signer manages validator keys on behalf of the consensus client.

From a capital efficiency perspective, running multiple clients through DVT consumes computational resources. In practical implementation, the same hardware can participate in multiple DVT groups. Importantly, DVT enhances the security of the protocol, so even if one group of node operators goes offline or behaves abnormally, the staking pool can still operate correctly.

Cosmos Interchain Security has an interesting approach to penalties (Proposal #187). Since ICS is still in its early stages, governance votes need to address all potential punishable events. While this aims to prevent any security contagion from consumer chains to the central hub, governance currently still delegates decision-making to human arbitration rather than code.

4) Withdrawals

In Ethereum, four exits are allowed per period. Due to mismatched entry and exit limits, with 8 validators per period and 4 validators for exits, long exit queues may occur. Once a withdrawal is initiated, validators must wait for 256 periods.

In Solana, delegation is established. Standard delegation to staking pools requires a cooldown period for withdrawals. However, liquid staking conducted through staking pools does not require a withdrawal cooldown period.

4. Looking Ahead

As the staking rate of Ethereum increases, with network usage remaining constant, the base yield should gradually approach 1.8%, which is the minimum yield set by the Ethereum Foundation. However, increases in gas fees and MEV may offset this trend to some extent.

Typically, opportunity costs will prompt stakers to stop staking when yields fall below other available yield sources. However, LST (Liquid Staking Tokens) can mitigate opportunity costs, as holders can simultaneously participate in economic security and economic bandwidth. Therefore, even with low returns, stakers are likely to continue depositing and using their LST to participate in DeFi for additional yields.

Due to the decline in Ethereum staking yields, another phenomenon is centralization. Independent stakers will find their yields continuously decreasing, eventually surpassing hardware costs.